Are you seeking a financial product that promises both security and growth potential?

Does the IndiaFirst Life Radiance Smart Invest Plan sound like the perfect solution?

But before diving in, have you considered the inherent risk-reward balance of Unit Linked Insurance Plans (ULIPs) and whether this specific plan aligns with your financial goals?

In this article, we’ll explore the features and benefits of the India First Life Radiance Smart Invest Plan and analyze the advantages and disadvantages along with the internal rate of return calculations. This information will assist you in making an informed decision.

Let’s get started.

Table of Contents:

What is the India First Life Radiance Smart Invest Plan?

What are the Features of India First Life Radiance Smart Invest Plan?

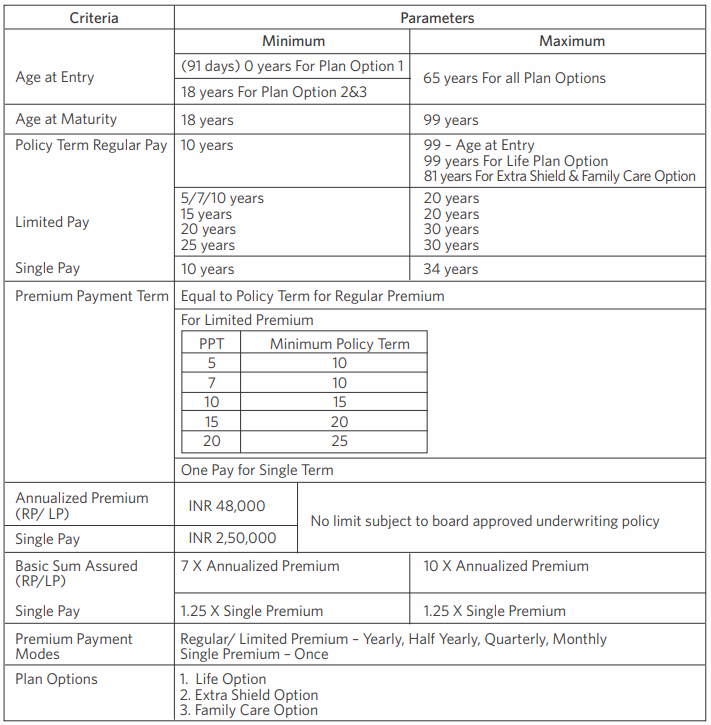

Who is Eligible for the India First Life Radiance Smart Invest Plan?

What are the Benefits of the India First Life Radiance Smart Invest Plan?

Investment Strategies & Fund Options of India First Life Radiance Smart Invest Plan

Grace period, Discontinuance & Revival of India First Life Radiance Smart Invest Plan

Free Look period of India First Life Radiance Smart Invest Plan

Surrendering India First Life Radiance Smart Invest Plan

What are the Advantages of India First Life Radiance Smart Invest Plan?

What are the Disadvantages of India First Life Radiance Smart Invest Plan?

Research Methodology of India First Life Radiance Smart Invest Plan Review

Benefit Illustration – IRR analysis of India First Life Radiance Smart Invest Plan

India First Life Radiance Smart Invest Plan Vs Other Investment Product

India First Policy Radiance Smart Invest Plan Vs. Pure Term +PPF / ELSS

Final Verdict on India First Life Radiance Smart Invest Plan

What is the India First Life Radiance Smart Invest Plan?

India First Life Radiance Smart Invest Plan is a Unit-linked, non-participating individual Life insurance endowment plan.

India First Life Radiance Smart Invest Plan provides complete financial security for your family by providing you with life insurance coverage. With this India First Life Radiance Smart Invest Plan plan, you can create a lasting legacy and a safety net for your loved ones

What are the Features of India First Life Radiance Smart Invest Plan?

- Provide a safety net for you and your loved ones through the life insurance cover.

- Tailor the India First Life Radiance Smart Invest Plan policy to suit your insurance needs through flexible term and premium paying options

- Choose from three different plan options based on your life insurance coverage need – Life Option, Extra Shield Option, Family Care Option

- Get the flexibility to choose from 10 fund options & investment strategies as per your requirement

- Grow your money while you participate in market-linked fund options

Three variants of India First Life Radiance Smart Invest Plan:

- Life Option: Provide a safety net of life insurance cover against Death through Life Option.

- Extra Shield Option: Provide cushion of additional insurance cover against Death and Accidental Death through Extra Shield Option

- Family Care Option: Maintain continuity of your India First Life Radiance Smart Invest Plan policy benefits through a waiver of premiums in the Family Care Option

Who is Eligible for the India First Life Radiance Smart Invest Plan?

