ICICI Prudential Signature Plan is a Unit Linked Insurance Plan (ULIP). ULIPs have always been popular among people.

They have some attention-grabbing features such as:

- They combine the advantages of investment and insurance in a single plan.

- The benefit of Life Cover.

As a result, your money is expected to grow, plus the future of your loved ones will remain protected from the unexpected turns of life.

With time, there have been significant improvements in ULIPs. Each new ULIP is coming up with innovative features and benefits.

What are the advantages(pros) and disadvantages(cons) of ICICI Prudential Signature Plan?

In this article, we will review the ICICI Prudential Signature Plan. Read on and find out whether it holds any major benefit for you or not!

Table of Contents:

1.)Advantages of ICICI Pru Signature Plan

2.)Disadvantages of ICICI Pru Signature Plan– Review

3.)ICICI Pru Signature Plan Review: Plan Options

4.)ICICI Prudential Signature: Special Features and Benefits– Review

5.)ICICI Pru Signature Plan Funds & Performance– Review

6.)Charges under The ICICI Prudential Signature Plan– Review

- Premium allocation charge

- Fund management charge

- Policy administration charge

- Mortality charges

- Discontinuance charges

- 7.)Analysis and Review of ICICI Prudential Signature Plan

- 8.)Impact of Inflation on ULIP Returns

9.) Who Should Avoid ICICI Pru Signature Plan?

10.)Returns of ULIP as Compared to Mutual Funds

- ICICI Prudential Signature Plan vs ICICI Prudential Future Perfect

- ICICI Prudential Signature Plan vs ICICI Pru Guaranteed Income For Tomorrow

11.)ICICI Prudential Signature Plan vs Other Investment Plan – Review Conclusion

12.)How to Surrender Your ICICI Pru Signature Plan?

- Surrender During the Free-look Period

- Surrender After the Free-look Period

13.)Final Review: Should you invest in the ICICI Prudential Signature plan?

ICICI Prudential Signature Plan Review:

1. ICICI Pru Signature Plan – Advantages Review:

i. Control over your Investment:

You will have control of your invested money in the ICICI Pru Signature Plan in the ways given below

- Fund Switch: With this option, it is possible to move your money between equity, balanced, and debt funds. This feature is especially useful when you want to reduce risk in a volatile market or shift to growth-oriented funds during a bullish phase.

- Premium Redirection: With this option, it is possible to invest your future premium in a different fund of your choice. Premium redirection helps you rebalance your portfolio without disturbing your existing investment.

- Partial Withdrawal: It is an option where you can withdraw a part of your money, but it comes with certain restrictions with different ULIPs.

Many investors exploring ULIPs often compare options like the ICICI ULIP plan, ICICI Prudential Signature ULIP, and other ICICI Prudential ULIP plans to understand how this signature plan stands out in terms of flexibility, fund choices, and long-term wealth creation potential.

ii. Significant Tax Benefits:

What is the ICICI Pru Signature Plan’s tax benefit?

Let us review what are the tax benefits offered by ICICI Prudential Signature Plan.

- Investments in ULIPs up to ₹1.5 Lacs per annum are Tax-Free u/s 80C of the Income Tax Act.

- The death benefit is also exempt from tax, under section 10(10D) of the income tax act.

- However, the maturity proceeds are taxable under the conditions mentioned in the Finance Act 2021.

- Also, it does not attract any tax while fund switching.

ICICI Prudential Signature Plan consists of all the tax benefits, listed above.

However, when comparing ICICI Prudential Signature Plan returns with other tax-saving options like ELSS or even traditional ICICI SIP plans, investors should evaluate post-tax returns rather than relying purely on tax deductions.

iii. More benefits in long-term investments:

Depending on the policy you choose, it will have specific rewards and bonuses, such as; wealth boosters, loyalty additions, etc.

2. Disadvantages of ICICI Pru Signature Plan – Review

- The biggest disadvantage of the ICICI Pru Signature Plan is that the returns are not guaranteed.

For example, if you have chosen a ULIP that invests a large portion of money in equity stocks, and if the shares are not doing well, then the chances of losing money are inevitable.

- Returns are poor because there are multiple charges in this ICICI Pru Signature scheme, such as mortality charges, annual maintenance charges, administration charges, etc.

- Compared to mutual funds or ELSS, ULIPs generally have higher cost structures.

These charges bring down the returns significantly. In the first year itself, as high as 5% of the premium was lost in paying these charges.

- A Lock-in period of 5 years, it makes the investor difficult to come out of this ICICI Pru Signature policy. Moreover, the policy also levies a discontinuance charge on the fund value.

- Under The Finance Act 2021, the maturity proceeding of ULIPs is taxable as capital gains if the Annual Premium in any year is more than ₹2.5 lakhs.

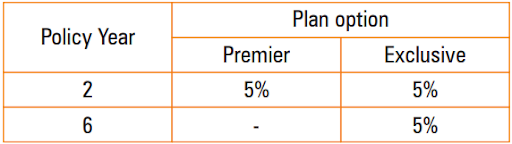

3. ICICI Prudential Signature Plan Review: Plan Options

How is the ICICI Pru Signature Plan performance?

Now, let’s know more about ICICI Pru Signature plan benefits:

Let’s understand each benefit of these options:

➢ i.) Wealth Boosters in ICICI Prudential Signature Scheme Premier Plan:

Extra units will be credited to your policy at the end of every 5th policy year, starting from the end of the 10th policy year till the end of your policy term. Each Wealth Booster will be equal to 3.25% of the average of the Fund Values, on the last business day of the last eight policy quarters.

Is ICICI Prudential a 5-year plan?

No. A policyholder can choose the premium term as per their financial convenience.

➢ ii.) Return of Mortality Charges and Policy Administration Charges:

The amount equal to total of mortality charges and policy administration charges deducted in the policy will be added back to the fund value at maturity (only for Whole-life option.

This feature is marketed as a benefit, but charges still affect compounding during the early years.

Understanding ICICI Pru Signature plan details, including its brochure features, fund options, and premium structure, becomes essential before evaluating whether this ULIP aligns with your financial goals.

4.)ICICI Prudential Signature: Special Features and Benefits – Review

Can I pay ICICI Insurance through online premium payment?

Yes. You can.

Minimum Premium Amount: Rs. 30,000 p.a. & For Whole-life option – ₹ 60,000

Maximum Premium Amount: Unlimited

Premium Payment Modes: Single, yearly, half-yearly and monthly

ii. Life Cover – Analysis

It is applicable for the entire policy term, to provide security to your family even in your absence.

In case of the unfortunate death of any policy-holder during the term of the policy, the nominee will receive the Death Benefits.

