Is the Digit Icon Guaranteed Savings Plan – Whole Life Variant truly a lifetime solution for financial security, or are there smarter investment paths you should explore?

Can the Whole Life Variant of the Digit Icon Guaranteed Savings Plan genuinely support your long-term goals, or is it just another traditional policy presented with modern packaging?

Is choosing the Digit Icon Guaranteed Savings Plan – Whole Life Variant a strategic move for wealth protection, or could your money work harder in better-performing investment options?

In this review, we break down the plan’s features, benefits, and limitations, and provide a detailed illustration to help you understand its real value.

Table of Contents

What is the Digit Icon Guaranteed Savings Plan – Whole Life?

What are the features of the Digit Icon Guaranteed Savings Plan – Whole Life?

What are the plan variants in the Digit Icon Guaranteed Savings Plan – Whole Life?

What are the benefits of the Digit Icon Guaranteed Savings Plan – Whole Life?

Grace Period, Discontinuance and Revival of the Digit Icon Guaranteed Savings Plan – Whole Life

Free Look Period for the Digit Icon Guaranteed Savings Plan – Whole Life

Surrendering the Digit Icon Guaranteed Savings Plan – Whole Life

What are the advantages of the Digit Icon Guaranteed Savings Plan – Whole Life?

What are the disadvantages of the Digit Icon Guaranteed Savings Plan – Whole Life?

Research Methodology of Digit Icon Guaranteed Savings Plan – Whole Life

Benefit Illustration – IRR Analysis of Digit Icon Guaranteed Savings Plan – Whole Life

Digit Icon Guaranteed Savings Plan – Whole Life Vs. Other Investments

Digit Icon Guaranteed Savings Plan – Whole Life Vs. Pure-term + Equity Mutual Fund

Final Verdict on the Digit Icon Guaranteed Savings Plan – Whole Life

What is the Digit Icon Guaranteed Savings Plan – Whole Life?

Digit Icon Guaranteed Savings Plan is a non-linked, non-participating individual life insurance savings plan. It provides both life insurance protection and guaranteed income or maturity benefits, depending on the variant chosen by the policyholder.

What are the features of the Digit Icon Guaranteed Savings Plan – Whole Life?

- Comprehensive Life Cover: Provides strong financial protection for your family through a robust life insurance component.

- Assured Returns: Offers fixed, guaranteed returns that remain unaffected by market fluctuations.

- Enhanced Protection: In case of accidental death, the nominee receives twice the Sum Assured, strengthening the safety net.

- Tax Benefits: Premiums qualify for deductions under Section 80C, and payouts enjoy exemptions under Section 10(10D) of the Income Tax Act.

- Guaranteed Income: Ensures a steady income flow throughout the chosen payout period.

What are the plan variants in the Digit Icon Guaranteed Savings Plan – Whole Life?

There are four variants under the plan.

- Lump-sum Benefit

- Income Benefit

- Income + Lumpsum Benefit

- Whole Life Benefit

This article focuses on the Whole Life benefit variant.

What are the benefits of the Digit Icon Guaranteed Savings Plan – Whole Life?

Death benefit

For Single Life (with only one Life Assured under the Policy), the Death Benefit payable shall be the highest of the following:

- Sum Assured on Death plus accrued special additions, if any, OR

- 105% of Total Premiums Paid as on the date of death of the Life Assured, OR

- Surrender Value applicable as on the date of death of the Life Assured.

For Joint Life (with two lives being assured under the Policy)

Under Joint Life, two lives will be covered under one Policy. Joint Life Option shall be available for the Single Premium Policy only.

In case of the first death during the Policy Term, the Death Benefit equal to 1.25 times of Single Premium shall be payable. The Policy shall continue till the occurrence of the second death or till Policy Maturity Date, whichever is earlier.

In case of second death during the Policy Term, the Death Benefit equal to 10 times of Single Premium plus accrued Special Additions, if any, shall be payable.

