Is the Edelweiss Life Premier Guaranteed STAR Plan truly a “premier” choice for guaranteed savings — or just another traditional product with modest returns?

Does the Edelweiss Life Premier Guaranteed STAR Plan’s guaranteed additions make up for lower growth potential — or do they fall short compared to market-linked alternatives?

Can this Edelweiss Life Premier Guaranteed STAR Plan truly provide peace of mind for retirees — or will it underdeliver compared to diversified retirement strategies?

To evaluate this, let us examine the plan’s features, assess its advantages and limitations, and analyse the benefit illustration provided in the policy brochure through a detailed calculation.

Table of Contents:

What is the Edelweiss Life Premier Guaranteed Star?

What are the features of the Edelweiss Life Premier Guaranteed Star?

Who is eligible for the Edelweiss Life Premier Guaranteed Star?

What are the benefits of the Edelweiss Life Premier Guaranteed Star?

Grace Period, Discontinuance and Revival of the Edelweiss Life Premier Guaranteed Star

Free Look Period for the Edelweiss Life Premier Guaranteed Star

Surrendering the Edelweiss Life Premier Guaranteed Star

What are the advantages of the Edelweiss Life Premier Guaranteed Star?

What are the disadvantages of the Edelweiss Life Premier Guaranteed Star?

Research Methodology of Edelweiss Life Premier Guaranteed Star

Benefit Illustration – IRR Analysis of Edelweiss Life Premier Guaranteed Star

Edelweiss Life Premier Guaranteed Star Vs. Other Investments

Edelweiss Life Premier Guaranteed Star Vs. Pure-term + Equity Mutual Fund

Final Verdict on Edelweiss Life Premier Guaranteed Star

What is the Edelweiss Life Premier Guaranteed Star?

Edelweiss Life Premier Guaranteed Star is an Individual, Non-Linked, Non-Participating, Savings, Life Insurance Product.

It is a life insurance plan designed to protect your family from any financial loss in case of an untimely death, and also offers a guaranteed regular income and/or a guaranteed lump sum on maturity to you and your family, provided all due premiums are paid.

What are the features of the Edelweiss Life Premier Guaranteed Star?

- Provides life insurance coverage to safeguard your family’s financial security.

- Helps support future goals by offering stable, assured returns in the form of regular income.

- Offers flexibility to customise the plan through multiple policy term and premium payment term options, along with a maturity benefit.

- Allows the addition of riders to enhance protection, subject to an additional premium.

- Eligible for tax benefits on premiums paid and benefits received, as per prevailing tax laws.

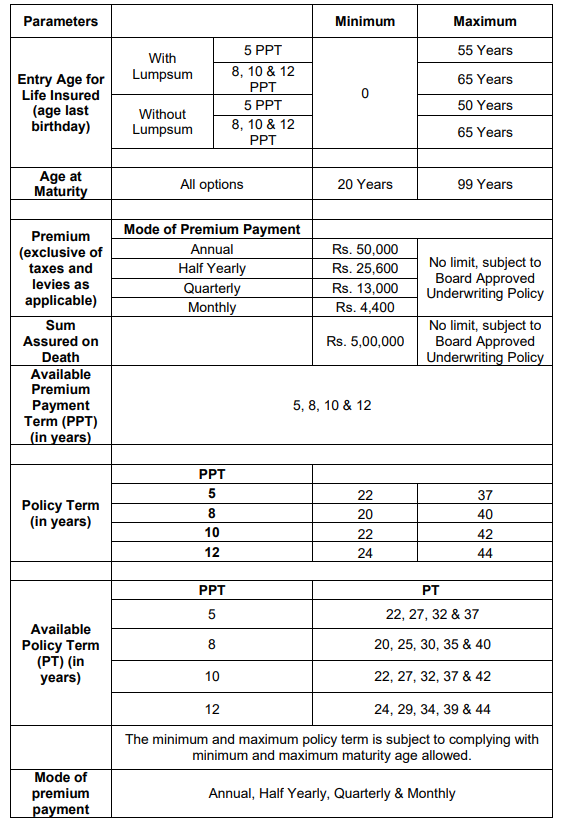

Who is eligible for the Edelweiss Life Premier Guaranteed Star?

