Is this asset suitable for long term or short term?

What are the risk associated with different asset classes?

What kind of returns can I expect from different asset classes?

Do I need to choose one asset class or multiple asset classes?

The investment lessons begin with the basics of different Asset classes followed by a technique called Asset Allocation.

This article is packed with enough content to teach you to swim in the ocean.

Even if you are a beginner investor starting from zero, do not worry, “Everything you don’t know is something you can learn”.

Come, let’s dive into the great ocean of investment.

Table of Contents:

- 1. Cash

- How Inflation Destroys Idle Cash

- 2. Fixed income

- 3. Equity

- 4. Real estate

- 5. Commodity

- 6. Alternative investment

Why asset allocation is important?

Creating your personalized asset allocation strategy

Geological diversification, an extra parachute

Rebalancing

4 pieces of advice you should not forget before investing

Final sum up:

Classes of assets

An asset class is a collection of financial products with similar characteristics like risk factor, liquidity, and return value, etc.

An asset in the sense, we determine both the financial asset and physical asset. We classify asset classes into six,

These are considered the major asset classes in India and form the foundation of most investment asset classes and diversified investment portfolios.

Understanding the different asset classes helps investors create a balanced asset mix based on financial goals, liquidity requirements, and risk tolerance.

1. Cash

Cash denotes hard cash and the money you have in the bank savings with liquidity which is mostly used for transactions.

Holding cash is not an investment, but it gives you the ability to invest in any asset or buy anything you want anytime.

The problem with holding excess cash for a long time is that it merely fails to beat inflation all the time.

Investors are advised to have 6-8 months of their expense in liquid cash always as back-up funds. It is the only tool that helps you in time of immediate or unexpected needs.

Cash is considered one of the safest asset classes and is often categorized under liquid asset classes because of its high accessibility and immediate usability.

Cash equivalent:

Cash equivalents are short-term investment securities that possess high credit value and high liquidity.

It is called Cash equivalent assets because the liquidity of this investment is equivalent to holding cash. The cash equivalent assets can be converted into cash quickly.

The basic objective of holding cash equivalents is to handle emergency money requirements while creating interest from it when not needed.

For example, a Flexible Fixed Deposit is one such cash equivalent financial product that gives you the benefits of liquidity in a savings account and the high returns of a fixed deposit.

Some of the common Cash equivalents are flexible fixed deposits and liquid funds.

How Inflation Destroys Idle Cash

Many people believe keeping money idle in cash or a savings account is safe.

While cash is the most liquid asset class, it slowly loses purchasing power because of inflation.

As prices rise every year, the value of your money falls over time.

For example, if inflation is 6% and your savings account gives only 3% return, your money is actually losing value in real terms.

This is why idle cash is not considered an effective long-term investment asset.

Cash and cash equivalent assets are important for emergency funds and short-term goals, but long-term wealth creation usually requires exposure to other investment asset classes like equity, fixed income, gold, and real assets.

A balanced asset allocation helps investors protect their money from inflation while maintaining liquidity and financial stability.

2. Fixed income

A fixed income is otherwise known as a bond or debt.

It works this way – the bank or government or any private organization borrows your money and pledges to return the capital amount to you with the interest of about 7-8% for the predefined period of time.

Fixed incomes are a less risky investment with less interest in return, with security for your capital. Examples of fixed income schemes are treasury bonds, corporate bonds, certificates of deposits, debentures, and fixed deposit schemes of a bank.

The fixed income asset class is widely preferred by conservative investors seeking predictable returns and lower volatility.

Unfortunately, fixed deposits are taxable. The accrued sum of nominal return (7-8%) will be cut with a percentage of tax and then the inflation rate, to get the actual return, which is probably negligible or sometimes negative even in the fixed deposits providing best interest.

Examples of investment assets under the cash asset class include savings accounts, liquid mutual funds, treasury bills, and fixed deposits with flexible withdrawal options.

Among all asset classes, fixed income investments are considered suitable for investors who prioritize capital safety over aggressive growth.

3. Equity

Equity or stock is, owning a small part of a public company.

What is the first thing that comes into your mind when talking about the stock market?

