Is the Pramerica Life Wealth Maximiser Plan truly the growth booster your portfolio needs, or could it leave your wealth underperforming?

Could the Pramerica Life Wealth Maximiser Plan be your gateway to long-term financial security, or are there smarter ways to invest?

Can the Pramerica Life Wealth Maximiser Plan really maximise your wealth, or is it just another routine investment option?

Let’s explore its key features, benefits, and drawbacks to find out.

Table of Contents

What is the Pramerica Life Wealth Maximiser?

What are the features of the Pramerica Life Wealth Maximiser?

Who is eligible for the Pramerica Life Wealth Maximiser?

What are the benefits of the Pramerica Life Wealth Maximiser?

What are the investment strategies and fun options in the Pramerica Life Wealth Maximiser?

What are the charges of the Pramerica Life Wealth Maximiser?

Grace Period, Discontinuance and Revival of the Pramerica Life Wealth Maximiser

Free Look Period of the Pramerica Life Wealth Maximiser

Surrendering the Pramerica Life Wealth Maximiser

What are the advantages of the Pramerica Life Wealth Maximiser?

What are the disadvantages of the Pramerica Life Wealth Maximiser?

Research Methodology of Pramerica Life Wealth Maximiser

Benefit Illustration – IRR Analysis of Pramerica Wealth Maximiser

Pramerica Life Wealth Maximiser Vs. Other Investments

Pramerica Life Wealth Maximiser Vs. Pure-term + PPF/Equity Mutual Fund

Final Verdict on Pramerica Life Wealth Maximiser

What is the Pramerica Life Wealth Maximiser?

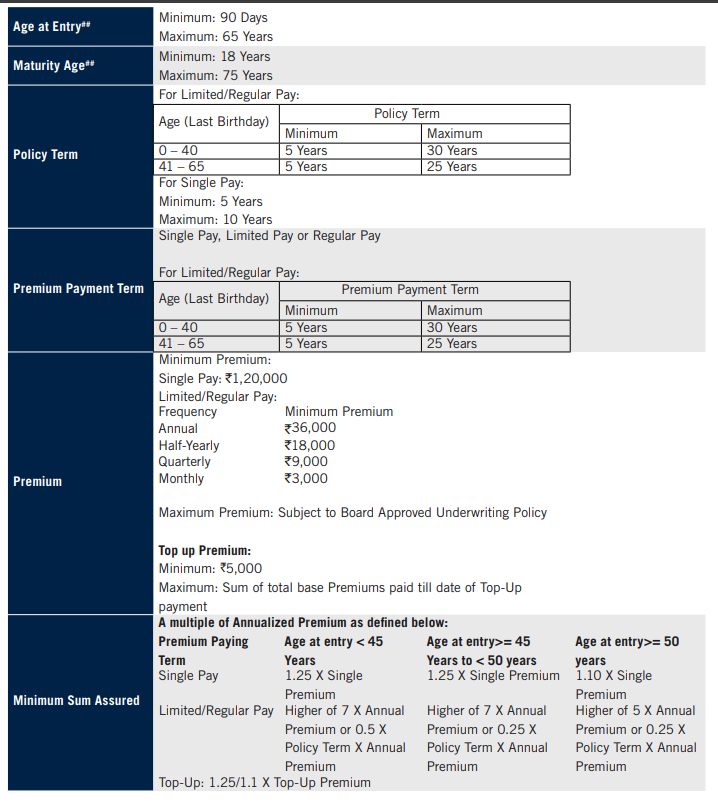

Pramerica Life Wealth Maximiser is a Unit Linked Non-Participating Individual Savings Life Insurance Plan. This plan offers multiple options of sum assured based on your age at entry to let you enjoy the benefit of choosing an adequate life cover as per your protection needs.

What are the features of the Pramerica Life Wealth Maximiser?

- Choose an adequate life cover that matches your protection needs, with multiple sum assured options available based on your entry age.

- Enjoy flexibility in premium payments by selecting Single, Regular, or Limited Premium Payment terms.

- Benefit from reduced charges when you opt for higher premium amounts.

- Get rewarded for long-term commitment through Persistency Units and Wealth Boosters at specific intervals to enhance your fund value.

- Actively manage your investments with the Defined Portfolio Strategy, allowing you to adjust based on market conditions.