What are the benefits of the Edelweiss Life Premier Guaranteed Star?

1. Death Benefit

The Death Benefit under this product is Sum Assured on Death. The Sum Assured on Death at any point in time, provided the Edelweiss Life Premier Guaranteed STAR Plan policy is in force, is the highest of:

- 10 times the Annualised Premium

- Any Absolute amount assured to be paid on death

- 10 times the Annual Premium

2. Income Benefit Pay-outs

‘Income Benefit Pay-out’ (expressed as a % of Annualised Premium) is a regular stream of income payable as survival benefits during the ‘Income Duration’.

‘Income Benefit Pay-out’ starting from the third policy year falling after the completion of PPT and will be payable in arrears till maturity or death of the Life Insured, whichever is earlier, while the Edelweiss Life Premier Guaranteed STAR Plan policy is in force.

‘Income Duration’ is equal to Policy Term (PT) – Premium Paying Term (PPT) – 2

The amount of Income Benefit Pay-out will increase by 5.00% after every 5 policy years (on a simple basis).

3. Maturity Benefit

If ‘Lumpsum Benefit’ is chosen:

If the Life Insured survives till the end of the Edelweiss Life Premier Guaranteed STAR Plan policy term, Sum Assured on Maturity will be payable on the maturity of the policy along with the last Income Benefit Pay-Out instalment as per the applicable Income Benefit pay-outs, and the policy will terminate without any further benefit.

Sum Assured on Maturity = Maximum of (10, PPT) times the Annualised Premium

If ‘Lumpsum Benefit’ is not chosen:

If the Life Insured survives till the end of the Edelweiss Life Premier Guaranteed STAR Plan policy term, no maturity benefit is payable; however, the last Income Benefit Pay-Out instalment will be payable as per the applicable Income Benefit pay-outs, and the policy will terminate without any further benefit.

Grace Period, Discontinuance and Revival of the Edelweiss Life Premier Guaranteed Star

Grace Period

The company will allow a Grace Period of 15 days, where the Edelweiss Life Premier Guaranteed STAR Plan Policyholder pays the premium on a monthly basis, and 30 days in all other cases, during which you must pay the premium due in full.

Discontinuance

If all the Premiums for at least the first Policy Year have not been paid in full within the Grace Period, the Policy shall immediately and automatically lapse, and no benefits shall be payable by us under the Policy.

After completion of the first policy year, provided one full year’s Premium has been paid and if we do not receive subsequent Premiums within the Grace Period, the Policy will acquire Reduced Paid-up status, and benefits will continue as per the Reduced Paid-up provision

Revival

If the premiums are not paid within the grace period, the Edelweiss Life Premier Guaranteed STAR Plan policy lapses and the policy may be revived within the Revival Period of five consecutive years from the date of the first unpaid premium.

Free Look Period for the Edelweiss Life Premier Guaranteed Star

You have a Free Look period of thirty (30) days beginning from the date of receipt of the Policy Document, whether received electronically or otherwise, to review the terms and conditions of this Edelweiss Life Premier Guaranteed STAR Plan Policy.

If you disagree with any of the terms or conditions, or otherwise, and you have not made any claims, you may return this Policy for cancellation.

Surrendering the Edelweiss Life Premier Guaranteed Star

After completion of the first policy year, provided one full year’s Premium has been paid, your policy will acquire a Surrender Value. On receipt of a written request for Surrender, the Surrender Value, if any, will be immediately paid.

The Surrender Value payable is the higher of Guaranteed Surrender Value (GSV) and Special Surrender Value (SSV).

What are the advantages of the Edelweiss Life Premier Guaranteed Star?

- The maximum loan available is capped at 60% of the surrender value.

- Provides enhanced protection through optional riders.

- Offers guaranteed payouts that increase at regular intervals of every five years.

What are the disadvantages of the Edelweiss Life Premier Guaranteed Star?

- The life insurance cover offered is inadequate to provide meaningful financial protection.