Probably the advice to avoid the risk of choosing the stock market, that you heard by someone from somewhere who lost their money in the stock market.

Of course, it involves risk, but tell me what is not?

Even a slow walk down the road has a risk of some mad car driver ruining the pedestrians. But we still

have to walk through the risks to reach the destination we aimed. Yet you may ask, “Why should I take such a risk?”

Your gain is the return.

Equity is optimally a long-term investment.

The returns from equity in the long-term cannot be chased by any other asset class. You can expect 12% to 15% year on year average return from equities.

This huge return is only catchable on accounting to some amount of risk.

The equity asset class is regarded as one of the best investment assets for long-term wealth creation.

Investors can buy and sell direct stocks online. Buying a share gives you a small percentage of ownership to a business.

Any business takes time to grow thus demands patience to rip your share of the profit.

The other advantage is that the investment capital is very less in stock compared to any other asset class.

Equities are growth-oriented investment assets and are often recommended for younger investors with higher risk tolerance and longer financial planning horizons.

Choosing the right market stock is very crucial in equity.

But, there are multiple factors that influence the ups and downs of the share market.

Mostly, the value of a company depends upon the performance of the business.

Yet, there are factors that can out-run the efforts made by the company, like technological advancements, market fluctuations, competitor strategy and etc., which goes beyond our reach of control.

Equity Mutual Funds:

Watching the numbers go up and down on a screen all the time without being able to focus on real-life happenings and happiness is something that most people would regret.

This made equity investments a night-mare for a commoner. Fortunately, this problem created the opportunity for the introduction of Mutual funds.

Mutual funds are one of the most beginner-friendly investment asset types because they provide diversification, professional management, and lower entry barriers for retail investors.

Equity mutual fund is no different than equity, where you are simply hiring a Fund Manager and give him the authority to manage your stocks on your behalf.

A fund manager invests your funds in diversified assets like stocks, debt, and gold for which he charges a fee on the overall assets under management.

Mutual funds are less risky than direct stock investments because a fund manager is a trained professional and well experienced in the stock market.

Only experience gives you a deep understanding of the market fluctuations, and the ability to analyze the performance of securities.

For a beginner investor, it is too much risk driven to invest in direct equity and is advisable to go with mutual funds to avoid risk.

For investors looking for balanced portfolio management, mutual funds can help create ideal asset allocation across multiple asset classes without requiring constant monitoring of the markets.

4. Real estate

Investing in Real estate is to own a physical space like plots or buildings which are used for residential or commercial purpose.

9 out of 10 in a town has a dream house in mind and every one of them wants that dream house to come into reality very immediately.

Real estate is considered a real asset because it has physical value and can potentially generate rental income along with long-term capital appreciation.

In metro cities like Chennai, Bangalore, and Delhi there are no notable variations in real-estate price for the past 3-5 years.

Real estate was once a magic happening business, but now it has become just another business that survived.

The fact that except a few real-estate businessmen, have failed to adopt environmentally sustainable practices is also a reason for the stagnant growth of the industry.

The value of your real estate investment is influenced by factors like the accessibility of property, up-coming government projects, transaction cost, potential demand, and political influence, etc. Notably, the transaction cost is high while both buying and selling.

It lacks transparency in market price, land titles and etc., which might bring you inconvenience or legal issue in the future. Also, there is no substantial way to know the actual market price of a real-estate.

Apart from all these factors, the liquidity of your cash in real estate is almost frozen. Finding the right buyer on the right time at the right price is not a quick buck.

Which means the asset cannot be converted into cash immediately?

Investment in real estate takes a lot of patience and more experience to generate good returns.

Compared to liquid asset classes like cash or stocks, real estate has lower liquidity but may offer better long-term stability and wealth preservation benefits.

5. Commodity

A commodity can be any type of goods like gold, copper, and silver, etc. that can be bought by anyone.

But in terms of investment, Gold is the most valuable trading commodity and easily affordable commodity available in the market.

India is always pleased about gold but it is rather seen as a privilege than investment. Likewise, all the commodities have got their own characteristics and market influence.

