HDFC SL Youngstar Super Premium Review (2021)—Should You Buy?

Every parent wants a better future for their child.

It becomes their priority to save, so that they can give their children the best opportunities available in the world.

Many parents realise that investing is the best way to make this happen for their children’s future.

HDFC SL Youngstar Super Premium policy is an investment insurance plan that is “tailor-made” for this purpose. At least that is how it is projected.

Is it true?

Table of Contents:

a) Death Benefit & Payment Preference

b) Maturity Benefits Review: HDFC SL Youngstar Super Premium

- Charges in HDFC SL Youngstar Super Premium

- Exclusions Under HDFC SL Youngstar Super premium

- PROS of HDFC SL YoungStar Super Premium

- CONS of HDFC SL YoungStar Super Premium

- Analysis of HDFC SL YoungStar Super Premium

- HDFC SL YoungStar Super Premium Review Against PPF

- HDFC SL YoungStar Super Premium Review Against ELSS Mutual Fund

- Verdict

- How to surrender HDFC SL YoungStar Super Premium?

- Conclusion

In this article, we are taking on the HDFC SL Youngstar Super Premium Policy review.

This is basically a unit-linked policy specifically designed for the children’s goals and their benefit.

Now, let’s take a look what this policy really has for children and then make a decision.

Features of HDFC SL YoungStar Super Premium

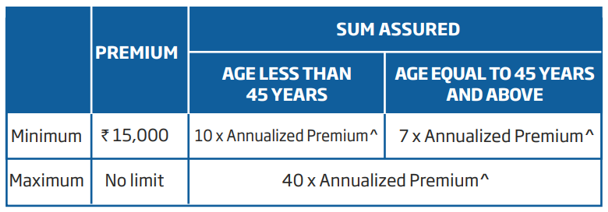

HDFC SL Youngstar super premium can be customized for your child with your own choice of premium, sum assured and plan option.

-

- This policy has 2 plan options – Death Benefit (by choosing life option) and Death Benefit + Critical Illness Benefit (by choosing life and health option).

- There is no ceiling on maximum premium amount. Basically the policyholder has the flexibility to select premium amount.

- The policyholder can choose their premium and level of protection as per the limits mentioned in the below image. The level of premium chosen by the policyholder cannot be changed anytime during the policy term. The premium can be paid only on an annual (yearly) basis.

-

- The policyholder has the flexibility to select tenure which ranges between 10, 15 and 20 years.

- HDFC SL Youngstar super premium child plan has the flexibility to select the sum assured.

- Tax benefits on premium paid under sections 80C and 10(10D) of the Income Tax Act 1961.

- There will be yearly payments to your family in case of your unfortunate demise.

- This policy has flexible Benefit Payment Preferences – Save Benefit or Save-n-Gain Benefit.

- The policyholder can also manage their investment fund(s) either by switching across fund options or re-directing future premiums into a different fund option.

- With a short medical questionnaire and no tedious medical tests, the policyholder can avoid hassles at the time of issuance of policy.

- Pay premiums at your convenience with multiple modes such as -credit card, internet banking, cheque, auto-debit facility.

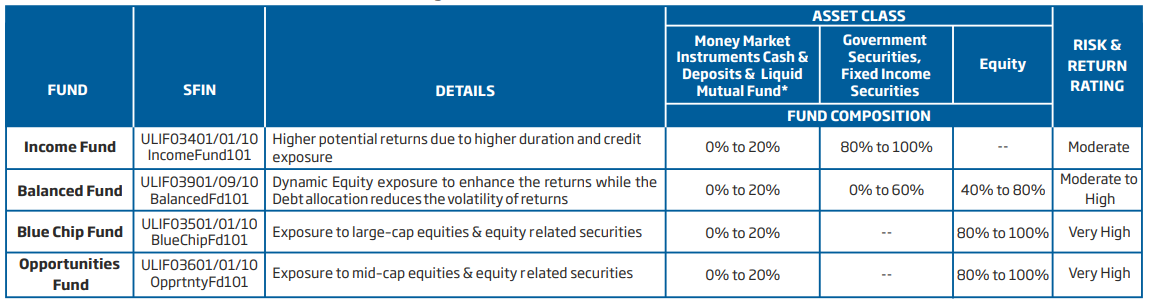

Fund Options of HDFC SL Youngstar Super Premium

HDFC SL Youngstar Super Premium has 4 fund options to choose to match your risk appetite. They are as follows.

Eligibility Conditions of HDFC SL YoungStar Super Premium

HDFC SL Youngstar Super Premium policy comes with 2 plan options.

Each of these plans have different eligibility criteria.

The table below depicts the eligibility criteria of this policy under the 2 plan options.

