Is the Edelweiss Life Premier Guaranteed Star Pro Plan truly the key to long-term financial security, or are there smarter investment avenues waiting to be explored?

Can the Premier Guaranteed Star Pro Plan genuinely help you achieve your life goals, or is it just another traditional plan wrapped in attractive promises?

Does the Edelweiss Premier Guaranteed Star Pro Plan offer real value for your hard-earned savings, or does it fall short when compared with more flexible investment options?

This review breaks down how the plan works, along with its key features, benefits, and limitations.

Table of Contents

What is the Edelweiss Life Premier Guaranteed Star Pro?

What are the features of the Edelweiss Life Premier Guaranteed Star Pro?

Who is eligible for the Edelweiss Life Premier Guaranteed Star Pro?

What are the benefits of the Edelweiss Life Premier Guaranteed Star Pro?

Grace Period, Discontinuance and Revival of the Edelweiss Life Premier Guaranteed Star Pro

Free Look Period for the Edelweiss Life Premier Guaranteed Star Pro

Surrendering the Edelweiss Life Premier Guaranteed Star Pro

What are the advantages of the Edelweiss Life Premier Guaranteed Star Pro?

What are the disadvantages of the Edelweiss Life Premier Guaranteed Star Pro?

Research Methodology of Edelweiss Life Premier Guaranteed Star Pro

Benefit Illustration – IRR Analysis of Edelweiss Life Premier Guaranteed Star Pro

Edelweiss Life Premier Guaranteed Star Pro Vs. Other Investments

Edelweiss Life Premier Guaranteed Star Pro Vs. Pure-term + PPF/Equity Mutual Fund

Final Verdict on Edelweiss Life Premier Guaranteed Star Pro

What is the Edelweiss Life Premier Guaranteed Star Pro?

Edelweiss Life Premier Guaranteed Star Pro is an Individual, Non-Linked, Non-Participating, Savings, Life Insurance Plan.

It is a life insurance plan designed to provide protection to your family from any financial loss in case of an untimely death, and also provide a regular income and a lump sum to you and your family.

It has various options to help you customise the Edelweiss Life Premier Guaranteed Star Pro plan as per your requirements.

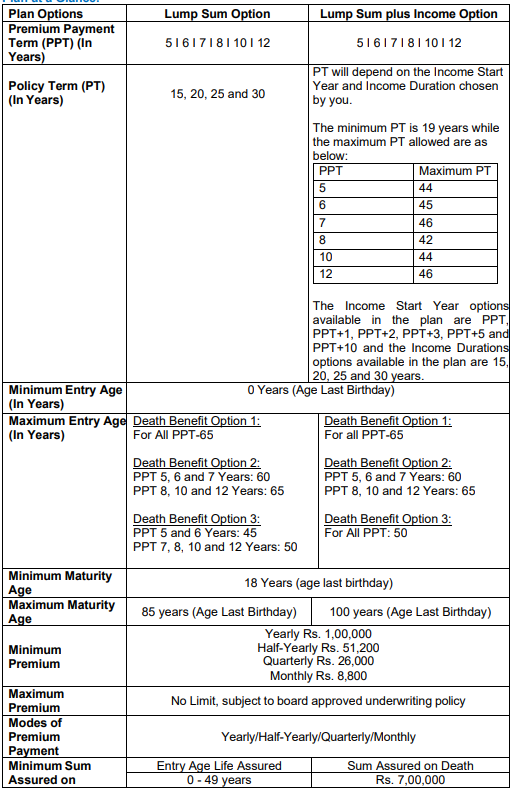

What are the features of the Edelweiss Life Premier Guaranteed Star Pro?

- Safeguard your family’s financial future with a comprehensive life insurance cover.

- Choose from two benefit structures—Lump Sum Option or Lump Sum plus Income Option—based on your needs.

- Achieve your long-term goals with a plan that provides guaranteed benefits.

- Enhance your protection by adding optional riders for an additional premium.

Who is eligible for the Edelweiss Life Premier Guaranteed Star Pro?

What are the benefits of the Edelweiss Life Premier Guaranteed Star Pro?