- Life Stage Portfolio Strategy helps to maintain a balanced allocation between Equity and Debt as per your age and changing risk profile.

Who is eligible for the Pramerica Life Wealth Maximiser?

What are the benefits of the Pramerica Life Wealth Maximiser?

i). Death benefit

In case of an unfortunate demise of the Life Insured during the Pramerica Life Wealth Maximiser Plan Policy Term, the Policy will pay the Death Benefit, which is the higher of

- Sum Assured, including Top-Up Sum Assured, if any, or

- Fund Value, including Top-Up Fund Value, if any, or

- 105% of total Premiums paid to date of death, including Top-Up premiums, if any

ii). Maturity Benefit

On survival of the Life Insured till maturity date and subject to the Pramerica Life Wealth Maximiser Plan Policy being in force for full risk benefits, the Policy will pay the Fund Value, including Top-Up fund value, if any, to the Policyholder.

iii). Persistency Units

As a reward for continuing your policy, Persistency units equal to 0.50% of the average of Fund Value, including Top-Up Fund Value of preceding 36 monthiversaries would be allocated to the Policyholder’s unit account at the end of every policy year, starting from the sixth policy year.

iv). Wealth Boosters

Wealth Boosters would be allocated as extra units at the end of every fifth policy year, starting from the end of the tenth policy year.

Wealth Booster as a percentage of average fund value, including Top-up Fund Value of preceding 36-month monthiversaries would be allocated to the Pramerica Life Wealth Maximiser Plan policyholder’s unit account at the end of 10th, 15th, 20th, 25th and 30th policy anniversaries, if they fall within the policy term.

| Policy Anniversary | Band 1 | Band 2 | Band 3 |

| 10th | 1.00% | 1.25% | 1.50% |

| 15th | 1.25% | 1.75% | 2.00% |

| 20th | 1.50% | 2.25% | 2.50% |

| 25th | 1.75% | 2.75% | 3.00% |

| 30th | 2.00% | 3.25% | 3.50% |

What are the investment strategies and fun options in the Pramerica Life Wealth Maximiser?

At inception, the Pramerica Life Wealth Maximiser Plan Policyholder can choose one of the following investment strategies:

- Defined Portfolio Strategy

- Life Stage Portfolio Strategy

Once opted in, the investment strategy will continue throughout the policy term. You cannot switch from one investment strategy to another during the Pramerica Life Wealth Maximiser Plan policy term.

Defined Portfolio Strategy

Under this option, you can choose to invest in any of the funds available (except the discontinuance fund or Liquid Fund) in proportion to your choice.

Within the Defined Portfolio strategy, you also have the option to select the Systematic Transfer Plan (STP) option, for which the Liquid Fund will be made available to you. You can switch money among these funds using the switch option.

You can choose from ten funds to invest your money. If you opt for more than one fund, the minimum investment in any fund should be at least 10% of the Annual Premium. The funds and fund objectives are as follows:

| S.no | Fund Name | Asset Allocation | Risk Profile | ||

| Equity & Equity-related instruments | Govt. Securities & Corp. Bonds | Money market instruments | |||

| 1 | Debt fund | 0% | 50-100% | 0-40% | Low |

| 2 | Balance Fund | 10-50% | 0-50% | 0-40% | High |

| 3 | Growth Fund | 40-80% | 0-30% | 0-40% | High |

| 4 | Large-cap Equity fund | 60-100% | 0% | 0-40% | High |

| 5 | Multi-cap opportunities | 50-100% | 0-30% | 0-50% | High |

| 6 | Balanced Equilibrium Fund | 65-75% | 25-35% | 25-35% | Medium |

| 7 | Growth Momentum fund | 75-85% | 15-25% | 15-25% | High |

| 8 | Large-cap advantage fund | 85-100% | 0-15% | 0-15% | High |

| 9 | Flexi Cap Opportunities Fund | 85-100% | 0-15% | 0-15% | High |

| 10 | Pramerica Nifty Mid Cap 50 Correlation Fund | 90-100% | 0-10% | 0-10% | High |

| Liquid fund | 0% | 0% | 100% | Low | |

| Discontinued policy fund | 0% | 60-100% | 0-40% | Low | |

Systematic Transfer Plan (STP)

With STP, you can invest a specific amount at monthly intervals, which gives you the advantage of Rupee Cost Averaging.

