ICICI Prudential Future Perfect is a non-linked insurance plan.

This plan claims guaranteed benefits and guaranteed bonuses. How “guaranteed” are their claims, we will find out in this article.

In this article, we will demonstrate all you need to know about this plan by giving an elaborative example.

You will be able to figure out whether this policy is really making your Future PERFECT, as it claims.

Or, does it have the elements which make your Future “Tense” instead; regardless of their claim.

Let’s read on and figure out the rest by yourself.

Table of Content

2. ICICI Prudential Future Perfect: Guaranteed Benefits

3. ICICI Prudential Future Perfect: Bonuses

4. ICICI Prudential Future Perfect: Illustrative Example

5. ICICI Prudential Future Perfect: Actual Returns

6. ICICI Prudential Future Perfect: Disadvantage (Secret Exposed)

7. ICICI Pru Future Perfect Vs. Other Investments

8. Who Should Avoid the ICICI Prudential Future Perfect Plan?

9. ICICI Prudential Future Perfect Surrender Value Rules

11. Commonly Asked Questions: ICICI Prudential Future Perfect

Key Features:

1. ICICI Prudential Future Perfect is an endowment plan.

2. You will get guaranteed benefits such as Guaranteed Maturity Benefit and Guaranteed Additions each year, based on your policy term.

3. You may also receive non-guaranteed bonuses such as reversionary and terminal bonuses; they are detailed in later sections in this article.

4. In case of the death of a policyholder, death benefits will be provided.

5. The below table shows the Premium Payment Term, Policy term, and basic eligibility criteria to invest in this policy. [Source: ICICI Pru Future Perfect brochure]

Let’s have a look at the video illustration showing the review of all the important aspects of ICICI Pru Future Perfect Plan.

ICICI Prudential Future Perfect: Guaranteed Benefits

This plan offers 2 guaranteed benefits, discussed below:

Guaranteed Maturity Benefits (GMB):

The Guaranteed Maturity Benefit (GMB) is a fixed amount that depends on various things like age, policy term, premium payment term & gender.

GMB gets activated as soon as you purchase the ICICI Prudential Future Perfect Policy.

And, you will receive the guaranteed amount from this benefit as soon as your policy matures.

For example, if your policy term is 20 years, you will receive the GMB in the 20th year.

These benefits are payable subject to payment of all the due premiums.

Investors often cross-check these values using the ICICI Prudential Future Perfect Returns Calculator to understand the realistic returns over time.

Many investors use the ICICI Prudential Future Perfect calculator and ICICI Prudential Future Perfect return calculator to estimate whether the guaranteed maturity benefit is sufficient to meet long-term financial goals.

Guaranteed Addition Benefits

Guaranteed Additions are added to your maturity amount for every policy year that you stay invested in.

The table below shows you how much GAs that will be paid out as a percentage of your annual premium:

You can notice from the table above that the longer you are invested; you will receive higher guaranteed returns on maturity.

For example, if you choose a premium payment term of more than 10 years and stay invested for more than 16 years, you will get the maximum Guaranteed Addition of 18%!

The Guaranteed Maturity Benefit & Guaranteed Additions together contribute to the total Guaranteed Returns you receive at maturity.

Policyholders comparing ICICI Future Perfect returns with other ICICI Prudential investment plans should note that guaranteed additions alone may not generate inflation-beating wealth over long durations.

ICICI Prudential Future Perfect: Bonuses

Bonuses are non-guaranteed. This plan offers 2 types of bonuses, described below:

Reversionary Bonuses

Reversionary Bonus is declared every year as a percentage of Guaranteed Maturity Benefit and Earlier Revisionary Bonuses (if any).

The exact calculation of the Reversionary bonus is unclear. It is calculated using the online calculator available on the website.

Reversionary bonus is payable at maturity of the policy, or it is payable along with death benefits.Reversionary bonus in Cash advantage is added every year to your maturity benefits.

The ICICI Pru Future Perfect bonus history indicates that declared reversionary bonuses have remained relatively moderate, which can significantly affect the final maturity value.

Terminal bonuses

Terminal bonus is a one-time bonus declared at the time of the maturity for participating policy.

Though they are a non-guaranteed bonus, still its value depends on the duration you stay invested.

There is no clear cut way to find Terminal Bonuses but you can use the ICICI Prudential Future Perfect Surrender Value online calculator and ICICI Prudential Future Perfect Maturity Calculator available on the company’s website to get the rough estimates.

