A Warning: What would be the impact on you and your family members if personal finance things don’t work out as per your expectation when you return to India…?

Bad news: 90% of NRI investors are not with the right financial planner.

Good news: You can choose the right financial planner now.

As an NRI returning to India, you need a well-thought-out financial plan. Making any impulsive decision will have an adverse effect.

Table of Contents

1.) Residential Status in India & Its Effects on Taxability

2.) Income Tax Implications for a Returning NRI/RNOR

3.) After Losing the RNOR Status

- What Should You Do After Returning to India as an NRI?

- How Long Can I Continue to Maintain My NRE Account?

- What Is an RFC Account?

- Retaining Overseas Assets

1) Residential Status in India & its Effects on Taxability

Residential status describes the duration of the physical presence of a citizen inside Indian Territory.

The Income-Tax Act defines the provision for determining the residential status of a person.

As of 1 April 2026, this is now Section 6 of the Income Tax Act, 2025, which carries forward the same rule that used to be Section 6 of the Income-tax Act, 1961.

The taxability of an individual is highly dependent on the residential status of that person for a particular financial year.

Under the Income-Tax law, a person must fall into one of these three categories,

- Non-Resident

- Resident but nor Ordinary Resident in India (RNOR)

- Resident and Ordinary Resident in India (ROR)

a) Who is an NRI?

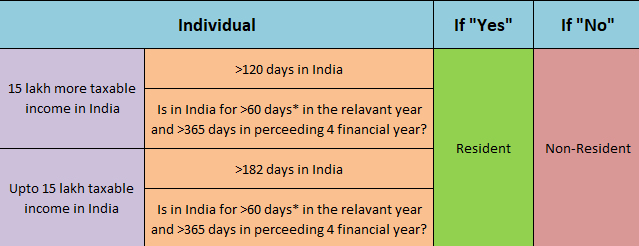

To determine your residential status as per the Indian Income-Tax law, you need to examine these two basic conditions given below.

(i) As per the financial year 2019-2020, if an Indian citizen or Persons of Indian Origin visit India for more than 182 days in the relevant Financial Year.

But after February 2020, as per the Budget 2020, the period reduced to 120 days for the people whose taxable income in India exceeds more than Rs. 15 Lakhs.

This 120-day rule is no longer a temporary Budget tweak — it has now been written permanently into Section 6 of the new Income Tax Act, 2025, effective from 1 April 2026, and continues to apply specifically to Indian citizens and PIOs whose Indian-source income exceeds ₹15 lakhs.

And it stays as 182 days for whose taxable income is up to Rs. 15 Lakhs,

(ii) Is in India for more than 60 days in the relevant financial year and more than 365 days in the preceding 4 Financial Years

then the individual is determined as a Resident of India if at least any one of the conditions is satisfied.

The individual is determined as a Non-Resident only if both the conditions (i) & (ii) are not satisfied.

For better understanding take a look at the infographic given below,

There is an exemption for individuals belonging to certain categories to satisfy only first condition as mentioned below,

There is an exemption for individuals belonging to certain categories to satisfy only first condition as mentioned below,

- An Indian citizen who leaves India during the previous year for employment

- An Indian citizen who leaves India as a member of the crew of an Indian ship

- Person of Indian Origin (POI) or Overseas Citizen of India (OCI) who comes to visit India on a visit during the previous year

Individuals who fall into these categories need not satisfy both conditions.

They will be determined as NRI if they satisfy condition (i) alone, i.e. if they stay outside of India for more than 182 days in the relevant year, then they are still considered as an NRI.

Another interesting information is the difference in the definition of “Resident” in Income Tax and FEMA. Which is clarified in the below video.

Deemed Residency for people in tax-free countries (e.g. UAE, Monaco, Bermuda):

If you are an Indian citizen earning ₹15 lakhs or more from Indian sources, and you are not liable to pay tax in ANY other country, you will now be treated as a deemed Resident of India — even if you spend zero days in India during the year.

This was first introduced via Section 6(1A) by the Finance Act, 2020 (effective AY 2021-22) and now continues under Section 6 of the Income Tax Act, 2025.

It mainly targets NRIs settled in zero-tax jurisdictions.

If this applies to you, your earlier assumption of being ‘safely NRI’ purely because you stayed below the day-count limits may no longer hold — talk to a tax advisor.

b) Who is an RNOR?

RNOR stands for “Resident Not Ordinary Resident”.

As per the Indian Income-Tax law,

(iii) If you have been a non-resident in India in 9 out of 10 years preceding that financial year.

OR

(iv) If you have lived for less than 729 days out of 7 years preceding that financial year,

Then you are considered as RNOR for that particular financial year you are returning to India and the subsequent year (2 years).

Let us understand this with an Example.

Take the case of Mr. Suresh, who worked for 10 years as a civil engineer in Canada.

On August 31, 2019, he relocated to India.

He could be considered an Indian resident for tax purposes because he spent 213 days (more than 182 days) in India during the financial year 2019-20.

However, because he spent nine of the previous ten years (2018-19 and prior), he was granted RNOR status for 2019-20.

He stayed in India for 609 days (less than 729 days) by the end of March 2020 and thus remained an RNOR.

He had been in India for 975 days (more than 729 days) by March 2021 and hence had become an Indian resident for the financial year 2021-22.

A Resident other than an NRI or NOR is generally referred to as an Ordinary Resident (ROR).

You can find out your residential status through the Official Income-Tax Residential Status Calculator.

c) NRI/RNOR status after returning to India

Your NRI status after returning to India will be deemed as RNOR status for 2-3 years and then eventually when the conditions for RNOR status are not satisfied, your residential status will become a ROR (Ordinary Resident).

However, the taxability of an NRI and RNOR is the same.

Many returning NRIs are unsure about when their NRI status expires after returning to India and how long the RNOR status continues.

Your residential status should be evaluated separately for every financial year based on the Income-tax Act.

Simply moving back to India permanently does not automatically make you a Resident and Ordinary Resident (ROR).

Understanding this transition is the first step towards effective tax planning for NRIs returning to India.

You must know the important things to do before losing your RNOR status (NRI 2 years includes the year of returning and the immediate subsequent year).

Because once you lose your RNOR status you will be restricted from many tax benefits.

I will elaborate on the checklist of the to do’s before losing the RNOR status at the end of this article.

2) Income Tax implications for a Returning NRI

Whether you are an NRI returning to India permanently or planning to split your time between India and another country, understanding your residential status is crucial because it determines how your Indian income and overseas income will be taxed during the transition period.

What do you think you need to do to ease yourself financially when you return to India…?

How about understanding the tax implications for a returning NRI…?

To potentially reduce the tax burden & ease the finances of an NRI returning to India, it is mandatory to understand the Income Tax implications for a returning NRI.

Income earned in India is taxable for an NRI in India.

Income earned outside India is not taxable for an NRI in India.

It means the taxability of your overseas income (such as rental income, capital gains, bank interest, dividends, etc.) arising out of your assets outside of India (such as bank accounts, stock market/securities, life insurance policies , loans, company deposits, debentures, bonds, residential properties, etc.) largely depends on your residential status in India.

Let’s see an example – As an NRI/RNOR returning to India, you want to buy a new property in India by selling one of your overseas assets.

In this case, if you sell your overseas assets and receive the sales proceeds (money) in your overseas bank account, you do not have to pay any taxes in India.

But you need the sales proceeds (money) to be in the Indian account to buy your new property in India.

You will not have to pay any taxes in India if you can simply transfer money from your overseas bank account to your Indian bank account.

What about GST? How can NRIs get the refund of GST of the insurance taken when being a Resident?

From 1 April 2026, the Tax Collected at Source (TCS) on large remittances sent abroad for education, medical treatment, or travel has been reduced to a flat 2%.

If you’re moving money out of India for these purposes around the time you return, this directly improves your cash flow compared to the older, higher TCS rates.

a) Income Tax rules of an NRI returning to India

Income received or received on your behalf or accrues in India during a financial year by a NOR/NRI are fully taxable as per the Income-tax slab.