Benefits Options of HDFC SL YoungStar Super premium

a) Death Benefit & Payment Preference

The policyholder can select from any one below mentioned benefit payment preference. Based on their choice, the beneficiary of the policy will get benefits in case of any claims in future.

i) Save Benefit – In case of the insured person’s death, the insurer will pay the sum assured to the beneficiary (child) and the risk cover will cease.

The family does not need to pay any further premiums. Instead the insurer will pay 100% of all future regular premiums.

And on maturity of the policy, the company will pay the fund value to the beneficiary.

ii) Save-n-Gain Benefit – In case of insured person’s death, the insurer will pay the sum assured to the beneficiary (child) and the risk cover will cease.

The family does not need to pay any further premiums.

In save-n-gain benefit, the company will pay 50% of all future regular premiums towards your policy. And the remaining 50% will be paid to the beneficiary as and when due on an annual basis.

And on maturity the company will pay the fund value to the beneficiary.

b) Maturity Benefits Review of HDFC SL Youngstar Super Premium Benefits

When the policy matures, the risk cover ceases and you can redeem your fund units at the prevailing unit price.

Expected Return of HDFC SL Youngstar Super Premium:

The expected return from HDFC SL Youngstar Super Premium totally depends on the fund performance.

Also, the insurer will levy charges on your premium every year that reduces your investment capital significantly. In turn, it affects your investment return significantly.

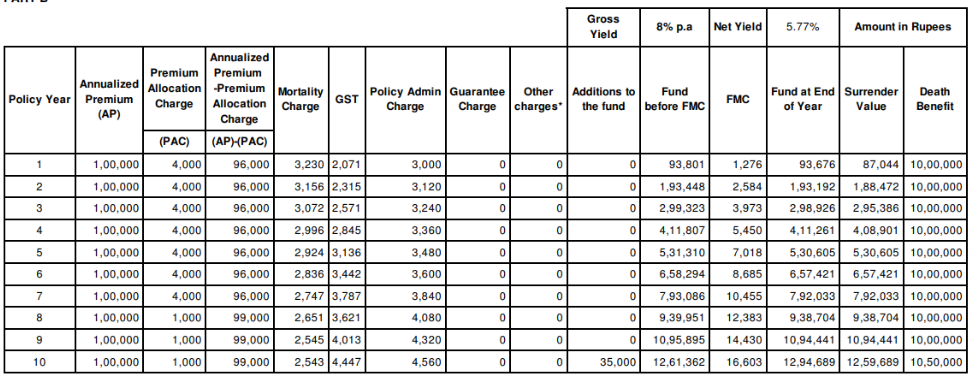

Below is a sample illustration to understand the maturity benefit of HDFC SL Youngstar Super Premium.

In the above table, the policyholder is investing ₹1 Lac annually for 10 years.

On maturity, the policyholder will receive in total ₹ 12,61,362 if the underlying funds earn a return of 8%.

However, 8% p.a. is only the fund’s earning.

After levying the charges and 18% GST on those charges, the policyholder will earn a return at just 5.77% IRR.

A 5.77% IRR for a market linked investment is a very poor return. Even Fixed Deposits offer similar but gives assured returns.

c) Critical Illness Benefits

If the policyholder is diagnosed with any of the critical illness mention in the policy document the benefit will be paid based on the benefit payment preference (i.e. save benefit or save-n-gain benefit) chosen by the policyholder.

d) Partial Withdrawal Options

The policyholder can make lump sum partial withdrawal from their funds only after 5 years of their policy provided the below conditions are met. They are as follows –

- The minimum withdrawal amount cannot be less than Rs 10,000

- After withdrawal and applicable charges, the fund value should not be less than 150% of their original premium.

- The maximum amount that can be withdrawn throughout the policy term has to be 300% of the original regular premium.

Charges in HDFC SL Youngstar Super Premium

Like all other policies, this policy also has some additional charges. Let us see what those charges are.

i) Premium Allocation Charge

The table below shows the premium allocation charges in the HDFC Life SL Youngstar Super Premium policy.

ii) Fund Management Charges (FMC)

The daily unit price includes fund management charge which is 1.35% annually, charged daily, of funds value. The FMC charge for discontinued policy fund is 0.50% per annum.

iii) Policy administration Charge

The policy administration charge of 0.25% per month of the original annual premium will be deducted monthly and will increase by 5% per annum on every policy anniversary, which is subject to a maximum charge of 0.4% of annual premium or ₹ 500 per month, whichever is lower.

This charge will be taken by cancelling units proportionately from each of the funds the policyholder has chosen.

iv) Mortality Charge

The insurer will levy a charge for providing the death or critical illness cover as you chose in your policy.

It includes the sum assured and the value of the future premiums payable.