Many investors looking for terminal bonus calculation details often rely on the ICICI Prudential Future Perfect maturity calculator to estimate possible non-guaranteed pay-outs.

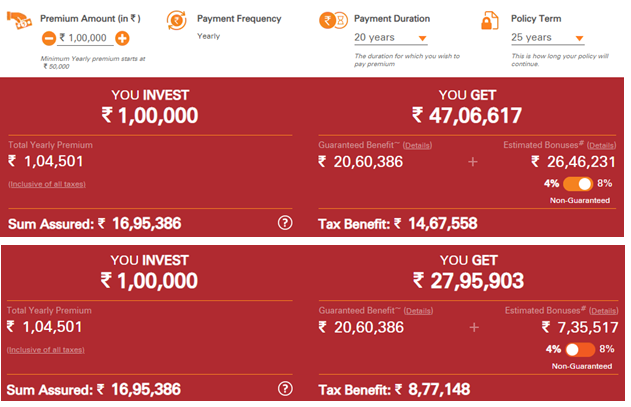

ICICI Prudential Future Perfect Plan: Illustration

Let us say you are 30 years old and you choose to invest in ICICI Pru Future Perfect Plan with the premium amount of Rs.1,00,000 per annum.

You opted your payment duration as 10 years and you have fixed your policy term as 20 years.

Now putting all these values in the Online Calculator, you will get various values shown below

Therefore, if you invest the premium of Rs.1,00,000 per annum.

With taxes, you have to pay the total yearly premium of Rs.1,04,501 for the first year and Rs.1,02,251 for subsequent years.

At maturity, you will get Rs.25,70,254, which consists of Guaranteed Benefits and Estimated Bonuses of Rs.13,84,426 @ 8%.

Or,

Please note, the estimated bonuses are not guaranteed.

The assured sum is Rs.10 Lakhs, it is the amount of life-insurance cover paid to the nominee, in case of policy holder’s death.

The ICICI Pru Future Perfect plan details and benefit illustration demonstrate that a major portion of maturity benefits depends on non-guaranteed bonuses rather than fixed returns.

Now, let’s have a closer look at the Guaranteed Benefits and Estimated Bonuses.

Guaranteed Benefits:

As you can notice, the total Guaranteed Benefits are Rs.11,85,828. It consists of Guaranteed Maturity Benefits (GMB) and Guaranteed Additions (GA) on Maturity. They described below:

Guaranteed Maturity Benefits are set at the inception of the policy, its value depends on the policy holder’s age, policy term, premium, premium payment term, and gender.

They are guaranteed but how this sum actually fixed is unknown.

Guaranteed Additions as we have defined earlier, they are added to your maturity amount for every policy year that you stay invested according to the rate of interest (per annum) as described in the previous section.

You are paying Rs. 1 Lacs per annum for 10 years exclusive of GST and you are receiving the guaranteed benefits of Rs.11,85,828.

It shows that ONLY the principal you paid is guaranteed, which does not contain ANY return!!

ICICI Prudential Future Perfect: Actual Returns

As defined earlier, your policy term is 20 years and your premium payment duration is 10 years.

And, you choose to invest Rs.1,00,000 per annum.

