Is Bandhan Life’s Guaranteed Income Plan really your ticket to a dependable secondary income — or just a life-insurance product dressed as an annuity?

Is the Bandhan Life Guaranteed Income Plan a dependable partner for long-term financial stability — or a conservative compromise in a volatile world?

Will the Bandhan Life Guaranteed Income Plan keep up with inflation — or will it feel less “guaranteed” as your expenses rise?

This article breaks down the plan’s features, highlights its pros and cons, and evaluates the cash flows with clear, detailed illustrations.

Table of Contents:

What is the Bandhan Life Guaranteed Income Plan?

What are the features of the Bandhan Life Guaranteed Income Plan?

Who is eligible for the Bandhan Life Guaranteed Income Plan?

What are the plan options in the Bandhan Life Guaranteed Income Plan?

What are the benefits of the Bandhan Life Guaranteed Income Plan?

Grace Period, Discontinuance and Revival of the Bandhan Life Guaranteed Income Plan

Free Look Period for the Bandhan Life Guaranteed Income Plan

Surrendering the Bandhan Life Guaranteed Income Plan

What are the advantages of the Bandhan Life Guaranteed Income Plan?

What are the disadvantages of the Bandhan Life Guaranteed Income Plan?

Research Methodology of Bandhan Life Guaranteed Income Plan

Benefit Illustration – IRR Analysis of Bandhan Life Guaranteed Income Plan

Bandhan Life Guaranteed Income Plan Vs. Other Investments

Bandhan Life Guaranteed Income Plan Vs. Pure-term + Equity Mutual Fund

Final Verdict on Bandhan Life Guaranteed Income Plan

What is the Bandhan Life Guaranteed Income Plan?

Bandhan Life Guaranteed Income Plan is a Non-Linked Non-Participating Life Insurance Individual Savings Plan. It is a flexible plan tailored to help you achieve your financial goals.

All benefits are guaranteed. Plus, the built-in life insurance coverage provides a layer of financial security for your loved ones.

What are the features of the Bandhan Life Guaranteed Income Plan?

- Guaranteed benefits with two plan options tailored to your financial needs.

- Assured income stream to support both short-term and long-term goals while keeping you insured.

- Option to receive income immediately, starting from the first policy month.

- Flexibility to accumulate the payouts and build a future wealth corpus.

- The Return of Premium feature offers a lump-sum benefit.

- Tax benefits are available as per prevailing tax laws.

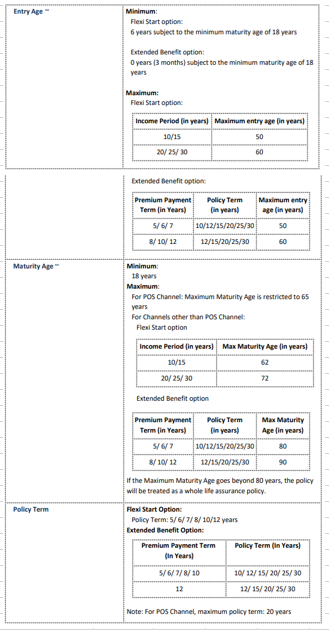

Who is eligible for the Bandhan Life Guaranteed Income Plan?

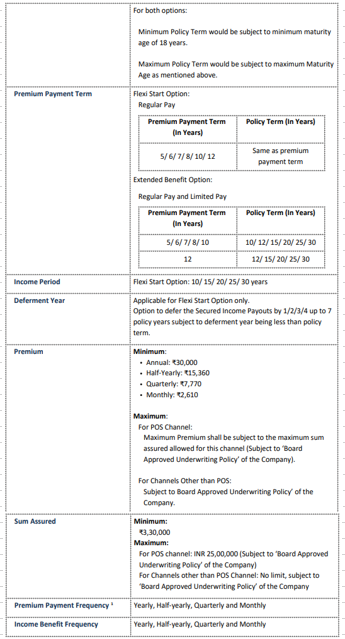

What are the plan options in the Bandhan Life Guaranteed Income Plan?

1. Flexi Start

This option provides a regular income (known as “Secured Income”) from the end of the 1st policy year till the end of your Bandhan Life Guaranteed Income Plan policy term.

Upon completion of the policy term, the income period as chosen by you at policy inception starts, during which you will receive a regular income known as “Guaranteed Income” in arrears.