Income that accrues or arises outside India and received outside India in a financial year from any other source, by a NOR/NRI is not taxable.

Income which accrues or arises outside India and received outside India during a financial year and remitted to India during that financial year, by both ROR and NOR/ NRI are not taxable.

b) Income Tax Benefits when you are an NRI/RNOR

When you are an NRI/RNOR, you will be exempted from income tax in India for your following incomes:

- Capital gain arising from the sale of fixed and financial assets held overseas (like properties and shares)

- Interest received from FCNR (Foreign Currency Non-Resident) and RFC (Resident Foreign Currency)deposits

- Withdrawals or pension from the retirement account or pension scheme held overseas

- Interest or dividends earned in deposits or securities held overseas

- Rent received from properties held overseas

Based on your return date to India, you stand to enjoy these tax benefits for 2 to 3 years. However, all your Indian income will be taxed.

Now we know about the Tax benefits.

But it is also important that we look at the other side of the coin.

What are the Deductions and Exemptions restricted to NRIs?

Unlike the US Federal Reserve, the Indian Income-Tax Act does not ask for its citizens to provide with the details of foreign investments in the form of FATCA.

When talking about foreign investments, we must get a clear idea of the ITR3 Form before the Income Tax Filing.

Returning to India: A Banking Checklist

Before settling permanently in India, consider completing the following:

- Convert or redesignated your NRE account wherever required.

- Review your FCNR and NRE fixed deposits before maturity.

- Update your residential status with banks, mutual funds and Demat accounts.

- Review nominee details and KYC records.

Evaluate whether an RFC account is suitable for holding foreign currency assets after your return.

3) After losing the NRI/RNOR status

When you return to India as an NRI, your NRI status expires after a limited period, and then you will become an RNOR on certain conditions.

Over time, you will lose your RNOR status also as and when you stop satisfying any one of the conditions mentioned for being an RNOR.

When you move out from RNOR and become an ordinary resident then even your global income will be taxed in India.

Suppose if your global income is taxed abroad, then you can claim the tax benefits as per the Double Taxation Avoidance Agreement.

Therefore, you will not pay tax twice for this global income after you return.

If you are planning to sell an overseas property or withdraw from overseas retirement accounts, it is advisable to do these when you are an NRI or RNOR to avoid taxation in India.

There are also many nuances in NRIs selling a property in India if it’s Agricultural land.

A detailed explanation is given below.

What Happens to Your NRE and NRO Accounts After Returning to India?

Returning to India also requires reviewing your banking relationships.

NRE accounts cannot be continued indefinitely once you become a resident under FEMA regulations and generally need to be redesignated into resident or Resident Foreign Currency (RFC) accounts, wherever applicable.

Your NRO account, however, can continue and may be used for managing income earned in India after your return.

a) What an NRI should do on return to India

What should be your next step after you return to India?

You should inform the banks!

i) On return to India, you should re-designate your bank accounts as domestic Resident accounts or transfer the balance in your NRE/FCNR accounts to Resident Foreign Currency (RFC) accounts, if you feel the need to do so.

ii) FCNR accounts can be continued till the date of maturity and upon maturity, can be converted to RFC accounts.

iii) Also, you need to open a resident Demat account, to transfer the shares from your NRI Demat account and should close the NRI Demat account.

iv) If you have invested in mutual funds as an NRI, then as and when you return to India, you need to update them with your resident bank details and change the residential status in mutual fund investments from NRI to a resident.

When talking about Mutual Funds, it is important to note that the taxation rules differ for NRIs. Refer below to get a clear picture of the Equity Mutual Fund taxation for NRIs.

v) What happens to the NRE FDs on returning to India?

vi) Can the returning NRI continue the NRE FD till maturity?

vii) Does the NRE FD need to be closed on return?

This is a common and important query about the NRE FDs on return to India. Let’s understand the problem with an example.

Siva returns from the US to India by September 2019, and the NRE FD that he holds will mature only by June 2022 i.e. after three years from the return to India.

Now what should Siva do about the NRE FD after returning to India?

When Siva approaches the bank regarding this query, a bank which is not properly instructed of the RBI regulations would give either of the two answers below,

The bank would either suggest Siva to continue the NRE FD as such until maturity which is a violation of FEMA and can attract serious retribution – or – the bank would ask Siva to prematurely close the NRE FD and open a new Resident FD which will attract penalty for premature closure of the NRE FD and also a reduced interest rate.

But as per RBI norms, Siva’s NRE FD account can be converted to Resident FD account without any penalty and without any change of interest rate and date of maturity.

The only change is that the interest earned will be taxed according to your slab if applicable.

As per the RBI Master Directions, upon returning to India permanently, the existing NRE FD account of the NRI account-holder is required to be converted to Domestic Resident FD account without any changes in the promised Rate of Interest.

The interest earned from NRE FD is not taxable, however after it is converted to a Resident FD the earned interest is taxed as per your income tax slab.

TDS will be deducted if applicable. But what about the TDS in Mutual Funds?

b) How long can I maintain my NRE account after returning to India?

You cannot maintain your NRE account and NRE FDs when you are an RNOR.

You need to convert your NRE account to resident account immediately upon returning to India.

You need to convert these accounts to resident accounts within a reasonable period of time.

The reasonable period can be assumed as 3 months.

If you have not converted the NRE account to resident account within 3 months, it would be considered as FEMA violation.

It is better to avoid those hardships and convert the NRE accounts within a reasonable period.

Even after becoming a resident if you continue your NRE account and FDs, then the interest from them will be taxable.

Similarly, if you are holding an NRE fixed deposit after returning to India, the tax treatment changes with your residential status.

Understanding what happens to an NRE FD after returning to India helps you avoid unexpected tax liabilities and remain compliant with RBI and FEMA regulations.

Interest from NRE account and FDs are tax-free only for non-residents.

And also, is TCS and TDS Applicable for NRE Account?

What’s the FIRST (and easiest) step you must take from the above as a returning NRI?

c) RFC Account

Resident Foreign Currency (RFC) is a Scheme approved by Reserve Bank of India permitting persons of Indian nationality or origin, who have returned to India on or after 18th April 1992 for permanent settlement (Returning Indians), after being resident outside India for a continuous period of not less than 1 year, to open foreign currency accounts with banks in India for holding funds brought by them to India.

Simply, Resident Foreign Currency (RFC) accounts are bank accounts maintained by Indian residents for Global-scale transactions in Foreign Currency.

Only returning NRI’s can open RFC account since it is specially established for NRI’s who want to bring their earnings in foreign currency from their overseas bank account to their bank account in India.

If you qualify as an RNOR, then the interest income from the RFC account is not taxable.

RFC accounts can be opened in different forms like current account or savings account or term deposits.

RFC Account should be opened before or after returning to India? Refer below for a detailed explanation.

d) Retaining Overseas Assets

It is not necessary for the NRI returned and turned Resident, to obtain any permission from RBI or any other authority to retain your overseas assets.

Section 6 (4) of FEMA has granted permissions for returning NRIs to retain the overseas assets.

This flexibility is especially valuable for NRIs who plan to continue holding overseas bank accounts, investments, retirement savings, or real estate while settling back in India, provided the applicable FEMA and income-tax provisions are followed.

If you (or a family member) forgot to declare an old overseas bank account, small investment, or asset in earlier Indian tax filings, a new scheme called FAST-DS 2026 gives a six-month window to disclose these foreign assets voluntarily without facing criminal prosecution.

This is worth knowing about before you finalize your RNOR-period asset planning, since unreported foreign assets after you become a full Resident can otherwise attract serious penalties under the Black Money Act, 2015.

4) Insurance

You should check if your previous insurance coverage, which you bought in another country, covers you in India.

If not, get solid health and life insurance coverage for yourself and your family when you return to India.

Following the COVID-19 pandemic, it has become critical to have complete health insurance coverage.

When it comes to life insurance, choose a term plan that provides high life cover with affordable premiums.

Read this article on how to choose the right term insurance plan for you to get more clarity.

Your homecoming journey will be smooth if you plan ahead of time and conduct adequate research on the best measures to take and things to buy.