Death Benefit would be the highest among:

- Sum Assured

- Fund Value, or

- Minimum Death Benefit of 105% of the total premiums paid

This dual structure of insurance plus investment is common across ULIP plans like ICICI ULIP Signature Plan, but it often results in compromises on both fronts—adequate coverage and optimal returns.

iii. Systematic Withdrawal Plan and Partial Withdrawal Benefits – Analysis

This facility allows you to withdraw a pre-determined percentage of your fund value regularly, under the conditions, given below:

- A systematic Withdrawal Plan is allowed only after the first five policy years.

- The pay outs may be taken monthly, quarterly, half-yearly or yearly, on the 1st or 15th date of a month.

- This facility can be opted at policy inception or anytime during the policy term. You may modify or output out of the facility by notifying your branch manager.

- The maximum number of withdrawals in a year should not exceed 20% of the Fund Value.

How to withdraw partial amount from ICICI prudential?

Systematic Withdrawal Plan can be used simultaneously with Partial Withdrawal benefits, which is designed to help you provide liquidity so that any immediate financial need can be met.

Partial Withdrawal can be availed after the completion of 5 policy years, provided that the money is not in the Discontinued Policy (DP) Fund.

With partial withdrawal benefits, you can make an unlimited number of Partial Withdrawals and they are free of cost.

Despite this flexibility, frequent withdrawals impact long-term wealth creation under ULIPs.

iv. Whole Life Policy Term – Analysis

For the Whole Life policy term option, the policy term will be equal to 99 minus Age at entry.

Here is an example for ICICI Pru term plan for 99 years.

For example, if you take this policy when you are 64 years old, then the policy term will be 99-64=35 years.

The maximum age of entry in this policy is 65 years under Limited and Regular Pay. And, 70 years under Single Pay.

The maturity age of the whole life policy term is 99 Years.

This long-term horizon is suitable for legacy planning but may not be ideal for short-term financial goals.

An assured sum of whole life policy is defined in the next section.

v. Sum Assured in ICICI Prudential Signature Plan: Analysis

Source: ICICI Pru Signature Plan Brochure PDF

The plan option and the additional benefits discussed here are only for the ICICI Pru Signature Plan Offline purchase a policy.

ICICI Pru also offers the same Signature Plan Online with slightly modified policy features.

You can check it out here: ICICI Pru Signature Plan Online Brochure PDF.

Other than these minor differences, both of the ICICI Pru Signature Plan policies are the same.

Let’s take a look at the review of the performance of the funds under the ICICI Pru Signature Plan.

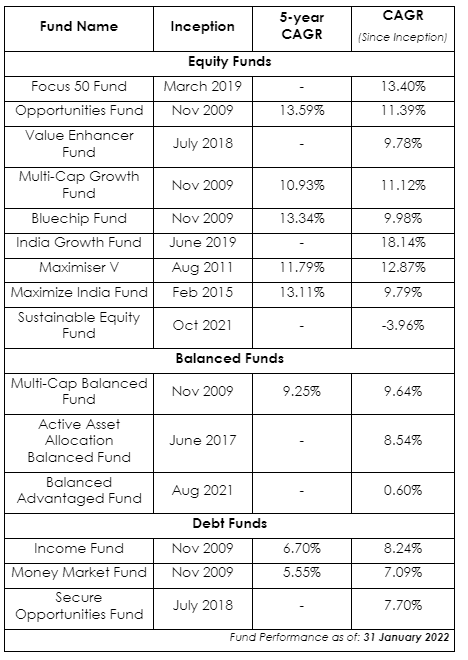

5. ICICI Pru Signature Plan Funds & Fund Performance – Review

Since ICICI Pru Signature Plan is a ULIP, it invests in various funds Equity, Debt, and Balanced funds.

These funds are created and managed by ICICI Pru itself. Also, they are not regulated by SEBI but by IRDA.

The table below shows the performance of these funds until 31 January 2023.

Data Source: ICICI Pru Official

As you can notice from the above data in illustration, 7 of the 15 funds in the ICICI Pru Signature Plan are relatively new funds with no long-term track record.

The CAGR of India Growth Fund since its inception in June 2019 is at 18.14%.

And even though the performance of equity funds seems to be on par with equity mutual funds, that is not the case in reality.

The past couple of years—2022 & 2023—have been a stellar year for the equity market.

Hence, while the 5 year CAGR of equity mutual funds reached an exceptional range of 18% and above, these funds managed to the 10%-13% range.

However, even though no one can predict the market, you can expect this return rate to drop as the current market cycle completes.

In addition, all of these funds have underperformed their respective benchmarks.

Balanced funds are expected to give returns of around 10%.

But they have delivered less than the expectation. Debt funds have been delivered reasonably.

However, equity mutual funds still performed better over 5 years with 18%+ CAGR compared to ULIP funds achieving 10–13%.

Therefore, the overall performance of ICICI Pru Signature Plan funds had been mediocre till January 2023!

For more details on each fund, you can visit the official website of ICICI Pru Signature Plan performance details.

6. Charges under the ICICI Prudential Signature Plan – Review

i. Premium Allocation Charges Review

NIL

ii. Fund Management Charges Review

What are the fund management charges in this ulip?

The Fund Management Charge in the ICICI Prudential Signature plan is fixed at 1.35% of the fund value per annum, except for the money market fund, which has 0.75% p.a.

However, if the monies are in the Discontinued Policy Fund, a Fund Management Charge of 0.50% p.a. will apply.

iii. Policy administration Charges Review

What is the policy administration charges?

Policy administration charge will be charged throughout the policy term, which is 0.5% p.m. (6.0%) of Annual Premium limited to ₹ 500 p.m. (₹ 6000 p.a.)

iv. Mortality Charges Review

What are the mortality charges in the ICICI Pru Signature plan?

Let’s figure out, how mortality charges can be made.

Mortality charges will be levied every month by the redemption of units based on the Sum at Risk.

And, the sum at risk is equal to the highest Sum Assured, minimum death benefits, and Fund Value.

How to calculate mortality charges in ULIP?

Indicative annual charges per thousand life cover for a healthy male and female life are as shown below:

| Age | 30 | 40 | 50 | 60 |

| Male (Rs) | 1.06 | 1.81 | 4.95 | 11.54 |

| Female (Rs) | 1.02 | 1.55 | 3.99 | 9.95 |

That is, if a 30-year-old male has taken the life cover of Rs. 10 Lacs, then he will be paying Rs. 1060. It increases with age.