The amount of the charge taken each month depends on your age and level of cover. This charge will be taken by cancelling units proportionately from each of the fund(s) you have chosen.

v) 18% GST on Policy Charges

Even though HDFC SL Youngstar Super Premium is tax exempted under section 80C, 18% GST is levied on the sum of all the policy charges.

Exclusions under HDFC SL Youngstar Super premium

a) The policyholder will not be eligible for any kind of critical illness benefit if the critical illness has occurred within 6months of the date of commencement or date of issue or date of revival of the policy whichever is later.

b) If the critical illness is caused by self-inflicted injury or attempted suicide, pregnancy, or childbirth or complications, the company will not pay the critical illness benefits.

c) The company will not pay critical illness benefit if the critical illness is caused directly or indirectly by any of the following –

- Alcohol or solvent abuse, or the taking of drugs except under the direction of a registered medical practitioner

- War, invasion, hostilities, revolution, or taking part in a riot or civil commotion.

- Taking part in any flying activity, other than as a passenger in a commercially licensed aircraft.

- Taking part in any act of a criminal nature.

PROS of HDFC SL YoungStar Super Premium

i) Fund Choices & Switching

The policyholder gets an option to change their investment fund choices in two ways. They are as follows –

Switching – The policyholder can move their accumulated funds from one fund to another available fund anytime.

Premium Redirection – The policyholder can pay their future premiums into a different selection of available funds, as per their needs.

However, each of these will incur a charge of ₹250 per request. It is ₹25, if the request is made online, on their official website.

ii) Rider Options For Added Protection

HDFC SL Youngstar Super Premium policy has 2 rider options.

HDFC Life Income Benet on Accidental Disability Rider – A benefit equal to 1% of Rider Sum Assured per month for the next 10 years, in case of an Accidental Total Permanent Disability.

HDFC Life Critical Illness Plus Rider – A lump sum benefit equal to the Rider Sum Assured shall be payable in case you are diagnosed with any of the 19 Critical Illnesses and survive for a period of 30 days following the diagnosis.

Rider options do not carry any maturity benefit in HDFC SL Youngstar Super Premium policy.

CONS of HDFC SL YoungStar Super Premium

i) No Top-up Facility in HDFC SL Youngstar Super Premium

Premium top-up facility is not allowed in this policy under any circumstances.

ii) Loan Option in HDFC SL Youngstar Super Premium Policy

Under any circumstances, the policyholder cannot take loan against this policy.

iii) Hassles in Discontinued Policy Revival

You can revive a discontinued policy within two consecutive years from the date of the first unpaid premium, subject to their underwriting policy.

a) During lock-in period:

All due and unpaid premiums shall be payable without charging any interest or fee.

Policy administration charge and premium allocation charge as applicable during the discontinuance period shall be levied.

b) After lock-in Period:

At the time of revival

All due and unpaid premiums under the base plan which have not been paid shall be payable without charging any interest or fee. The policyholder also has the option to revive the rider.

Premium allocation charge as applicable shall be levied. The guarantee charges shall be deducted if the guarantee continues to be applicable. No other charges shall be levied.

iv) Lack of Flexibility in Surrender Options

A policyholder can surrender their HDFC SL Youngstar Super Premium policy only after 5 years provided the premium.

If a policyholder wants to surrender before completing 5 years, the insurance cover ceases and the fund value is transferred to the discontinued policy fund.

Analysis of HDFC SL YoungStar Super Premium

One can break down everything about this policy and examine it from A to Z.

But it finally boils down to, how does this policy fair against the alternate options?

Here, I’ll compare HDFC SL Youngstar Super Premium against PPF, and ELSS mutual fund separately to find out whether it is good to have in your portfolio.

HDFC SL YoungStar Super Premium Review Against PPF

Let us now look at a table which shows the comparison between ULIP and PPF.

Now, let us see how much the policyholder will receive by investing ₹ 1 Lac annually for 10 years in PPF.

The prevailing PPF interest rate for Q1 2021-2022 is 7.1% p.a.

Even though PPF has a lock-in period of 15 years, let’s see the assured earnings at the end of 10th year in PPF.

See the compounding table below.

You can see that by the end of 10th year, the policy holder will have an assured return of almost ₹14 Lacs.

It is more than ₹1 Lac higher than the HDFC SL Youngstar Super Premium returns. Even more interesting part is that, unlike HDFC SL Youngstar Super Premium, PPF returns are guaranteed by the Govt. of India.

However, PPF does not offer life cover like HDFC SL Youngstar Super Premium does.

Alternatively, you can buy a term insurance plan for the same sum assured but far less premium. In this way, you can have your life covered, earn better and assured returns than HDFC SL Youngstar Super Premium.