2. Extended Benefit

This variant provides a regular income (known as “Secured Income”) from the end of the 1st policy year, till the end of the policy term.

At the end of the Bandhan Life Guaranteed Income Plan policy term, a lump sum benefit amounting to 100% of Total Premiums Paid will be payable.

What are the benefits of the Bandhan Life Guaranteed Income Plan?

A. Survival Benefit

Flexi Start

Secured Income shall be paid in arrears starting from the first policy year until death or the end of the Bandhan Life Guaranteed Income Plan policy Term, whichever is earlier.

Secured Income = Secured Income Rate * Annualised Premium. You can also choose to defer your Secured Income by up to 7 years

Extended Benefit

You will receive a stream of regular income known as ‘Secured Income’ which starts from the end of 1st year policy year until the death of the life assured or the end of the policy term, whichever is earlier.

Secured Income = Secured Income Rate * Annualised Premium. You can also accumulate Secured Income payouts at any point during the Bandhan Life Guaranteed Income Plan policy term

B. Maturity Benefit

Flexi Start

Upon survival of the life assured until the end of the Bandhan Life Guaranteed Income Plan policy term, income payouts known as ‘Guaranteed Income’ will be paid in arrears starting from the end of the (Policy Term + 1)th year till the end of the income period.

Guaranteed Income = Guaranteed Income Rate * Annualised Premium. The income period must be chosen at policy inception. Once chosen, this period cannot be changed.

Extended Benefit

On maturity, you will receive 100% of the Total Premiums Paid as a lump sum benefit at the end of the policy term. Accumulated Secured Income (if any), if not paid earlier, will also be paid at maturity.

C. Death Benefit

For both options

Life cover shall be provided during the Bandhan Life Guaranteed Income Plan policy term.

In case of death of Life Assured during the policy term, the death benefit payable will be a maximum of Sum Assured on Death and Surrender Value as on the date of death in a lump sum, wherein Sum Assured on Death will be the higher of:

- 11 times of Annualised Premium, which is Base Sum Assured

- 105% of Total Premiums Paid till date of death

Under the Extended Benefit Option, Accumulated Secured Income Payouts (if any), if not paid earlier, will be paid along with the death benefit mentioned above.

Grace Period, Discontinuance and Revival of the Bandhan Life Guaranteed Income Plan

Grace Period

The Grace Period is thirty (30) days for frequencies other than monthly and fifteen (15) days for monthly frequency during which the Policy is considered to be in-force with the risk cover.

Discontinuance

If you have not paid at least one (1) full year’s premium, your policy will immediately and automatically lapse at the expiry of the grace period, and no benefit other than accumulated Secured Income Payouts, if any and not paid earlier, will be payable under the policy.

Such payouts, if any, in the policy will be paid out at the end of the grace period. All other benefits under the policy shall cease, and nothing is payable on death, maturity, survival or surrender.

If at least one (1) full year’s premium has been paid and subsequent premiums are not paid, then the policy shall not lapse; instead, the policy will be immediately and automatically converted to a reduced paid-up policy at the expiry of the grace period.

Revival

You can revive your lapsed or paid-up policy within five (5) consecutive years from the due date of the first unpaid premium and before the end of the Bandhan Life Guaranteed Income Plan policy term.

Free Look Period for the Bandhan Life Guaranteed Income Plan

If you are not satisfied with any of the terms and conditions of the policy, or otherwise and have not made any claim, then you may request the company for cancellation of the Policy within 30 days (Thirty Days) from the date of receipt of the Policy document, whether received electronically or otherwise.

Surrendering the Bandhan Life Guaranteed Income Plan

You can surrender the policy at any time during the Bandhan Life Guaranteed Income Plan policy term after completion of the first policy year, provided one full year’s premium has been paid.

The surrender benefit payable will be the highest of the guaranteed surrender value (GSV) and special surrender value (SSV).

What are the advantages of the Bandhan Life Guaranteed Income Plan?

- You can choose to accumulate the Secured Income at any point during the policy term.

- The Premium Offset feature allows you to adjust future premiums using the Secured Income payouts received.

- You may opt to receive Secured Income or Guaranteed Income payouts on any date of your choice, not just on the Policy Anniversary.

- By default, payouts are made in arrears, but you also have the option to receive them in advance.

- Income payout frequency is flexible — choose from yearly, half-yearly, quarterly, or monthly modes.