Gold is one of the most recognized commodity asset classes and is commonly used as a hedge against inflation, economic uncertainty, and currency fluctuations.

The term ‘investment in commodity’ is a contradiction.

A commodity is for trading, and clearly not for investing. The idea is simple about successful trading since ancient times – buy a commodity when the price is less and sell it when high.

To predict the rise and fall in the price of a commodity, a trader must be up-to-date on all the factors influencing supply and demand proportion.

Investing vs Trading:

The major difference between Investing and Trading is that investment over time will generate more money by earning profit to both the buyer and the seller like in the stocks, whereas trading will only swap the money between the buyer and seller’s pockets.

Investing focuses on long-term asset growth and wealth generation, while trading primarily depends on short-term market price fluctuations and timing strategies.

In trading, the trader makes predictions about demand and market price; take, for example, a trader bought an oil barrel of market value Rs 100.

If the market demand for oil increases assume that the trader expects to gain 10% profit i.e., oil price goes to Rs 110.

But if the trader’s prediction fails and the market demand decline, the trader loses by 10% i.e., oil price goes to Rs 90.

Thus, if the market demand increases, Rs 10 goes to the seller’s pocket from the buyer.

If the demand decreases, Rs 10 goes to the buyer’s pocket from the seller. Thus trading is just Money rotation.

But in investing, both the buyer and seller can make money. Take, for example, you are buying a stock for Rs 100 and after a period of some 7 years, the right stock value must rise, and you could sell your share for Rs 200.

If I’m buying the stock you sold for Rs 200, I can keep it for some more years and further sell it to Rs 300 or more when the market rises again.

Here the buyer and the seller both can make a profit and it is a real win-win deal.

Thus investment is Money generation.

6. Alternative investment

There is a unique perspective of investment such as collecting the State of Art pieces like artefacts, antique goods, and rare vintage pieces.

Usually, the value of any commodity depreciates over time, while some commodities that are created with extreme care and passion end up to be the favourite one of that generation.

This makes such a product more valuable with respect to time. But this is an unregulated market, without any proper demand and supply.

Return is unpredictable. With the right buyer, the return is huge, and without the right buyer, the loss may also be huge.

Alternative investment asset classes include collectibles, art, venture capital, hedge funds, private equity, and rare vintage assets.

These asset classes and their properties would bring you more questions on the return flexibility, liquidity of cash, capital investment amount, and etc.

The possible criteria that can influence all the asset classes are compared for an easy understanding.

A beginner investor needs an in-depth understanding of the asset classes first; which I hope we have discussed enough.

Then the very crucial part of the investment is asset allocation, which influences decision making in your investment portfolio.

Why asset allocation is important?

The reasons why an investor cannot avoid Asset allocation:

Have you ever noticed a street vendor sell diverse or unrelated products together like, umbrella and sunglasses; hot coffee and chill fresh juice.

Sunglasses are only for sunny days and umbrellas are for rainy as well as sunny days.

Of course, nobody would buy both of them at the same. This may not even make sense to an outsider.

It is true that the vendor cannot sell everything at the same time, but that’s the point.

He can definitely sell any one of his product at a time for sure without worrying about the current climate. No matter the sunshine or the misty rain, the vendor can run his business.

The same way, an investor is advised to invest in diverse products which do not respond to the market fluctuations in a similar manner.

When your investment is diversified across the asset classes, you can play the game with more stability.

Understand that the asset allocation is not a strategy to increase the return of your investment portfolio but to optimize the risk vulnerability.

The risk and return are mutually proportional and should be balanced for a steady investment portfolio.

The best asset allocation depends on age, income, financial goals, emotional stability, and investment horizon.

Conservative investors may prefer fixed income asset classes, while aggressive investors may allocate more towards equities and growth assets.

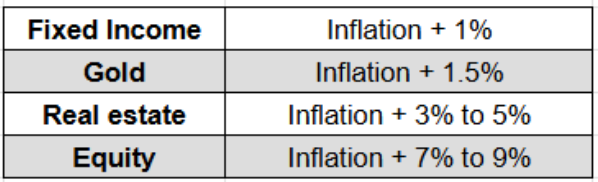

Inflation Adjusted Returns from Different Investment Assets:

The general population works hard at a young age to save enough money to enjoy their retirement with financial safety.