Let’s calculate the average returns using all the data discussed earlier,

|

At 4% p.a. |

At 8% p.a. |

||||

|

Age |

Year |

Annualised premium / Maturity benefit |

Death benefit |

Annualised premium / Maturity benefit |

Death benefit |

|

30 |

1 |

-1,00,000 |

10,00,000 |

-1,00,000 |

10,00,000 |

|

31 |

2 |

-1,00,000 |

10,00,000 |

-1,00,000 |

10,00,000 |

|

32 |

3 |

-1,00,000 |

10,00,000 |

-1,00,000 |

10,00,000 |

|

33 |

4 |

-1,00,000 |

10,00,000 |

-1,00,000 |

10,00,000 |

|

34 |

5 |

-1,00,000 |

10,00,000 |

-1,00,000 |

10,00,000 |

|

35 |

6 |

-1,00,000 |

10,00,000 |

-1,00,000 |

10,00,000 |

|

36 |

7 |

-1,00,000 |

10,00,000 |

-1,00,000 |

10,00,000 |

|

37 |

8 |

-1,00,000 |

10,00,000 |

-1,00,000 |

10,00,000 |

|

38 |

9 |

-1,00,000 |

10,00,000 |

-1,00,000 |

10,00,000 |

|

39 |

10 |

-1,00,000 |

10,00,000 |

-1,00,000 |

10,00,000 |

|

40 |

11 |

0 |

10,00,000 |

0 |

10,00,000 |

|

41 |

12 |

0 |

10,00,000 |

0 |

10,00,000 |

|

42 |

13 |

0 |

10,00,000 |

0 |

10,00,000 |

|

43 |

14 |

0 |

10,00,000 |

0 |

10,00,000 |

|

44 |

15 |

0 |

10,00,000 |

0 |

10,00,000 |

|

45 |

16 |

0 |

10,00,000 |

0 |

10,00,000 |

|

46 |

17 |

0 |

10,00,000 |

0 |

10,00,000 |

|

47 |

18 |

0 |

10,00,000 |

0 |

10,00,000 |

|

48 |

19 |

0 |

10,00,000 |

0 |

10,00,000 |

|

49 |

20 |

0 |

10,00,000 |

0 |

10,00,000 |

|

50 |

15,53,975 |

25,70,254 |

|||

|

IRR |

2.86% |

6.18% |

|||

So, in the policy term of 20 long years, you are getting the average return of just 6.18%.

Please note it is the best interest rate of this policy, as we have assumed the ARR of 8%.

If we consider the Assumed Rate of Return (ARR) as 4%, the average IRR comes down to 2.86%!!

On average, you can expect your returns to be somewhere between 3% to 6.2%!!

Reversionary Bonuses:

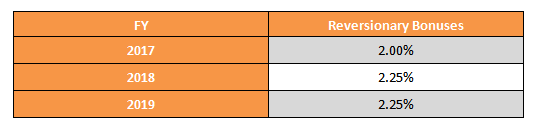

This policy started in the year 2016 and though they claim their estimated bonuses to be around 4% or 8%; below table shows the rate of reversionary bonuses declared so far… It is in the range of 2%-2.25%!!

It is in the range of 2%-2.25%!!

For more accurate calculations, investors can use ICICI Prudential Future Perfect Bonus History and the ICICI Prudential Future Perfect Plan Maturity Calculator available on the official portal.

Now, do you think it is good enough return for a 20-year long investment term?

Do you think, at this bonus rate, will they be able to achieve an IRR of 7%? I doubt.

If you are still looking for more details on this plan, then you should read the ICICI Prudential Future Perfect Product Brochure.

ICICI Prudential Future Perfect: Disadvantage (Secrets Exposed)

Though this policy uses catchy words such as “Guaranteed Benefits” or “Future Perfect”, but in reality, it is not true.

Let’s have a look at its biggest disadvantage:

As you might have noticed in the illustration in the above section, that in the best case scenario you are getting the maximum returns of merely 6.18%!

Therefore, you are receiving Rs.11,85,828, plus the non-guaranteed estimated bonus of Rs.13,84,426!

Anyways, in the best-case scenario, you will receive the sum of above, that is Rs.25,70,254 on maturity, means after 20 years!!

Is it a good deal?

Despite promises in the ICICI Prudential Future Perfect plan brochure, the ICICI Pru Future Perfect actual returns are often much lower than expected, especially considering inflation and long-term investment horizons.

Although the plan uses words like “Future Perfect” and “Guaranteed Benefits,” the actual long-term return percentage may remain lower than several alternative investment avenues.

ICICI Pru Future Perfect Vs. Other Investments

Let’s say if you invest in PPF or Mutual Fund instead, as defined below:

|

Pure Term Life Insurance Policy |

|

|

Sum Assured |

₹ 10,00,000 |

|

Policy Term |

20 years |

|

Premium Paying Term |

10 years |

|

Annualised Premium |

₹ 6,600 |

|

Investment |

₹ 93,400 |

By separating insurance and investment, you can accumulate a higher corpus.

For life coverage, a pure term life insurance policy with a sum assured of ₹10 Lakhs costs a premium of ₹6,600 annually.

The policy term is 20 years with a premium payment term of 10 years.

This allows you to save ₹93,400 out of the ₹1,00,000 annual budget, which can be invested for corpus accumulation.

We’ll consider two investment instruments – one for equity and one for debt – to illustrate how different asset classes perform.