Death Benefit

The death benefit payable on the death of Life Insured, under the Lump Sum option and the Lump Sum plus Income Option, is the higher of:

- Sum Assured on Death as per the chosen Death Benefit Option

- 105% of Total Premiums Paid

- Surrender Value applicable at the time of death

In addition, for the Lump Sum plus Income Option, the ‘Income Benefit Pay-out’ due in the policy year of death will be paid on a pro-rata basis, considering the number of months elapsed in the policy year and duly adjusted for the survival benefits paid out in that policy year.

Death Benefit Option 1:

For age at entry less than 50 years: 7 times the Annualised Premium

For age at entry 50 years and above: 5 times the Annualised Premium

Death Benefit Option 2:

SAD is the Higher of 10 times the Annualised Premium and 10 times the Annual Premium

Death Benefit Option 3:

SAD is 20 times the Annualised Premium

Maturity Benefit

Lump Sum option

Maturity benefit is equal to Sum Assured on Maturity (SAM) plus accrued Guaranteed Additions (GA). The maturity benefit will be payable on maturity if the Life Assured survives till the end of the policy term, provided the policy is in force.

Sum Assured on Maturity = PPT X Annualised Premium

Guaranteed Additions = Guaranteed Additions Rate (GA Rate) X total Annualised Premium paid

Lump Sum Plus Income Option

In addition to the last Income Benefit Pay-out instalment, Maturity Benefit, which is equal to Sum Assured on Maturity (SAM), will be payable as a lump sum on the maturity of the policy if the Life Assured survives till the end of the Policy Term, provided the policy is in force.

SAM = Max (10, PPT) X Annualised Premium

Income Benefit

Lump Sum Option – Not Applicable

Lump Sum Plus Income Option

A level guaranteed income called ‘Income Benefit Pay-out’ starting from the chosen policy year called ‘Income Start Year’, will be payable in arrears as per the Income Benefit Payout Frequency chosen. The benefit will be payable till maturity or death, whichever is earlier, while the policy is in force.

‘Income Benefit Pay-out’ = Income Rate X Total Annualised Premium paid

Income Rate varies by Age, PPT, Income Duration, Income Start Year, Premium Band and Death Benefit Option

Grace Period, Discontinuance and Revival of the Edelweiss Life Premier Guaranteed Star Pro

Grace Period

The company will allow a Grace Period of 15 days, where the Policyholder pays the Premium on a monthly basis, and 30 days in all other cases, during which you must pay the Premium due in full.

Discontinuance

If all the premiums have not been paid in full for at least the first policy year, then on premium discontinuance, the policy will lapse, and no surrender value or paid-up value will be payable.

If all Premiums for at least the first Policy Year have not been paid in full, then the paid-up value is nil.

After completion of the first Policy Year, provided one full year’s Premium has been paid, then on Premium Discontinuance, the Policy will continue as a ‘Reduced Paid-up’ policy, and all the benefits shall be reduced proportionately.

Revival

The policy may be revived within the Revival Period. Revival Period means the period of five consecutive complete years from the date of the first unpaid premium.

Free Look Period for the Edelweiss Life Premier Guaranteed Star Pro

You have a Free Look period of thirty (30) days beginning from the date of receipt of the Policy Document, whether received electronically or otherwise, to review the terms and conditions of this Policy.

If you disagree with any of the terms or conditions, or otherwise, and you have not made any claims, you may return this Policy for cancellation.

Surrendering the Edelweiss Life Premier Guaranteed Star Pro

After completion of the first Policy Year, provided one full year’s Premium has been paid, your policy will acquire a Surrender Value. On receipt of a written request for Surrender from you, the Surrender Value, if any, will be payable after completion of the first Policy year.

The Surrender Value payable is the higher of Guaranteed Surrender Value (GSV) and Special Surrender Value (SSV).

What are the advantages of the Edelweiss Life Premier Guaranteed Star Pro?

- Strengthen your coverage with optional rider benefits.

- You can avail a loan of up to 60% of the policy’s surrender value.

- All policy benefits are fully guaranteed.

What are the disadvantages of the Edelweiss Life Premier Guaranteed Star Pro?

- Although the benefits are guaranteed, the overall returns are not competitive.

- The sum assured may fall short of providing adequate and comprehensive life coverage.

Research Methodology of Edelweiss Life Premier Guaranteed Star Pro

The Edelweiss Life Premier Guaranteed Star Pro Plan offers a guaranteed maturity benefit or survival benefit along with guaranteed additions. However, depending solely on these guarantees is not advisable.

