In today’s evolving financial environment, individuals increasingly look for solutions that help their money serve multiple purposes rather than remain idle.

Along with providing life insurance protection, the Pramerica Life Invest Shield Plan aims to offer substantial financial security to your family while creating wealth through market-linked investment opportunities.

In this article, we will take a closer look at how the plan works and evaluate its key features, benefits, and limitations to determine whether it is a suitable choice for investors.

Table of Contents

1.) What is the Pramerica Life Invest Shield Plan?

2.) What are the Features of the Pramerica Life Invest Shield Plan?

3.) Who is Eligible for the Pramerica Life Invest Shield Plan?

4.) What are the Benefits of the Pramerica Life Invest Shield Plan?

5.) What are the Investment Strategies and Fund Options in the Pramerica Life Invest Shield Plan?

6.) What are the Charges in the Pramerica Life Invest Shield Plan?

7.) Grace Period, Discontinuance and Revival of the Pramerica Life Invest Shield Plan

8.) Free Look Period for the Pramerica Life Invest Shield Plan

9.) Surrendering the Pramerica Life Invest Shield Plan

10.) What are the Advantages of the Pramerica Life Invest Shield Plan?

11.) What are the Disadvantages of the Pramerica Life Invest Shield Plan?

12.) Research Methodology of Pramerica Life Invest Shield Plan

13.) Pramerica Life Invest Shield Plan Vs. Other Investments

14.) Final Verdict on Pramerica Life Invest Shield Plan

1.) What is the Pramerica Life Invest Shield Plan?

The Pramerica Life Invest Shield Plan is a Unit-Linked Non-Participating Individual Savings Life Insurance Plan.

It gives your family life cover while also building wealth through market-linked returns.

Security and savings, seamlessly combined in Pramerica Life Invest Shield.

2.) What are the features of the Pramerica Life Invest Shield Plan?

- Comprehensive life insurance protection coupled with the potential for long-term wealth creation through market-linked investments.

- Mortality Charge Refund Benefit: Starting from the end of the 11th policy year, a portion of the mortality charges deducted—ranging from 50% to 300%—is credited back to the fund value, enhancing the overall corpus.

- Premium Allocation Charge Refund: The plan refunds 100% of the premium allocation charges during the period from the 11th to the 17th policy year, depending on the policy terms.

- Persistency Boosters: Additional fund value enhancements are provided at specified milestones, rewarding long-term policy continuation.

- Maturity Addition: An extra addition is credited to the fund value at maturity, helping increase the final payout.

- Flexible Investment Options: Policyholders can choose between two investment strategies and invest in any of the nine available fund options, based on their risk appetite and financial objectives.

- Flexible Premium Payment Structure: Offers multiple premium payment modes along with customizable policy and premium payment terms.

- Tax Benefits: Premiums paid and benefits received may qualify for tax benefits under prevailing tax laws, subject to applicable conditions and regulations.