What are the Benefits of the India First Life Radiance Smart Invest Plan?

i.) Death benefit

The Nominee(s)/Legal Heir will receive the death benefit under the India First Life Radiance Smart Invest Plan policy equal to the higher fund value as on the date of death or sum assured.

ii.) Maturity benefit

The policyholder will receive –

- Fund Value, at the end of the India First Life Radiance Smart Invest Plan policy term, plus,

- Total mortality charges deducted throughout the India First Life Radiance Smart Invest Plan policy term, plus,

- An amount equal to Y% of Annualized Premium (based on India First Life Radiance Smart Invest Plan policy term & premium paying term)

Investment Strategies & Fund Options of India First Life Radiance Smart Invest Plan

You can choose and opt for any one of the below strategies to ensure that you are getting the optimum returns out of your premiums.

A. Automatic Trigger Based Investment Strategy (ATBIS) of India First Life Radiance Smart Invest Plan

This investment strategy will secure your returns regularly and provide you with a balanced portfolio over the years.

In case you opt for ATBIS the funds will be allotted in chosen Equity Option. You can select any one Equity Fund from the available Equity Fund Options (Equity 1 fund, Value Fund, Index Tracker Fund, Equity Elite Opportunities Fund, Flexi Cap Equity Fund & Sustainable Equity Fund) and automatically transfer the earnings on your funds in chosen equity Fund to Debt 1 Fund based on a predefined trigger rate of 10%.

B. Fund Transfer Strategy of India First Life Radiance Smart Invest Plan

Your premium after deduction of applicable charges will be allocated to the chosen debt-oriented fund, along with existing units in that fund, if any. The units in the chosen debt-oriented fund are then transferred systematically on a monthly basis to the chosen equity-oriented fund.

You have to choose two fund options, one from a debt-type fund i.e. either Debt 1 or Balanced 1 and another one from equity type fund i.e. any one of Equity1/Value/Index Tracker/Equity Elite Opportunities Fund, Flexi Cap Equity Fund & Sustainable Equity Fund.

C. Age-Based Investment Strategy of India First Life Radiance Smart Invest Plan

Your premium after deduction of applicable charges will be distributed between Equity1 Fund, Debt1 Fund, and Value Fund based on your age. As you grow older and move from one band to another, your funds are redistributed.

This strategy will balance your portfolio and adjust the risk exposure as you grow older. The age-wise fund distribution is shown in the below table.

| Age (years) | Equity 1 | Debt 1 | Value |

| 5 to 25 | 40% | 30% | 30% |

| 26 to 35 | 35% | 40% | 25% |

| 36 to 45 | 30% | 50% | 20% |

| 46 to 55 | 25% | 60% | 15% |

| 56 to 65 | 20% | 70% | 10% |

| 66 to 70 | 15% | 80% | 5% |

| 71 to 90 | 5% | 90% | 5% |

D. Smart Switch Strategy of India First Life Radiance Smart Invest Plan

This investment strategy is designed to systematically move your savings into low-risk fund options near maturity to safeguard your returns. In this strategy, you may choose to save in any or all of the 10 available fund options. When you choose this strategy, we move your funds systematically to Liquid 1 Fund in the last 5 policy years to ensure your hard-earned money is secure from any sudden market dips. The movement to the Liquid 1 Fund will happen in the manner specified as per below table –

| Start of policy year | Fund allocation in chosen funds | Liquid 1 Fund Allocation |

| T-4 | 80% | 20% |

| T-3 | 70% | 30% |

| T-2 | 40% | 60% |

| T-1 | 10% | 90% |

| T | 0% | 100% |

E. Defined Allocation Strategy of India First Life Radiance Smart Invest Plan

You can choose any 4 fund options from the 10 fund options available. You would also specify the allocation for each of these selected funds. The funds will be re-distributed on a half-yearly basis to ensure that your funds remain in the same allocation as specified by you, at the beginning of the IndiaFirst Life Radiance Smart Invest Plan policy.