It is important to evaluate the Edelweiss Life Premier Guaranteed Star Pro plan based on actual percentage returns. Let’s examine the Internal Rate of Return (IRR) using the figures provided in the policy brochure.

Benefit Illustration – IRR Analysis of Edelweiss Life Premier Guaranteed Star Pro

A 40-year-old male opts for this plan with a sum assured of ₹10 lakhs, a 20-year policy term, and a 12-year premium payment term, paying ₹1 lakh annually. He chooses the Lump Sum Option.

| Male | 40 years |

| Sum Assured | ₹ 10,00,000 |

| Policy Term | 20 years |

| Premium Paying Term | 12 years |

| Annualised Premium | ₹ 1,00,000 |

Under this structure, he pays premiums for 12 years and receives the maturity benefit plus the guaranteed additions at the end of 20 years. The total maturity value is ₹28.79 lakhs, resulting in an IRR of 6.07% as per the Edelweiss Life Premier Guaranteed Star Pro Plan maturity calculator.

This is below the inflation rate, making the return unattractive.

| Age | Year | Annualised premium / Maturity benefit | Death benefit |

| 40 | 1 | -1,00,000 | 10,00,000 |

| 41 | 2 | -1,00,000 | 10,00,000 |

| 42 | 3 | -1,00,000 | 10,00,000 |

| 43 | 4 | -1,00,000 | 10,00,000 |

| 44 | 5 | -1,00,000 | 10,00,000 |

| 45 | 6 | -1,00,000 | 10,00,000 |

| 46 | 7 | -1,00,000 | 10,00,000 |

| 47 | 8 | -1,00,000 | 10,00,000 |

| 48 | 9 | -1,00,000 | 10,00,000 |

| 49 | 10 | -1,00,000 | 10,00,000 |

| 50 | 11 | -1,00,000 | 10,00,000 |

| 51 | 12 | -1,00,000 | 10,00,000 |

| 52 | 13 | 0 | 10,00,000 |

| 53 | 14 | 0 | 10,00,000 |

| 54 | 15 | 0 | 10,00,000 |

| 55 | 16 | 0 | 10,00,000 |

| 56 | 17 | 0 | 10,00,000 |

| 57 | 18 | 0 | 10,00,000 |

| 58 | 19 | 0 | 10,00,000 |

| 59 | 20 | 0 | 10,00,000 |

| 60 | 28,79,514 | ||

| IRR | 6.07% |

Moreover, the investment stays locked until the end of the policy term—meaning an additional 8-year wait after completing premium payments. The ₹10 lakh sum assured is also insufficient to provide meaningful financial protection.

With limited liquidity, low life coverage, and subpar returns, the Edelweiss Life Premier Guaranteed Star Pro Plan does not serve well as either an insurance product or an investment solution.

Edelweiss Life Premier Guaranteed Star Pro Vs. Other Investments

Instead of choosing an endowment plan, a more effective approach is to buy a pure-term life insurance policy that offers substantial coverage at a much lower premium. Since term plans are non-profit products, they are far more affordable.

The remaining savings can then be invested across suitable asset classes aligned with your financial goals—helping you build a diversified and potentially higher-return portfolio. Let’s compare this strategy using the same parameters as the earlier example.

Edelweiss Life Premier Guaranteed Star Pro Vs. Pure-term + PPF/Equity Mutual Fund

A term insurance policy offering a ₹10 lakh sum assured costs ₹10,700 annually for a 20-year term with a 10-year premium payment period. This leaves ₹89,300 per year from the ₹1 lakh allocated earlier, which can now be invested based on risk preference.

| Pure Term Life Insurance Policy | |

| Sum Assured | ₹ 10,00,000 |

| Policy Term | 20 years |

| Premium Paying Term | 10 years |

| Annualised Premium | ₹ 10,700 |

| Investment | ₹ 89,300 |

High-risk investors may choose equity-based instruments.

Low-risk investors may prefer debt products.