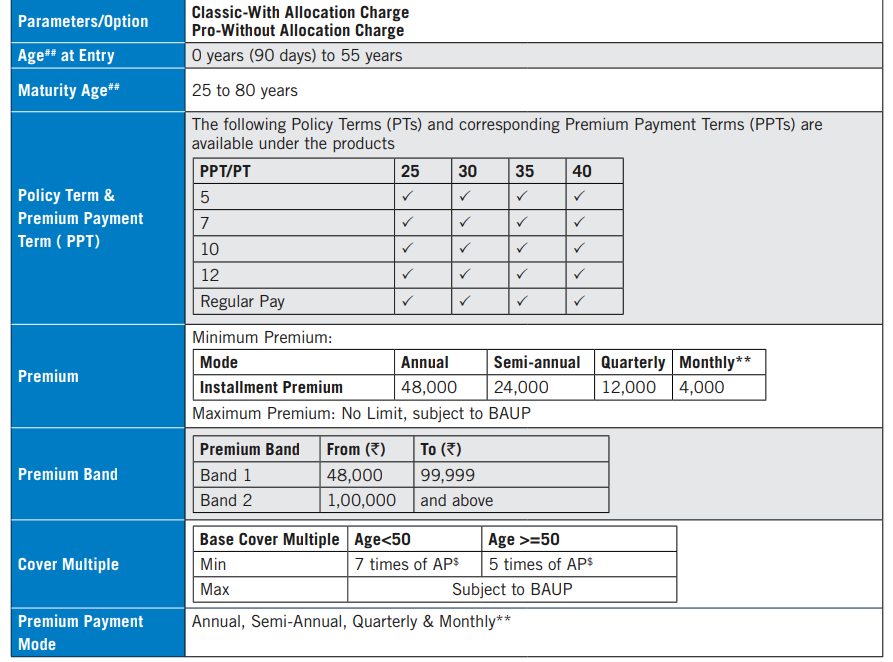

3.) Who is eligible for the Pramerica Life Invest Shield Plan?

4.) What are the benefits of the Pramerica Life Invest Shield Plan?

Death Benefit

(For both Plan Options)

In case of an unfortunate demise of the Life Insured during the Policy Term, provided all due premiums are paid, the following benefits shall be payable:

The death benefit shall be the higher of

- Sum Assured, including Top-Up Sum Assured, if any, or

- Fund Value, including Top-Up Fund Value, if any, or

- 105% of total premiums paid, including Top-Up premiums till date of death, if any

Where Sum Assured is a multiple of Annualised Premium that is based on age at entry of Life Insured, Annualised Premium, Premium Payment Term and Policy Term.

Maturity Benefit

(For both Plan Options)

On survival of the Life Insured till the maturity date, the Fund Value, including Top-Up fund value, if any, shall be payable, and the policy shall terminate.

Persistency Boosters

(For both plan options)

Provided all due premiums are paid, Persistency Boosters of 1% will be allocated as extra units at the end of every 5th policy year, starting from the end of the 5th policy year.

Persistency Boosters as a percentage of average fund value, including Top-up Fund Value at preceding 36-month anniversaries, would be allocated to the policyholder’s unit account.

Maturity Additions

(For both plan options)

Provided all due premiums are paid, on survival till the end of the policy term, Maturity Additions as % of Total Premiums Paid will be added to the Fund Value, as per the table below:

| Payment Options | Maturity Additions |

| Limited Pay | 15% |

| Regular Pay | 8% |

5.) What are the investment strategies and fund options in the Pramerica Life Invest Shield Plan?

At inception, the Policyholder can choose one of the following investment strategies.

- Defined Portfolio Strategy

- Life Stage Portfolio Strategy

Within the Defined Portfolio Strategy, the Policyholder can choose to invest with or without the Systematic Transfer Plan Option.

Defined Portfolio Strategy

Under this option, you can choose to invest in any of the funds available (except the discontinuance fund or Liquid Fund) in proportion to your choice. Within the Defined Portfolio strategy, you also have the option to select the Systematic Transfer Plan (STP) option, for which the Liquid Fund will be made available to you.

You can switch money among these funds using the switch option. You can choose from nine funds to invest your money.

If you opt for more than one fund, the minimum investment in any fund should be at least 10% of the Annual Premium.

The funds and fund objectives are as follows:

| S.no | Fund Name | Asset Allocation | Risk Profile | ||

| Equity & Equity-related instruments | Govt. Securities & Corp. Bonds | Money market instruments | |||

| 1 | Debt fund | 0% | 50-100% | 0-40% | Low |

| 2 | Balanced Equilibrium Fund | 65-75% | 25-35% | 25-35% | Medium |

| 3 | Growth Momentum fund | 75-85% | 15-25% | 15-25% | High |

| 4 | Large-cap advantage fund | 85-100% | 0-15% | 0-15% | High |

| 5 | Flexi Cap Opportunities Fund | 85-100% | 0-15% | 0-15% | High |

| 6 | Pramerica Nifty Mid Cap 50 Correlation Fund | 90-100% | 0-10% | 0-10% | High |