You can choose investments based on your risk appetite.

|

Term Insurance + PPF |

Term insurance + ELSS |

||||

|

Age |

Year |

Term Insurance premium + PPF |

Death benefit |

Term Insurance premium + ELSS |

Death benefit |

|

30 |

1 |

-1,00,000 |

10,00,000 |

-1,00,000 |

10,00,000 |

|

31 |

2 |

-1,00,000 |

10,00,000 |

-1,00,000 |

10,00,000 |

|

32 |

3 |

-1,00,000 |

10,00,000 |

-1,00,000 |

10,00,000 |

|

33 |

4 |

-1,00,000 |

10,00,000 |

-1,00,000 |

10,00,000 |

|

34 |

5 |

-1,00,000 |

10,00,000 |

-1,00,000 |

10,00,000 |

|

35 |

6 |

-1,00,000 |

10,00,000 |

-1,00,000 |

10,00,000 |

|

36 |

7 |

-1,00,000 |

10,00,000 |

-1,00,000 |

10,00,000 |

|

37 |

8 |

-1,00,000 |

10,00,000 |

-1,00,000 |

10,00,000 |

|

38 |

9 |

-1,00,000 |

10,00,000 |

-1,00,000 |

10,00,000 |

|

39 |

10 |

-97,500 |

10,00,000 |

-1,00,000 |

10,00,000 |

|

40 |

11 |

-500 |

10,00,000 |

0 |

10,00,000 |

|

41 |

12 |

-500 |

10,00,000 |

0 |

10,00,000 |

|

42 |

13 |

-500 |

10,00,000 |

0 |

10,00,000 |

|

43 |

14 |

-500 |

10,00,000 |

0 |

10,00,000 |

|

44 |

15 |

-500 |

10,00,000 |

0 |

10,00,000 |

|

45 |

16 |

0 |

10,00,000 |

0 |

10,00,000 |

|

46 |

17 |

0 |

10,00,000 |

0 |

10,00,000 |

|

47 |

18 |

0 |

10,00,000 |

0 |

10,00,000 |

|

48 |

19 |

0 |

10,00,000 |

0 |

10,00,000 |

|

49 |

20 |

0 |

10,00,000 |

0 |

10,00,000 |

|

50 |

27,56,302 |

51,21,208 |

|||

|

IRR |

6.64% |

10.81% |

|||

Debt Instrument – PPF: The PPF account requires a minimum contribution of ₹500 per year for 15 years.

Given the policy term is only 10 years, adjustments are made for the contributions in the remaining years.

The final maturity value in the PPF account is ₹27.56 Lakhs, with an IRR of 6.64% when combined with the pure-term policy.

Equity Instrument – ELSS: The pre-tax final maturity value of the ELSS fund is ₹57.01 Lakhs.

After accounting for capital gains tax, the post-tax maturity value is ₹51.21 Lakhs, with an IRR of 10.81% (post-tax return) when combined with the pure-term policy.

|

ELSS Tax Calculation |

|

|

Maturity value after 20 years |

57,01,524 |

|

Purchase price |

9,34,000 |

|

Long-Term Capital Gains |

47,67,524 |

|

Exemption limit |

1,25,000 |

|

Taxable LTCG |

46,42,524 |

|

Tax paid on LTCG |

5,80,315 |

|

Maturity value after tax |

51,21,208 |

The accumulated corpus from these investments can help you achieve your life goals.

These investments offer better returns, making them superior to the ICICI Pru Perfect Future Plan.

Many investors consult ICICI Prudential Future Perfect reviews and ICICI Pru Future Perfect bonus history to understand whether the policy aligns with long-term wealth goals.

While the ICICI Future Perfect plan claims to offer terminal and reversionary bonuses, historical ICICI Pru Future Perfect bonus history suggests actual bonuses may vary significantly year to year.

Who Should Avoid the ICICI Prudential Future Perfect Plan?

This plan may appear attractive at first glance because of its promises of “guaranteed benefits” and long-term savings.

However, when you look deeper into the actual returns, bonus structure, and long maturity period, it becomes clear that this policy may not suit everyone.

In fact, certain types of investors should seriously reconsider choosing this plan.

1. Investors seeking returns higher than inflation

If your primary goal is to grow your wealth meaningfully above inflation, this plan may disappoint you.

Over long durations like 15–20 years, returns close to or below inflation can erode your purchasing power.

Anyone hoping for strong long-term compounding will likely find more suitable alternatives elsewhere.

2. Individuals who prefer transparent and market-linked investments

People who like to see where their money is going — such as in mutual funds, direct equity, PPF, or even debt funds — may find this plan too opaque.

The bonus structure is non-guaranteed, maturity values vary depending on company performance, and the exact growth path isn’t straightforward.

