Is the Bharti AXA Life InstaGain Plan truly a smart way to gain returns quickly — or just a short-term savings gimmick with limited long-term benefit?

Is Bharti AXA InstaGain Plan a good choice for both short-term and long-term financial planning — or is it too focused on early benefits at the cost of later growth?

Does the Bharti AXA InstaGain Plan reward disciplined investors — or mainly appeal to those who prioritize quick returns over strategic growth?

This article critically examines the features of the Bharti AXA Life InstaGain Plan, highlighting its key benefits and limitations.

Table of Contents:

What is the Bharti AXA Life InstaGain Plan?

What are the features of the Bharti AXA Life InstaGain Plan?

Who is eligible for the Bharti AXA Life InstaGain Plan?

What are the benefits of the Bharti AXA Life InstaGain Plan?

Grace Period, Discontinuance and Revival of the Bharti AXA Life InstaGain Plan

Free Look period for the Bharti AXA Life InstaGain Plan

Surrendering the Bharti AXA Life InstaGain Plan

What are the advantages of the Bharti AXA Life InstaGain Plan?

What are the disadvantages of the Bharti AXA Life InstaGain Plan?

Research Methodology of Bharti AXA Life InstaGain Plan

Benefit Illustration – IRR Analysis of Bharati AXA Life InstaGain Plan

Bharati AXA Life InstaGain Plan Vs. Other Investments

Bharati AXA Life InstaGain Plan Vs. Pure-term + Equity Mutual Fund

Final Verdict on Bharati AXA Life InstaGain Plan

What is the Bharti AXA Life InstaGain Plan?

Bharti AXA Life InstaGain Plan is a non-linked, non-participating, individual life insurance, savings plan.

It provides you with a life cover, along with guaranteed income and a Guaranteed lumpsum benefit to meet your immediate as well as future needs. With this plan, you can enjoy instant returns with ‘InstaGain Income’.

What are the features of the Bharti AXA Life InstaGain Plan?

- Life Cover: Provides life insurance protection to financially secure your family throughout the Bharti AXA Life InstaGain Plan policy term.

- Guaranteed Returns: Offers assured benefits in the form of Guaranteed Early Income, Guaranteed Income, and Loyalty Income to help you meet your financial goals.

- InstaGain Income: Provides an upfront payout of up to 50% of the annual premium at the time of policy issuance.

- Lump Sum Benefit Option: Allows you to receive 100% or 150% of the total premiums paid (based on the chosen variant) as a lump sum to enhance overall returns.

- Flexibility: Enables you to customise premium payment terms, income duration, and death benefit multiple according to your needs and preferences.

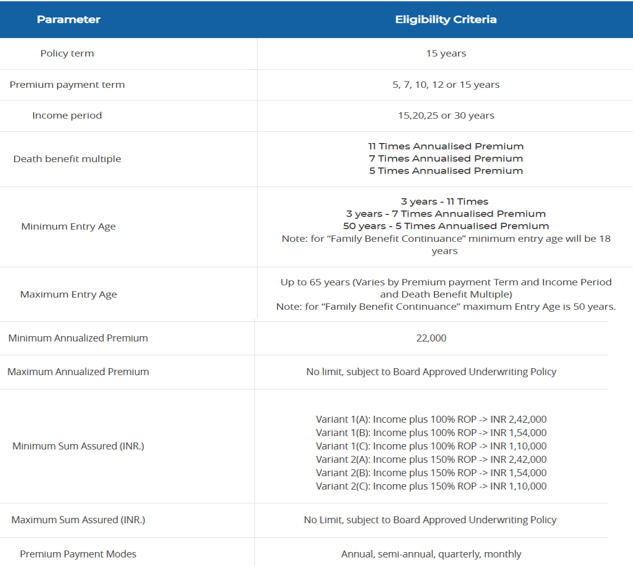

Who is eligible for the Bharti AXA Life InstaGain Plan?

What are the benefits of the Bharti AXA Life InstaGain Plan?

1. Death benefit

Death Benefit (in case Family Benefit Continuance option is not selected):

In case of the death of the Life Insured during the Bharti AXA Life InstaGain Plan Policy Term, provided the Policy is in force, the Death Benefit will be payable to the Nominee immediately on death.

On payment of the death benefit to the nominee, the policy will terminate, and no further benefits will be payable.