F. Self-Managed Strategy of India First Life Radiance Smart Invest Plan

By choosing this strategy option you get access to all the 10 segregated funds. You can choose to put your premiums in one, multiple, or all of these options based on your risk appetite and needs.

| Asset Allocation | ||||

| Fund Name | Equity | Debt | Money Market | Risk Profile |

| Equity 1 | 80% to 100% | 0% | 0% to 20% | High |

| Balanced 1 | 50% to 70% | 30% to 50% | 0% to 20% | Moderate to High |

| Debt 1 | 0% | 70% to 100% | 0% to 30% | Moderate |

| Value | 70% to 100% | 0% | 0% to 30% | Very High |

| Index Tracker | 90% to 100% | 0% | 0% to 10% | High |

| Dynamic Asset Allocation | 0% to 80% | 0% to 80% | 0% to 40% | High |

| Equity Elite opportunities | 60% to 100% | 0% | 0% to 40% | High |

| Liquid 1 | 0% | 0% to 20% | 80% to 100% | Low |

| Flexi cap Equity | 65% to 100% | 0% | 0% to 35% | Medium to High |

| Sustainable Equity | 80% to 100% | 0% | 0% to 20% | Medium to High |

Grace period, Discontinuance & Revival of India First Life Radiance Smart Invest Plan

Grace Period

A grace period of 30 days for payment of all premiums under quarterly, half-yearly yearly, and yearly modes and 15 days under monthly mode is available in IndiaFirst Life Radiance Smart Invest Plan.

Discontinuance

Discontinuance of the IndiaFirst Life Radiance Smart Invest Plan Policy during the lock-in period:

For other than single premium policies, upon expiry of the grace period, in case of discontinuance of a IndiaFirst Life Radiance Smart Invest Plan policy due to non-payment of premium, the fund value after deducting the applicable discontinuance charges, shall be credited to the discontinued policy fund and the risk cover and rider cover, if any, shall cease.

The proceeds of the discontinued policy fund shall be paid to the policyholder at the end of the revival period or lock-in period whichever is later.

For other than Single Premium Policies:

Upon expiry of the grace period, in case of discontinuance of a policy due to non-payment of premium after the lock-in period, the IndiaFirst Life Radiance Smart Invest Plan policy shall be converted into a reduced paid-up policy with the paid-up sum assured i.e. original sum assured multiplied by the total number of premiums paid to the original number of premiums payable.

Revival

The IndiaFirst Life Radiance Smart Invest Plan policy can be revived within the revival period of three years.

Free Look period of India First Life Radiance Smart Invest Plan

In case you do not agree to any policy terms and conditions, you have the option of returning the IndiaFirst Life Radiance Smart Invest Plan policy within 15 days from the date of receipt of the policy.

The free-look period for policies purchased through distance marketing or electronic mode will be 30 days.

Surrendering India First Life Radiance Smart Invest Plan

Surrender of the IndiaFirst Life Radiance Smart Invest Plan Policy during the lock-in period:

The policyholder has the option to surrender the policy anytime and proceeds of the discontinued policy shall be payable at the end of the lock-in period or date of surrender whichever is later.

Surrender of the Policy after the lock-in period:

The policyholder has the option to surrender the IndiaFirst Life Radiance Smart Invest Plan policy anytime and proceeds of the policy fund shall be payable immediately.

In the case of Single Premium Policies, the policyholder has the option to surrender the IndiaFirst Life Radiance Smart Invest Plan policy at any time. Upon receipt of the request for surrender, the fund value as of the date of surrender shall be payable.

What are the Advantages of India First Life Radiance Smart Invest Plan?

- You can switch from one fund to another fund, any number of times during the IndiaFirst Life Radiance Smart Invest Plan policy term.

- In case of any financial emergencies, you can make partial withdrawals from the accumulated funds.

- Systematic Partial Withdrawal is allowed, after the completion of the first 5 policy years provided the life assured is 18 years and above.

- Total mortality charges deducted throughout the IndiaFirst Life Radiance Smart Invest Plan policy term will be payable at the end of the policy term.

What are the Disadvantages of India First Life Radiance Smart Invest Plan?

- There is no liquidity in the first five policy years.

- There is no loan facility.

- No loyalty addition or Fund boosters in the plan.

Research Methodology of India First Life Radiance Smart Invest Plan Review

It’s time to do some calculations. Directing your savings effectively should yield long-term benefits. Therefore, it’s crucial to calculate the potential return before investing in the IndiaFirst Life Radiance Smart Invest Plan.

Let’s determine the Internal Rate of Return (IRR) for the Bajaj Allianz Radiance Smart Invest Plan by obtaining a quote from the portal.