You can buy more units when markets are down and fewer units when markets are up, thereby reducing the average unit purchase cost. You can choose STP only for 12 months; an option would be available to policies wherein the premium is to be paid annually.

Life Stage Portfolio Strategy

The plan offers a life-stage-based investment strategy wherein the investments are distributed between the Large Cap Equity Fund and the Debt Fund, with their proportions varying as per the different life stages.

At inception, the funds will be distributed between two funds, the Multi Cap Opportunities Fund & Debt Fund. As and when the next milestone is achieved, the funds will be redistributed according to the attained age (age bands) as given in the following table:

| Age as on the last birthday and the last policy anniversary | Debt fund | Large cap Equity Fund |

| Up to 25 | 15% | 85% |

| 26 – 30 | 20% | 80% |

| 31 – 35 | 25% | 75% |

| 36 – 40 | 30% | 70% |

| 41 – 45 | 35% | 65% |

| 46 – 50 | 40% | 60% |

| 51 – 55 | 45% | 55% |

| 56 and above | 50% | 50% |

What are the charges of the Pramerica Life Wealth Maximiser?

A). Premium Allocation charge

| Policy Year/Premium Band | Band 1 | Band 2 | Band 3 |

| 1 | 5.0% | 2.0% | 2.0% |

| 2 to 5 | 2.5% | 2.0% | 2.0% |

| 6+ | 2.5% | 0.0% | 0.0% |

B). Policy Administration Charge

| Policy Year/Premium Band | Band 1 | Band 2 | Band 3 |

| 1 to 5 | 0.21% | 0.10% | 0.00% |

| 6+ | 0.25% | 0.10% | 0.00% |

C). Mortality charge

Monthly mortality charges for Top-up Sum Assured cover would be calculated as Top-up Sum Assured less Top-up Fund Value x mortality charge rate for the given age/gender. Annual charges per 1000 sum at risk for a healthy male are as follows:

| Attained Age of Life Insured | 25 | 30 | 35 | 40 |

| D). Mortality charge | 0.989 | 1.07 | 1.32 | 1.881 |

E). Fund Management Charges (FMC)

| S.no | Fund Name | Fund Management Charges (FMC) |

| 1 | Debt fund | 1.20% |

| 2 | Balance Fund | 1.20% |

| 3 | Growth Fund | 1.35% |

| 4 | Large-cap Equity fund | 1.35% |

| 5 | Multi-cap opportunities | 1.35% |

| 6 | Balanced Equilibrium Fund | 1.35% |

| 7 | Growth Momentum fund | 1.35% |

| 8 | Large-cap advantage fund | 1.35% |

| 9 | Flexi Cap Opportunities Fund | 1.35% |

| 10 | Pramerica Nifty Mid Cap 50 Correlation Fund | 1.25% |

| Discontinued policy fund | 0.50% |

E). Discontinuance Charge

Discontinuance charge will be based on the year of discontinuance and the premium amount. There is no discontinuance charge from the 5th policy year.

F). Switching charge

There are no switching charges or restrictions on the number of switches during the entire policy term

Inference from the charges: ULIPs involve several additional expenses, such as policy administration charges, premium allocation charges, and other related costs.

These charges make ULIPs more expensive compared to most other market-linked investment products. Over time, they can significantly reduce your effective returns, thereby limiting your potential for wealth accumulation.

Grace Period, Discontinuance and Revival of the Pramerica Life Wealth Maximiser

For other than Single Premium policies

a). Garce Period

A grace period of 30 days in case of non-monthly mode policies and a 15-day grace period in case of monthly mode policies from the due date to pay the Premium is given.

b). Discontinuance

Discontinued during the first five Policy years: the fund value after deducting the applicable discontinuance charges shall be credited to the Discontinued Policy Fund, and the risk cover and rider cover, if any, shall cease.

The proceeds of the discontinued policy fund shall be paid to the Pramerica Life Wealth Maximiser Plan policyholder at the end of the revival period or lock-in period, whichever is later.

Discontinued after the first five Policy years: the policy shall be converted into a reduced paid-up policy with the paid-up sum assured, i.e. original sum assured multiplied by a ratio of “total period for which premiums have already been paid” to the “maximum period for which premiums were originally payable”.