| 7 | Pramerica Nifty Small cap 250 Quality 50 Correlation Fund | 90-100% | 0% | 0-10% | High |

| 8 | Pramerica A.G.A.M Ethical Equity Fund | 80-100% | 0-20% | 0% | High |

| 9 | Pramerica Rising Bharat Fund | 90-100% | 0-10% | 0-10% | High |

| Liquid fund | 0% | 0% | 100% | Low | |

| Discontinued policy fund | 0% | 60-100% | 0-40% | Low | |

Systematic Transfer Plan (STP)

With STP, you can invest a specific amount at monthly intervals, which gives you the advantage of Rupee Cost Averaging.

You can buy more units when markets are down and fewer units when markets are up, thereby reducing the average unit purchase cost.

You can choose STP only for 12 months; an option would be available to policies wherein the premium is to be paid annually.

Life Stage Portfolio Strategy

The plan offers a life-stage-based investment strategy wherein the investments are distributed between the Large Cap Equity Fund and the Debt Fund, with their proportions varying as per the different life stages.

At inception, the funds will be distributed between two funds, the Multi Cap Opportunities Fund & Debt Fund.

As and when the next milestone is achieved, the funds will be redistributed according to the attained age (age bands) as given in the following table:

| Age as on the last birthday and the last policy anniversary | Debt fund | Large cap Equity Fund |

| Up to 25 | 15% | 85% |

| 26 – 30 | 20% | 80% |

| 31 – 35 | 25% | 75% |

| 36 – 40 | 30% | 70% |

| 41 – 45 | 35% | 65% |

| 46 – 50 | 40% | 60% |

| 51 – 55 | 45% | 55% |

| 56 and above | 50% | 50% |

6.) What are the charges in the Pramerica Life Invest Shield Plan?

Premium Allocation Charge

Plan Option- Classic

| Policy Year | % of Annualized Premium |

| 1 | 7% |

| 2 | 6% |

| 3 | 6% |

| 4 | 3% |

| 5 | 3% |

| 6 | 2% |

| 7 | 1% |

| Thereafter | Nil |

Top-up premiums are subject to an allocation charge of 2.0%.

Plan Option –Pro

No charge on base premium, as well as on Top-up premium, is applicable.

Policy Administration Charge

The administration Charge of 0.34% of Annualised Premium, increasing 5% annually, will be levied from the 4th policy year at the beginning of every month by redemption of units for a maximum of 30 years, subject to a maximum of ₹500 per month.

Mortality Charge

Mortality charge will apply to the sum at risk. It will be deducted monthly by cancellation of units from the unit account.

For females, there is a three-year age setback in mortality rates compared to males.

| Attained Age | 20 | 30 | 40 | 50 |

| Mortality Charge | 1.0164 | 1.0747 | 1.848 | 4.8796 |

Fund Management Charges (FMC)

| Fund Name | FMC per annum |

| Debt Fund | 1.20% |

| Balanced Equilibrium Fund | 1.35% |

| Growth Momentum Fund | 1.35% |

| Large Cap Advantage Fund | 1.35% |

| Flexi Cap Opportunities Fund | 1.35% |

| Pramerica Nifty Mid Cap 50 Correlation Fund | 1.25% |

| Pramerica Nifty Small cap 250 Quality 50 Correlation Fund | 1.25% |

| Pramerica A.G.A.M Ethical Equity Fund | 1.35% |

| Pramerica Rising Bharat Fund | 1.35% |

| Liquid Fund (in case of STP only) | 1.20% |

| Discontinued Policy Fund | 0.50% |

Discontinuance Charge

Discontinuance charge will be based on the year of discontinuance and the premium amount.

There is no discontinuance charge from the 5th policy year.

Inference from the charges:

The charge structure reveals one of the key drawbacks of ULIPs.