5) Final Thoughts

To summarize, an Ordinary Resident (ROR) is liable to pay tax on his global income, while an NRI is liable to tax on the income ‘earned’ in India.

You may reap the above tax benefits until you claim that you are an NRI, but once you pronounce your residential status as Resident, you will avail no benefits and will be considered as a full-time resident of India and will have to follow the regular tax format.

Whether you are an NRI returning to India permanently or planning your move over the next few months, timely decisions regarding your residential status, bank accounts, fixed deposits, overseas investments, and tax planning can significantly reduce avoidable taxes and compliance issues.

That is you will enjoy NRI income tax benefits until the time you hold the NRI status in India.

What human resources do you have access to mentor your personal finance-related issues before and after returning to India…?

A Certified financial planner can make all the difference to your personal finances. Here’s a step-by-step guide to choosing the right financial planner for NRIs.

What is the one step you could take right now that would indicate you are moving forward in the right direction as an NRI…?

How about having a short discussion with a financial planner about your challenges and difficulties…?

To invest your savings properly and become wealthier after your return to India, you need a route map to take you from where you are financially and where you want to go financially.

You will have a clear route map only when you create a financial plan for yourself and your family.

Every returning NRI has a unique financial situation.

Reviewing your NRE accounts, resident account options, tax residency, investments, and retirement corpus before your RNOR benefits expire can help you transition back to India with greater financial confidence and fewer tax surprises.

I hope this article has given valuable insights about the tax implications for you as an NRI. Let us know your thoughts in the comment section.

If you want to create a workable financial plan, then I firmly vouch for you to take advantage of If you have any comments or questions, write them in the comment box below.

Or are you interested in creating a Comprehensive Financial Plan for your financial goals?

Skip the queue by registering for your 30 Minute FREE Financial Plan Consultation. Click the ‘Book Now’ button below.

I’m an NRI planning to move to India. What is the taxation when I sell my US shares held with an US broker?

Hi, Thank you for your article. I am from Singapore and planning to return India by 2025. I am doing trading and investment in US market (options and stocks).

Please advice me,

Can I still continue the same trading from India?

Do I need to close all account before retuning back to India?

Regards,

When your NRI status changes to resident and your NRE FDs are converted to residential FDs the interest from that financial year onwards is taxable, correct?

So can this taxable interest be declared and offered on receipt/cash basis, or do you have to declare it on accrual/mercantile basis?

Yes, the taxable interest from converted NRE FDs must be declared. You can choose to declare it either on a receipt/cash basis or an accrual/mercantile basis, depending on your method of accounting.

I hold OCI card and abroad since 30 years with few visits to India. Now retiring with pension from abroad. No Indian income.

1. If I returned to India in January 2025, would I get RNOR status for 2025-2026, 2026-2027 and 2027-2028? Or I do I have to move to India in April 2025 to qualify for 3 years RNOR from April 2025 until March 2028?

2. Do I have to stay minimum 182 days per calendar year (e.g. anytime in 2024) or does it have to be financial year (April 2025-March 2026 onwards).

Thank you.

You can book a Free Financial Consultation with one of our Financial Planners by using the following link:

https://www.holisticinvestment.in/complimentary-financial-plan-consultation/

This paragraph is truly a fastidious one it

helps new net users, who are wishing for blogging.

Hi Sir, very useful information. Thanks! However, I have a query not covered in your otherwise, nice article.

I have RNOR status for FY 2021-22 & 2022-23. For current FY 2023-24 my status is ROR.

I have a balance of Saudi Riyal 150,000/- ( received towards salary arrears & gratuity) in my overseas bank a/c till 31st March’2023, which for some banking issues in both countries, could not be remitted to my Indian a/c during my RNOR status. Moreover, despite my asking, my India bank neither convert my NRE a/c into RFC a/c to facilitate this transfer nor close NRE a/c . Now to bring this money to India,

1- Which a/c I should use ; 2- What will be tax implication ; 3- FEMA violation ?

Please help !

I returned to india in June 2023,after remaining NRI for 8 years 5 months.

[1] How I can claim tax benefits until three next years what is the procedure of it.

[2] my some amount is not paid by my foreign employer which will come to my indian account through my foreign account after 10 days whether the same also be taxable or it will be treated as income accrued and earned outside india

I am NRI Indian, preparing to return to India. This article is much helpful to plan ahead. Thank you

hey i have NRE account and fd i came back to India in the year 2020 and as it was covid period i could not convert my account so what should i do and by when can i convert my NREaccount to normal accounts

Thank you for this informative article. Do I need to request the bank to redesignate my account to resident account, once I return to India or is it done automatically? An officer in my bank told me I can keep the status until my passport expires which is after a year. Can you please advise what I should do?

I am an NRI and my husband is a PIO Canadian. If we return to India, will my husband who is not an Indian national also be taxed on his worldwide income?

If we were to stay in India for not more than 100 days a year, would we continue to remain NRIs and not get taxed on our worldwide income?

Hi,

I am a NRI over the past 25 years and planning to return to India in Septembwer 2024 to settle down permanently. I have NRE FDs jointly with my son – in some FDs my name is first and his second and in other FDs his name is first and mine second. He is still a NRI and will continue to be so for more years.

1. If my status changes, will the income from NRE FDs where my son’s name is prefixed be liable for income tax in India or only those NRE FDs where my name is prefixed?

2. I have not been in India for more than 729 days during the preceding 7 years.

3. How long can I remain as an RNOR?

Nice article. It gives very good clarity and would also be beneficial to bankers in giving right advice to their customers. I would like to bring to your attention to RNOR status assessment example of Mr Suresh. If the person worked abroad for 10 years and returned on Aug 31, 2019, I would like to point out that he most likely meets 10 out of 10 yesrs as NRI in the preceeding years (FY 2018 and prior) – not just 9 out 10 yrs, plus he most probably also meets < 729 days in last 7 years condition too. In the same manner, for FY 2020-21, the person may be meeting 9 out of 10 years as NRI in the preceeding years (FY 2019-20 and prior) rule too in addition to less than 730d in the preceeding 7 years, as FY 2019-20 is most likely the only year the person wasn't NRI). As you already mentioned, the person would have Ordinary Resident status for the next FY (2021-22) based on the number of days' stay during preceeding 7 years exceeding 729 days (FY 2020-21 and prior).

I wrote this comment just to give more clarity to readers on RNOR assessment.. Your views please.

Your points regarding the RNOR status assessment for Mr. Suresh are absolutely correct. Here’s a breakdown of his situation:

FY 2018 and prior:

Mr. Suresh most likely worked abroad for the entire period, fulfilling the 10 out of 10 years requirement for NRI status.

He would also satisfy the less than 729 days in India condition for these years.

FY 2019-20:

As he returned on August 31, 2019, he likely wouldn’t qualify as NRI based on the number of days spent in India.

However, he would still meet the 9 out of 10 year requirement for NRI status considering the preceding years.

He would most probably fulfill the less than 730 days stay in India condition for this year as well.

FY 2020-21:

Similar to FY 2019-20, he wouldn’t be considered NRI due to exceeding the 182-day limit in India.

However, based on the preceding years (including FY 2019-20 where he wasn’t NRI), he would likely meet the 9 out of 10 year requirement.

He would also satisfy the less than 730 days stay in India condition considering the previous 7 years.

FY 2021-22 onwards:

Since Mr. Suresh would have stayed in India for more than 729 days in the preceding 7 years (FY 2020-21 and prior), his residential status would become Ordinary Resident as per the rules.

Your comment effectively clarifies the RNOR assessment process for readers and highlights the crucial factors to consider, especially regarding the preceding years’ residency status.

I am returning to India in Jan 2023 after 6 years in US. I have NRE account and NRE FDs. Few questions:

1. Am I required to close NRE account immediately after returning back ?

2. Some of the NRE FDs will mature in Sep/Oct 2023. Can I continue them until maturity (tax-free) ?

3. Does RNOR status allow me to continue using NRE account/FDs ?

4. I have some RNOR FDs as well, can those be continued till maturity (Nov 2025) ?

No, you don’t need to close your NRE account immediately, but there are some actions to take upon returning to India:

NRE Account:

You aren’t required to close it immediately, but you need to convert it to a Resident Savings Account or a Resident Foreign Currency (RFC) account within three months of your return.