At the end of the revival period, the proceeds of the Pramerica Life Wealth Maximiser Plan policy fund shall be paid to the policyholder.

c). Revival

You have an option to revive your discontinued policy within three years from the date of first unpaid premium.

Free Look Period of the Pramerica Life Wealth Maximiser

You will have a period of 30 days from the date of receipt of the Pramerica Life Wealth Maximiser Plan Policy document to review the terms and conditions of the Policy, and if you disagree with any of these terms and conditions, you have the option to return the Policy.

Surrendering the Pramerica Life Wealth Maximiser

For Single Premium Policies

During the Lock-in Period: The Pramerica Life Wealth Maximiser Plan policyholder has an option to surrender at any time during the lock-in period.

Upon receipt of a request for surrender, the fund value, after deducting the applicable discontinuance charges, shall be credited to the Discontinued Policy Fund.

The Pramerica Life Wealth Maximiser Plan policy shall continue to be invested in the Discontinued Policy Fund, and the proceeds from the discontinuance fund shall be paid at the end of the lock-in period.

After the lock-in period: The policyholder has the option to surrender the policy anytime. Upon receipt of a request for surrender, the fund value as on the date of surrender shall be payable.

For other than Single Premium policies

Surrender during the first five Policy years: the policyholder has an option to surrender the policy anytime, and proceeds of the discontinued policy shall be payable at the end of the lock-in period or date of surrender, whichever is later.

Surrender after the first five Policy years: the Pramerica Life Wealth Maximiser Plan policyholder has an option to surrender the policy anytime, and the proceeds of the policy fund shall be payable.

What are the advantages of the Pramerica Life Wealth Maximiser?

- Use the Systematic Transfer Plan (STP) to gradually move your funds from the Liquid Fund to your chosen investment funds every month.

- Boost your investment and life cover by adding a Top-up Premium.

- Within the Defined Portfolio Strategy, you can switch investments and redirect premiums among the available fund options.

- Partial withdrawals are allowed only after completing 5 policy years (the mandatory lock-in period).

- Benefit from the Fund Conservation Option to protect your fund value from market volatility.

- At policy maturity, you can choose to receive your maturity benefits as structured payouts over a period of up to 5 years through the Settlement Option.

- You can increase or decrease the sum assured (within the permitted limits) after the third policy anniversary.

- Enjoy flexibility to extend or shorten both the Premium Payment Term and the Pramerica Life Wealth Maximiser Plan Policy Term as per your financial goals.

What are the disadvantages of the Pramerica Life Wealth Maximiser?

- No loan facility is available under this plan.

- Liquidity is restricted during the first five policy years.

- Premiums are invested only after deducting applicable charges.

- The sum assured may be insufficient to provide adequate financial protection for the family.

- The returns are not commensurate with the level of risk involved.

Research Methodology of Pramerica Life Wealth Maximiser

After evaluating the Pramerica Life Wealth Maximiser Plan, it becomes crucial to assess its performance and potential returns to understand how it compares with other investment avenues.

Let’s analyse the Internal Rate of Return (IRR) based on the data provided in the Pramerica Life Wealth Maximiser Plan policy brochure.

Benefit Illustration – IRR Analysis of Pramerica Wealth Maximiser

A 30-year-old male purchases the plan with a sum assured of ₹10 lakhs, a policy term of 20 years, and a premium payment term of 10 years, paying an annual premium of ₹1 lakh.

| Male | 30 years |

| Sum Assured | ₹ 10,00,000 |

| Policy Term | 20 years |

| Premium Paying Term | 10 years |

| Annualised Premium | ₹ 1,00,000 |

The maturity benefit will be the fund value, including the persistency units and wealth additions. The brochure provides illustrations at 4% p.a. and 8% p.a. return scenarios — these are only indicative and not guaranteed.