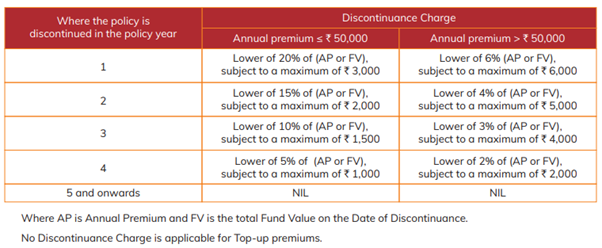

v. Discontinuance Charge:

ICICI Pru Signature plan ULIP discontinued charges:

Source: ICICI Pru Signature Plan Brochure PDF

If you surrender the policy during the first five policy years, your money will be transferred to Discontinued Policy (DP) Fund after the deduction of the applicable Discontinuance Charge.

A detailed understanding of ICICI Prudential Signature ULIP charges, including premium allocation, mortality, and fund management fees, is critical to evaluating the true cost of this plan.

7. Analysis & Review of ICICI Prudential Signature Plan:

What better way is there to review the ICICI Pru Signature Plan than to calculate the returns with an illustration?

Let’s take, for example, a 35-year-old health male buying the ICICI Pru Signature Plan.

He is choosing 20 years’ policy term with a 10-year limited premium payment term.

And he will pay an annual premium of ₹1 lakh for a Sum Assured of ₹10.5 lakhs.

Many investors look at the ICICI Pru Signature Plan primarily for its “long-term wealth creation” appeal, but the actual numbers reveal how ULIP charges dilute returns despite seemingly attractive fund performance.

This makes analysing real returns essential before committing to any ULIP investment.

|

Male |

35 years |

|

Sum Assured |

₹ 10,50,000 |

|

Policy Term |

20 years |

|

Premium Paying Term |

10 years |

|

Annualised Premium |

₹ 1,00,000 |

Then what are the ULIP returns in 20 years?

Based on these specs, the official ICICI Pru suggests a maturity value of ₹27.11 lakhs at an assumed fund return rate of 8% p.a and ₹ 15.08 Lakhs at an assumed fund return of 4% p.a.

Now, this looks fair, and the 8% CAGR is achievable by the equity funds of the ICICI Pru Signature Plan.

However, the projected values do not reflect the actual investor experience because ULIP deductions—like policy administration charges, mortality charges, fund management charges—directly reduce the effective return or IRR.

This is why ULIPs often underperform compared to simple, low-cost investment products.

But, the 8% CAGR does not mean that the investor gets the same investment return.

This may be confusing or surprising, but you can verify it in the IRR of the ICICI Pru signature plan calculation table shown below.

|

At 4% p.a. |

At 8% p.a. |

||||

|

Age |

Year |

Annualised premium / Maturity benefit |

Death benefit |

Annualised premium / Maturity benefit |

Death benefit |

|

35 |

1 |

-1,00,000 |

10,50,000 |

-1,00,000 |

10,50,000 |

|

36 |

2 |

-1,00,000 |

10,50,000 |

-1,00,000 |

10,50,000 |

|

37 |

3 |

-1,00,000 |

10,50,000 |

-1,00,000 |

10,50,000 |

|

38 |

4 |

-1,00,000 |

10,50,000 |

-1,00,000 |

10,50,000 |

|

39 |

5 |

-1,00,000 |

10,50,000 |

-1,00,000 |

10,50,000 |

|

40 |

6 |

-1,00,000 |

10,50,000 |

-1,00,000 |

10,50,000 |

|

41 |

7 |

-1,00,000 |

10,50,000 |

-1,00,000 |

10,50,000 |

|

42 |

8 |

-1,00,000 |

10,50,000 |

-1,00,000 |

10,50,000 |

|

43 |

9 |

-1,00,000 |

10,50,000 |

-1,00,000 |

10,50,000 |

|

44 |

10 |

-1,00,000 |

10,50,000 |

-1,00,000 |

10,50,000 |

|

45 |

11 |

0 |

10,50,000 |

0 |

10,50,000 |

|

46 |

12 |

0 |

10,50,000 |

0 |

10,50,000 |

|

47 |

13 |

0 |

10,50,000 |

0 |

10,50,000 |

|

48 |

14 |

0 |

10,50,000 |

0 |

10,50,000 |

|

49 |

15 |

0 |

10,50,000 |

0 |

10,50,000 |

|

50 |

16 |

0 |

10,50,000 |

0 |

10,50,000 |

|

51 |

17 |

0 |

10,50,000 |

0 |

10,50,000 |

|

52 |

18 |

0 |

10,50,000 |

0 |

10,50,000 |

|

53 |

19 |

0 |

10,50,000 |

0 |

10,50,000 |

|

54 |

20 |

0 |

10,50,000 |

0 |

10,50,000 |

|

55 |

15,08,000 |

10,50,000 |

27,11,000 |

10,50,000 |

|

|

IRR |

2.67% |

6.53% |

|||

In the above illustration we have calculated the IRR at 6.53% for the 8% scenario and 2.67% for the 4% scenario.

While the ₹27.11 lakhs maturity value looked good, the net return rate from the policy reveals the truth.

This big difference in the return rate is because of the various charges levied by the ICICI Pru Signature Plan.

Like every other ULIP, the ICICI Pru Signature Plan presents one thing and delivers another. In the best-case scenario, the IRR of ICICI Pru Signature plan is 6.53%.

This return rate is something offered by fixed deposits and other assured return investment instruments.

When a long-term product delivers FD-like returns despite taking equity-market risk, it fails the basic purpose of wealth creation.

And when we take the inflation rate—6%-8% average—into account, 6% or even 6.5% will be ineffective in the long term.

This gap between projected returns and actual IRR is a common issue across ULIP plans, including ICICI Prudential Signature ULIP, making return expectations often misleading for first-time investors.

8. Impact of Inflation on ULIP Returns

While the ICICI Pru Signature Plan shows a projected IRR of 6.53% in the best-case scenario, it is crucial to understand the impact of inflation on your real returns.

Inflation represents the rising cost of living over time, and historically, India’s inflation rate has averaged around 6%-8% per year.

Even if your ULIP delivers an 8% return on paper, after accounting for inflation, the real growth of your investment is significantly lower.

For example, with an 8% nominal return and 6% inflation, the effective real return is only around 2% per year.

Over a long-term horizon of 20 years, this means the purchasing power of your maturity amount could be far less than what you expect.

In contrast, equity-based investments like ELSS Mutual Funds typically offer inflation-beating returns in the range of 12%-15% CAGR, helping you preserve and grow your wealth in real terms.

Therefore, when evaluating any ULIP like the ICICI Pru Signature Plan, it’s not enough to look at the maturity value alone—you must consider the erosion of returns due to inflation to make a truly informed decision.

Hence, in reality, your investments will be losing value in terms of real return.