RFC accounts allow holding foreign currency deposits and offer some repatriation benefits.

NRE FDs:

You can continue existing NRE FDs till maturity. However, the interest earned from the date you become resident (Jan 2023) will be taxable in India.

RNOR Status:

RNOR (Resident but Not Ordinarily Resident) status offers some tax benefits, but it doesn’t allow you to continue with NRE accounts/FDs. NRE accounts are for Non-Resident Indians.

RNOR FDs:

You can continue existing RNOR FDs till maturity (Nov 2025).

Hi

Very informative article. I have a question in this regard.

If the spouse was working abroad and had NRE fixed deposits in her name and later she left the job and was a house wife (abroad) and the husband has invested in NRE FD in her name in India, while they were residing abroad. If they decide to return permanently to India, will they be taxed separately for their interest on FD or will it be clubbed with the Husbands tax returns.

Yes, they will be taxed individually.

I am an NRI since 1995 and will be returning to India in November after staying 184 days abroad. My total stay in India for 2022-23 FY would be 181 days. So as per rules, I am supposed to maintain my NRI status for FY 2022-23.

Q1. Am I right in the above understanding?

Q2. Will my NRE FD interest from Nov-22 to 31 st March 2023 be taxable?

Q3. For FY 2023-24, I shall be considered as RNOR as I have been NRI for the previous 10 out of 10 years. Right?

Q4. For 2024-25 also I should be considered as RNOR as I have been NRI for the past 9 out of 10 years. Am I right?

Best Regards

Hi! Yes! You are right for Q1, 2 & 4. Q2 – Yes, Taxable.

Hello Sir, I will be returning to India in April 2023 after leaving outside for 22 years. I have NRE Fixed deposits for 10 years matured in Oct 2025, as a normal practice I want to move these NRE FD to resident FD with in 3 months. Since I opt the return of Interest after maturity date, is it I need to pay tax for this entire 10 years interest, in these over all Deposit period year 2015 to 2022 till March my status is NRI,

Pls advice

Hi!

Once you return, you need to redesignate your FDs as redesignation. Then on whatever the interest is getting accrued, that is taxable.

I went to Uganda in 2010 for a job in an African Bank. In Nov, 2021, I came back to India permanently. I remitted app. 10000/= usd to my indian NRE account in October 2021. When I came back to India, I converted my NRE account into domestic savings account. Do I need to submit any Return for 21-22 FI ? I do not have any other income or Deposit. Please guide me.

If you qualify as an NRI, then your overseas income is not taxable. If you qualify as Resident then your overseas income also taxable.

Hello, and thanks for an interesting article.

I am an NRI for the last 15 years and plan to return in early 2023. I could return in March 2023, which is this financial year OR I could return in April 2023, which is the next financial year. I only have NRE account, NRO account and FDs in India.

Please let me know if any one of the return months is more advantageous to me as far as my RNOR status and taxation is concerned.

RNOR status will help you get tax exemption for your overseas income. There is no special benefits for RNRO on NRE, NRO FDs. NRE, NRO and FDs are taxable the moment you return regardless of you or RNOR or ROR.

Very good information. I have some queries regarding Tax. Currently I am living in Thailand and paying income tax in Thailand. My question is when I will return to India what are the document needed regarding Tax ?

It is better to keep the Tax filed documents to avoid unnecessary problems in the future.

Hi Thanks for the valuable info. I plan to return to India in 2022. On arrival I want to sell one property and buy another of equal value. As a NRI of 10 years, will 20%+ capital gains tax on Transaction amount, be withheld by the buyer of my property (I sell) (as I would be RNOR for two years, until 2024)? I would like to become a resident immediately on arrival to avoid this deduction as most buyers don’t want to deal with this withholding.

Also can i apply for Adhar as resident, as this is my intention?

You have to fulfil anyone of the following conditions to become a Resident Indian.

i. If you are staying 182 days or more in India.

ii. If you are staying 365 days in India during the previous 4 financial years and 60 days in the current financial year.

I am a NRI retiring to India shortly to reside there as a Resident.I have a NRE account with the following names:-

Aloysius Dias. ———Father

Louisa Dias ——-Mother

Domnic Dias ———-Son

CAN DOMNIC DIAS KEEP AND MAINTAIN THE NRE account, after we two have changed to NRO or domestic account.

Hi! It is depending on the son’s residential status.

Hi,

This is a very comprehensive and interesting article. Thank you for all the efforts to consolidate the information in 1 place.

I want to understand a scenario with an example:

1) I need to I understand that an NRI/RONR can have global income tax free for up to 2 years which also includes the global income remitted to India.

2) You mentioned i should convert my NRE/NRO account to domestic at the earliest after landing in India (preferably 3 months).

Example: I sell my global investments and transfer funds in my Indian bank account (NRE/NRO) in INR (lets say INR 5cr). Then I visit India for good and convert NRE/NRO account into domestic account and since Interest income in the domestic account is taxed at the regular Indian income tax rates, won’t the interest earned on INR 5cr be taxed?

If I have misunderstood or misaligned concepts then pls suggest the practical way of parking (INR 5cr) in this case in the regular domestic savings account (until I decide to invest the funds further into real estate/ shares/ FD’s etc.)

Hi!

Yes, the interest will be taxed in India. As for the personalized investment plan, you can make use of our 30 minute complimentary financial plan consultation to consult our financial planners.

Please click the link to get your appointment.

https://www.holisticinvestment.in/complimentary-financial-plan-consultation/

Thanks for the excellent article .

I have been living in Finland since Jan 2014 and have had NRI status since then. I am planning to move back to India permanently in Jun 2022 and taking up employment in India starting July 2022.

1. Would I be taxed in India for Finland income earned from Apr 2022 to June 2022 ?

2. What would be my residency status for FY 2022-2023? I guess it would be RNOR ?

3. I have some NRE FDs which are maturing in July/Aug 2022 ? Do I need to pay tax in India on the FD interest ?

Since you are returning to India June 2022, you have three months to convert to covert your NRE account to Resident Account. But since it is mature within 3 months, you don’t have to pay tax for it.

Sir at some places you mentioned from the date of arrival in India you have to pay tax on your NRE FDs, and here you mention 3 months grace period after arrival. Which is correct?

The correct rule regarding taxation on NRE (Non-Resident External) Fixed Deposits upon returning to India is as follows:

Immediate Taxation: From the date you become a resident of India (typically the day after you complete 182 days in India in a financial year), the interest on NRE Fixed Deposits becomes taxable.

Grace Period: The 3-month grace period typically refers to the time given for you to inform your bank of your change in residential status. However, this does not affect the taxability. For tax purposes, the interest becomes taxable from the date you qualify as a resident, not after the grace period.

So, interest on NRE FDs is taxable from the date you become a resident in India.

Hi ,

After my marriage in dec 2015, I moved to the UAE, I was working in UAE since 2018 and had a NRE account in india. I left my job on 31st mar 2021 and was in india for 7 month in the current financial year. I have also join an Indian company for work.

As it allows me to work from home, I came back in UAE and am living with my husband now.

I have couple of queries now

1. What happens to my NRI status

2. should I convert my accounts to RNOR/resident.

1. Since you have stayed more than 182 days in India in the current financial year, then you will be considered a Resident Indian.

2. You need to redesignate your NRE / NRO accounts to resident accounts.

Thanks so much for the informative article – Very helpful.

On a different note, can I do an international wire transfer from abroad to some one else’s account in India? Is that allowed or does it attract any fees/penalties?

Glad that we can help you.

As for your question, you can transfer the amount to anyone’s account in India. No fees. But Tax liability need to be checked based on the context for the transfer.

nice blog very Informative

Thank you

Loved this and Very good article, I have the below query. I am coming back to India on 31 march 2022

1. I have a 10 year FD , 9 years completed and 1 more year to go. If I convert this to Resident FD, I read here I may get the same/maintain interest rate. So will TDS be applicable only for last year as only 1 year is pending and 1 year is resident . Will bank system mess up at maturity?