- Annual income payouts may encourage unplanned or discretionary spending.

- The income benefit cannot be deferred, limiting alignment with specific financial requirements.

- Regular annual withdrawals disrupt the power of compounding, thereby constraining long-term wealth creation.

Research Methodology of Edelweiss Life Premier Guaranteed Star

The Edelweiss Life Premier Guaranteed Star Plan offers annual cash payouts that increase over time, along with a maturity benefit payable at the end of the Edelweiss Life Premier Guaranteed STAR Plan policy term, depending on the option selected.

However, guaranteed cash flows alone should not be the sole criterion for investing in this plan. The more relevant metric is the return generated. To assess this, let us examine an illustration and compute the Internal Rate of Return (IRR).

Benefit Illustration – IRR Analysis of Edelweiss Life Premier Guaranteed Star

Consider a 35-year-old male who opts for the Edelweiss Life Premier Guaranteed Star Plan with a base sum assured of ₹50 lakhs.

The policy term is 44 years, with a premium payment term of 12 years, requiring an annual premium of ₹5 lakhs. He chooses the Lump sum option.

| Male | 35 years |

| Sum Assured | ₹ 50,00,000 |

| Policy Term | 44 years |

| Premium Paying Term | 12 years |

| Annualised Premium | ₹ 5,00,000 |

Income benefits commence after 15 years. The first annual payout is ₹6.86 lakhs, which increases by 5.00% every five policy years on a simple basis.

In addition, a maturity benefit of ₹60 lakhs is payable at the end of the policy term. Based on these cash flows, the IRR works out to approximately 6.55% as per the Edelweiss Life Premier Guaranteed STAR Plan maturity calculator.