But neither your money nor you are safe! No offense. That’s just the fact. If your money just lies in a place where you think will have safety, it is not.

There is a quote which says, “It’s easy to make money than to manage money”. Maybe it should be changed like this for the modern world as, “It’s hard to make money, but it’s even more hard to manage money”

It’s pretty obvious for a common man like you and me, chasing dreams in this chaos to be unaware of the concept ‘Time value of money’.

But, you would have come across the term ‘Inflation’ that reduces the value of money over time. “A Rupee today is worth more than a Rupee tomorrow”.

Which means you can buy an apple for 10 Rs today, but you may need 11 Rs for an apple next year.

Investing is simply putting your money to work, to beat inflation.

So, if you are going to keep your money in a safe place, well and good, but better in form of an investment in an asset that grows at least more than the inflation rate of our country which is around 4%.

To help you picture the nominal return above inflation the table below will help.

Inflation-adjusted returns are one of the most important factors to consider while comparing different investment assets.

You cannot blindly invest in a maximum return producing asset. We need to evaluate the risk factor before investing.

A detailed note is given below about Risk Vs. Return to give you a good understanding.

Risk vs. Return:

Basically, risk and return are proportional.

Asset allocation is the principle of investing in diverse asset classes and different financial products in the same asset class to balance the risk versus reward phenomena to minimize the volatility of your capital investment.

Instead of dropping a bulk bag of investment in a single asset class, asset allocation advises the investor to split it into multiple smaller bags and drop them to various asset classes which reduces the risk of losing everything you’ve got.

A balanced portfolio usually contains a mix of equity asset classes, debt asset classes, cash equivalents, commodities, and real assets to optimize both risk and return.

The idea of asset allocation is to build an investment portfolio in a ratio that the criteria affecting one asset class do not affect the other in the same way at the same time.

Remember the basics, if the risk is less, return is also less and as risk goes high, then the return also climbs high.

The Art of Asset Allocation:

Asset allocation is the mix of asset classes of your choice in a specific ratio in your investment portfolio. There are multiple criteria to be considered while choosing your asset allocation ratio.

The ideal asset allocation differs from person to person because financial responsibilities, investment goals, age, income level, and emotional tolerance toward risk vary for every investor.

An asset allocation strategy must be created on the basis of the investor’s individual goals, risk tolerance ability and emotional stability.

To create the strategy that works for you, you need a better understanding of yourself i.e., your emotional stability and financial stability.

Plus, you have to constantly gain knowledge of the assets you have chosen to invest and the factors that can, directly and indirectly, affect the value of your assets.

Asset allocation examples may include aggressive portfolios focused on equities, conservative portfolios focused on fixed income asset classes, or hybrid portfolios containing multiple investment asset categories for balanced growth.

If there is a fool proof way of asset diversification then it is to invest in all the asset classes with an optimal ratio.

The Pyramid of Asset Allocation will give you an easy understanding of the diversification process.

Now that you know what you are going to deal with, you need to know what you are made to choose wisely.

As stated before, only a better understanding of yourself will help you to make the right choice on what you want.

AGE MIRRORING is already broken!

We now talk of age mirroring only to prove it is not worth believing! Old school of thought in personal finance advocates for the following age mirroring calculation.

(100-age) -> EQUITY (Offensive)

Age-based asset allocation is only a broad guideline and not a universal investment formula suitable for every investor or every financial situation.

It is not a general formula that everyone can use; instead, it can only guide you to create an asset allocation strategy with minimal risk involvement.

Consider an investor, at the retirement age of 70, has created a regular income for his expenses and now wants to invest for his grandchildren.

The time horizon of this financial goal is at near 25 years.

So the right choice of investment for this goal would be equity. So it is not mandatory to employ age mirroring for this goal.

Long-term financial goals generally require growth-oriented investment asset classes such as equities, whereas short-term goals are better supported by fixed income asset classes and liquid investment assets.