2. I have overseas capital gains accrued, is it better to sell and book capital gain and make fresh purchase before coming to India to book & reduce capital gain liability ( Currently I have capital gain with 0% taxed UAE).

3. What is the penalty for Delay in notifying by 6months. I prefer inform bank after staying in India for 180days, that way I can save some FDs (just woried if I inform bank they mess up TDS and interest rates). Thanks if you can help

1. Same interest rate applicable. TDS for the last year is applicable.

2. Yes

3. It is a violation of FEMA regulations.

Hi ,

Thank you for such nice article.

I have been in US for last 7 years. Now I am planning to return to India permanently. Now my questions are.

1. What do I have to do to convert my NRI status to RNOR?

2. As per article I can benefit from RNOR for 2 yrs and I need not to pay taxes in India on my overseas income such as dividends and capitol gains from mutual funds in my overseas investments. But do I have to pay taxes in USA for those incomes?

3. I have overseas investments in shares, mutual funds and 401K. How long can I keep them in USA?

1 You can’t get converted from NRI to RNOR. You need to qualify based on the conditions given in the article as RNOR when you return,

2 If your residential status is RNOR, then you don’t have to pay tax for the income you earned outside India but you have to pay tax on the respective countries.

3. You can keep your overseas investments as long as you want. After RNOR period, those investment returns will become taxable in India.

As for personalized investment suggestions, you can make use of our 30-minute complimentary financial plan consultation to consult our financial planners.

Please click the link to get your appointment.

https://www.holisticinvestment.in/complimentary-financial-plan-consultation/

Iam a 53 year old NRI for the past 20 years who is returning back to India permanently due to loss of job. So far I have saved 4cr as FD with an average rate of ineterst for 5% and still have to meet the additional expenses towards higher education of my 2 childern for the next 10 years as well as medical expenses in addition to leading a decent life. My only source of income will be the interest earned for the above FD. What would be my tax liability? What are the resources to reduce the taxes to facilitate a decent life.

Hi!

For personalized advice, kindly make use of our 30-minute complimentary financial plan consultation and consult our financial planners.

Please click the link to get your appointment.

https://www.holisticinvestment.in/complimentary-financial-plan-consultation/

Hi,

I hold NRE savings and FD accounts with HDFC bank. The tenure of FD is 3years started in 2018, at present 2 and half is completed. Now I returned back to India and I want to know once my stauts is changed to Resident, The total interest earned on FD maturity is taxable/only proportionate interest earned since my stauts changed to till maturity period will be taxable. what will be your best advise. Also HDFC bank not providing any interest certificate for accrued and paid interest against NRE FD’s. Whereas SBI is providing interst certificate for accrued interest and paid interest during FY for every NRE FD’s receipts.

Thank you.

The proportionate interest after you have returned is taxable,

Very nice and informative. Highly appreciated.

Thank you

From 2003 till June 2020 I was working abroad and had NRI status. Since I have stayed for more than 182 days in FY20-21 I have the following queries

i) What is my status i.e RNOR or ROR

ii) What happens to my NRE & NRO banks account

iii) What happens to my NRE bank FD

iv) What happens to interest accumulated on the NRE bank FD’s that are more than 1 year old and for FD’S less than 1-year-old.

1. Your residential status will be determined based on your stay in India from 2003 to 2020.

2. Once you return to India permanently, then you need to convert your NRE account to a residential account.

3. You need to convert your NRE FD to resident FD.

4. Interest accumulated before conversion is tax-free. After you convert, whatever the interest getting accrued is taxable.

Can we transfer money from NRE account to normal account of parents or wife? Can I invest money in MF, Stocks, property etc from NRE account? Any tax implications

Yes, you can transfer to normal account. You can invest from NRE account.

Dear,

We are in Gulf for more than 10 years, and planning to return to India in may 2021 for good. My wife was working few years back but currently house wife. We have both separate NRE accounts and PAN cards. I understand that we need to convert our NRE account/FDs to resident account with in 3 months after we return.Now my question is when we return to India, can we file a income tax separately or her income (interest) from her FD will be clubbed to my income.

Regards,

TG

You need to pay income tax individually.

Hello. I have been working in India. I came to Uk in July 2018 and returned back to India in April 2019. For FY 2018-19 I was given NRI status in India. For FY 2019-20, will I be considered returning NRI and given that tax treatment or ROR? Pls help explain. Have foreign bank account, do I need to pay tax on it in India?

You will be treated as a Resident.

Hi,

Thanks for the article. I have been living in the UK since 2004 (have a British passport, OCI) and plan to return to India permanently in 2022. I have been going to India every now and then for few weeks. In 2018 and 2019, I went to India 3-4 times in total for 1 to 3 weeks. I put a NRE FD in Dec 2020 till June 2022 thinking I’ll need to convert my account to resident straight away. I had some questions:

1) Was I wrong in thinking that I’ll have to convert my NRE account to normal resident account straight away (say in July 2022)? or do I have 1-3 years to keep using NRE account, FDs? If so, how long do you think?

2) I was thinking of doing more NRE FDs but the minimum time for NRE FD is 1 year so can I still put NRE FDs (without having to change to Resident FD) of 2-3 years if I decide to move to India in July 2022? How long maximum can I put it for and keep it as NRE FD (without any tax)?

3) I don’t plan to work in India at all after moving. My only source of income will be through fixed deposits. Am I right in thinking I’ll still need to convert to resident account or can I keep it as NRE forever since I have a foreign passport and will not be having any source of income except FDs?

Many thanks.

Hi S Shah,

There is nothing wrong with converting your NRE FD to resident account. So what you are thinking is right. But there is no option to keep your NRE FD to 1-3 years. You need to convert your account immediately.

You can put more FDs. But need to redesignate your NRE FD to the resident account after your return to India. Also, the interest you earn from your FD is tax-free until you hold your NRI residential Status.

Instead of investing in FDs during this time frame, you can invest in Income Funds with better tax benefits.

Hi, i will return to India next year December 2021. I will keep my earning in USA savings account

Once my status turn from NRI to normal resident. And then i want to transfer my earnings to India, will it become taxable? How to avoid?

Yes, Will not be taxed.

Hi. I was in Qatar for almost 7 Years 6 Months. I returned back to India permanently by November, 2020. I have NRE and NRO account in India.

I dont have any investments like FDs, etc in India. I dont have any income from overseas also.

Let me know what is my immediate action.

Hi Kamaraj,

Since you have no investments in India and Overseas, all you need to do is change your NRE and NRO account to domestic account.

I will be coming back to India from US around July 2021. I don’t have any existing Indian bank account. I wanted to transfer some of my US savings to an Indian bank account (new) before i return.

1. Wanted to know is NRE the account i should be opening and transferring the funds? is that taxable, how can i use it once i come back to India? Can i keep it open and keep withdrawing till 0 balance or shutdown? Is it taxable at any point later after i come back to India?

3. Plan was to have another regular Indian savings salary account for earnings i make in India.

You can apply for NRE or NRO accounts to transfer your money.

After transferring your money to your NRE account, the interest you gain for that account is tax-free. Also, if you want to transfer your money overseas before you return to India, you can do that easily from NRE account. Money in your NRE account is repatriable.

But once you return to India, you need to convert your NRE / NRO account into domestic account within 3 months.

Once you convert your NRE account to domestic account the interest you earn from your savings will be taxable.

As for NRO account, you need to pay tax for the interest you earn from your money. Also, you cannot easily repatriate the money to overseas if needed

I have returned to India due to a job loss from the UAE in the month of October 2020. I was in UAE from 2015-2020 but now planning to settle in India permanently. I have one NRE account maintained in one of the nationalized banks and holding one NRE FD as well.

Please suggest me for the account conversion if required. I also wish to know if I am liable to pay the income tax or its return for FY20.

Yes, you need to convert your NRE FD and SB. You will be taxed based on your Residential Status and the income you earned in India.

I recently came back to India on 25th October after being in US for nearly 6 years.