Of course, the ICICI Pru Signature Plan funds have delivered more than 8% as per the past performance.

But the point is that the IRR of ICICI Prudential Signature plan does not deliver the returns earned by the funds—and it is wildly misleading the policyholders.

No matter how much the ULIP’s funds earn, the charges in the ICICI Signature Plan will drag it down by at least 2% on all returns.

ICICI Pru Signature contains all the top-notch features that any ULIP holder will like to have.

But if you choose to invest in ULIPs, you may be compromising on your most important financial goals.

On the bright side, all hope is not lost.

There are better alternative investment options available…

When evaluating ICICI Prudential Signature Plan returns, adjusting for inflation provides a clearer picture of whether the investment truly generates real wealth over time.

9. Who Should Avoid ICICI Pru Signature Plan?

This plan is not ideal for investors who are focused on high returns and wealth creation, as ULIP charges significantly reduce actual returns despite decent fund performance.

It also may not suit those who prefer transparency and simplicity, since ULIPs come with multiple charges and complex structures compared to mutual funds.

If you need liquidity or flexibility, the 5-year lock-in and exit charges can be restrictive.

Lastly, investors who already have a term insurance plan should avoid combining insurance and investment, as it often leads to lower efficiency in both areas.

(ICICI Pru Signature Plan) ULIP vs Mutual fund:

Instead of investing in ICICI Pru Signature Plan, you may consider choosing the combination of Equity Mutual Fund and Term Insurance Policy.

Compare to the IRR of ICICI Prudential Signature plan, mutual fund offers much better—inflation-beating—returns and far more flexibility and control over your investments.

The combination of Equity Mutual Fund and Term Insurance Policy contains all the benefits of ULIPs such as Fund Switching, Partial Withdrawal, All tax benefits, and more benefits in Long-Term Investments.

Apart from having all these benefits, the combination of Mutual Funds and Term Insurance also overcomes the limitations of ULIPs.

Investing in ICICI Pru Signature Plan may seem attractive, but careful analysis shows ULIP returns lag behind Mutual Fund growth.

10. Returns of ULIP as compared to Mutual Funds: Who is better?

Are the returns of the ICICI Pru Signature Plan lower than the returns of the Mutual Fund or higher?

Let’s find out by taking the below example:

We have already seen that the ICICI Pru Signature Plan has a better chance of delivering ₹27.11 lakhs returns at the “8% CAGR” of the fund.

However, the same amount of investment in ELSS Mutual Funds will reap returns in the range of 12%-15% CAGR.

We are particularly choosing the ELSS Mutual Fund because it offers the same tax benefit as the ICICI Pru Signature Plan u/s 80C of the IT Act, 1961.

Using the same metrics in the previous example, we have worked out a pure-term and an ELSS fund combo.

A pure term insurance policy for a sum assured of ₹ 10.5 Lakhs costs an annual premium of ₹ 6,800.

The policy term is 20 years and the premium paying term is 10 years. The balance ₹ 93,200 can be invested in the first 10 years and allowed to grow in the following 10 years.

|

Pure Term Life Insurance Policy |

|

|

Sum Assured |

₹ 10,50,000 |

|

Policy Term |

20 years |

|

Premium Paying Term |

10 years |

|

Annualised Premium |

₹ 6,800 |

|

Investment |

₹ 93,200 |

|

Age |

Year |

Term Insurance premium + ELSS |

Death benefit |

|

35 |

1 |

-1,00,000 |

10,50,000 |

|

36 |

2 |

-1,00,000 |

10,50,000 |

|

37 |

3 |

-1,00,000 |

10,50,000 |

|

38 |

4 |

-1,00,000 |

10,50,000 |

|

39 |

5 |

-1,00,000 |

10,50,000 |

|

40 |

6 |

-1,00,000 |

10,50,000 |

|

41 |

7 |

-1,00,000 |

10,50,000 |

|

42 |

8 |

-1,00,000 |

10,50,000 |

|

43 |

9 |

-1,00,000 |

10,50,000 |

|

44 |

10 |

-1,00,000 |

10,50,000 |

|

45 |

11 |

0 |

10,50,000 |

|

46 |

12 |

0 |

10,50,000 |

|

47 |

13 |

0 |

10,50,000 |

|

48 |

14 |

0 |

10,50,000 |

|

49 |

15 |

0 |

10,50,000 |

|

50 |

16 |

0 |

10,50,000 |

|

51 |

17 |

0 |

10,50,000 |

|

52 |

18 |

0 |

10,50,000 |

|

53 |

19 |

0 |

10,50,000 |

|

54 |

20 |

0 |

10,50,000 |

|

55 |

51,10,276 |

10,50,000 |

|

|

IRR |

10.79% |

12% CAGR is a conservative assumption even for an average-performing ELSS Mutual Fund.

And, the fund value at maturity is just shy of ₹ 51.10 lakhs. It is almost double the fund value of ICICI Pru Signature Plan.

|

ELSS Tax Calculation |

|

|

Maturity value after 20 years |

56,89,315 |

|

Purchase price |

9,32,000 |

|

Long-Term Capital Gains |

47,57,315 |

|

Exemption limit |

1,25,000 |

|

Taxable LTCG |

46,32,315 |

|

Tax paid on LTCG |

5,79,039 |

|

Maturity value after tax |

51,10,276 |

In the above illustration we have calculated the post – tax return of mutual fund at 10.79%.

As you can notice from the above example, the return of the ELSS Mutual Funds is still way higher than the ICICI Pru Signature Plan.

It is precisely ₹24 Lakhs higher return than the ULIP.

Some key highlights of ELSS Mutual Funds are: Analysis

- Only 3 years lock-in period (5 years for ULIPs)

- Similar investment risk as ULIPs

- Far better returns

- Much diversified portfolio than ULIPs

- No hidden charges

- Higher liquidity

- Similar tax treatment as ULIPs

The post-tax IRR of Mutual Funds demonstrates higher net returns compared to ICICI Pru Signature Plan ULIP returns.

It is noteworthy that despite the common belief, the returns from ULIP policies are also taxable as per the amendment in section 10(10D) by The Finance Act, 2021.

i. Who is more Goal focused? Mutual Funds or ULIPs! – Comparison Review

The Financial goals are the basic building block of any Financial Plan. Through any ULIP it is practically impossible to achieve any financial goal, due to their fixed lock-in periods and lesser returns on investments.

But, with Mutual Funds, you can list your short-term (2-5 years) and long-term (7+ years) goals and invest accordingly in the right scheme, where you will be benefitted from Higher Returns as compared to ULIPs.