Death Benefit (in case Family Benefit Continuance option is selected):

In case of the death of the Life Insured during the Policy Term, provided the Bharti AXA Life InstaGain Plan Policy is in force, the Death Benefit will be payable immediately on death, and all future premiums due shall be waived off.

The policy shall continue, and applicable future Survival Benefits and Maturity Benefit shall be paid to the Claimant as and when due.

Under this Option, upon the death of the Life Insured, the Claimant shall have no right to discontinue the Policy, and once the claim is triggered, the Nominee cannot change the Income Frequency.

This option can only be chosen if the Policyholder and Life Insured are the same person and, once opted for, cannot be opted out of during the Bharti AXA Life InstaGain Plan Policy Term.

Death Benefit is the higher of

- Sum Assured on Death

- 105% of Total Premiums Paid

- Surrender Value applicable as on the date of death

2. Survival benefit

InstaGain Income:

InstaGain Income is equal to InstaGain Income Factor multiplied by the Annualised Premium multiplied by InstaGain Income Modal Factor.

InstaGain Income shall be payable in advance only in the first policy year. The Bharti AXA Life InstaGain Plan policyholder shall have an option to receive the “InstaGain income” on an Annual/Semi-annual/Quarterly/Monthly frequency.

Guaranteed Early Income:

Payable on survival of the Life insured (or death of Life Insured, in case of Family Benefit Continuance option) during the policy term, provided all premiums due till date are paid (or waived off, in case of Family Benefit Continuance option).

Each instalment is calculated as the Guaranteed Early Income Factor multiplied by the Annualised Premium multiplied by the Income modal factor.

It is payable in arrears during the Bharti AXA Life InstaGain Plan Policy Term from the second policy year till the last year of the Policy term (15th year). The Income Modal factor will depend on the Income Frequency chosen at inception.

3. Maturity benefit

Upon survival of the Life Insured till the end of the Policy Term (or death of Life Insured, in case of Family Benefit Continuance option) and provided the Policy is in force, all due premiums have been paid (or waived off, in case of Family Benefit Continuance option); the maturity benefit shall be payable in the following instalments: –

Guaranteed Income(s) and Loyalty Income(s) are payable in arrears every year. The income shall be payable as per the Income Frequency chosen at inception for the policy and shall not change during the Bharti AXA Life InstaGain Plan policy term.

Guaranteed Income will be payable from the end of the Policy Term till the last year of the Income period.

Guaranteed Income is defined as Guaranteed Income Factor X Annualised Premium X Income Modal Factor

Loyalty Income is the Sum of all Accrued Loyalty Additions. Loyalty Addition is defined as Loyalty Addition Factor X Total Premiums Paid (excluding modal loadings).

This accrues to the policy at the end of each policy year, starting from the second policy year till the last year of the policy term, provided the Bharti AXA Life InstaGain Plan policy is in force and at least two full years’ premiums are paid.

Guaranteed lump sum benefit is a lump sum equal to the following (based on the plan variant chosen), along with the last Income Instalment, and the same will vary depending on the variant chosen.

- Variant 1: 100% of ROP

- Variant 2: 150% of ROP

Grace Period, Discontinuance and Revival of the Bharti AXA Life InstaGain Plan

Grace Period

The grace period is 15 days for the monthly mode and 30 days for annual/ semi-annual/ quarterly premium payment modes.

Discontinuance

The policy acquires a surrender value after completion of the first policy year, provided one full year’s premium has been received.

If the Policy has not acquired Surrender Value: If the policyholder does not pay the due premiums within the Grace Period, the policy shall lapse with effect from the date of such unpaid premium (‘lapse date’).

You can revive the policy within the period allowed for revival of the policy. At the end of the revival period, if the policy is not revived, then the Bharti AXA Life InstaGain Plan policy will be terminated, and no benefits will be payable.

If the Policy has acquired Surrender Value: After completion of the first policy year, provided one full year’s premium has been received, and further premiums have not been paid for any reason, the Policy will automatically be converted into Paid up, on expiry of the Grace period, and all the guaranteed benefits under the Policy will be reduced.

Revival

You have the flexibility to revive your lapsed/ paid-up policy within the revival period of five years after the due date of the first unpaid premium.