If transparency matters to you, this plan may not align with your expectations.

3. Those with limited liquidity or unpredictable income

This policy requires consistent long-term premium payments.

Missing payments early can cause the policy to lapse or become paid-up with reduced benefits.

Anyone who anticipates career breaks, income fluctuations, or liquidity needs should be cautious about locking money into a rigid commitment.

4. Young investors looking for aggressive wealth creation

If you are in your 20s or 30s and aim to build a substantial corpus through long-term compounding, products like equity mutual funds, ELSS, or even flexible hybrid investments may serve your goals better.

Traditional endowment plans generally generate modest returns and may not match the potential of market-linked instruments.

5. People who prefer separating insurance and investment

Many financial planners recommend keeping insurance and investment independent.

If you believe in buying a simple term plan plus investing the surplus in diversified instruments, this plan may not align with your financial strategy.

6. Anyone uncomfortable with non-guaranteed bonuses

A significant part of the final maturity amount depends on bonuses that are not guaranteed.

This can create uncertainty, especially when the policy is expected to run for decades.

If you want completely predictable outcomes, you may want to consider alternatives with clearer guarantees.

7. Investors seeking shorter commitment periods

This plan works only over the long term.

If you prefer shorter lock-ins, quicker liquidity, or the flexibility to shift your investments, this product might feel restrictive.

People looking for flexible liquidity, transparent investment growth, and higher equity-linked returns may find alternative investment plans more suitable than traditional participating policies.

ICICI Prudential Future Perfect Surrender Value Rules

This section can explain how the ICICI Prudential Future Perfect policy acquires surrender value only after a minimum number of premiums are paid, depending on the premium payment term selected.

You can also cover how the policy becomes “paid-up” if premiums are discontinued after acquiring surrender value, leading to reduced maturity and death benefits.

Additionally, include how surrendering the policy in the early years may result in lower returns because bonuses are non-guaranteed and various deductions apply.

Mention that many investors use the ICICI Prudential Future Perfect surrender value calculator and policy illustrations to estimate approximate pay-outs before making an exit decision.

Final Verdict

As you might have noticed that the claim of the company of making Future Perfect, is not so perfect.

Instead, it is making your Future Tensed by providing you the returns less than the average rate of inflation of 8%!

In fact, you are losing your money through this policy!!

Our advice is you should avoid investing in this policy.RDs can offer you the guaranteed return greater than 7%, in the much shorter term!

Or, you can invest in PPF which offers a guaranteed return of 7.1%.

If you can tolerate the risk, then we suggest you invest in equity mutual funds where you can get 12% returns on average.

Based on ICICI Prudential Future Perfect reviews, this policy is often compared with endowment plans, RDs, and PPF, highlighting that alternate investment options can deliver better IRR and flexibility over long-term horizons.

Based on multiple ICICI Prudential Future Perfect reviews and bonus history analysis, the policy appears more suitable for conservative investors prioritizing safety over aggressive wealth creation.

ICICI Prudential Future Perfect: Commonly asked questions

1. How to cancel this policy?

You can discontinue this policy by downloading and filling up the surrender form.

You can access the surrender form by visiting the official website of ICICI Prudential Life.

You need to enter your Policy number and date of birth to access your surrender form.

After downloading the surrender form you can fill up the important details and submit it at your nearby branch of ICICI Prudential Life and your surrender request will be processed from there.

Users can also refer to the ICICI Pru Future Perfect policy status online or login to check bonus history and surrender values before making any decision.

2. What pay-outs to expect after surrendering this policy?

If you have chosen to pay a premium for 10 years or more, your policy will acquire a surrender value after you have paid premium fully for 3 years.

If you have chosen to pay a premium for less than 10 years, the policy will acquire a surrender value after you paid premium fully for 2 years.

And, if you discontinue your premiums before your policy has acquired a surrender value, you will NOT receive any pay-out.

For more details on the exact surrender pay-out value, you can refer to the product brochure.

The ICICI Prudential Future Perfect surrender value calculator and official policy documents can help investors estimate realistic pay-outs, but keep in mind that bonuses are non-guaranteed.

The ICICI Prudential Future Perfect surrender value calculator can provide an approximate estimate, but final surrender benefits may still vary depending on bonus accruals and policy duration.

3. What if I stop paying my premiums?

If you stop paying the premium before your policy acquires a surrender value, your policy will lapse and no benefits will be paid.

However, if you stop paying the premiums AFTER your policy acquires a surrender value, the policy would continue as a “paid-up” policy with reduced benefits.