Benefit Illustration – IRR analysis of India First Life Radiance Smart Invest Plan

A 35-year-old male buys India first Life Radiance Smart Invest Plan for a sum assured of ₹ 15 Lakhs. He pays a premium of ₹ 1.5 Lakhs for 20 years. The policy term is 20 years.

| Male | years |

| Sum Assured | ₹ 15,00,000 |

| Policy Term | 20 years |

| Premium Paying Term | 20 years |

| Annualised Premium | ₹ 1,50,000 |

At the end of the policy term, he receives the maturity benefit. The returns indicated at 4% and 8% are illustrative and not guaranteed and do not indicate the upper or lower limits of returns under the IndiaFirst Life Radiance Smart Invest Plan Policy.

| At 4% p.a. | At 8% p.a. | ||||

| Age | Year | Annualised premium / Maturity benefit | Death benefit | Annualised premium / Maturity benefit | Death benefit |

| 35 | 1 | -1,50,000 | 15,00,000 | -1,50,000 | 15,00,000 |

| 36 | 2 | -1,50,000 | 15,00,000 | -1,50,000 | 15,00,000 |

| 37 | 3 | -1,50,000 | 15,00,000 | -1,50,000 | 15,00,000 |

| 38 | 4 | -1,50,000 | 15,00,000 | -1,50,000 | 15,00,000 |

| 39 | 5 | -1,50,000 | 15,00,000 | -1,50,000 | 15,00,000 |

| 40 | 6 | -1,50,000 | 15,00,000 | -1,50,000 | 15,00,000 |

| 41 | 7 | -1,50,000 | 15,00,000 | -1,50,000 | 15,00,000 |

| 42 | 8 | -1,50,000 | 15,00,000 | -1,50,000 | 15,00,000 |

| 43 | 9 | -1,50,000 | 15,00,000 | -1,50,000 | 15,00,000 |

| 44 | 10 | -1,50,000 | 15,00,000 | -1,50,000 | 15,00,000 |

| 45 | 11 | -1,50,000 | 15,00,000 | -1,50,000 | 15,00,000 |

| 46 | 12 | -1,50,000 | 15,00,000 | -1,50,000 | 15,00,000 |

| 47 | 13 | -1,50,000 | 15,00,000 | -1,50,000 | 15,00,000 |

| 48 | 14 | -1,50,000 | 15,00,000 | -1,50,000 | 15,00,000 |

| 49 | 15 | -1,50,000 | 15,00,000 | -1,50,000 | 15,00,000 |

| 50 | 16 | -1,50,000 | 15,00,000 | -1,50,000 | 15,00,000 |

| 51 | 17 | -1,50,000 | 15,00,000 | -1,50,000 | 15,00,000 |

| 52 | 18 | -1,50,000 | 15,00,000 | -1,50,000 | 15,00,000 |

| 53 | 19 | -1,50,000 | 15,00,000 | -1,50,000 | 15,00,000 |

| 54 | 20 | -1,50,000 | 15,00,000 | -1,50,000 | 15,00,000 |

| 55 | 38,44,447 | 15,00,000 | 60,17,181 | 15,00,000 | |

| IRR | 2.31% | 6.24% | |||

Based on the India First Life Radiance Smart Invest Plan Maturity Calculator, in the 4% scenario, the fund value is ₹ 38.44 lakhs with an IRR of 2.31%.

Based on the India First Life Radiance Smart Invest Plan Maturity Calculator, in the 8% scenario, the fund value is ₹ 60.17 lakhs with an IRR of 6.24%.

In both cases, the IRR is too low for a market-related investment. Therefore, investing in the India First Radiance Smart Invest Plan may not be effective for wealth accumulation.

India First Life Radiance Smart Invest Plan Vs Other Investment Product

Now, let’s compare the returns with other investment options. Using the figures from the previous illustration, we’ll consider a life cover with a sum assured of ₹15 lakhs and explore investment opportunities for wealth accumulation separately.

Rather than combining insurance and investment, we’ll separate the two aspects and evaluate the returns individually.

India First Policy Radiance Smart Invest Plan Vs. Pure Term +PPF / ELSS

A pure term life insurance policy with a sum assured of ₹ 15 lakhs would cost ₹7,900 per annum over a 20-year premium paying term. The policy term is also 20 years.