Free Look period for the Bharti AXA Life InstaGain Plan

If the Policyholder disagrees with any of the terms and conditions of the Policy, there is an option to return the original Policy along with a letter stating the reason/s within 30 days of receipt of the Policy Document.

Surrendering the Bharti AXA Life InstaGain Plan

The policy acquires a surrender value after completion of the first policy year, provided one full year’s premium has been received. On surrender post the Policy acquires surrender value, you will receive the higher of:

Guaranteed Surrender Value (GSV)

Special Surrender Value (SSV)

What are the advantages of the Bharti AXA Life InstaGain Plan?

- Loan Facility: You can avail a loan of up to 70% of the policy’s surrender value, subject to applicable terms and conditions.

- Family Benefit Continuance Option: In the event of the life assured’s death, all survival and maturity benefits will continue to be paid to the nominee as scheduled, while future premiums are fully waived.

- Commuted Maturity Value: Provides the option to receive the present value of all future benefits at any time during the income period.

- Flexi-Wallet Feature: An in-built wallet that allows you to accumulate guaranteed early income during the policy term.

- Rider Options: Enhanced protection can be added through optional riders by paying an additional premium.

- Tax Benefits: Eligible for tax benefits as per the prevailing income tax laws.

What are the disadvantages of the Bharti AXA Life InstaGain Plan?

- Fixed Policy Term: The policy term is locked at 15 years, limiting flexibility to align the plan with changing financial goals.

- Low Sum Assured: The sum assured is relatively low, resulting in limited life insurance protection.

- Survival Benefits Risk: Periodic survival benefits may lead to discretionary spending rather than disciplined long-term investing.

- No Life Cover During Income Period: Life insurance coverage does not continue throughout the income payout phase, reducing protection when it may still be required.

- Impact on Compounding: Early income payouts dilute the power of compounding, potentially lowering overall returns.

Research Methodology of Bharti AXA Life InstaGain Plan

The Bharti AXA Life InstaGain Plan offers regular guaranteed payouts along with a maturity benefit. While such periodic income may appear attractive, it is essential to assess the plan’s actual return potential.

To evaluate this, we calculate the Internal Rate of Return (IRR) based on the benefit illustration provided in the policy brochure.

Benefit Illustration – IRR Analysis of Bharati AXA Life InstaGain Plan

Consider a 35-year-old male opting for the Bharti AXA Life InstaGain Plan with a sum assured of ₹11 lakh. The policy term is fixed at 15 years, with a premium payment term of 10 years and an annual premium of ₹1,00,000.

The income payout period extends for 30 years. The Bharti AXA Life InstaGain Plan policyholder selects Variant 1, which offers 100% return of premium (ROP) as a maturity benefit.

|

Male |

35 years |

|

Sum Assured |

₹ 11,00,000 |

|

Policy Term |

15 years |

|

Premium Paying Term |

10 years |

|

Annualised Premium |

₹ 1,00,000 |

Benefit structure:

InstaGain Income: A one-time payout of ₹50,000, payable in advance in the first policy year.

Guaranteed Early Income: ₹38,950 per year, payable in arrears from the 2nd policy year until the end of the policy term (15th year).

Guaranteed Income and Loyalty Income: Annual payouts of ₹29,214 and ₹9,736, respectively, payable in arrears from the end of the policy term until the conclusion of the income period.

Maturity Benefit: A guaranteed lump sum of ₹10 lakh (100% ROP under Variant 1), payable along with the final income instalment.

Based on these cash flows, the plan delivers an IRR of approximately 5.05% as per the Bharti AXA Life InstaGain Plan maturity calculator.