This way, the investments in Mutual Funds provide a more focused and goal-oriented approach. For more details, read the 5-Steps Financial Planning Guide for beginners.

ii. Fixed Lock-in Period – Review

In ICICI Prudential Signature Plan there is a fixed insurance lock-in period of 5 years and cancellation charges are significantly high as mentioned in the previous section.

But, if you want to cancel and come out from any Mutual Fund Scheme at any time, you can do so at a much lower cost as compared to ULIPs in the first year.

There are no cancellation charges in Mutual Funds from 1 year onwards.

iii. Competitiveness of Fund Managers: Mutual Fund Vs. ULIP! – Comparison Review

Fund managers who are involved in managing Mutual Funds have strong pressure to perform the best among their various competitors.

Otherwise, investors may withhold their SIPs and invest in other mutual fund schemes, withdrawal of SIP may lead to the bad reputation of any scheme!

This competitive nature of work tends to maximize the profitability of the Mutual Funds significantly.

But with ULIPs, there is no such pressure among their Fund Managers, as the returns are lower, plus there are 5 years of the lock-in period.

Therefore, the fund managers handling Mutual Funds are highly competitive as compared to their ULIP counterparts.

iv. Regulatory Authority: Mutual Funds Vs. ULIPs: Comparison Review

Mutual Funds are regulated by a reputed agency called SEBI. Whereas, ULIPs are regulated by IRDA, which basically regulates insurance policies.

SEBI ensures greater security and safeguards against all frauds in Mutual Funds or Stock investments. Whereas, SEBI has no such role to play in ULIPs.

IRDA’s regulations are predominantly focused on Insurance regulation and not on investment regulation.

SEBI’s regulation is well evolved in regulating the investments, protecting investor’s interest and proactively taking measures to stop misselling.

If your purpose is investing and getting returns, then SEBI’s regulation is better for you.

v. Transparency in Investment: Mutual Fund Vs. ULIP:

Mutual funds are more transparent than ULIPs about the fees charged and the portfolio holdings.

Also, there is transparency in the level playing field in the Mutual Fund investment, as the categorization of the mutual funds is defined by SEBI.

For example, if you choose to invest in the Large Cap Mutual Fund, your investment will be 100% in large-cap.

And, you can easily compare various other Large-cap funds, and select the best choice.

Whereas the investment in the ULIP is rather complex, for example if you choose to invest in Large Cap funds through ULIP, it is NOT 100% in Large Cap; they may be exposed to Mid-Cap or other categories by 20%.

Therefore, it becomes hard to compare one ULIP to another. The nature of ULIP investment is not transparent as compared to Mutual Fund investment.

Comparing ICICI Pru Signature Plan vs ELSS Mutual Funds shows a clear advantage in liquidity, diversification, and tax-efficient returns.

Financial planners recommend replacing ULIP investments like ICICI Pru Signature Plan with Mutual Funds plus Term Insurance for higher returns and flexibility.

Investors should be aware that ULIP returns are taxable, whereas long-term ELSS Mutual Funds offer strategic tax efficiency.

Lock-in period differences favour Mutual Funds over ULIPs, allowing earlier redemption and portfolio reallocation.

Competitiveness of fund managers in Mutual Funds often leads to superior fund performance vs ULIPs.

The combination of Mutual Fund growth and term insurance protection ensures risk-adjusted returns exceed those of ICICI Pru Signature Plan.

Transparent portfolio allocation in Mutual Funds ensures investors know exactly where their capital is invested, unlike ULIPs.

When planning long-term wealth creation, ICICI Pru Signature Plan ULIP returns are often overshadowed by Mutual Fund CAGR potential.

You can check your ICICI Prudential Signature Plan Policy Status here.

vi. Affordability of Insurance: Term Insurance Vs. ULIPs – Review

Your investment in ULIP is divided among Insurance and Investment, you can choose to pay as a single payment or on a monthly basis.

And the minimum premium amount is Rs. 2 Lacs per annum!

Existing Term Insurance plans come with a much more affordable price as compared to the ULIPs and provide the same amount of benefits.

For more details about the Best Life Insurance policy, you can read this Cheat Sheet to select the best term insurance plan for you.

You will earn way better returns in the combination of Mutual Fund and Term Insurance as compared to ULIPs and you will have more control over your investments.

Click here and watch the video for the Hindi version of ICICI Pru Signature Plan (आयसीआयसीआय प्रुडेन्शियल सिग्नेचर प्लॅन)-Watch here!

-

ICICI Prudential Signature Plan vs ICICI Prudential Future Perfect

ICICI Prudential Future Perfect is an endowment plan and there are non-guaranteed bonuses such as reversionary and terminal bonuses.

To read the complete review of this plan check below

ICICI Prudential Future Perfect [Review]

-

ICICI Prudential Signature Plan vs ICICI Pru Guaranteed Income For Tomorrow

The main focus of the ICICI Pru Guaranteed Income For Tomorrow(GIFT) plan is savings and protection.

It is a traditional Life insurance policy and you can get your guaranteed income either in the form of regular income or as a lump sum.

Read the below review with IRR analysis.

ICICI Pru Guaranteed Income For Tomorrow Review [2023]: Worth Buying Or Not?

11. ICICI Prudential Signature Plan Vs Other Investment Plan – Review Conclusion

After a thorough and detailed analysis of all the other alternatives for the ICICI Prudential Signature Plan, it is very clear that mutual funds are much more reliable for investment.

As we discussed earlier,

you can list your short-term (2-5 years) and long-term (7+ years) financial goals and invest in mutual funds accordingly in the appropriate scheme. You will gain Higher Returns compared to ULIPs.

12. How to Surrender Your ICICI Pru Signature Plan?

Whether you are buying a ULIP or surrendering one, I suggest you consult your Financial Advisor before taking any step.

They will be able to analyse the situation and help you make the right decision.

-

Surrender during the Free-Look Period:

Starting from the date of receipt of the policy document, you will have 15-day period to review the ICICI Prudential Signature Plan policy document.

If you find the policy terms and conditions are not satisfying, for any reason, you can surrender your policy.

ICICI Prudential should process your surrender request in a matter of days. And you get a refund of your policy premium.

You can cancel your policy by filling up this Free-look form and submitting it to any of the ICICI Prudential Insurance branches.

Note: The Free-look period is 30 days in case you bought the policy online.

-

Surrender after the Free-Look Period: Review

Since the ICICI Pru Elite Life Super Plan is a ULIP, it has a lock-in period of 5 years. Hence you cannot get your fund value before that.

But you can still submit a surrender request before the completion of 5 policy years.

In such a case, your policy will be considered a “Discontinued Policy” (like a paid-up policy). And all your investments will be moved to the “Discontinued Policy Fund” earning a minimum return.

You do not have to pay any more premiums. And you will receive the fund value on completion of 5 policy years.