After the paying premium, you would have a remaining balance of ₹1,42,100 each year available for investment. You can allocate this amount according to your personal risk appetite.

| Pure Term Life Insurance Policy | |

| Sum Assured | ₹ 15,00,000 |

| Policy Term | 20 years |

| Premium Paying Term | 20 years |

| Annualised Premium | ₹ 7,900 |

| Investment | ₹ 1,42,100 |

Here we have chosen a PPF account for debt instruments & ELSS fund for Equity instruments. After the premium payment for a pure term life insurance policy, the balance is invested for wealth accumulation.

| Term Insurance + PPF | Term insurance + ELSS | ||||

| Age | Year | Term Insurance premium + PPF | Death benefit | Term Insurance premium + ELSS | Death benefit |

| 35 | 1 | -1,50,000 | 15,00,000 | -1,50,000 | 15,00,000 |

| 36 | 2 | -1,50,000 | 15,00,000 | -1,50,000 | 15,00,000 |

| 37 | 3 | -1,50,000 | 15,00,000 | -1,50,000 | 15,00,000 |

| 38 | 4 | -1,50,000 | 15,00,000 | -1,50,000 | 15,00,000 |

| 39 | 5 | -1,50,000 | 15,00,000 | -1,50,000 | 15,00,000 |

| 40 | 6 | -1,50,000 | 15,00,000 | -1,50,000 | 15,00,000 |

| 41 | 7 | -1,50,000 | 15,00,000 | -1,50,000 | 15,00,000 |

| 42 | 8 | -1,50,000 | 15,00,000 | -1,50,000 | 15,00,000 |

| 43 | 9 | -1,50,000 | 15,00,000 | -1,50,000 | 15,00,000 |

| 44 | 10 | -1,50,000 | 15,00,000 | -1,50,000 | 15,00,000 |

| 45 | 11 | -1,50,000 | 15,00,000 | -1,50,000 | 15,00,000 |

| 46 | 12 | -1,50,000 | 15,00,000 | -1,50,000 | 15,00,000 |

| 47 | 13 | -1,50,000 | 15,00,000 | -1,50,000 | 15,00,000 |

| 48 | 14 | -1,50,000 | 15,00,000 | -1,50,000 | 15,00,000 |

| 49 | 15 | -1,50,000 | 15,00,000 | -1,50,000 | 15,00,000 |

| 50 | 16 | -1,50,000 | 15,00,000 | -1,50,000 | 15,00,000 |

| 51 | 17 | -1,50,000 | 15,00,000 | -1,50,000 | 15,00,000 |

| 52 | 18 | -1,50,000 | 15,00,000 | -1,50,000 | 15,00,000 |

| 53 | 19 | -1,50,000 | 15,00,000 | -1,50,000 | 15,00,000 |

| 54 | 20 | -1,50,000 | 15,00,000 | -1,50,000 | 15,00,000 |

| 55 | 63,07,618 | 15,00,000 | 1,06,14,761 | 15,00,000 | |

| IRR | 6.64% | 10.94% | |||

The final maturity value in a PPF account is ₹63.07 lakhs, with an IRR of 6.64% when combined with pure-term life insurance.

For an ELSS investment, the pre-tax maturity value amounts to ₹1.14 crores, and after capital gains tax, the post-tax maturity value is ₹1.06 crores, resulting in an IRR of 10.94% when combined with pure term life insurance.

Investing in this strategy offers a higher yield compared to the India First Life Radiance Smart Invest Plan. If the yield exceeds the inflation rate, it will accelerate the wealth accumulation process.

| ELSS Tax Calculation | |

| Maturity value after 20 years | 1,14,67,290 |

| Purchase price | 28,42,000 |

| Long-Term Capital Gains | 86,25,290 |

| Exemption limit | 1,00,000 |

| Taxable LTCG | 85,25,290 |

| Tax paid on LTCG | 8,52,529 |

| Maturity value after tax | 1,06,14,761 |

Final Verdict on India First Life Radiance Smart Invest Plan

The India First Life Radiance Smart Invest Plan is a market-linked product that offers life cover and various fund options to cater to different risk appetites. However, investing in this IndiaFirst Life Radiance Smart Invest Plan is not advisable due to its poor returns.

Investment returns should outpace inflation in the long run. The yield from the India First Life Radiance Smart Invest Plan is lower than inflation because of hefty charges due to high agent commissions and other reasons, making this plan unsuitable for investment.

A pure-term life insurance policy with adequate coverage is essential for providing a safety net for your family. Separating insurance and investment decisions is prudent, as it simplifies the wealth accumulation process.

Social media platforms like Quora, Twitter, and Facebook can be a great launching pad for your financial education journey, but they shouldn’t be your final destination. While you might find interesting tidbits and tips, they lack the crucial elements needed for sound financial decisions.

If you need guidance in selecting investment products, seek professional help. A Certified Financial Planner (CFP) can create a tailored financial plan to suit your needs.

Leave a Reply