|

Age |

Year |

Annualised premium / Maturity benefit |

Death benefit |

|

35 |

1 |

-50,000 |

11,00,000 |

|

36 |

2 |

-1,00,000 |

11,00,000 |

|

37 |

3 |

-61,050 |

11,00,000 |

|

38 |

4 |

-61,050 |

11,00,000 |

|

39 |

5 |

-61,050 |

11,00,000 |

|

40 |

6 |

-61,050 |

11,00,000 |

|

41 |

7 |

-61,050 |

11,00,000 |

|

42 |

8 |

-61,050 |

11,00,000 |

|

43 |

9 |

-61,050 |

11,00,000 |

|

44 |

10 |

-61,050 |

11,00,000 |

|

45 |

11 |

38,950 |

11,00,000 |

|

46 |

12 |

38,950 |

11,00,000 |

|

47 |

13 |

38,950 |

11,00,000 |

|

48 |

14 |

38,950 |

11,00,000 |

|

49 |

15 |

38,950 |

11,00,000 |

|

50 |

16 |

38,950 |

|

|

51 |

17 |

38,950 |

|

|

52 |

18 |

38,950 |

|

|

53 |

19 |

38,950 |

|

|

54 |

20 |

38,950 |

|

|

55 |

21 |

38,950 |

|

|

56 |

22 |

38,950 |

|

|

57 |

23 |

38,950 |

|

|

58 |

24 |

38,950 |

|

|

59 |

25 |

38,950 |

|

|

60 |

26 |

38,950 |

|

|

61 |

27 |

38,950 |

|

|

62 |

28 |

38,950 |

|

|

63 |

29 |

38,950 |

|

|

64 |

30 |

38,950 |

|

|

65 |

31 |

38,950 |

|

|

66 |

32 |

38,950 |

|

|

67 |

33 |

38,950 |

|

|

68 |

34 |

38,950 |

|

|

69 |

35 |

38,950 |

|

|

70 |

36 |

38,950 |

|

|

71 |

37 |

38,950 |

|

|

72 |

38 |

38,950 |

|

|

73 |

39 |

38,950 |

|

|

74 |

40 |

38,950 |

|

|

75 |

41 |

38,950 |

|

|

76 |

42 |

38,950 |

|

|

77 |

43 |

38,950 |

|

|

78 |

44 |

38,950 |

|

|

79 |

45 |

38,950 |

|

|

80 |

10,38,950 |

||

|

IRR |

5.05% |

Despite its guaranteed nature, the Bharti AXA Life InstaGain Plan suffers from several significant limitations. The returns are extremely low, making the plan unsuitable for long-term wealth creation.

The extended lock-in period effectively ties up the investor’s capital until the end of the income period, which spans 30 years.

Moreover, the sum assured is relatively modest and does not continue during the income period, leaving the family with inadequate financial protection in the event of unforeseen circumstances.

Overall, the Bharti AXA Life InstaGain Plan falls short on both investment efficiency and insurance adequacy. With limited flexibility, insufficient life cover, and subpar returns, it does not align well with long-term financial planning objectives.

Bharati AXA Life InstaGain Plan Vs. Other Investments

The Bharti AXA Life InstaGain Plan delivers modest investment returns and inadequate life cover primarily because it combines insurance and investment into a single product.

Rather than locking funds into such a structure, allocating the same premium more strategically can lead to significantly better outcomes.

Bharati AXA Life InstaGain Plan Vs. Pure-term + Equity Mutual Fund

A pure-term life insurance policy with a sum assured of ₹11 lakh costs approximately ₹6,200 per year for a 15-year term, with premiums payable for 10 years.

This results in an annual surplus of ₹93,800 available for investment over the same 10-year period.

|

Pure Term Life Insurance Policy |

|

|

Sum Assured |

₹ 11,00,000 |

|

Policy Term |

15 years |

|

Premium Paying Term |

10 years |

|

Annualised Premium |

₹ 6,200 |

|

Investment |

₹ 93,800 |

This surplus is invested in an equity mutual fund, with systematic withdrawals structured to replicate the survival benefits offered by the Bharti AXA Life InstaGain Plan.

At the end of the 10-year investment phase, the remaining units are redeemed and reinvested in a fixed-income instrument yielding 7% per annum.

Capital gains tax is considered only at the final redemption, after factoring in the annual long-term capital gains exemption of ₹1.25 lakh.