Clearly, PPF+ a term insurance policy is a far better option for a conservative investor, when compared to HDFC SL Youngstar Super Premium policy.

HDFC SL YoungStar Super Premium Review Against ELSS Mutual Fund

Below is a table of comparison between HDFC SL Youngstar Super Premium and ELSS Mutual Fund.

Now let us find out the total returns the policy holder is likely to receive from ELSS Mutual Fund.

The investment is ₹ 1 Lac annually for 10 years, same as we saw in the HDFC SL Youngstar Super premium policy illustration.

We are assuming a very conservative 12% CAGR for the ELSS mutual fund. And the investment risk is literally the same as HDFC SL Youngstar Super Premium, since both are market linked investments.

As you can see that the maturity amount the policy holder will receive on the 10th year will be almost ₹18 Lacs.

In comparison, it is almost ₹5 Lacs higher return than the returns from HDFC SL Youngstar Super Premium.

And again, ELSS Mutual Fund purely an investment instrument. It does not offer life cover like HDFC SL Youngstar Super Premium does.

But, alternatively, you can buy a term insurance plan for the same life cover. Term insurance policies offer higher sum assured amount for far less premium.

This combination of ELSS Mutual Fund + Term Insurance gives you a better life cover, and earn better returns than HDFC SL Youngstar Super Premium.

Verdict

After all the analysis, and comparison, it is the final call that matters.

Should you buy HDFC SL Youngstar Super Premium policy or not?

The answer is, obviously, DO NOT BUY the HDFC SL Youngstar Super Premium policy.

An insurance product, a pure term insurance plan can offers higher and appropriate life cover for a lesser premium amount.

On the other hand, as an investment instrument, it is evident that even PPF with guaranteed benefits is a better alternative.

On considering equal investment risk, ELSS mutual fund are a way better investment option for the following reasons.

- Better Returns

- 10+ better performing funds to choose

- Same Tax Benefit u/s 80C

- Only 3 years Lock-in period

- Flexibility to choose a different fund at any time.

Moreover, HDFC SL Youngstar Super Premium is a long-term commitment. There is no systematic compulsion on the policy’s fund manager to perform at his best all the time.

But with ELSS mutual funds, the investor can get out of the fund anytime, this compels the fund managers to deliver better returns consistently.

If you are considering to buy HDFC SL Youngstar Super Premium, take a look into your alternate options before you make a decision.

But if you have already bought the policy, you still have a way out to invest in better alternative instruments.

How to surrender HDFC SL YoungStar Super Premium?

Considering the fact that there are more than one better alternative options, here are your surrender options.

Surrender during the Free-look Period:

IRDA allows policy buyers a 15day free-look period to review the policy terms. During this period, a buyer can surrender their policy and get back their premium.

The free-look period is 30 days in case the policy is bought online.

On receipt of your letter along with the original policy documents, the company shall arrange to refund you the value of units allocated to you on the date of receipt of request plus the unallocated part of the premium plus charges levied.

No charges or deductions will be levied other than the underwriting charges, and medical examination charges, if any.

Surrendering after the Free-look Period:

As you know, a policyholder can surrender their HDFC SL Youngstar Super Premium policy only after completing 5 years policy term.

To surrender your HDFC SL Youngstar Super Premium policy, follow the following steps.

-

- 1. Get Original Policy Document

2. Fill The Surrender Processing Form

3. Original Cancelled Cheque or Bank Passbook or Bank Statement with pre-printed name, bank account number and IFSC Code (Self Attested).

4. Original ID and Address proof of Policy holder/ Beneficiary for verification by HDFC Life employee (Self Attested).

You can submit these at the HDFC Life branch with the surrender request.

Is It Financially The Right Time to Surrender?

If it has already been a few years with this policy, you may not be sure whether it is financially a better decision to surrender.

As a general rule, it is always good to surrender your policy in the early years. The alternate investment options can offset any apparent loss and earn more return if you surrender early.

But it is always better to consult a Certified Financial Advisor to calculate whether it is financially right for you.

Conclusion

HDFC SL Youngstar Super premium will look attractive to an amateur investors. Maybe that is what keeps them amateur investors.

You must remember to never mix insurance and investment.

For conservative investors, I would suggest to take term insurance policy separately and invest in PPF.

For risk tolerant investors, it is better to go for the term insurance plan + ELSS mutual fund combination for all the advantages considered.

If you have any comments or questions, write them in the comment box below.

Or are you interested in creating a Comprehensive Financial Plan for your financial goals?

Skip the queue by registering for your 30 Minute FREE Financial Plan Consultation. Click the ‘‘BOOK YOUR SLOT NOW!’’ button below.

I always emailed this blog post pae to all my friends, as if like

to read iit afterward my friends will too.