A self-employed chartered accountant with a ₹70 lakh home loan parks ₹8 lakh in her OD account after a strong tax-filing season.

Her tenure should have shrunk from 20 years to roughly 15.

Instead, it keeps sliding back toward 18 — a festival expense here, an office upgrade there, and every time the market dips or a “can’t miss” investment idea lands in her inbox, a chunk of that balance quietly walks out the door. (Illustrative, composite scenario.)

By the time she notices, she hasn’t lost money in the way she’d fear from a bad trade. She’s lost something quieter: years of interest savings that will never come back.

That’s the part almost nobody explains properly.

Table of Contents:

The reveal

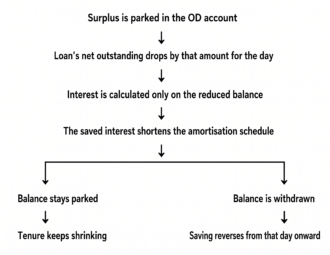

A home loan overdraft — SBI MaxGain, Bank of Baroda’s Home Loan Advantage, and similar products from most major lenders — isn’t a clever savings account bolted onto your loan.

It’s a discipline test wearing a savings account’s clothing. The mechanism is real and the math genuinely works.

But the product is sold on its interest rate and flexibility, when the thing that actually decides whether you win or lose is something no brochure measures: how often you touch the money.

The proof

Run the numbers on three borrowers with the identical ₹70 lakh loan, to see how much of the outcome is actually decided by behaviour rather than by the bank:

| Borrower A

(No OD) |

Borrower B

(OD) Balance Stays Parked |

Borrower C

(OD) Frequent Withdrawals |

|

|---|---|---|---|

| Interest rate | 8.60% | 8.95% |

8.95% |

|

EMI |

₹61,191 | ₹62,761 | ₹62,761 |

| Average balance parked | – | ₹8 lakh |

₹2 lakh |

|

Tenure |

20 years | ~15 years | ~18.5 years |

| Total repayment | ₹1.47 crore | ₹1.13 crore |

₹1.39 crore |

|

Saving vs Borrower A |

– | ~₹33.9 lakh |

~₹7.5 lakh |

(Illustrative example, EMI-calculator based.)

Borrower C is the trap most borrowers fall into. She opens the OD account, pays the higher 8.95% rate for the entire tenure, but lets withdrawals erode the balance until only ₹2 lakh, on average, is actually doing any work.

The result: she pays the OD premium the whole way through and ends up saving barely a fifth of what Borrower B saves. Borrower B and Borrower C hold the exact same product, at the exact same rate.

The only thing that separates a ₹33.9 lakh outcome from a ₹7.5 lakh outcome is what each of them did with the balance.

Even after accounting for what Borrower B’s ₹8 lakh could have earned instead in a fixed deposit (roughly ₹8.6 lakh post-tax over the same period) and the slightly higher EMI outgo, her net advantage still lands around ₹21 lakh.

That’s not a rounding-error benefit. That’s real money, and it’s why the mechanism deserves attention.

Before you count the ₹21 lakh

Two caveats are worth flagging before that number sticks in your head.

First, Borrower B’s outcome assumes a constant ₹8 lakh balance, a stable interest rate, and zero withdrawals over 15 years.

Real earnings, real festival and family expenses, and real rate cycles rarely stay that cooperative — which is exactly why Borrower C exists in the table above. Treat ₹21 lakh as a ceiling, not a guarantee.

Second, the comparison above uses a fixed deposit as the opportunity-cost benchmark, and that understates the real trade-off for many borrowers.

Someone with a 10-plus year horizon and an emergency fund already in place could potentially earn meaningfully more from a diversified, long-term investment than from an FD.

The true comparison isn’t “OD versus FD” — it’s “interest saved versus your realistic long-term investment return, after tax.”

There’s also a quieter tax angle. Interest saved through an OD account isn’t taxed at all, while FD interest is fully taxable at your slab rate. For someone in a higher tax bracket, that alone can make the OD’s real, in-hand advantage larger than the FD comparison suggests.