- You can modify your premium payment frequency anytime during the premium payment term.

- Policy loans are available, up to a maximum of 80% of the Surrender Value at the time of availing the loan.

What are the disadvantages of the Bandhan Life Guaranteed Income Plan?

- Survival benefits are generally suited only for discretionary or non-essential expenses.

- Although these benefits are guaranteed, the overall returns tend to be modest.

- The sum assured offered under the plan may fall short of adequately meeting your financial protection needs.

Research Methodology of Bandhan Life Guaranteed Income Plan

The Bandhan Life Guaranteed Income Plan offers a survival benefit starting from the end of the first policy year. At maturity, the benefit can be received either as a lump sum or as a regular payout, similar to the survival benefit.

To understand whether these payouts hold real value, we analyse a benefit illustration from the policy brochure and review the cash flows in detail.

Benefit Illustration – IRR Analysis of Bandhan Life Guaranteed Income Plan

Consider a 35-year-old male opting for this plan with a sum assured of ₹11 lakhs and a premium payment term of 10 years.

The plan runs for 25 years, during which the survival benefit is paid annually. He chooses the Extended Benefit option.

| Male | 35 years |

| Sum Assured | ₹ 11,00,000 |

| Policy Term | 25 years |

| Premium Paying Term | 10 years |

| Annualised Premium | ₹ 1,00,000 |

| Age | Year | Annualised premium / Maturity benefit | Death benefit |

| 35 | 1 | -1,00,000 | 11,00,000 |

| 36 | 2 | -65,550 | 11,00,000 |

| 37 | 3 | -65,550 | 11,00,000 |

| 38 | 4 | -65,550 | 11,00,000 |

| 39 | 5 | -65,550 | 11,00,000 |

| 40 | 6 | -65,550 | 11,00,000 |

| 41 | 7 | -65,550 | 11,00,000 |

| 42 | 8 | -65,550 | 11,00,000 |

| 43 | 9 | -65,550 | 11,00,000 |

| 44 | 10 | -65,550 | 11,00,000 |

| 45 | 11 | 34,450 | 11,00,000 |

| 46 | 12 | 34,450 | 11,00,000 |

| 47 | 13 | 34,450 | 11,00,000 |

| 48 | 14 | 34,450 | 11,00,000 |

| 49 | 15 | 34,450 | 11,00,000 |

| 50 | 16 | 34,450 | 11,00,000 |

| 51 | 17 | 34,450 | 11,00,000 |

| 52 | 18 | 34,450 | 11,00,000 |

| 53 | 19 | 34,450 | 11,00,000 |

| 54 | 20 | 34,450 | 11,00,000 |

| 55 | 21 | 34,450 | 11,00,000 |

| 56 | 22 | 34,450 | 11,00,000 |

| 57 | 23 | 34,450 | 11,00,000 |

| 58 | 24 | 34,450 | 11,00,000 |

| 59 | 25 | 34,450 | 11,00,000 |

| 60 | 10,34,450 | ||

| IRR | 4.67% |

Starting from the end of the first policy year, the plan provides a guaranteed income of ₹34,450, along with a maturity benefit of ₹10 lakhs.

However, the Internal Rate of Return (IRR) works out to just 4.67% as per the Bandhan Life Guaranteed Income Plan maturity calculator, which is lower than what most debt instruments offer.

In addition, both the guaranteed income and the sum assured are insufficient. Over such a long term, these payouts fail to keep up with inflation, making the Bandhan Life Guaranteed Income Plan a weak fit for a well-diversified financial portfolio.

Bandhan Life Guaranteed Income Plan Vs. Other Investments

Analysing cash flows and comparing returns across investment options is crucial for making informed financial decisions.

To ensure a fair assessment, we apply the same evaluation framework used earlier. Since the Bandhan Life Guaranteed Income Plan combines life cover with survival benefits, we break these components apart to understand their true value.

Bandhan Life Guaranteed Income Plan Vs. Pure-term + Equity Mutual Fund

A pure-term insurance policy with a ₹11 lakh sum assured costs around ₹10,800 annually for a 10-year premium payment term and a 25-year policy duration.