Steps to Surrender ICICI Pru Signature Plan: Analysis

To surrender your ICICI Pru Signature Plan, you need to fill out the ICICI Prudential policy surrender form and submit it along with other documents at the nearest ICICI Prudential branch.

The documents are,

- Filled the Surrender Form

- Original Policy Document

- A signed copy of a photo ID (must carry original ID)

- A Cancelled cheque with the policyholder’s name

Once you submit your surrender request, ICICI Prudential will process it within 10 working days and confirm the same.

Can I surrender ICICI prudential policy online?

Yes. You can surrender the ICICI prudential policy online by sending them email.

Surrendering ICICI Pru Signature Plan may help investors recover capital tied up in ULIPs with high charges.

ICICI Prudential policy surrender process is straightforward if all required documents are correctly submitted.

Opting for online surrender ensures faster processing and avoids unnecessary branch visits.

Be aware that ICICI Pru Signature Plan surrender value may be lower than your total premiums due to ULIP charges and lock-in deductions.

13. Final Review: Should you invest in ICICI Pru Signature Plan?

So, what is our verdict on ICICI Prudential Signature Plan?

ICICI prudential is good or bad?

As we analysed earlier on various aspects, this ULIP policy is NOT up to the mark.

Do Not Invest in this ULIP!

The insurance agents would convince you to buy this plan for their agent commission. Please beware!

Our suggestion is to invest in Mutual Funds (and/or PPF) and Term insurance policies separately.

Not only they will provide you with higher returns and risk benefits, but it also takes away the limitations of any ULIP, including the ICICI Pru Signature Plan.

And, also beware of the mis-selling of this ULIP by your bank.

They may lure you to invest in this ULIP by showing its various benefits.

But, after reading the complete analysis, we hope that you get a clear idea about this ULIP.

Please don’t search for ICICI Pru Signature Plan Review in Quora or any other social media.

Financial Influencers can confuse. Instead, check with certified and experienced financial planners.

The ICICI Pru Signature Plan has hidden charges and low IRR, making it less effective than Mutual Funds.

Investing in term insurance plus Mutual Funds offers better long-term wealth creation than ULIP policies.

Mis-selling of ULIPs like ICICI Pru Signature Plan is common; always consult professional financial planners.

Before choosing any ULIP, including ICICI Prudential Signature ULIP plan, it is essential to compare it with alternative investment options to ensure it aligns with your long-term financial goals.

Do not rely on social media reviews for investment decisions; they may exaggerate benefits.

Are you interested in creating a Comprehensive Financial Plan for your financial goals?

Do you think you can make a long-term investment strategy based on information from social media sites like Quora, Facebook, Twitter, etc.? Please consult a professional financial planner for reliable advice.

Skip the queue by registering for your 30-minute FREE Financial Plan Consultation. Click the ‘‘BOOK YOUR SLOT NOW!’’ button below.

Your mide of describing everything in this piece of writing is

really fastidious, all be capable of without ifficulty undersrand it,

Thanks a lot.

Hi Why are you miss guiding people about ICICI Prudential Signature plan?

Can you be more specific? We have used the official illustration to compare.

I see all negative reviews for any of the ULIPs, and keep saying invest in MF.

If the funds available in the ULIP (offered by so called pros with all their best knowledge) doesn’t perform good, how can an individual investor can research and find winning MF..

So there is no guarantee that one could succeed with investing in MF and could lose money there also.

Keeping these ULIPs aside, how about picking some LIC plans which offers low, but guaranteed returns like 5% for life (as they are better than FDs)?

Instead of traditional plans which offer 5% kind of returns. It is better to invest in PPF.

As ULIPs have higher charges and have lesser competitive performance, better to invest in Mutual Funds.

Beyond 20 lakhs, there is no premium allocation charge as per the icici PRU person I spoke to. Does it mean that at 20 lakhs value, ULIP and mutual funds are both about the same and there is no disadvantage of ULIP, except of course the lock in period?

Also, the funds seem to be performing/picking up now in 2021.

What are your thoughts?

Hi,

For personalized investment advice, you can sign up for our 30-minute complimentary financial plan consultation.

You can click the link to get your appointment to talk with our financial planners.

https://www.holisticinvestment.in/complimentary-financial-plan-consultation/

I have invested in ICICI Pru ULIP II plan at an annual premium of 2lakhs /annum and paid all 5 yrs premium with a min locking period of 5 yrs and maturity at 20 yrs. I paid the last premium in Feb 2021. Its not performing good. Should i continue now or should i withraw partially or fully?

Since you have already taken this insurance plan, then you have two options.

Option: 1 You can surrender and encash the policy. And reinvest the surrender value and future premium money with better investment plans like PPF or MF.

Option: 2 You can continue with the insurance plan until the policy matures.

It is advisable to work out the outcome of both the options and proceed with the better option.

80% of the times, option 1 is better.

You can consult a financial planner to choose the better option.

Or

You can take advantage of our free complimentary financial plan consultation and talk to our financial planners.

Get your appointment here!

https://www.holisticinvestment.in/complimentary-financial-plan-consultation/

Hi,

Is mutual fund return guaranteed, like u have been highlighted. 3times return etc. Is this guaranteed and can u brief on market crash or down turn in market in mutual funds and its impact too for investers who are not regular market followers.

Hi!

If you are looking for safe and assured returns, then PPF will be a better choice.

Hello Sir,

I should have read this article before investing. I have invested just 3 months back. What would be your suggestion for me?

Thanks in advance.

Regards

Since you have already taken this insurance plan, then you have two options.

Option: 1 You can surrender and encash the policy. And reinvest the surrender value and future premium money with better investment plans like PPF or MF.

Option: 2 You can continue with the insurance plan until the policy matures.

It is advisable to work out the outcome of both the options and proceed with the better option.

80% of the times, option 1 is better.

You can consult a financial planner to choose the better option.

Or

You can take advantage of our free complimentary financial plan consultation and talk to our financial planners.

Get your appointment here!

https://www.holisticinvestment.in/complimentary-financial-plan-consultation/

I got this policy in March 2021. Due to some error we missed that the policy premium option in the document during the free look period. It is whole life instead of the Policy term period of 15years as discussed with the sales person. Should I surrender ? How much money will I lose as I paid one premium amount of Rs 125000 till now.

Is it possible to change terms from whole life to 10/15 years ??

Since you have already taken this insurance plan, then you have two options.

Option: 1 You can surrender and encash the policy. And reinvest the surrender value and future premium money with better investment plans like PPF or MF.

Option: 2 You can continue with the insurance plan until the policy matures.

It is advisable to work out the outcome of both the options and proceed with the better option.