| At 4% p.a. | At 8% p.a. | ||||

| Age | Year | Annualised premium / Maturity benefit | Death benefit | Annualised premium / Maturity benefit | Death benefit |

| 35 | 1 | -1,00,000 | 10,00,000 | -1,00,000 | 10,00,000 |

| 36 | 2 | -1,00,000 | 10,00,000 | -1,00,000 | 10,00,000 |

| 37 | 3 | -1,00,000 | 10,00,000 | -1,00,000 | 10,00,000 |

| 38 | 4 | -1,00,000 | 10,00,000 | -1,00,000 | 10,00,000 |

| 39 | 5 | -1,00,000 | 10,00,000 | -1,00,000 | 10,00,000 |

| 40 | 6 | -1,00,000 | 10,00,000 | -1,00,000 | 10,00,000 |

| 41 | 7 | -1,00,000 | 10,00,000 | -1,00,000 | 10,00,000 |

| 42 | 8 | -1,00,000 | 10,00,000 | -1,00,000 | 10,00,000 |

| 43 | 9 | -1,00,000 | 10,00,000 | -1,00,000 | 10,00,000 |

| 44 | 10 | -1,00,000 | 10,00,000 | -1,00,000 | 10,00,000 |

| 45 | 11 | 0 | 10,00,000 | 0 | 10,00,000 |

| 46 | 12 | 0 | 10,00,000 | 0 | 10,00,000 |

| 47 | 13 | 0 | 10,00,000 | 0 | 10,00,000 |

| 48 | 14 | 0 | 10,00,000 | 0 | 10,00,000 |

| 49 | 15 | 0 | 10,00,000 | 0 | 10,00,000 |

| 50 | 16 | 0 | 10,00,000 | 0 | 10,00,000 |

| 51 | 17 | 0 | 10,00,000 | 0 | 10,00,000 |

| 52 | 18 | 0 | 10,00,000 | 0 | 10,00,000 |

| 53 | 19 | 0 | 10,00,000 | 0 | 10,00,000 |

| 54 | 20 | 0 | 10,00,000 | 0 | 10,00,000 |

| 55 | 14,33,263 | 26,20,263 | |||

| IRR | 2.33% | 6.31% | |||

At 4% return: Fund value is ₹14.33 lakhs, with an IRR of 2.33% as per the Pramerica Life Wealth Maximiser Plan maturity calculator,, offering negligible real value addition.

At 8% return: Fund value is ₹26.20 lakhs, with an IRR of 6.31% as per the Pramerica Life Wealth Maximiser Plan maturity calculator.

Even under optimistic conditions, the returns from the Pramerica Life Wealth Maximiser Plan remain unimpressive compared to other market-linked investment options.

Despite carrying market risk, its performance aligns more closely with low-risk debt instruments, making the risk-return balance unfavourable.

In conclusion, investing in the Pramerica Life Wealth Maximiser plan could hinder your financial progress rather than enhance it, as the returns do not justify the level of risk involved.

Pramerica Life Wealth Maximiser Vs. Other Investments

The Pramerica Life Wealth Maximiser Plan does not effectively support long-term wealth creation and offers a relatively low sum assured.

For better financial security and meaningful wealth accumulation, it’s more beneficial to separate insurance and investment. Let’s compare the outcomes of this approach using the same example.

Pramerica Life Wealth Maximiser Vs. Pure-term + PPF/Equity Mutual Fund

A pure-term life insurance policy with a sum assured of ₹10 lakhs costs only ₹7,500 annually for a 20-year term.

In comparison, the Pramerica Life Wealth Maximiser Plan requires an annual premium of ₹1 lakh. Choosing the term plan saves ₹92,500 per year, which can instead be invested to grow wealth.

| Pure Term Life Insurance Policy | |

| Sum Assured | ₹ 10,00,000 |

| Policy Term | 20 years |

| Premium Paying Term | 10 years |

| Annualised Premium | ₹ 7,500 |

| Investment | ₹ 92,500 |

Depending on one’s risk appetite, the investment portion can be directed towards suitable options —

Low-risk investors can choose debt instruments such as PPF (Public Provident Fund).