If you’re saving for your child’s higher education, which is forward in 2 years, then equity is definitely not safe, fixed income is a wise choice.

Thus age mirroring is not the only strategy to create your financial portfolio or asset allocation.

But you cannot find out that one perfect asset allocation strategy that suits for everyone, because it does not even exist! So, what is it then?

Creating your personalized asset allocation strategy

“A ring does not fit into all fingers”. We all have different strengths and weaknesses. The same goes for an investment strategy.

There is no general formula to create the best asset allocation strategy. You just cannot fit into any financial manager’s predefined proposal of an asset allocation strategy.

Every investor requires a personalized asset allocation strategy because different asset classes react differently to inflation, economic conditions, liquidity requirements, and market volatility.

A sensible guideline to create a personalized asset allocation strategy involves, focusing on these three major factors,

- Your financial goal

- Your time horizon

- Your personal risk tolerance

1. Nature of financial goal

Financial goals are unique for everyone like saving for retirement, paying a debt, saving for your child’s higher education, saving an emergency fund, etc.

You are that one who sets your goals and influences it to the possible extreme. They can be classified into two, based on your priority as,

- Personal goals

- Life goals

Investment planning becomes more effective when financial goals are clearly categorized into short-term, medium-term, and long-term asset allocation categories.

Some goals are purely dependent on your financial status while some require a huge commitment of work and time which will have an overall influence in your life.

Try to understand the relationship between your emotional stability and financial goal to manipulate it as desired.

Regardless of the nature of your goal, it should fall into a time horizon which we generally categorize as a short term financial goal and long term financial goal.

2. Time horizon

Moreover, it is mandatory to make your asset allocation based on your financial goal’s time horizon with first priority. Categorized as

- Short term goal (<5 yrs)

- Long term goal (>5 yrs)

The time horizon of an investment plays a major role in deciding the right asset class allocation and investment asset types suitable for the portfolio.

For your long term goal, you can take risk and invest in equity. Equity as an asset class needs 5-7 years to have definite performance. Equity will beat out all other asset classes in the long run.

Equity asset classes are often considered the best investment assets for long-term wealth creation because they have historically generated inflation-beating returns over extended periods.

For your short term goal, you need security to capital and thus a fixed income is the right place. For a commitment in the next one year, you need the money in cash or cash equivalents.

3. Risk tolerance

Your risk tolerance depends on your financial stability and emotional stability.

The way you react for the daily morning traffic jam, your tendency to accept the wrong decisions you made in life, etc., decides your emotional stability.

Thus the level of your tolerance is in accordance with your emotions.

Risk tolerance is one of the most important factors in determining the right asset mix between aggressive investment assets and defensive asset classes.

Understanding Risk and Rewards

It’s human nature to want the best rate of return possible, but in reality, we always have to keep in mind that the greater the returns, the higher are the risks.

Which is why getting the right mix of assets is a must. And you can do that by following an old familiar idea – Don’t put all your eggs in one basket. Asset Allocation and Diversification are the two main principles that can help build the right mix.

Diversification across different investment asset classes can reduce portfolio volatility and improve the balance between risk and return.

Asset Allocation just means diversifying your money into a range of investment types to help manage your risk – typically, cash, bonds and equities.

And Diversification means spreading your money within each of those investment types to ensure that your portfolio is not dependent on the performance of any one investment.

A diversified investment portfolio may contain equities, debt instruments, gold, cash equivalents, real estate, and alternative investment assets depending on the investor’s financial profile.

In simple, the risk factor and return of stock are volatile which means, the appreciation or depreciation would be aggressive; whereas a fixed income is comparatively a less volatile investment that is defensive in nature.

If you have a regular source of income like a Doctor, Software professional, or Salaried NRI in young age then your investment should be more aggressive than defensive.

Since you are financially stable and can create more money with an ample amount of time left, aggressive investment suits your portfolio.

As you approach or in retirement or if your source of income is flexible, then your investment should be more defensive than aggressive.

It is not wise to risk your need for greed.