80% of the times, option 1 is better.

You can consult a financial planner to choose the better option.

Or

You can take advantage of our free complimentary financial plan consultation and talk to our financial planners.

Get your appointment here!

https://www.holisticinvestment.in/complimentary-financial-plan-consultation/

Thank you for the amazing analysis. I am yet to figure out how to take on Term Insurance and Mutual Fund together to get tax free income from the investments.. but I assume that should be easily available on the net and through the links you have provided. I was about to invest in the Signature Wealth Premium plan – have already given my verbal confirmation and was to send my documents today- but thanks to your analysis I have just arranged another meeting with my wealth manager. Will ask them to help me with mutual funds and term insurance instead.

Which are the best mutual funds you would recommend?

Hi,

For personalized investment advice, you can sign up for our 30-minute complimentary financial plan consultation.

You can click the link to get your appointment to talk with our financial planners.

https://www.holisticinvestment.in/complimentary-financial-plan-consultation/

I have been lured by the bank to take this policy Advantage with 12 years term on December 2020. Paid second year premium of 2 lakhs also. Is it good to continue till 5 years? Or wait till 10 years? Kindly guide me.

Since you have already taken this insurance plan, then you have two options.

Option: 1 You can surrender and encash the policy. And reinvest the surrender value and future premium money with better investment plans like PPF or MF.

Option: 2 You can continue with the insurance plan until the policy matures.

It is advisable to work out the outcome of both options and proceed with the better option.

80% of the time, option 1 is better.

You can consult a financial planner to choose the better option.

Or

You can take advantage of our free complimentary financial plan consultation and talk to our financial planners.

Get your appointment here: https://www.holisticinvestment.in/complimentary-financial-plan-consultation/

Anyone who is reading the message. Please don’t buy ICICI prudential signature. Every year they will take 10 % of the premium which includes (morality charges, policay adminitratoin, GST and many more charges) . The profit will be fund performance – 10%. If fund is performing 6%. Then the loss if 6-10 = 4%. I made a mistake. Please don’t make the mistake. Choose Birla it had better performance.

Thank you for sharing your experience with us.

Hi,

I Invest in ICICI PRU SIGNATURE PLAN in Aug2020 and now i am confused whether i will continue or revoke this..

Agent says that you will get around 30 to 35 lakh

I am totally confused what should i do i had give one premium till now.

Since you have already taken this insurance plan, then you have two options.

Option: 1 You can surrender and encash the policy. And reinvest the surrender value and future premium money with better investment plans like PPF or MF.

Option: 2 You can continue with the insurance plan until the policy matures.

It is advisable to work out the outcome of both the options and proceed with the better option.

80% of the times, option 1 is better.

You can consult a financial planner to choose the better option.

Or

You can take advantage of our free complimentary financial plan consultation and talk to our financial planners.

Get your appointment here!

https://www.holisticinvestment.in/complimentary-financial-plan-consultation/

Thanks for the detailed analysis. Very good work. I agree that Insurance + Direct MF is way better than any ULIP.

Had a question, if we consider only from tax point of view is then this scheme better than MF? We have to pay 10% long term gains tax on equity MF but here it is fully tax exempt under Sec 10(10D)? Please guide.

Hi!

Post-tax returns from MFs are better than ULIP returns in general.

Why are you taking 8% return in ulip 15% in mf ulip can’t gibe similar return are both are invest in equity

2 if i invest in mf and ulip in 15 years what are the return if i assume same return in both

The charges are higher with ULIPs. That impacts the ROI.

Hi All,

I am investing in ICICI Prudential Pension Fund since 2008 (for 20 years). I ICICI Prudential Adviser suggested to stop paying in the Pension Fund and start ICICI Prudential Signature Plan with receipts from Pension Fund for 5 years. I do not have to pay anything from my side for next five years.

ICICI Prudential will stop my ICICI Prudential Pension Fund and start ICICI Prudential Signature.

Please advise.

Thanks and Regards,

Ankur Pradhan

This is basically a new sales technique followed by Insurance agents or RMs off-late. As they have reaped maximum commission from the first policy, they don’t get much benefit if you continue the first policy. So they ask you to close the first one and take the 2nd policy to get better commission for them. Please beware.

This was very detailed and informative, thank you so much. Could you also please suggest any investment plans with fewer charges and guaranteed returns?

Hi,

For personalized investment advice, you can sign up for our 30-minute complimentary financial plan consultation.

You can click the link to get your appointment to talk with our financial planners.

https://www.holisticinvestment.in/complimentary-financial-plan-consultation/

Thanks for your review and saved me from the first time investor like me.

You are welcome.

You are welcome

Hi, I have an IPRU wealth builder-II plan which is 6 year old now. I paid 6L in 5 years and getting approx 7.2L if I surrender now.

Am getting calls from IPRU to withdraw this amount and suggesting me to invest 1.25L in IPRU signature plan for 5 years.

Please suggest, also suggest me a good mutual fund.

Thanks.

Hi!

This is basically a new sales technique followed by Insurance agents or RMs off-late. As they have reaped maximum commission from the first policy, they don’t get much benefit if you continue the first policy. So they ask you to close the first one and take the 2nd policy to get better commission for them. Please beware.

For personalized advice, you can take advantage of our free complimentary financial plan consultation and talk to our financial planners regarding your personalized advice.

Get your appointment here: https://www.holisticinvestment.in/complimentary-financial-plan-consultation/

Investing in MF requires time and effort wherein one must know where to invest and one needs to invest time and keep updating very regularly . Can u suggest some good MF which give a return of minimum 15 percent where investment horizon is of 5 years

Hi,

For personalized investment advice, you can sigh up for our 30-minute complimentary financial plan consultation.

You can click the link to get your appointment to talk with our financial planners.

https://www.holisticinvestment.in/complimentary-financial-plan-consultation/

Dear Sir,

Excellent Analysis! Thank you for bringing real and factual picture picture

You are welcome

I am investing in this ICICI Signature ULIP from last 2 years and fund value is equal. one bank employee called and invested in this Policy. Should I surrender or wait for 5 years locking. After Surrender how much will return. Bank will give money after 5 years locking Period. What should I do ??

Since you have already taken this insurance plan, then you have two options.

Option: 1 You can surrender and encash the policy. And reinvest the surrender value and future premium money with better investment plans like PPF or MF.

Option: 2 You can continue with the insurance plan until the policy matures.

It is advisable to work out the outcome of both the options and proceed with the better option.

80% of the time, option 1 is better.

You can consult a financial planner to choose the better option.

Or

You can take advantage of our free complimentary financial plan consultation and talk to our financial planners.