In addition to fund management charges, policyholders are subject to various other costs such as premium allocation charges, policy administration charges, mortality charges, and other deductions.

As a result, ULIPs tend to be costlier than most standalone market-linked investment products such as mutual funds.

These charges can erode a portion of your investment corpus over time, potentially reducing the overall returns generated and limiting long-term wealth creation.

Even though some charges may be refunded at later stages of the policy, the impact of these deductions during the initial years cannot be ignored.

7.) Grace Period, Discontinuance and Revival of the Pramerica Life Invest Shield Plan

Garce Period

A grace period of 30 days in case of non-monthly mode policies and a 15-day grace period in case of monthly mode policies from the due date to pay the Premium is given.

Discontinuance

Discontinued during the first five Policy years: the fund value after deducting the applicable discontinuance charges shall be credited to the Discontinued Policy Fund, and the risk cover and rider cover, if any, shall cease.

The proceeds of the discontinued policy fund shall be paid to the policyholder at the end of the revival period or lock-in period, whichever is later.

Discontinued after the first five Policy years: the policy shall be converted into a reduced paid-up policy with the paid-up sum assured, i.e. original sum assured multiplied by a ratio of “total period for which premiums have already been paid” to the “maximum period for which premiums were originally payable”.

At the end of the revival period, the proceeds of the policy fund shall be paid to the policyholder.

Revival

You have an option to revive your discontinued policy within three years from the date of the first unpaid premium.

8.) Free Look Period for the Pramerica Life Invest Shield Plan

You will have a period of 30 days from the date of receipt of the Policy document to review the terms and conditions of the Policy, and if you disagree with any of these terms and conditions, you have the option to return the Policy.

9.) Surrendering the Pramerica Life Invest Shield Plan

The policy will acquire surrender value immediately from the first policy year.

However, no surrender value will be payable during the “lock-in period”, which is a period of five consecutive Policy years from the date of commencement of the Policy.

If the Policyholder opts for surrender within the first five Policy years, the Fund Value, after deducting the applicable discontinuance charges, shall be credited to the Discontinued Policy Fund, and the risk cover and rider cover, if any, shall cease.

The proceeds from the Discontinued Policy Fund shall be paid at the end of the lock-in period as Surrender Value.

Only the fund management charge shall be deducted from this fund during this period.

10.) What are the advantages of the Pramerica Life Invest Shield Plan?

- Top-Up Premium Facility: The plan allows you to invest additional amounts through Top-Up Premiums over and above your regular premiums, helping you enhance your investment corpus whenever surplus funds are available.

- Fund Switching Option: Under the Defined Portfolio Strategy, you can switch your investments between the available funds, enabling you to align your portfolio with changing market conditions and financial goals.

- Premium Redirection Facility: You can modify the allocation of future premiums among different funds without affecting your existing investments, providing greater flexibility in managing your portfolio.

- Partial Withdrawal Facility: Partial withdrawals are permitted only after the completion of the mandatory 5-year lock-in period, allowing access to funds when needed.

- Systematic Withdrawal Option (SWO): From the 10th policy year onwards, you can opt for an automated withdrawal facility whereby a predetermined percentage of the fund value is withdrawn at regular intervals, helping create a stream of periodic cash flows.

- Settlement Option at Maturity: Instead of receiving the entire maturity benefit as a lump sum, you may choose to receive the proceeds in a structured manner over a period of up to five years after maturity, providing greater flexibility in managing the maturity corpus.

11.) What are the disadvantages of the Pramerica Life Invest Shield Plan?

- No Loan Facility: The plan does not offer a loan feature, meaning policyholders cannot borrow against the policy value to meet short-term financial needs.

- Limited Liquidity in the Initial Years: Access to funds is restricted during the first five policy years due to the mandatory lock-in period, reducing financial flexibility.

- Premiums Are Subject to Charges: Not all of the premium paid is invested. Various charges are deducted before the balance is allocated to the chosen funds, which can impact corpus accumulation, especially during the initial years.