Accidental Death Benefit is an in-built feature

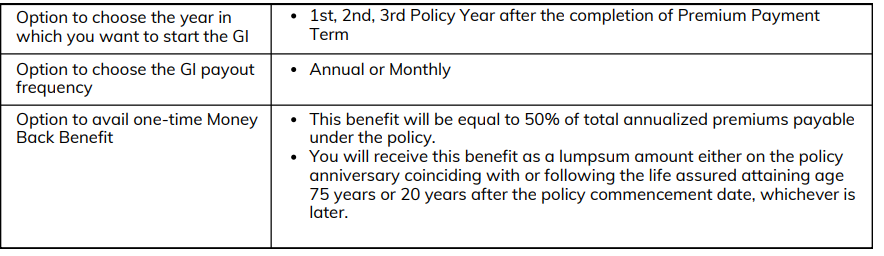

Survival Benefit

Under the Whole Life variant, a regular stream of Guaranteed Income will start after the completion of the premium payment term.

Additionally, a one-time lump sum Money Back Benefit will also be paid as a survival benefit during the policy term, if you choose to avail the money back benefit at inception. The following options will be available to you at inception under the Whole Life Benefit variant:

Maturity Benefit

Sum Assured on Maturity, which will be equal to 100% of total annualised premiums payable under the policy.

Staggered Maturity Benefit: Policyholder can choose to receive it in the form of a regular stream of Guaranteed Income after the Policy Maturity Date, over a chosen period called staggered maturity period and a lump sum amount (if opted for) at the end of such staggered maturity period.

However, no Death benefit will be available during the staggered maturity period.

Grace Period, Discontinuance and Revival of the Digit Icon Guaranteed Savings Plan – Whole Life

Grace Period

A Grace Period of fifteen (15) days from the due date of the first unpaid Premium for Policies with a monthly Premium payment frequency and thirty (30) days from the due date of the first unpaid Premium for all other available Premium payment frequencies will be allowed for the payment of each due Premium instalment.

Discontinuance

Lapse: If at least one full year’s Premiums have not been paid, the Policy will lapse on the expiry of the Grace Period until the Policy is revived for full Benefits within the Revival Period.

Reduced paid-up: If at least one full year’s Premiums have been paid and if any subsequent Premium which is due has not been paid by the end of the Grace Period, the Policy will acquire reduced paid-up status, and the Policyholder / Claimant will be eligible for Reduced Paid-up Benefit.

Revival

If the policy is in lapsed or in reduced paid-up status, it may be revived for full Benefits before the Policy Maturity Date, but within five years from the due date for payment of the first unpaid Premium.

Free Look Period for the Digit Icon Guaranteed Savings Plan – Whole Life

If you do not agree with the terms and conditions of the Policy, you have the option to request cancellation of the Policy by returning the original Policy Document (in case the physical copy of the Policy Document was sent to the Policyholder) along with a written request stating the reasons for objection within 30 days from the date of receipt of the Policy Document.

Surrendering the Digit Icon Guaranteed Savings Plan – Whole Life

In case of Single Premium Policies, the Policy can be surrendered at any time after the Policy Commencement Date.

For Limited Pay and Regular Pay Policies, the Policy can be surrendered any time after completion of the first Policy Year, provided at least one full year’s Premiums have been paid.

The Surrender Value payable shall be the higher of Guaranteed Surrender Value (GSV) or Special Surrender Value (SSV).

What are the advantages of the Digit Icon Guaranteed Savings Plan – Whole Life?

- Senior Citizen Health Benefits: Additional health-related advantages are provided for senior citizens.

- Wellness Benefits: Encourages and rewards maintaining a healthy lifestyle.

- Premium Offset Option: You can use all or part of the survival benefit to offset future premiums when they become due.

- Flexible Income Dates: Allows you to receive the guaranteed income on a chosen Special Date, not just on the policy anniversary.

What are the disadvantages of the Digit Icon Guaranteed Savings Plan – Whole Life?

- No Policy Continuance or Family Income Benefit: The Whole Life Variant does not provide policy continuance benefits or a family income benefit.

- Modest Returns: Although the Digit Icon Guaranteed Savings plan offers guaranteed payouts, the overall returns remain relatively low.

- Limited Sum Assured: The life cover may not be adequate to fully address your long-term financial requirements.

Research Methodology of Digit Icon Guaranteed Savings Plan – Whole Life

The Digit Icon Guaranteed Savings – Whole Life Plan provides a unique feature: regular income for life. While this may appear attractive, it shouldn’t be the only reason to opt for the Digit Icon Guaranteed Savings plan.

A sound decision requires assessing the potential returns. Below is an illustration based on details from the policy brochure.