| Age | Year | Annualised premium / Maturity benefit | Death benefit |

| 35 | 1 | -5,00,000 | 50,00,000 |

| 36 | 2 | -5,00,000 | 50,00,000 |

| 37 | 3 | -5,00,000 | 50,00,000 |

| 38 | 4 | -5,00,000 | 50,00,000 |

| 39 | 5 | -5,00,000 | 50,00,000 |

| 40 | 6 | -5,00,000 | 50,00,000 |

| 41 | 7 | -5,00,000 | 50,00,000 |

| 42 | 8 | -5,00,000 | 50,00,000 |

| 43 | 9 | -5,00,000 | 50,00,000 |

| 44 | 10 | -5,00,000 | 50,00,000 |

| 45 | 11 | -5,00,000 | 50,00,000 |

| 46 | 12 | -5,00,000 | 50,00,000 |

| 47 | 13 | 0 | 50,00,000 |

| 48 | 14 | 0 | 50,00,000 |

| 49 | 15 | 0 | 50,00,000 |

| 50 | 16 | 6,86,386 | 50,00,000 |

| 51 | 17 | 6,86,386 | 50,00,000 |

| 52 | 18 | 6,86,386 | 50,00,000 |

| 53 | 19 | 6,86,386 | 50,00,000 |

| 54 | 20 | 6,86,386 | 50,00,000 |

| 55 | 21 | 7,20,705 | 50,00,000 |

| 56 | 22 | 7,20,705 | 50,00,000 |

| 57 | 23 | 7,20,705 | 50,00,000 |

| 58 | 24 | 7,20,705 | 50,00,000 |

| 59 | 25 | 7,20,705 | 50,00,000 |

| 60 | 26 | 7,55,025 | 50,00,000 |

| 61 | 27 | 7,55,025 | 50,00,000 |

| 62 | 28 | 7,55,025 | 50,00,000 |

| 63 | 29 | 7,55,025 | 50,00,000 |

| 64 | 30 | 7,55,025 | 50,00,000 |

| 65 | 31 | 7,89,344 | 50,00,000 |

| 66 | 32 | 7,89,344 | 50,00,000 |

| 67 | 33 | 7,89,344 | 50,00,000 |

| 68 | 34 | 7,89,344 | 50,00,000 |

| 69 | 35 | 7,89,344 | 50,00,000 |

| 70 | 36 | 8,23,663 | 50,00,000 |

| 71 | 37 | 8,23,663 | 50,00,000 |

| 72 | 38 | 8,23,663 | 50,00,000 |

| 73 | 39 | 8,23,663 | 50,00,000 |

| 74 | 40 | 8,23,663 | 50,00,000 |

| 75 | 41 | 8,57,983 | 50,00,000 |

| 76 | 42 | 8,57,983 | 50,00,000 |

| 77 | 43 | 8,57,983 | 50,00,000 |

| 78 | 44 | 8,57,983 | 50,00,000 |

| 79 | 68,57,983 | ||

| IRR | 6.55% |

Although the plan provides guaranteed and predictable payouts, the income may not be adequate to meet large financial requirements.

Since the income benefit cannot be deferred, it may also result in avoidable or unplanned spending. Moreover, the life insurance cover is insufficient to adequately protect the family’s long-term financial interests.

In conclusion, while the Edelweiss Life Premier Guaranteed Star Plan combines guaranteed benefits with life insurance coverage over an extended period, the limited flexibility in benefit payouts and the inadequate level of protection make it an unsuitable choice for achieving long-term financial goals.

Edelweiss Life Premier Guaranteed Star Vs. Other Investments

Edelweiss Life Premier Guaranteed Star offers assured benefits, including increasing income payouts and life insurance coverage throughout the policy term.

However, a more effective approach may be to separate insurance and investment, thereby aiming for comparable benefits with the potential for superior returns.

Edelweiss Life Premier Guaranteed Star Vs. Pure-term + Equity Mutual Fund

Using the same assumptions as the earlier illustration, consider opting for a pure-term life insurance policy with a sum assured of ₹50 lakhs.

The annual premium is ₹17,600, payable for 10 years, with a policy term of 30 years—coverage limited to the working years is typically sufficient. This structure leaves approximately ₹4.82 lakhs per year available for investment, which can be deployed in line with the investor’s risk appetite.

| Pure Term Life Insurance Policy | |

| Sum Assured | ₹ 50,00,000 |

| Policy Term | 30 years |

| Premium Paying Term | 10 years |

| Annualised Premium | ₹ 17,600 |

| Investment | ₹ 4,82,400 |

Conservative investors may prefer instruments such as the Public Provident Fund (PPF), while those with a higher risk tolerance can consider equity-oriented options such as equity mutual funds.

In this illustration, the surplus is assumed to be invested in an equity mutual fund scheme.