It’s also worth noting where interest rates sit right now: the RBI has held the repo rate steady at 5.25% since December 2025, with the next policy review due in early August.

Home loan rates across major banks are, for the moment, relatively stable — which means the OD premium you’re quoted today is unlikely to move sharply in either direction in the near term.

That stability is exactly when the discipline question matters most, because there’s no rate volatility to blame if the plan doesn’t work.

The mechanism

Here’s how it actually works. In a regular home loan, interest is charged on your full outstanding principal, and every rupee you prepay is gone for good.

In an OD loan, your surplus sits in a linked account, and interest is calculated only on the net outstanding — loan minus whatever’s parked.

Think of it as a scale that resets daily: the day money sits in the account, it weighs less on your loan. The day you withdraw it, the weight comes right back.

Nothing exotic about it — it’s simple interest math applied daily instead of monthly. The only variable in the entire chain that a borrower actually controls is the top line: whether the money stays parked.

The catch is the premium. OD loans typically carry a slightly higher rate than a regular home loan — commonly a 0.05% to 0.40% markup depending on the lender, based on current 2026 published rates from major banks. That premium is the price of the flexibility to withdraw.

One thing most borrowers get wrong: they assume the benefit only counts if the balance stays parked forever.

It doesn’t. Interest is computed daily, so even a ₹4 lakh surplus parked for six months against a ₹62 lakh outstanding loan generates real, immediate savings — smaller than a full-tenure commitment, but real.

You don’t need permanence to benefit. You just need the balance to sit there for however long it actually sits there.

The empathy beat

None of this happens because someone was careless. It happens because the product is marketed almost entirely on its interest-saving mechanics — the calculator, the tenure reduction, the flexibility — and almost never on the one variable that determines whether any of that math survives contact with real life. Every rupee sitting in that OD account is one tap away on a banking app.

A bonus, a market dip, a “once-in-a-lifetime” opportunity from a relative — the withdrawal always feels justified in the moment.

Sometimes it isn’t even for spending at all — it’s for an investment opportunity that feels too good to pass up, which is its own kind of trap, because that withdrawal is competing against a guaranteed, tax-free return on the loan itself.

The interest cost of that withdrawal is invisible; it shows up as a slower-shrinking tenure months later, not as a number anyone sees today.

The reframe

Used well, an OD account isn’t a place to keep money you might spend — it’s a place to keep money you’ve already decided not to spend, but don’t want locked away permanently.

Borrowers like Borrower B, who actually capture that ₹21 lakh advantage, tend to treat the OD balance the same way they’d treat a prepayment: gone from their mental spending list, available only for genuine emergencies, not for opportunities.

This is where it helps to separate two things people tend to lump together: your emergency corpus and your long-term investment corpus.

An OD account is genuinely one of the better homes for the emergency piece — the money keeps working (reducing interest) while staying fully liquid the moment you need it.

It’s a poor home for the long-term piece, because money that’s meant to grow for 10-15 years toward a goal is better off compounding elsewhere than sitting still, tax-free saving or not.

And the OD account isn’t automatically the right home for surplus either.

Someone with a ₹50 lakh outstanding loan who suddenly receives a ₹40 lakh windfall may generate higher long-term returns putting that money to work elsewhere than by parking it against the loan. The question is never “does OD save interest” — it always does, on paper.

The question is what the surplus is for, and whether the person holding it will leave it alone long enough for the math to play out.

A useful rule of thumb: if the money is likely to be needed within the next few years, an OD account may be a sensible home for it. If it’s earmarked for a goal 10-15 years away, it may deserve a different destination altogether.

Which raises the real question worth sitting with: if you opened an OD account tomorrow, would the balance still be there in year three — or would it have quietly become an ATM?

That single question usually says more about which loan structure is right for you than any interest rate comparison ever could.

Leave a Reply