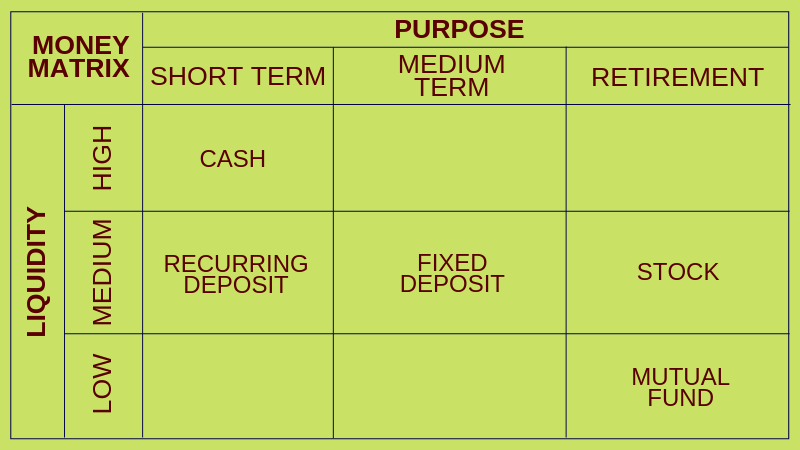

Liquidity of different asset classes

The very first step to investing is to have a financial goal. Is it a home you’re investing for? Or retirement?

We are all very different individuals with our own personal circumstances.

And so the next step is to establish the type of investor you are. For instance, would you say that your approach is cautious or bold? Or, do you think you’ll fall somewhere in between?

Liquidity is a crucial factor while comparing different asset classes because it determines how quickly an investment asset can be converted into usable cash without significant loss in value.

You could consider aggressive options for longer-term goals and conservative options for more immediate needs.

25 years to go:

Emphasis on equities for the potential of long-term capital growth.

10 years to go:

Portfolio could get a bit conservative to consolidate some of the gains. Part of the money stays in equities, part moves into lower-risk bond investments.

5 years to go:

Aim to preserve any gains made. Lay emphasis on lower-risk bond and cash investments.

Liquidity is one more important factor to consider during the asset allocation process.

What good is your money that does not come for your help when needed? But of course, it is mandatory to allocate some of your investments into highly illiquid assets for your long term usage.

But make sure to drop some cash in a handy place. The MONEY MATRIX we have created will be useful for you to a better understanding of the purpose and liquidity of your investment.

Keeping in mind, your target, the time horizon to achieve your financial goal, inflation rate, amount you can invest every month, I have created a simple asset allocation calculator using Excel macro.

With minor adjustments to the equity and debt allocation percentage, you can create a customized asset allocation strategy by yourself, and also check the expected return in the predefined time horizon. Download it for free from the below link.

Geological diversification, an extra parachute

Diversification is done to minimize the risk factor to the best possible level.Bear in mind that few people choose just one investment.

Most investors diversify or choose a variety of investments. The benefit is that you are less likely to lose out if one type of investment does badly.

You also have more chance of benefiting from investments that do well.

International diversification is an advanced asset allocation strategy that helps investors reduce country-specific economic and market risks.

But, what happens in case of a tragic fall in the economy, and the whole country’s stock market crashes as it happened in history.

You may suffer the loss along with the rest of the stock-holders in the country. But there is always a way out.

Geological diversification or international diversification is investing in share markets of foreign countries.

International mutual funds and global fund of funds provide exposure to foreign equity asset classes and global investment opportunities without directly opening overseas trading accounts.

You may find it complicated to understand an international stock market without prior exposure. As already said, there is always a way out and it is called International FUND OF FUNDS (FOF).

International FOF is an Indian mutual fund scheme where in which the money collected from investors will be invested in another foreign mutual fund scheme.

Example: Frankin India Feeder: Franklin US Opportunities Fund. “Franklin US opportunities fund” is a US based fund that invests in leading growth companies of “USA.“

Frankin India Feeder: Franklin US Opportunities Fund” is an Indian Mutual fund scheme that collects money and feeds the investment in Frankin US opportunities fund.

You can invest in a foreign mutual funds company through a domestic mutual company which has an alliance with the company abroad.