Benefit Illustration – IRR Analysis of Digit Icon Guaranteed Savings Plan – Whole Life

A 50-year-old male chooses the Digit Icon Guaranteed Savings – Whole Life Plan with a Sum Assured of ₹10 lakhs. The policy term is 50 years, with a premium payment term of 10 years and an annual premium of ₹1,00,000.

| Male | 50 years |

| Sum Assured | ₹ 10,00,000 |

| Policy Term | 50 years |

| Premium Paying Term | 10 years |

| Annualised Premium | ₹ 1,00,000 |

After completing the premium payment term, he begins receiving an annual guaranteed income of ₹76,977 for life. A maturity benefit of ₹10 lakhs is payable at the end of the policy term.

Assuming a life expectancy of 85 years, the overall Internal Rate of Return (IRR) works out to 5.15% as per the Digit Icon Guaranteed Savings Plan maturity calculator.

| Age | Year | Annualised premium / Maturity benefit | Death benefit |

| 50 | 1 | -1,00,000 | 10,00,000 |

| 51 | 2 | -1,00,000 | 10,00,000 |

| 52 | 3 | -1,00,000 | 10,00,000 |

| 53 | 4 | -1,00,000 | 10,00,000 |

| 54 | 5 | -1,00,000 | 10,00,000 |

| 55 | 6 | -1,00,000 | 10,00,000 |

| 56 | 7 | -1,00,000 | 10,00,000 |

| 57 | 8 | -1,00,000 | 10,00,000 |

| 58 | 9 | -1,00,000 | 10,00,000 |

| 59 | 10 | -1,00,000 | 10,00,000 |

| 60 | 11 | 0 | 10,00,000 |

| 61 | 12 | 76,977 | 10,00,000 |

| 62 | 13 | 76,977 | 10,00,000 |

| 63 | 14 | 76,977 | 10,00,000 |

| 64 | 15 | 76,977 | 10,00,000 |

| 65 | 16 | 76,977 | 10,00,000 |

| 66 | 17 | 76,977 | 10,00,000 |

| 67 | 18 | 76,977 | 10,00,000 |

| 68 | 19 | 76,977 | 10,00,000 |

| 69 | 20 | 76,977 | 10,00,000 |

| 70 | 21 | 76,977 | 10,00,000 |

| 71 | 22 | 76,977 | 10,00,000 |

| 72 | 23 | 76,977 | 10,00,000 |

| 73 | 24 | 76,977 | 10,00,000 |

| 74 | 25 | 76,977 | 10,00,000 |

| 75 | 26 | 76,977 | 10,00,000 |

| 76 | 27 | 76,977 | 10,00,000 |

| 77 | 28 | 76,977 | 10,00,000 |

| 78 | 29 | 76,977 | 10,00,000 |

| 79 | 30 | 76,977 | 10,00,000 |

| 80 | 31 | 76,977 | 10,00,000 |

| 81 | 32 | 76,977 | 10,00,000 |

| 82 | 33 | 76,977 | 10,00,000 |

| 83 | 34 | 76,977 | 10,00,000 |

| 84 | 35 | 76,977 | 10,00,000 |

| 85 | 10,00,000 | ||

| IRR | 5.15% |

Despite offering lifetime income, the Digit Icon Guaranteed Savings plan delivers low returns, which significantly reduces its attractiveness. Moreover, the guaranteed income is fixed and does not factor in inflation, resulting in declining purchasing power over time.

The insurance component is also limited—the life cover until age 99 is more than what most individuals require, and the sum assured is insufficient to meet meaningful financial goals.

In summary, both the investment and insurance components of the Digit Icon Guaranteed Savings – Whole Life Plan offer limited value, making it an ineffective choice for most investors.

Digit Icon Guaranteed Savings Plan – Whole Life Vs. Other Investments

The regular income offered by the Digit Icon Guaranteed Savings – Whole Life Plan does not keep pace with inflation.