I know I have to convert my NRO/NRE account to resident savings account.Once I convert my NRE account to resident savings , will it be subjected to tax?Any way to get tax benefit on NRE account

Yes, you will be taxed. But you can get tax benefits by using Tax saving schemes.

Exceptionally well written article. Congratulations!

I have been working outside since Sep 2014 and expect to return back permanently in Feb 2021. Have the following queries:-

1. I spent about 20 days in India so far during this FY. Should I go out of India again in Feb/ Mar 21 and return in Apr 21 so that my NRI status remains for the whole FY 20-21. I am assuming that if I do that, then my RNOR status will continue till 31 Mar 24, instead of Mar 23 which would have been the case otherwise. Is this a correct assumption ?

2. I have FCNR FDs which are due to mature in Dec 21. Will I be able to keep the FDs till maturity and if so will there be any tax liability despite my RNOR status?

3. Once my foreign currency funds are transferred to a new RFC account, will I have to give any reasons for repatriating money out of the account abroad?

Thank you.

1. You are already NRI for FY 20-21.

2. FCNR FD interest is not taxed during your RNOR status..

3. No.

Hi,

I am working in UAE from June 2019 and I didn’t visit India since March 2020. I have NRE account in India and transfer my overseas income in the same NRE account on regular basis.

Now I am moving to India permanently but will be working for the same UAE employer from India. So I want to know

1) What will be my resident status for FY 2020-21?

2) Till when I can use my NRE account?

3) Can I receive my salary in my NRE account from UAE employer? If yes, will it be taxable?

4) Can i open a saving account in India in 2020-21 and transfer money from NRE account to that new account?

Please help me with these queries.

1. If you are coming back after OCT 3, then you will be NRI – otherwise resident

2. You need to convert your NRE account to resident account immediately on your return. The reasonable period is within 3 months.

3. Taxable

4. Yes, you can. Or you can simply convert your NRE account to Resident Account.

I worked in UK from April till Dec and returned permanently to Ind in dec. What will be my resident status for that FY.

You will be considered as NRI.

I went abroad for employment for the first time in July 2018, I returned back to India in June 2019.

For FY2018-19 I filed tax as NRI.

For FY2019-20 what is my resident status ? and which ITR form I should use ? and should I declare my foreign salary income ?

For FY 19-20, you will be a Resident Indian. Yes, you should declare your foreign income while your file your income tax.

I am planning to come back to India in Mar 2022 after 30+ years in Middle East. What I understood is that my NRE-FD’s i will have to convert to Res FD’s & pay Tax on interest which was earlier exempt of course subject to Resident status. In my case since I will come Mar 22. for FY 2022-23 Tax will be applicable. Will there be TDS on Resident FD Interest?

I have a child studying in the US. I wish to retain some Dollar Fund even after becoming resident where I am not restricted paying the fees by RBI rules after becoming resident. Is it possible

Yes need to pay tax for the FY 2022-23.

I have left india on 2013/2 on project and return to india on 2020/3, after a span of 7 years , i am currently not able to return abroad due to lack of flight and i hold a NRE acccount and NRO account , i pay tax for my oversees job in that country which will expire in 2021/07, I do maintain some FD in my NRE account . i have already filled ITR2 for 2018-2019 and 2019-2020 FY’s as NRI , I want to know incase if i am not able to return aboard, how long I maintain my NRE account status? is it 2-3 years? what should i do to my NRE and NRO accounts and can i renew my mature FD’s at this point of time? please do advise me

The moment you become a Resident, you need to convert your NRI bank accounts and deposits into resident accounts.

After 23 year nri (UAE) in December 19 came back to india . Was planed to go back in march 20 again, due to covid 19 now decied to stay in india. How long i can keep my NRI status? If not what i should do? What ITR should i file? Your contact number? In case need assistance in filing itr.

You will not be able to retain NRI status. Your eligibility for RNOR is to be decided on your visits during previous years.

Hi, I am working in Netherlands since Dec 2017. I want to move back to India in June 2020. Will my foreign income earned in April 2020 and May 2020 be taxed on India?

Yes

Hi,

I went to UAE in July 2019 for work and got the resident visa. However, I came back to India in mid Sep 2020 permanently. What will be my residential status and what will be the tax implications?

Can double tax treaty agreement between India and UAE help me out in avoiding the taxes, if any? Also, if applicable how much tax will be deducted over my salary earned abroad?

You will be Resident for FY 2020-21 and taxed in India.

Hi , the article is really very good .

I came to india on 27th March 2020. During COVID I thought I should not go back to abroad and make my mind to be in india .

My question is during the year 2019-2020 , I stayed only 31 days and during the year 20-21 once I will complete 182 days ( May be 30th sept or 1st October ) and I will inform the bank . I have FD from NRI account . Am I doing right thing as recently I have decided not to return .

2) The bank will deduct TDS FROM oct 20 and while filling return I have to pay Tax from October 20 to March 21 and I will get the proportionate deduction under various sections.

Will be great if you please highlight this.

You have to change your NRE account to Resident Account within 3 months of your return.

Hi, returned from US in Aug2019 , paid taxes for full salary (Indian+US) as the company deposited everything in $ . After return to India in Sept2019, was taxed from April till Aug 2019 (5 months) for Indian component salary as i have become resident Indian , is this double taxation? is the tax paid for 5 months can be claimed under DTAA ? if yes how to do it?

Hi! You can claim tax benefits. For more information, you can take advantage of our free complimentary financial plan consultation and talk to our financial planners regarding your personalized advice.

Get your appointment here: https://www.holisticinvestment.in/complimentary-financial-plan-consultation/

Hi,

I am NRI living in Sweden since July 2015. My question is:

In case I return back to India (permanently) anytime between April 2021 to Sept 2021, then my stay in India will be more than 182days for FY 21-22. In this case, should I be paying taxes in India for the earnings I made in Sweden between 1st April 2021 to the date I landed in India?

No don’t have to.

Will the tax on interest of NRE FD’s be deducted on Pro-rata basis, i.e. the interest for NRI status period will be tax free and after becoming Resident it will be taxed OR will the whole amount of interest will be taxed.

Pro-rata Basis

hi

thanks for sharing valuable information.

my uncle was working in dubai. after his retirement he came to india permanently on oct 2018

he is hold NRE and NRO account in nationalized bank yet because of fd’s maturity in jan 21

kindly suggest me the NRE account fd interest taxable or not for f.y 18-19 & 19-20 .

if no then where i show the interest income of these fd account

thanks

After returning, he should have redesignated to Resident FDs. Interest earned after return is taxable.

I have been in UAE from Feb 2013 through 31 Jul 2020, returned finally to India on 1 Aug 2020. My questions are-1) Will I be RNOR for F/Y 2020-21+ 2021-2022 and my salary of Apr 2020 be tax free in India ; 2) Is there any point in opening RFC account because there is no foreign income now and I don’t need to send foreign currency anywhere, if yes then how can I transfer INR from NRE to RFC without loosing on conversion to foreign currency; 3) What is the current definition of NRI, is it 182 days or 245 days out of India?; 4) What if the bank does not know the RBI rule that NRE deposit can be simply converted to resident FDs with same rate of interest and maturity date?

Hi, for NRI financial planning, you can take advantage of our free complimentary financial plan consultation and talk to our financial planners regarding your personalized advice.

Get your appointment here: https://www.holisticinvestment.in/complimentary-financial-plan-consultation/

Sir, I shifted to Dubai in July 2019 and have been in employment since then. I am looking to return to India in 1 st Nov, 2020 for a new employment. What will happen to my income earned in Dubai since April, 2020 – 30 th Oct, 2020 – will it get taxable in India. How can I save such taxes if applicable.

No, you will not be taxed in India.

I am a nri, returned to India in April 2017 after 25 years employment.

I have nri deposits. Interest is the only revenue.

What’s my Residential status for IT purposes for the FY 2017-18,2018-19 and 2019-20

You need to redesignate your NRI FDs into resident FD immediately after returning and interest will become taxable.