| Age | Year | Term Insurance premium + Equity Mutual Fund | Death benefit |

| 35 | 1 | -5,00,000 | 50,00,000 |

| 36 | 2 | -5,00,000 | 50,00,000 |

| 37 | 3 | -5,00,000 | 50,00,000 |

| 38 | 4 | -5,00,000 | 50,00,000 |

| 39 | 5 | -5,00,000 | 50,00,000 |

| 40 | 6 | -5,00,000 | 50,00,000 |

| 41 | 7 | -5,00,000 | 50,00,000 |

| 42 | 8 | -5,00,000 | 50,00,000 |

| 43 | 9 | -5,00,000 | 50,00,000 |

| 44 | 10 | -5,00,000 | 50,00,000 |

| 45 | 11 | -5,00,000 | 50,00,000 |

| 46 | 12 | -5,00,000 | 50,00,000 |

| 47 | 13 | 0 | 50,00,000 |

| 48 | 14 | 0 | 50,00,000 |

| 49 | 15 | 0 | 50,00,000 |

| 50 | 16 | 6,86,386 | 50,00,000 |

| 51 | 17 | 6,86,386 | 50,00,000 |

| 52 | 18 | 6,86,386 | 50,00,000 |

| 53 | 19 | 6,86,386 | 50,00,000 |

| 54 | 20 | 6,86,386 | 50,00,000 |

| 55 | 21 | 7,20,705 | 50,00,000 |

| 56 | 22 | 7,20,705 | 50,00,000 |

| 57 | 23 | 7,20,705 | 50,00,000 |

| 58 | 24 | 7,20,705 | 50,00,000 |

| 59 | 25 | 7,20,705 | 50,00,000 |

| 60 | 26 | 7,55,025 | 50,00,000 |

| 61 | 27 | 7,55,025 | 50,00,000 |

| 62 | 28 | 7,55,025 | 50,00,000 |

| 63 | 29 | 7,55,025 | 50,00,000 |

| 64 | 30 | 7,55,025 | 50,00,000 |

| 65 | 31 | 7,89,344 | 50,00,000 |

| 66 | 32 | 7,89,344 | 50,00,000 |

| 67 | 33 | 7,89,344 | 50,00,000 |

| 68 | 34 | 7,89,344 | 50,00,000 |

| 69 | 35 | 7,89,344 | 50,00,000 |

| 70 | 36 | 8,23,663 | 50,00,000 |

| 71 | 37 | 8,23,663 | 50,00,000 |

| 72 | 38 | 8,23,663 | 50,00,000 |

| 73 | 39 | 8,23,663 | 50,00,000 |

| 74 | 40 | 8,23,663 | 50,00,000 |

| 75 | 41 | 8,57,983 | 50,00,000 |

| 76 | 42 | 8,57,983 | 50,00,000 |

| 77 | 43 | 8,57,983 | 50,00,000 |

| 78 | 44 | 8,57,983 | 50,00,000 |

| 79 | 5,05,98,735 | ||

| IRR | 8.41% |

To generate regular income, the accumulated equity mutual fund corpus can later be shifted to an instrument offering an assumed return of 7% per annum.

Withdrawals are structured to broadly mirror the income pattern of the Edelweiss Life Premier Guaranteed Star Plan, with the terminal value aligned to its maturity benefit.

| Equity Mutual Fund Tax Calculation | |

| Maturity value after 15 years | 1,83,77,346 |

| Purchase price | 58,24,000 |

| Long-Term Capital Gains | 1,25,53,346 |

| Exemption limit | 1,25,000 |

| Taxable LTCG | 1,24,28,346 |

| Tax paid on LTCG | 15,53,543 |

| Maturity value after tax | 1,68,23,803 |

Under this approach, the equity mutual fund investment grows to a pre-tax value of ₹1.83 crores and a post-tax value of ₹1.68 crores.

This corpus, when invested at 7% per annum and withdrawn periodically in a manner similar to the insurance plan, results in a final investment value of ₹5.05 crores.

The combined post-tax IRR of this strategy—comprising a pure-term insurance policy and equity mutual fund investments—works out to approximately 8.41%.

This return comfortably exceeds inflation, and refraining from periodic withdrawals could further enhance wealth creation.

Overall, when planning long-term financial goals, separating insurance from investments generally delivers more efficient and rewarding outcomes than relying on traditional life insurance-cum-investment products.

Final Verdict on Edelweiss Life Premier Guaranteed Star

The Edelweiss Life Premier Guaranteed Star Plan offers guaranteed, increasing income along with life insurance coverage.

While the promise of an assured income may appeal to investors seeking regular cash flows, the rigid payout structure is a significant limitation, as the benefits cannot be accumulated and taken at a later stage.

The rising income payouts are unlikely to meet large or inflation-adjusted expenses and may instead encourage discretionary spending. Moreover, the sum assured is inadequate to address long-term financial requirements and it also has a high agent commission.

By combining insurance and investment into a single product, the plan falls short on both protection and wealth creation.

From a long-term investment perspective, the plan does not align with the expectations of most investors. Those looking for a regular income are better served by investing separately through appropriate financial instruments rather than depending on cash payouts from a life insurance policy.

At the same time, safeguarding your family against unforeseen risks remains critical, and a pure-term life insurance policy is the most efficient solution for adequate life cover.

Do Quora, Facebook, and Twitter have the final say when it comes to financial advice?

To effectively achieve your financial goals, it is advisable to build an investment portfolio aligned with your risk appetite, financial objectives, and time horizon. Seeking guidance from a Certified Financial Planner can help you design a customised financial plan and ensure long-term financial security.

Leave a Reply