ICICI Pru Future Perfect reviews often highlight that premiums missed before acquiring surrender value can significantly reduce the overall maturity benefits, impacting the future perfect planning outcome.

4. Who to contact in case any help is required during the policy term?

Investors interested in ICICI Prudential Future Perfect plan benefits, bonus history, or policy details can contact ICICI Prudential Life customer care or use the official online portal for assistance.

You can give a missed call on 18003157751 and you will get a call-back.

Or, you can contact them through their official website by sending an online message or request a call-back.

Investors can also use the ICICI Prudential Future Perfect login portal to access premium details, bonus updates, policy statements, and customer support services online.

Still, if you have any specific queries on this plan, feel free to ask them in the comment section.

For your customized investment advice, you can take advantage of our FREE complementary consultation call, by clicking the link in the description below.

If you have any comments or questions, write them in the comment box below.

Or are you interested in creating a Comprehensive Financial Plan for your financial goals?

Skip the queue by registering for your 30 Minute FREE Financial Plan Consultation. Click the ‘Book Now’ button below.

Where is calculator link. Please

Sir

Am in this plan of paying 3 lakhs per year (4 terms paid, i.e., 12 lakhs paid } one more year to pay, 5 years paying and maturity at 10th year. Please advise on what should I do now.

Thanks.

As of today, 35.79% is equity allocation. Do you think that will be beneficial ?. I guess that will add as one time bonus at the time of maturity

Excellent review . I have decided not to opt as today post 2023 Budget all Insurence and rest agents simply suggest that the Maturity will be taxed and hence rush for investment before 3st March 2023. This isnt right way of suggestions by the people . Please double check and invest Please.

Yes. That’s why we dont recommend these kind of schemes and suggested better alternatives.

Would you recommend to me changing it to a paidup policy or I go and surrender and put it in MFs? I have paid 6 premiums (from Jan’18 to Jan’23). Its a 10 year payment term (4 more) with maturity in 15 years (2033)

Which is more beneficial route? converting to paid up or surrendering?

Consulting your financial planner is essential. They will compare the benefits of continuing with the policy versus surrendering it and investing in mutual funds. If you convert to a paid-up policy, you retain some insurance coverage and accrued benefits. If you surrender and invest in MFs, you could potentially achieve higher returns, but this carries more risk. Your planner can project both scenarios to help you make an informed decision.

Best Explanation. I wish I came across this page in 2019. simply I am losing 25k yearly in this non-sense plan 🙁

Excellent analysis. Icici pru perfect is a cruel joke. I wish I have read this article before I took the policy.

This policy is a horrible trap. Even the ICICI Prulife people are not able to explain the policy. I was dumb to have taken this policy in a hurry without much research. After paying 5 annual installment, I get only 60% of invested amount ie.. 6Lacs for 10Lacs if I wish to cancel the policy now. Had I not invested, at least would have made double thru regular MF in that much period.

thanks for a well explained article..i have been in this invest.ent for more than 3 years and my payment term is 10 years, with monthly investments of 42500/. suppose i sureender it today, what would be the final payout and do they charge anything for surrendering after 3 yrs?

Since you have already taken this insurance plan, then you have two options.

Option: 1 You can surrender and encash the policy. And reinvest the surrender value and future premium money with better investment plans like PPF or MF.

Option: 2 You can continue with the insurance plan until the policy matures.

It is advisable to work out the outcome of both options and proceed with the better option.

80% of the time, option 1 is better.

You can consult a financial planner to choose the better option.

Or

You can take advantage of our free complimentary financial plan consultation and talk to our financial planners.

Get your appointment here: https://www.holisticinvestment.in/complimentary-financial-plan-consultation/

My brother suggested me to put icici prudential future perfect plan, I don’t exactly about this plan. now I want to know about this plan. Kindly explain. I think it’s not profitable so that only I ask

Please check with your financial planner.

You can also book a slot with our financial planner for an initial complimentary consultation.

https://www.holisticinvestment.in/complimentary-financial-plan-consultation/

Lucid explaination. I wish I should’ve referred to your article before investing in this product.

1) Thanks a lot, Dr. Sravan for sharing your feedback.

2) We are happy that our article has given you a new perspective. Thanks for sharing your feedback with us.

very good explanation and concluding with suggestions for investment … Goof Job !

Thanks Sandeep.

Nicely analysed. Thanks for your valuable input

Thanks Rajan.