A more effective strategy is to separate your insurance and investment components, allowing you to create an inflation-adjusted income stream while ensuring adequate life cover. The following illustration highlights the advantages of this approach. A pure-term life insurance policy with a sum assured of ₹10 lakhs costs an annual premium of ₹23,300 for a 20-year term. This leaves you with ₹76,700 per year to invest. For the first 10 years, this amount can be invested in either equity or debt instruments. In this example, it is allocated to an equity mutual fund scheme. After 10 years, the accumulated corpus is moved to an instrument delivering a 7% annual return, enabling regular withdrawals similar to those offered by the Digit Icon Guaranteed Savings – Whole Life Plan. The post-tax accumulated corpus after 10 years stands at ₹14.30 lakhs. When this corpus earns a 7% return, it supports annual withdrawals comparable to the Digit Icon Guaranteed Savings plan while still retaining value. By age 85, the remaining corpus is ₹29.72 lakhs—almost three times the final payout of the Digit plan. This strategy yields an IRR of 6.84%. If withdrawals are delayed in the initial years, the power of compounding further enhances both the corpus and the eventual IRR. Another key advantage is flexibility: you can adjust withdrawal amounts as your needs change, including increasing them over time to offset inflation’s impact. By separating insurance from investment, you achieve better returns, greater control, and a more resilient financial strategy that clearly outperforms the Digit Icon Guaranteed Savings – Whole Life Plan. The Digit Icon Guaranteed Savings – Whole Life Plan allows you to pay premiums for a limited period and receive income for life. While this may seem attractive for those seeking steady cash flow, a deeper analysis shows that the Digit Icon Guaranteed Savings plan underdelivers in terms of returns and it also has a high agent commission. Although it provides whole-life coverage, the sum assured is too low to meet meaningful financial goals. In personal finance, life cover should be aligned with your responsibilities, future goals, and liabilities—primarily during your working years when protection matters most. The plan’s shortcomings include modest returns, inadequate life cover, and a rigid income structure that offers fixed payouts for life, leaving no room to adjust for inflation or evolving financial needs. A more effective strategy is to separate insurance from investment. Pure-term insurance policies provide substantial life cover at a reasonable cost, ensuring your family’s financial security. Meanwhile, directing your savings into appropriate investment products helps you build a corpus that can support your long-term goals and generate flexible, inflation-adjusted income. Choose investments based on your risk profile, time horizon, and financial objectives. Do Quora, Facebook, and Twitter have the final say when it comes to financial advice? If you’re uncertain about structuring your insurance and investment plan, consulting a certified Financial Planner can help you design a strategy tailored to your needs.

Pure Term Life Insurance Policy

Sum Assured

₹ 10,00,000

Policy Term

20 years

Premium Paying Term

10 years

Annualised Premium

₹ 23,300

Investment

₹ 76,700

Age

Year

Term Insurance premium + Equity Mutual Fund

Death benefit

50

1

-1,00,000

10,00,000

51

2

-1,00,000

10,00,000

52

3

-1,00,000

10,00,000

53

4

-1,00,000

10,00,000

54

5

-1,00,000

10,00,000

55

6

-1,00,000

10,00,000

56

7

-1,00,000

10,00,000

57

8

-1,00,000

10,00,000

58

9

-1,00,000

10,00,000

59

10

-1,00,000

10,00,000

60

11

0

10,00,000

61

12

76,977

10,00,000

62

13

76,977

10,00,000

63

14

76,977

10,00,000

64

15

76,977

10,00,000

65

16

76,977

10,00,000

66

17

76,977

10,00,000

67

18

76,977

10,00,000

68

19

76,977

10,00,000

69

20

76,977

10,00,000

70

21

76,977

10,00,000

71

22

76,977

10,00,000

72

23

76,977

10,00,000

73

24

76,977

10,00,000

74

25

76,977

10,00,000

75

26

76,977

10,00,000

76

27

76,977

10,00,000

77

28

76,977

10,00,000

78

29

76,977

10,00,000

79

30

76,977

10,00,000

80

31

76,977

10,00,000

81

32

76,977

10,00,000

82

33

76,977

10,00,000

83

34

76,977

10,00,000

84

35

76,977

10,00,000

85

29,72,568

IRR

6.84%

Equity Mutual Fund Tax Calculation

Maturity value after 10 years

15,07,507

Purchase price

7,67,000

Long-Term Capital Gains

7,40,507

Exemption limit

1,25,000

Taxable LTCG

6,15,507

Tax paid on LTCG

76,938

Maturity value after tax

14,30,568

Final Verdict on the Digit Icon Guaranteed Savings Plan – Whole Life

Leave a Reply