I have been a NRI since 1995 and will be returning to India in January 2021. I believe that I will be NRI for AY 20-21 and NROR for AY 21-22. Currently I have money in my bank accounts in Dubai and Singapore. By when do I have to transfer this money to India without any tax implication in India. I also have property in Dubai for which I receive rent, I understand the rent received till AY 21-22 in Dubai and transferred to India will be tax free – is that correct? I will also receive substantial end of work benefits from my company who have deposited these funds with Generali International in my name which I can receive after my retirement in December 2020. These funds are based on my service with the company internationally (I am an NRI for those years). If iI receive this money in India in the AY 21-22 as a lumpsum is this taxable in India?Thank you for your advice.

Hi, for NRI financial planning, you can take advantage of our free complimentary financial plan consultation and talk to our financial planners regarding your personalized advice.

Get your appointment here: https://www.holisticinvestment.in/complimentary-financial-plan-consultation/

Suppose I have a property or shares outside India and declared their worth (Don’t know how to declare ?) and if I sell them after becoming a Resident, then the Capital Gains only Taxable (If its not taxed in the other country) or the total money received will be taxable ?

Once you become a Resident Indian, then you need to pay tax for the income you earned outside of India. So, you need to pay tax for the gain.

Hello, I am working in Dubai since 10th April’18 and employed in Dubai with residential visa. Now i am planning to return back to India by 7th Oct’20.

Prior to April’18, i was totally living in india.

Now my question is whether my income earned in Dubai for the period of 1st April’20 to 7th Oct’20 will be taxable in India or not.

The NRI law as per section 6 to determine residential status is confusing to me as it does not states anything about an NRI retruning back to India.

No, your overseas income will not be taxed in India as you are an NRI.

I would like to know if I am returning to India from the Middle East after working for 20+ years can I retain my foreign bank account. Also I have investments in foreign markets. Should I be closing these trading accounts before I move back or can I continue to invest in overseas markets using my foreign bank account. Also what are the implications of retaining foreign bank account and what happens (tax implications) if I transfer moneys from these into my resident savings account (redesignated NRE accounts) as and when needed after I turn resident.

Hi, for NRI financial planning, you can take advantage of our free complimentary financial plan consultation and talk to our financial planners regarding your personalized advice.

Get your appointment here: https://www.holisticinvestment.in/complimentary-financial-plan-consultation/

Hi,

I am working in UAE from June 2019 and planning to come back in India in mid September,

Shall I be applicable for global tax ?

You will become resident and will be taxed in India

Hi sir,

I am working in Saudi Arabia from April 2018 to till date (July 2020). Now i am planning to move India end of July 2020.

Kindly let me know my NRI status FY 20-21.

Am i required to pay earnings in Abroad.

Am i eligible for RNOR Status.

For FY 20-21 -You will be a resident.

No. You are not eligible for RNOR status.

I started working in UAE from 1st April 2019 and will work up to 31st July 2020 .

I want to return to India now, will my UAE salary income be taxable in India when I return to India in August?

Income earned during April 20 to Jul 20 will be taxable as you are turning resident.

I am staying in singapore since April 2013 till now and returning back permanently in 1st October 2020. What will be my status NRI or RNOR? Is the income between April 2020 to 30th sept 2020 taxable in India?

Need more details to answer this. Please share number of days you have visited India during your NRI period. So that we can check your eligibility for RNOR.

Hi,

I can to UAE on work visa in Dec 2016.

Every year I spend around 30 days in India.

I am planning to return to India permanently in Oct 2020.

Will I be considered as NRI for FY 20-21 ? Will my foreign income be taxable in India if I convert my accounts to ordinary accounts once I am back ?

Thanks

If you are returning on or after on or after 3rd October, you will be considered an NRI.

But once you become a Resident Indian, then you need to pay tax for your overseas income.

Hi

I’m abroad for 10+years for job with MNC. Due to my office/personal travel, I stay in india as follows.

14-15-80 days

15-16 -100 days

16-17-77 days

17-18 -180 days

19-20- 130 days

All these years i’m NRI. For Fy 2019-20 IT submission now, Am I an NRI? as changes have been introduced.

Your residential status will be NRI.

I have been working in UAE since Sept 2014 and now wish to return to India in August 2020. Will my overseas income be taxable in India (April 2020 to July 2020). In last five years , i stayed in India around 200 days.

If your residential status is an NRI, then your overseas income will not be taxed in India. If you become a resident it will be taxed.

Hi sir

From 2017 i am Working in abroad (u a e) my savings deposit to my NRE account, 2020 jan i want return and settle in india

That savings(NRI account( taxable in india

The money you earned from abroad is not taxable in India. But once you settled in India. You cannot maintain your NRE account. You need to convert your NRE account to resident account immediately upon returning to India.

The reasonable period to convert your account is 3 months. If you have not converted the NRE account to resident account within 3 months, it would be considered as FEMA violation.

Even after becoming a resident if you continue your NRE account and FDs, then the interest from them will be taxable. Interest from NRE account and FDs are tax-free only for non-residents.

Hello Sir,

If I sell my foreign property , after I lose my NRNO status and if I repatriate the sale proceeds, would this be treated as income and taxed in India or only capital appreciation tax will be applicable.

In my case, the sale will result in capital depreciation. In this case, can I get benefit of capital depreciation to adjust against India taxes in the current financial year and balance carried forwards to the subsequent financial years.

Yes, you will be taxed in India for the appreciation.

Hi,

I have been working in Singapore for last 25 years. I am a Premanent Resident of Singapore. I plan the live in India. I plan to hold my property and investment in Singapore. For retirement I plan to live of the rental and dividend earning from my investment in Singapore. I will be paying tax in Singapore.

May I know how I will be taxed in India?

Thanks

Sunil

Hi! Once you become a Resident Indian, then your global income will be taxable in India. However, DTAA will be applicable.

I stayed in Gulf for 14 years and planning to return on 30-07-2020. I have NRE FDs (>5cr) in four nationalized banks. I would like to continue NRE FDs which are maturity date is before 31-03-2021 (IT finical year). Other FDs to re-designate to resident FDs which are maturity date is after 31-03-2021.

Will convert the NRE savings accounts to resident savings account in the March 2021.

Is it legal as per IT act ?. Please advise.

Hi Srinivas,

If you are planning to continue your NRE FDs till maturity, then it will consider as violating the FEMA. But you can convert your NRE FDs to Resident FD till your FD matured without any reduction on your interest. But the interest you earn from your resident FD is taxable according to the Indian Income Tax law.

Hi,

I am currently an NRI planning to return to india for good in July 2020.

Where would you suggest I transfer my savings (I’m india) currently held in a bank a/c outside india?

Please check with your financial planner.

You can also book a slot with our financial planner for an initial complimentary consultation.

https://www.holisticinvestment.in/complimentary-financial-plan-consultation/

Hello Sir, thanks for the kind information.

my situation is I am OCI holder, planning to return to India from Canada after 17 years Aug 2020, I have Canadian bank accounts and retirement savings accounts in Canada and NRE accounts with Indian bank, what happens to my interest gained over the Canada accounts after I return, should I transfer to INR or can I leave them, also can I leave retirement savings plan from Canada, Please advise how do I file taxes in India.

Regards

Venkat

During your RNOR period, your overseas income is not taxed in India. After RNOR period it will be taxed in India based on DTAA.

Hi,

Thks for the informative article!

I am an NRI in UAE for more than 20 years. I would like to know if on my permanent return to India in case I decide to (1) sell my residential property in UAE & (2) redeem my fixed-interest bearing National Bonds after expiry of my NRI / RNOR status, will I be taxed on only the Capital Gains (if any) or on the total sale/ redemption proceeds (as wealth tax)? Also, will it make any difference in taxation if I transferred the proceeds to India or kept them in a UAE bank account?

I assume that there will be no taxation on above if it is done while I am NRI or RNOR.

You are right!

Thanks for the information.

I was in US for 3 years and now returned to India 9 months before. I still hold some cash in Bank of America and Employee stocks, 401K in US. Do I have to pay tax in India if I have to transfer those to India ? (These are earned in US and I’ve payed Tax in US)

Is there a time limit should I transfer before it get taxed in India ?