- Risk-Return Trade-off Appears Unfavourable: Although the plan exposes investors to market-linked risks, the net returns—after accounting for multiple policy charges—may not adequately compensate for the level of risk undertaken. Comparable investment avenues, such as mutual funds, may potentially offer better risk-adjusted returns at a lower cost.

12.) Research Methodology of Pramerica Life Invest Shield Plan

After understanding the features, benefits, and charges of the Pramerica Life Invest Shield Plan, the next step is to evaluate its return potential.

A practical way to do this is by analysing the Internal Rate of Return (IRR) based on the benefit illustrations provided in the policy brochure.

Benefit Illustration – IRR Analysis of Pramerica Life Invest Shield Plan

Consider a 35-year-old male who purchases the plan with a sum assured of ₹75 lakhs, a policy term of 40 years, and a premium payment term of 12 years.

He pays an annual premium of ₹1 lakh and opts for the Classic Plan Option.

| Male | 35 years |

| Sum Assured | ₹ 75,00,000 |

| Policy Term | 40 years |

| Premium Paying Term | 12 years |

| Annualised Premium | ₹ 1,00,000 |

Under the plan, the maturity benefit comprises the accumulated fund value along with applicable persistency additions and maturity enhancements.

The insurer has provided illustrations assuming annual returns of 4% and 8%.

These figures are purely illustrative and do not represent guaranteed returns.

| At 4% p.a. | At 8% p.a. | ||||

| Age | Year | Annualised premium / Maturity benefit | Death benefit | Annualised premium / Maturity benefit | Death benefit |