High-risk investors may prefer equity instruments like Equity Mutual Funds.

| Term Insurance + PPF | Term insurance + Equity Mutual Fund | ||||

| Age | Year | Term Insurance premium + PPF | Death benefit | Term Insurance premium + Equity Mutual Fund | Death benefit |

| 35 | 1 | -1,00,000 | 10,00,000 | -1,00,000 | 10,00,000 |

| 36 | 2 | -1,00,000 | 10,00,000 | -1,00,000 | 10,00,000 |

| 37 | 3 | -1,00,000 | 10,00,000 | -1,00,000 | 10,00,000 |

| 38 | 4 | -1,00,000 | 10,00,000 | -1,00,000 | 10,00,000 |

| 39 | 5 | -1,00,000 | 10,00,000 | -1,00,000 | 10,00,000 |

| 40 | 6 | -1,00,000 | 10,00,000 | -1,00,000 | 10,00,000 |

| 41 | 7 | -1,00,000 | 10,00,000 | -1,00,000 | 10,00,000 |

| 42 | 8 | -1,00,000 | 10,00,000 | -1,00,000 | 10,00,000 |

| 43 | 9 | -1,00,000 | 10,00,000 | -1,00,000 | 10,00,000 |

| 44 | 10 | -97,500 | 10,00,000 | -1,00,000 | 10,00,000 |

| 45 | 11 | -500 | 10,00,000 | 0 | 10,00,000 |

| 46 | 12 | -500 | 10,00,000 | 0 | 10,00,000 |

| 47 | 13 | -500 | 10,00,000 | 0 | 10,00,000 |

| 48 | 14 | -500 | 10,00,000 | 0 | 10,00,000 |

| 49 | 15 | -500 | 10,00,000 | 0 | 10,00,000 |

| 50 | 16 | 0 | 10,00,000 | 0 | 10,00,000 |

| 51 | 17 | 0 | 10,00,000 | 0 | 10,00,000 |

| 52 | 18 | 0 | 10,00,000 | 0 | 10,00,000 |

| 53 | 19 | 0 | 10,00,000 | 0 | 10,00,000 |

| 54 | 20 | 0 | 10,00,000 | 0 | 10,00,000 |

| 55 | 27,29,733 | 50,72,011 | |||

| IRR | 6.58% | 10.74% | |||

PPF Investment

Over 20 years, the maturity value comes to ₹27.29 lakhs, delivering an IRR of 6.58%. This is comparable to the 8% return scenario of the Pramerica Life Wealth Maximiser Plan, even though PPF is a low-risk debt option.

Equity Mutual Fund Investment

Investing the annual surplus of ₹92,500 in an equity mutual fund grows to a pre-tax value of ₹56.46 lakhs. After accounting for capital gains tax, the post-tax maturity value stands at ₹50.72 lakhs, with a post-tax IRR of 10.74%.

| Equity Mutual Fund Tax Calculation | |

| Maturity value after 20 years | 56,46,584 |

| Purchase price | 9,25,000 |

| Long-Term Capital Gains | 47,21,584 |

| Exemption limit | 1,25,000 |

| Taxable LTCG | 45,96,584 |

| Tax paid on LTCG | 5,74,573 |

| Maturity value after tax | 50,72,011 |

This combined strategy of term insurance plus independent investment generates a larger corpus, offers better inflation-adjusted returns, and provides adequate life cover.

In contrast, the Pramerica Life Wealth Maximiser Plan delivers low risk-adjusted returns and inadequate coverage, making it a less effective option for achieving long-term financial goals.

Final Verdict on Pramerica Life Wealth Maximiser

The Pramerica Life Wealth Maximiser Plan offers a market-linked investment option combined with life insurance coverage. The maturity benefit comprises the fund value, along with persistency units and wealth boosters.

As an investor, you might expect this plan to generate inflation-beating returns. However, an analysis of its performance shows otherwise — high charges significantly erode returns, preventing the plan from achieving meaningful long-term growth and it also has a high agent commission.

The plan fails to build a sufficient corpus to meet important life goals, and the insurance coverage provided is inadequate to serve as a reliable financial safety net. Effective financial planning demands both comprehensive protection and strong wealth creation, areas where this plan falls short.

Overall, the Pramerica Life Wealth Maximiser Plan is not a worthwhile choice considering the risks involved. There are better risk-adjusted investment products available in the market that can deliver superior results.

A smarter approach would be to build a diversified investment portfolio for wealth creation and to opt for a pure-term life insurance policy for family protection.

Do Quora, Facebook, and Twitter have the final say when it comes to financial advice?

Before committing to any financial product, evaluate its suitability carefully. For personalised advice, consider consulting a Certified Financial Planner (CFP) who can design a resilient, goal-based investment strategy aligned with your risk tolerance, time horizon, and financial objectives.

Leave a Reply