I HAVE CAME TO QATAR FOR JOB ON 13 NOV 2019 TILL DATE(4-4-2020. TILL THEN I WAS STAYING IN INDIA. I AM QATARI RESIDENT SINCE 13 NOV 2019.

WILL MY STATUS BE NRI?

Yes

Sir

Exhaustive details. Thanks for the article. I have the below question.

Fiscal Year No of Days in India NRI Status

2014-15 120 NRI

2015-16 200 RNOR

2016-17 100 RNOR or NRI?

2017-18 90 NRI?

The question is if you become a resident in one year or two years continuously and then if you dont stay for more than 180 days in the next coming years, how those years will be considered? Can one change status from RNOR to NRI? Can one exceed the 180 days in one year and continue as NRI starting next year? Please answer

Thanks

Rajan

Hi, thanks for your article. few questions

1) I left India 13 years ago, and an in transition right now, so plan to be in India till I figure next move. Can I stay 181 days in India fy 20 and 181 days in fy 21 and remain NRI ?

2) Incase one was to return to India permanently ?, overseas assets declared to income tax will have scrutiny ?s asking for details of 13 years income etc ?..as suddenly assets would be higher versus 13 years ago

3) and those overseas assets after turning resident all normal resident like taxation…?..for example capital gains is 10-15% in India …but if money is Hong Kong capital gains is zero there….so lower rate will apply ? given India has DTAA with Hong Kong ?

thank you so very much !

“1) Yes you can.

2) All you have to do is to provide the related documents. Show the overseas investments in your IT filing.

3)During your RNOR period, the Capital gain from Overseas investements will not be taxed. However, after that, it will be taxed in India”

I first time came to UK for employment purpose in November 2017 and never came back to India till date.

I am planning to come back India permanently in December 2019.

I have below quries.

1.what will be my residential status for F.Y 2019-2020?

2. Will my foreign income taxable India for year for F.Y 2019-2020.

1. Your Residential status for FY 2019-2020 is Non-Resident.

2. No, you do not have to pay tax for your income generated overseas till you return to India (i.e. till DEC 2019). But you will have to pay tax in India for the income generated between your return to India-Dec 2019 to Mar 2020.

Hi

Recently I will receive my citizenship in Australia, now my question is can I still keep my NRE account in india and help my parents in india from the interest received from FDs. How long I can do this ? And is the money can be repatrative to Australia in futer.

Yes, you can have NRE account and repatriate.

Hi,

1. I returned to India on August 16 2017 and was out of India for two months (US/other countries visits). I filed taxes RNOR status this year. In above article, it says I can use RNOR status until 3 years. But two conditions above mentioned above (729 days) considers RNOR status for only two years. Where can I find reference for 3 years?

2. When I have to show rental income outside India, what deduction can take before taxation? e.g. US rental income 25000, actual income after actual deductions (property taxes, maintenance work, HOA, home loan interest) is only 5000. What should be my taxable income? I hope I don’t have to pay taxes on 25000 because I did not get that money in my hand, and is not reasonable.

3. Capital gain from US – I pay management fees, shouldn’t I be allowed to deduct it before taxation? I hope so.

Please let me know. Your help is greatly appreciated.

Regards,

Manju

“As per your questions,

1. We cannot calculate how many years your can claim the RNOR status due to lack of some information.

2. During your RNOR status, you don’t have to pay income tax in India for the income you have earned abroad.

3. Yes, you can claim your tax deduction.”

I went to Sweden on work visa in July 2016, came to visit India in December 2017 for 18 days and returned back to India permanently in July 2018. I have been working in India since then. For FY 2019-20 (AY 2018-19), will I be considered an NRI, RNOR or ROR?

In the FY 2018-2019(AY 2019-2020), you will be considered as RNOR.

In the FY 2017-2018(AY 2018-2019), you will be considered as NRI.

Hi,

This article is so helpful, Thanks for writing this. I’m staying outside India since October -2013. Planning to return to India on September 15th, 2019.

So, will I be consider with RNOR status is it? if so what ever i’m earning during Fiscal Year 2019-2020 after post September will be considered as taxable amount? also being as RNOR I could transfer the money whatever I have in overseas accounts can be transferred easily to India during 3 years without tax.? does my understanding is correct. Thanks in advance

Yes, your understanding is correct. You will be considered as RNOR for 3 financial years(including FY 2019-2020), which you can use to transfer your overseas money to India. Income earned in India in the fiscal year 2019-2020 post September will be taxed.

I have been to US for higher studies in Aug 2015. I have been visiting India for not more than 20 days in a year. After completing studies I started Job in US in Feb 2017 and continued till Nov 2018. Due to visa issue my company relocated me to India and I returned to india on 2 Dec 2018 and started earning from Dec 2018. Kindly clarify my residential status from IT return filing point of veiw for AY 2019-2020

For the Assessment Year 2019-2020 you will be considered as an NRI. So you do not have to pay tax for the income you earned until Dec 2018.

The income you earn from Dec 2, 2018 to Mar 31, 2019 (4 months) is earned from India, so that income will be taxed as per your income tax slab.

Hi,

I am working in abroad since September 2009 and since then used to come and stay for vacation around 20 days(average every year). But during FY 2018-19, I happened to stay in India for about 250 days and got continuously paid by my employer. Still I am under employment visa and will stay in abroad for around 200 days during 2019-2020. Should I file IT returns for financial years 2018-19 & 2019-2020 for my overseas income. and Can I continue to hold my NRE accounts/deposits?

As per the information you have provided on the number of days of your stay in India during FYs 2018-2019 and 2019-2020, you will fall into the NRI category.

You need NOT pay tax for the income you received from your overseas employer for both the FYs and you can continue to hold your NRE accounts/deposits till you have your NRI status.

Hi,

Thanks for the Informative article. If an NRI wants to settle in India & start working as a Freelancer for Overseas outsource jobs, will there be Income Tax on the amount received from Overseas client? If not then till when I can evade Income Tax?

You will be taxed for any income from an overseas source if you are a resident.

If you are a returning NRI, you can enjoy RNOR status and tax-exempt from global incomes for 3 financial years. But the tax-exempt is for pending payments or income received for work done while in the foreign country.

When you work as a freelancer for a foreign company, your source of income is from abroad and the income is received on a regular and will be questionable by the authorities and thus will be taxed.

I will be filing my IT Return as RNOR in FY 18-19 & FY19-20. Do I have to declare my foreign bank account details, balances and overseas investments in my IT Returns as RNOR.

No. You don’t need to declare your overseas bank details in your IT returns. However, when you lose your RNOR status, you have to provide all the details of overseas income including the percentage of tax you paid in the foreign country.

I am a non resident Indian for last 39 years. I want to return to India by 30/07/2019 for permanent settlement. Can I avail RNOR status? if so for how many years?

Yes. You can enjoy RNOR status tax benefits for 3 financial years(1st April to 31st March).

Dear Sir,

I have taken Retirement after working in the Middle East for nearly 30 years of service in February 2019.

I have NRE accounts with more than one Nationalised Bank.

Sir, how long can I maintain this NRE accounts and when do I need to intimate the banks that I have returned back to India. I have NRE FDs only with the banks.

I have not submitted any tax returns.

Please advice.

Regards

Devadasan

Immediately. You are NOT ALLOWED to continue an NRE account once you become a resident of India as per FEMA regulations.

But the NRE FDs can he held until maturity by redesignating the FD to a Resident FD.

I have been an NRI Since August 2010 and I am returning permanently to India by end of July 2019. For the past years I have been visiting India during my annual vacation for a period of 20 days or so.

I want to know my status for this FY 2019-20 and also whether I can claim RNOR status for two years. Also, If I convert my NRI deposits into RFC accounts am I liable to be taxed on the interest amount ? Can I remit directly from my RFC account to my children’s account who stay abroad.

Thanks in advance

Yes. You can enjoy RNOR status tax benefits for 3 financial years(1st April to 31st March). Your interest income for deposits in RFC account is not taxable until you are an RNOR.

Yes you can directly remit from your RFC account to your childrens’ account or any account in the country using the same currency.