| 35 | 1 | -1,00,000 | 75,00,000 | -1,00,000 | 75,00,000 |

| 36 | 2 | -1,00,000 | 75,00,000 | -1,00,000 | 75,00,000 |

| 37 | 3 | -1,00,000 | 75,00,000 | -1,00,000 | 75,00,000 |

| 38 | 4 | -1,00,000 | 75,00,000 | -1,00,000 | 75,00,000 |

| 39 | 5 | -1,00,000 | 75,00,000 | -1,00,000 | 75,00,000 |

| 40 | 6 | -1,00,000 | 75,00,000 | -1,00,000 | 75,00,000 |

| 41 | 7 | -1,00,000 | 75,00,000 | -1,00,000 | 75,00,000 |

| 42 | 8 | -1,00,000 | 75,00,000 | -1,00,000 | 75,00,000 |

| 43 | 9 | -1,00,000 | 75,00,000 | -1,00,000 | 75,00,000 |

| 44 | 10 | -1,00,000 | 75,00,000 | -1,00,000 | 75,00,000 |

| 45 | 11 | -1,00,000 | 75,00,000 | -1,00,000 | 75,00,000 |

| 46 | 12 | -1,00,000 | 75,00,000 | -1,00,000 | 75,00,000 |

| 47 | 13 | 0 | 75,00,000 | 0 | 75,00,000 |

| 48 | 14 | 0 | 75,00,000 | 0 | 75,00,000 |

| 49 | 15 | 0 | 75,00,000 | 0 | 75,00,000 |

| 50 | 16 | 0 | 75,00,000 | 0 | 75,00,000 |

| 51 | 17 | 0 | 75,00,000 | 0 | 75,00,000 |

| 52 | 18 | 0 | 75,00,000 | 0 | 75,00,000 |

| 53 | 19 | 0 | 75,00,000 | 0 | 75,00,000 |

| 54 | 20 | 0 | 75,00,000 | 0 | 75,00,000 |

| 55 | 21 | 0 | 75,00,000 | 0 | 75,00,000 |

| 56 | 22 | 0 | 75,00,000 | 0 | 75,00,000 |

| 57 | 23 | 0 | 75,00,000 | 0 | 75,00,000 |

| 58 | 24 | 0 | 75,00,000 | 0 | 75,00,000 |

| 59 | 25 | 0 | 75,00,000 | 0 | 75,00,000 |

| 60 | 26 | 0 | 75,00,000 | 0 | 75,00,000 |

| 61 | 27 | 0 | 75,00,000 | 0 | 75,00,000 |

| 62 | 28 | 0 | 75,00,000 | 0 | 75,00,000 |

| 63 | 29 | 0 | 75,00,000 | 0 | 75,00,000 |

| 64 | 30 | 0 | 75,00,000 | 0 | 75,00,000 |

| 65 | 31 | 0 | 0 | ||

| 66 | 32 | 0 | 0 | ||

| 67 | 33 | 0 | 0 | ||

| 68 | 34 | 0 | 0 | ||

| 69 | 35 | 0 | 0 | ||

| 70 | 36 | 0 | 0 | ||

| 71 | 37 | 0 | 0 | ||

| 72 | 38 | 0 | 0 | ||

| 73 | 39 | 0 | 0 | ||

| 74 | 40 | 0 | 0 | ||

| 75 | 27,03,644 | 1,06,21,999 | |||

| IRR | 2.37% | 6.45% | |||

At a 4% annual return assumption:

Maturity fund value: ₹27.03 lakh

IRR: 2.37% p.a.

This return is significantly below the long-term inflation rate and offers very little real wealth creation despite the long investment horizon.

At an 8% annual return assumption:

Maturity fund value: ₹1.06 crore

IRR: 6.45% p.a.

Even under this relatively optimistic scenario, the effective return remains modest when compared with alternative market-linked investments.

The numbers reveal a key concern with the plan. While the investor bears market risk, the effective returns are diluted by various policy charges and costs embedded within the product.

As a result, the return profile resembles that of relatively conservative investment options rather than a long-term market-linked product.

The return illustrations suggest that the wealth-creation component may not be compelling enough to justify the costs and risks involved.

Based on the projected IRRs, the plan appears unlikely to significantly accelerate wealth creation and may, in fact, slow down long-term financial progress compared to other market-linked investment avenues.

13.) Pramerica Life Invest Shield Plan Vs. Other Investments

The analysis clearly indicates that the Pramerica Life Invest Shield Plan is not an efficient vehicle for long-term wealth creation.

A more effective strategy is to separate insurance and investments, allowing each component to serve its intended purpose.

Let us compare the outcomes using the same assumptions.

Pramerica Life Invest Shield Plan Vs. Pure-term + PPF/Equity Mutual Fund

A pure-term life insurance policy providing a sum assured of ₹75 lakh costs approximately ₹23,900 per year for a 30-year term.

In contrast, the Pramerica Life Invest Shield Plan requires an annual premium of ₹1 lakh.

By opting for the term plan, the investor saves ₹76,100 every year, which can be invested separately to build wealth.

| Pure Term Life Insurance Policy | |

| Sum Assured | ₹ 75,00,000 |

| Policy Term | 30 years |

| Premium Paying Term | 10 years |

| Annualised Premium | ₹ 23,900 |

| Investment | ₹ 76,100 |

Another important point is that the premium payment term under the Pramerica Life Invest Shield Plan is 12 years, whereas the term insurance premium is payable only for 10 years in this illustration.

Therefore, during the final two years, the entire ₹1 lakh can be invested.

Necessary adjustments have also been made to satisfy the minimum investment period requirement of PPF.

The investment component can then be allocated based on the investor’s risk appetite:

- Conservative investors may choose debt-oriented options such as PPF.