For this comparison, we use PPF (debt) and an equity mutual fund (equity).

| Age | Year | Term Insurance premium + PPF | Death benefit | Term Insurance premium + Equity Mutual Fund | Death benefit |

| 40 | 1 | -1,00,000 | 10,00,000 | -1,00,000 | 10,00,000 |

| 41 | 2 | -1,00,000 | 10,00,000 | -1,00,000 | 10,00,000 |

| 42 | 3 | -1,00,000 | 10,00,000 | -1,00,000 | 10,00,000 |

| 43 | 4 | -1,00,000 | 10,00,000 | -1,00,000 | 10,00,000 |

| 44 | 5 | -1,00,000 | 10,00,000 | -1,00,000 | 10,00,000 |

| 45 | 6 | -1,00,000 | 10,00,000 | -1,00,000 | 10,00,000 |

| 46 | 7 | -1,00,000 | 10,00,000 | -1,00,000 | 10,00,000 |

| 47 | 8 | -1,00,000 | 10,00,000 | -1,00,000 | 10,00,000 |

| 48 | 9 | -1,00,000 | 10,00,000 | -1,00,000 | 10,00,000 |

| 49 | 10 | -1,00,000 | 10,00,000 | -1,00,000 | 10,00,000 |

| 50 | 11 | -1,00,000 | 10,00,000 | -1,00,000 | 10,00,000 |

| 51 | 12 | -98,500 | 10,00,000 | -1,00,000 | 10,00,000 |

| 52 | 13 | -500 | 10,00,000 | 0 | 10,00,000 |

| 53 | 14 | -500 | 10,00,000 | 0 | 10,00,000 |

| 54 | 15 | -500 | 10,00,000 | 0 | 10,00,000 |

| 55 | 16 | 0 | 10,00,000 | 0 | 10,00,000 |

| 56 | 17 | 0 | 10,00,000 | 0 | 10,00,000 |

| 57 | 18 | 0 | 10,00,000 | 0 | 10,00,000 |

| 58 | 19 | 0 | 10,00,000 | 0 | 10,00,000 |

| 59 | 20 | 0 | 10,00,000 | 0 | 10,00,000 |

| 60 | 30,19,840 | 54,36,494 | |||

| IRR | 6.40% | 10.53% |

PPF requires a minimum annual contribution of ₹500 for 15 years. Since the premium payment term is 10 years, adjustments are made to comply with PPF rules. The PPF maturity value works out to ₹30.19 lakhs, generating an IRR of 6.40%.

Investing the annual savings into an equity mutual fund, after accounting for capital gains tax at redemption, produces a post-tax maturity value of ₹54.36 lakhs (pre-tax value: ₹60.39 lakhs). The combined IRR from the term insurance plus equity mutual fund strategy is 10.53% (post-tax).

| Equity Mutual Fund Tax Calculation | |

| Maturity value after 20 years | 60,39,135 |

| Purchase price | 10,93,000 |

| Long-Term Capital Gains | 49,46,135 |

| Exemption limit | 1,25,000 |

| Taxable LTCG | 48,21,135 |

| Tax paid on LTCG | 6,02,642 |

| Maturity value after tax | 54,36,494 |

These returns comfortably beat inflation and provide far better liquidity.

This comparison clearly highlights the advantages of keeping insurance and investments separate—yielding higher returns, improved flexibility, and superior financial efficiency, benefits that the Edelweiss Life Premier Guaranteed Star Pro Plan does not deliver.

Final Verdict on Edelweiss Life Premier Guaranteed Star Pro

The Edelweiss Life Premier Guaranteed Star Pro provides life coverage along with guaranteed benefits—either as a lump sum or as periodic payouts followed by a final lump sum.

While these benefits are assured from the outset, the Edelweiss Life Premier Guaranteed Star Pro plan lacks investment flexibility and locks in your funds until maturity. Moreover, the life cover offered is insufficient and it also has a high agent commission.

The return analysis further shows that the Edelweiss Life Premier Guaranteed Star Pro plan delivers suboptimal long-term returns.

Overall, its combination of poor returns, restricted liquidity, and inadequate life coverage makes it unsuitable as both an insurance product and an investment avenue. In short, the Edelweiss Life Premier Guaranteed Star Pro does not add meaningful value to your portfolio.

A more effective strategy is to separate insurance and investment. A pure-term insurance policy offers robust financial protection at a low cost, while your investments can be diversified and aligned with your risk profile, time horizon, and life goals.

Creating a solid financial plan is crucial for long-term stability.

Do Quora, Facebook, and Twitter have the final say when it comes to financial advice?

For personalised guidance, consider consulting a certified financial planner who can help structure your insurance and investments in line with your goals.

Leave a Reply