The remaining ₹89,200 can then be invested according to one’s risk profile, allowing the accumulated corpus to generate systematic annual withdrawals—similar to the survival benefits offered by the Bandhan Life Guaranteed Income Plan.

| Pure Term Life Insurance Policy | |

| Sum Assured | ₹ 11,00,000 |

| Policy Term | 25 years |

| Premium Paying Term | 10 years |

| Annualised Premium | ₹ 10,800 |

| Investment | ₹ 89,200 |

Assume this surplus premium is invested in an equity mutual fund. The investment supports yearly withdrawals that match the plan’s survival benefits.

At the end of 25 years, the entire investment is redeemed to replicate the maturity benefit of the Bandhan Life Guaranteed Income Plan.

| Term insurance + Equity Mutual Fund | |||

| Age | Year | Term Insurance premium + Equity Mutual Fund | Death benefit |

| 35 | 1 | -1,00,000 | 11,00,000 |

| 36 | 2 | -65,550 | 11,00,000 |

| 37 | 3 | -65,550 | 11,00,000 |

| 38 | 4 | -65,550 | 11,00,000 |

| 39 | 5 | -65,550 | 11,00,000 |

| 40 | 6 | -65,550 | 11,00,000 |

| 41 | 7 | -65,550 | 11,00,000 |

| 42 | 8 | -65,550 | 11,00,000 |

| 43 | 9 | -65,550 | 11,00,000 |

| 44 | 10 | -65,550 | 11,00,000 |

| 45 | 11 | 34,450 | 11,00,000 |

| 46 | 12 | 34,450 | 11,00,000 |

| 47 | 13 | 34,450 | 11,00,000 |

| 48 | 14 | 34,450 | 11,00,000 |

| 49 | 15 | 34,450 | 11,00,000 |

| 50 | 16 | 34,450 | 11,00,000 |

| 51 | 17 | 34,450 | 11,00,000 |

| 52 | 18 | 34,450 | 11,00,000 |

| 53 | 19 | 34,450 | 11,00,000 |

| 54 | 20 | 34,450 | 11,00,000 |

| 55 | 21 | 34,450 | 11,00,000 |

| 56 | 22 | 34,450 | 11,00,000 |

| 57 | 23 | 34,450 | 11,00,000 |

| 58 | 24 | 34,450 | 11,00,000 |

| 59 | 25 | 34,450 | 11,00,000 |

| 60 | 45,34,756 | ||

| IRR | 10.59% | ||

Since annual withdrawals fall within the ₹1.25 lakh capital gains exemption limit, tax applies only at final redemption.

The investment grows to ₹50.37 lakhs, and after capital gains tax, the post-tax value stands at ₹45.34 lakhs. This cash flow delivers an impressive 10.59% IRR.

| Equity Mutual Fund Tax Calculation | |

| Maturity value after 25 years | 50,37,293 |

| Purchase price | 8,92,000 |

| Long-Term Capital Gains | 41,45,293 |

| Exemption limit | 1,25,000 |

| Taxable LTCG | 40,20,293 |

| Tax paid on LTCG | 5,02,537 |

| Maturity value after tax | 45,34,756 |

This alternative approach not only beats inflation but also offers far greater flexibility to adjust withdrawals as per financial needs.

When compared side-by-side, it becomes evident that more efficient strategies exist for generating regular income. The Bandhan Life Guaranteed Income Plan, therefore, falls short as an optimal investment option.

Final Verdict on Bandhan Life Guaranteed Income Plan

The Bandhan Life Guaranteed Income Plan provides survival benefits and a maturity benefit—either as a lump sum or as regular payouts.

While these benefits are guaranteed, the returns are notably subpar. A guaranteed structure alone should not justify including this plan in your portfolio.

Additionally, the sum assured is inadequate, and when combined with the plan’s low returns, its overall effectiveness diminishes even further and it also has a high agent commission.

This makes it an unsuitable choice for a well-balanced investment portfolio. Traditional life insurance policies like these are best avoided for meeting regular income needs.

A more efficient approach is to build a strong corpus through investments aligned with your risk appetite. This not only offers better returns and liquidity but also allows you to choose the right amount of life cover to protect your family.

A pure-term life insurance policy provides essential protection, while a diversified investment portfolio helps grow your wealth effectively.

Do Quora, Facebook, and Twitter have the final say when it comes to financial advice?

Since standard payout-based insurance plans don’t suit everyone, consulting a certified financial planner is advisable. A personalised plan based on your risk profile and long-term goals will help you achieve financial security in a more efficient and structured way.

Leave a Reply