Get your appointment here!

https://www.holisticinvestment.in/complimentary-financial-plan-consultation/

Hi,I had invested in this policy last week only by transferring my old life link policy.I was lured by one of the employee of the company. Does this policy still hold good. Please respond.

thanks

Since you have already taken this insurance plan, then you have two options.

Option: 1 You can surrender and encash the policy. And reinvest the surrender value and future premium money with better investment plans like PPF or MF.

Option: 2 You can continue with the insurance plan until the policy matures.

It is advisable to work out the outcome of both options and proceed with the better option.

80% of the time, option 1 is better.

You can consult a financial planner to choose the better option.

Or

You can take advantage of our free complimentary financial plan consultation and talk to our financial planners.

Get your appointment here: https://www.holisticinvestment.in/complimentary-financial-plan-consultation/

Really helpful! But I had to buy this policy after a lot of calls from the bank. It’s just been 3 days now, what should I do? Even if it’s free to look in and withdraw possible, I see the Fund value with a 7% loss. Please advise!

Thanks for your feedback.

You can surrender asap even if there is a small loss and reinvest in better products.

Thank you for your detailed analysis, my bank manager pushing me to take this policy, but i declined that, after reading your review.

Thanks

Thanks Gopi Manimuthu for your feedback.

We are happy that you found our review useful.

Hi,I had invested in this policy last week only by transferring my old life link policy.I was lured by one of the employee of the company.Now what shall I do? Please respond?

Within 15days , free look-in period, you can surrender.

Thanks 👍

Please do not invest on this policy. better to take one term plan and one mutual fund to invest to growing your money

Thank you for sharing your view.

The review was very detail and comprehensive to understand about the plan.

Could you please make a review of TATA AIA Value Income Plan in the same way for a annual premium of 4lacs.

Thank you for sharing your opinion. We will let you know once we publish the article.

Dont opt for this at all, I have my funds running almost -18% withing 7 months, and when you decide to step out of this, you realize that there are so many charges involved for the same.

Thank you for sharing your experience with us.

ICICI Signature online has now removed Premium Allocation charges for annual premium 20 lacs and above. Wealth Boosters are given at 3.5% of fund value after 10 years and every 5 years thereafter. Will this be a better option in this case since the withdrawls are Tax free?

After considering all the above only, we have calculated the IRR. The IRR is not beating the post-tax mf returns.

Hi, Thanks for the detailed and thorough article.

ICICI Team has contacted me for this investment. Their suggestion is to make an investment of Rs. 25 Lakhs in ICICI regular savings fund. Every year Rs. 6 Lakhs will be withdrawn from this fund and parked in Signature plan.

ICICI is recommending this on following grounds : 1.Maturity amount is tax free and i also can claim tax benefits under Sec 80C. 2. right time to enter since NAV is quite low. 3. Unlimited switches with nil charges 4. Unlimited systematic tax free withdrawals till age 99. 5. Wealth booster bonus @ 3.25% after 10th year and every 5 years thereafter.

Can you please share your opinion on this. Thanks

You can consult a financial planner to choose the better option.

Or

You can take advantage of our free complimentary financial plan consultation and talk to our financial planners.

Get your appointment here: https://www.holisticinvestment.in/complimentary-financial-plan-consultation/

hi

My querry is same as above and i am in 2nd year and premium is due on 22 May. Pls advise if i should discountinue as down by 30%

Will be happy to talk to you for more advise and my phone is 9664340995

Hi,

For personalized investment advice, you can sigh up for our 30-minute complimentary financial plan consultation.

You can click the link to get your appointment to talk with our financial planners.

https://www.holisticinvestment.in/complimentary-financial-plan-consultation/

What about be your recommendation for someone who has already enrolled into ICICI prulife ULIP and running 2nd year with lock in period of 5 years? Since it’s performing pathetically and my funds are running negative by almost -22%.

Would continuing to invest be wise at this time or leave the policy as is and enter into non performing FUND would be better off? Please advice.

You can stop contributing your future premiums and divert them in better-performing mutual funds. Existing investments in ULIP (though at substantial loss) redeem them as and when the lock-in is over and reinvest.

Regards

Ramalingam

I have invested 1.25 lac per anum in icici Prudential signature plsn before 3 week ago . Kindly suggest me is this good plan.?

And how much return i will get …???

Hi,

For personalized investment advice, you can sign up for our 30-minute complimentary financial plan consultation.

You can click the link to get your appointment to talk with our financial planners.

https://www.holisticinvestment.in/complimentary-financial-plan-consultation/

Very informative Article

Thank you.

Thank you so much for your detailed Explanation, review and feedbacks!!!

You are welcome.

Thanks for detailed analysis. It connected all the dots very well. Super Job. Very informative Keep up the good work.

Thanks Ameet.

Hi,

I already invested in ICICI Prudential ULIP signature policy with 3 L per annum in August 2019.

It’s giving me – 4% return 🙁

Where are all other MF which I personally invested is giving higher returns

What should I do? Should I discontinue the policy, I know my money will be stuck for 5 yrs bug at least, I can’t invest rest of the premium elsewhere

Since you have already taken this insurance plan, then you have two options.

Option: 1 You can surrender and encash the policy. And reinvest the surrender value and future premium money with better investment plans like PPF or MF.

Option: 2 You can continue with the insurance plan until the policy matures.

It is advisable to work out the outcome of both the options and proceed with the better option.

80% of the times, option 1 is better.

You can consult a financial planner to choose the better option.

Or

You can take advantage of our free complimentary financial plan consultation and talk to our financial planners.

Get your appointment here!

https://www.holisticinvestment.in/complimentary-financial-plan-consultation/

Good Article. One question: Mutual Funds return is taxed at 10% (for equity/hybrid if gains more than 1 lakh) and 20% (for Debt) if the holding period is more than 3 years. Hence, if MF gave 11% return – 10% of that or close to 1% is lost in taxes. And, this amount should be equal to the amount lost in no-gains on the 5% mortality charge which is returned at the end of 10 years. So – you basically trade flexibility of MF with a life cover of ULIP and the returns should be more or less same. Am I correct?

The Post-tax return from equity funds are better than Ulip returns.

I feel ULIP has one big advantage of Switching of funds from Debt to Equity and Visa versa with out any Tax implication and make use of market turbulence and maximise return. eg. If stock market is showing descending trend, switch to Debt fund till the trend continues. Switch to Equity option when trend reverses at lower NAV in equity fund. In such case the yield maximises and beats Equity Mutual funds.

Theoretically, what you said is correct. However, in practice, timing proactively is not possible even for fund managers of MF. Their Balanced Advantage Fund which has the flexibility to move between equity to debt and debt to equity didn’t beat the equity fund returns in the long fund.