|

Term insurance + Equity Mutual Fund |

|||

|

Age |

Year |

Term Insurance premium + Equity Mutual Fund |

Death benefit |

|

35 |

1 |

-50,000 |

11,00,000 |

|

36 |

2 |

-1,00,000 |

11,00,000 |

|

37 |

3 |

-61,050 |

11,00,000 |

|

38 |

4 |

-61,050 |

11,00,000 |

|

39 |

5 |

-61,050 |

11,00,000 |

|

40 |

6 |

-61,050 |

11,00,000 |

|

41 |

7 |

-61,050 |

11,00,000 |

|

42 |

8 |

-61,050 |

11,00,000 |

|

43 |

9 |

-61,050 |

11,00,000 |

|

44 |

10 |

-61,050 |

11,00,000 |

|

45 |

11 |

38,950 |

11,00,000 |

|

46 |

12 |

38,950 |

11,00,000 |

|

47 |

13 |

38,950 |

11,00,000 |

|

48 |

14 |

38,950 |

11,00,000 |

|

49 |

15 |

38,950 |

11,00,000 |

|

50 |

16 |

38,950 |

|

|

51 |

17 |

38,950 |

|

|

52 |

18 |

38,950 |

|

|

53 |

19 |

38,950 |

|

|

54 |

20 |

38,950 |

|

|

55 |

21 |

38,950 |

|

|

56 |

22 |

38,950 |

|

|

57 |

23 |

38,950 |

|

|

58 |

24 |

38,950 |

|

|

59 |

25 |

38,950 |

|

|

60 |

26 |

38,950 |

|

|

61 |

27 |

38,950 |

|

|

62 |

28 |

38,950 |

|

|

63 |

29 |

38,950 |

|

|

64 |

30 |

38,950 |

|

|

65 |

31 |

38,950 |

|

|

66 |

32 |

38,950 |

|

|

67 |

33 |

38,950 |

|

|

68 |

34 |

38,950 |

|

|

69 |

35 |

38,950 |

|

|

70 |

36 |

38,950 |

|

|

71 |

37 |

38,950 |

|

|

72 |

38 |

38,950 |

|

|

73 |

39 |

38,950 |

|

|

74 |

40 |

38,950 |

|

|

75 |

41 |

38,950 |

|

|

76 |

42 |

38,950 |

|

|

77 |

43 |

38,950 |

|

|

78 |

44 |

38,950 |

|

|

79 |

45 |

38,950 |

|

|

80 |

64,17,040 |

||

|

IRR |

7.66% |

||

|

Equity Mutual Fund Tax Calculation |

|

|

Maturity value after 10 years |

11,51,746 |

|

Purchase price |

9,38,000 |

|

Long-Term Capital Gains |

2,13,746 |

|

Exemption limit |

1,25,000 |

|

Taxable LTCG |

88,746 |

|

Tax paid on LTCG |

11,093 |

|

Maturity value after tax |

11,40,652 |

This approach provides regular withdrawals similar to the InstaGain Plan while maintaining greater control over the investment corpus.

The strategy delivers an estimated IRR of 7.66% and a maturity value of approximately ₹64 lakh, which is nearly six times the return of premium offered by the Bharti AXA Life InstaGain Plan.

In addition to superior returns, this structure offers meaningful flexibility—allowing withdrawals to be aligned with actual financial needs—unlike the fixed and rigid payout schedule of the insurance plan.

In conclusion, the Bharti AXA Life InstaGain Plan underperforms due to low returns, limited flexibility, and insufficient life cover. A combination of pure-term insurance and mutual fund investment emerges as a far more effective and efficient strategy for achieving long-term financial goals.

Final Verdict on Bharati AXA Life InstaGain Plan

The Bharti AXA Life InstaGain Plan combines survival benefits, instalment-based maturity payouts, and life insurance coverage. The survival benefits begin from the first policy year and include guaranteed income along with Loyalty Income.

Additionally, the plan promises a return of premium at the end of the income period. This combination of features may appear appealing at first glance.

However, in substance, the plan resembles a traditional money-back policy—offering below-average returns and a relatively low sum assured.

The investment component is ineffective in creating long-term wealth, making it unsuitable for achieving meaningful financial goals and it also has a high agent commission.

Further, the life cover is limited and does not extend through the income period, resulting in inadequate financial protection when it may still be required. Overall, the plan does not merit a place in a well-constructed portfolio.

A pure-term life insurance policy, in contrast, provides substantially higher coverage at a much lower cost, ensuring meaningful financial security for your family.

When combined with a thoughtfully diversified investment portfolio aligned to your goals, time horizon, and risk tolerance, it offers a far more efficient path to wealth creation.

In summary, avoid blending savings with insurance. Selecting the right standalone financial products is fundamental to effective financial planning.

Do Quora, Facebook, and Twitter have the final say when it comes to financial advice?

For a structured, goal-based approach, consulting a Certified Financial Planner can help design strategies that are better aligned with your long-term needs.

Leave a Reply