This will make your investment more diversified and also provides additional safety from a market crash.

This would be a way far better advice you could get in asset allocation for the safety of your savings, than any.

Rebalancing

There also comes a time when it makes sense to change your investment mix to lock in the gains made.

Major life events and fluctuations in your portfolio’s performance may mean your plan is off-track and you’ll want to consider rebalancing.

Monitor your plan on your own or with the help of your financial adviser and keep investing.

Portfolio rebalancing is the process of restoring the original asset class allocation whenever market movements create imbalance in the investment portfolio.

Once you are done with allocating your assets, over a period of time your investment will start to appreciate in one asset class and may depreciate in the other.

This will create an imbalance in the asset allocation you have created for your investment.

For example, let’s say you have a sum of Rs 3 lakhs with you to invest, and after making all the risk assessment and asset allocation your investment is made to be 60% aggressive and 40% defensive.

| Assets | Allocation | Your Investment | Returns in 1 Year | Investment Return after 1 Year | Allocation Required |

|---|---|---|---|---|---|

| Equity | 60% | 180000 | 15% | 207000 | 200880 |

| Debt | 30% | 90000 | 7% | 96300 | 100440 |

| Gold | 10% | 30000 | 5% | 31500 | 33480 |

| 300000 | 334800 | 334800 |

The above chart shows that now is the time to rebalance the allocation suitable to your risk profile, you need to sell Rs 6120/- of equity and buy Rs 4140/- and Rs 1980/- of debt and gold respectively.

Rebalancing is simply the process of maintaining the asset allocation ratio whenever required. It must be done with precision once in a year or even more frequently when the allocation percentage varies a lot, to manage risk and optimize returns.

Regular portfolio rebalancing helps investors maintain discipline, control risk exposure, and preserve the intended balance between offensive and defensive asset classes.

Shifting money away from an asset class when it is doing well in favour of an asset category that is doing poorly may not be easy.

But it can be a wise move. By cutting back on current “winners” and adding more current “losers,” rebalancing forces you to buy low and sell high. This is the ultimate rule of money making.

Also, you need to consider the transaction fee and tax consequences while rebalancing. A financial advisor can give you guidance to minimize this cost potentially.

4 pieces of advice you should not forget before investing

1. Keep an eye on your financial goal timeline:

If you have your financial goal in the next year, keep it liquid. If you have your financial goal in the next 1-5 years, put your money in a maximum return debt.

If your financial goal is more than 5 years away, go straight away to equity. Do not lose focus.

2. Remember the Risk vs. Return:

I will be happy to show you an investment with zero risk and high return, but something like that does not exist.

So remember if you expect for a mountain of return then the risk is already on the hill-top. The choice is yours. Play safe? Or play smart?

3. Hold stocks:

It is always wise to have a long term plan, which is obviously going to be an investment in equity. Nothing gives you a return to beat the inflation as stocks, so just hold for the long run.

Equity investments continue to remain one of the strongest long-term inflation-beating asset classes for wealth generation and financial independence.

4. Refresh your financial goals and investments:

Sometimes, you may reach your financial goals before your predetermined timeline, so refresh and review your financial goals and investments at least twice a year. Be updated.

Final sum up:

“Never invest in something you don’t understand”, is advice from the most powerful investor alive, Warren Buffet.

You should completely read the disclosure agreement and the terms & conditions carefully before investing. I hope to have shared my knowledge of asset allocation and asset classes.

Understanding different types of investment assets, asset allocation strategies, liquidity, diversification, and risk management principles can help investors create a stronger and more stable financial future.

This article can guide a beginner investor to find the right path and also holds some tips for the pro-investors.

If you still need any clarification, then seek help from a reputed Financial Advisor or Investment Planner. But educating yourself can only give you the confidence to make the right decisions.

Remember, “In a room of millionaires, knowledge is true wealth.”

If you have any comments or questions, write them in the comment box below.

Or are you interested in creating a Comprehensive Financial Plan for your financial goals?

Skip the queue by registering for your 30-minute FREE Financial Plan Consultation. Click the ‘‘BOOK YOUR SLOT NOW!’’ button below.

Well said article