- Aggressive investors may prefer equity-oriented options such as Equity Mutual Funds.

| Term Insurance + PPF | Term insurance + Equity Mutual Fund | ||||

| Age | Year | Term Insurance premium + PPF | Death benefit | Term Insurance premium + Equity Mutual Fund | Death benefit |

| 35 | 1 | -1,00,000 | 75,00,000 | -1,00,000 | 75,00,000 |

| 36 | 2 | -1,00,000 | 75,00,000 | -1,00,000 | 75,00,000 |

| 37 | 3 | -1,00,000 | 75,00,000 | -1,00,000 | 75,00,000 |

| 38 | 4 | -1,00,000 | 75,00,000 | -1,00,000 | 75,00,000 |

| 39 | 5 | -1,00,000 | 75,00,000 | -1,00,000 | 75,00,000 |

| 40 | 6 | -1,00,000 | 75,00,000 | -1,00,000 | 75,00,000 |

| 41 | 7 | -1,00,000 | 75,00,000 | -1,00,000 | 75,00,000 |

| 42 | 8 | -1,00,000 | 75,00,000 | -1,00,000 | 75,00,000 |

| 43 | 9 | -1,00,000 | 75,00,000 | -1,00,000 | 75,00,000 |

| 44 | 10 | -1,00,000 | 75,00,000 | -1,00,000 | 75,00,000 |

| 45 | 11 | -1,00,000 | 75,00,000 | -1,00,000 | 75,00,000 |

| 46 | 12 | -98,500 | 75,00,000 | -1,00,000 | 75,00,000 |

| 47 | 13 | -500 | 75,00,000 | 0 | 75,00,000 |

| 48 | 14 | -500 | 75,00,000 | 0 | 75,00,000 |

| 49 | 15 | -500 | 75,00,000 | 0 | 75,00,000 |

| 50 | 16 | 0 | 75,00,000 | 0 | 75,00,000 |

| 51 | 17 | 0 | 75,00,000 | 0 | 75,00,000 |

| 52 | 18 | 0 | 75,00,000 | 0 | 75,00,000 |

| 53 | 19 | 0 | 75,00,000 | 0 | 75,00,000 |

| 54 | 20 | 0 | 75,00,000 | 0 | 75,00,000 |

| 55 | 21 | 0 | 75,00,000 | 0 | 75,00,000 |

| 56 | 22 | 0 | 75,00,000 | 0 | 75,00,000 |

| 57 | 23 | 0 | 75,00,000 | 0 | 75,00,000 |

| 58 | 24 | 0 | 75,00,000 | 0 | 75,00,000 |

| 59 | 25 | 0 | 75,00,000 | 0 | 75,00,000 |

| 60 | 26 | 0 | 75,00,000 | 0 | 75,00,000 |

| 61 | 27 | 0 | 75,00,000 | 0 | 75,00,000 |

| 62 | 28 | 0 | 75,00,000 | 0 | 75,00,000 |

| 63 | 29 | 0 | 75,00,000 | 0 | 75,00,000 |

| 64 | 30 | 0 | 75,00,000 | 0 | 75,00,000 |

| 65 | 31 | 0 | 75,00,000 | 0 | 75,00,000 |

| 66 | 32 | 0 | 75,00,000 | 0 | 75,00,000 |

| 67 | 33 | 0 | 75,00,000 | 0 | 75,00,000 |

| 68 | 34 | 0 | 75,00,000 | 0 | 75,00,000 |

| 69 | 35 | 0 | 75,00,000 | 0 | 75,00,000 |

| 70 | 36 | 0 | 75,00,000 | 0 | 75,00,000 |

| 71 | 37 | 0 | 75,00,000 | 0 | 75,00,000 |

| 72 | 38 | 0 | 75,00,000 | 0 | 75,00,000 |

| 73 | 39 | 0 | 75,00,000 | 0 | 75,00,000 |

| 74 | 40 | 0 | 75,00,000 | 0 | 75,00,000 |

| 75 | 1,03,69,837 | 4,43,07,897 | |||

| IRR | 6.38% | 10.83% | |||

Scenario 1: Term Insurance + PPF

Investing the surplus amount in PPF over a 40-year period results in a maturity value of approximately ₹1.03 crore, generating an IRR of 6.38%.

What is noteworthy is that this return is broadly comparable to the 6.45% IRR generated by the Pramerica Life Invest Shield Plan under its optimistic 8% illustration.

However, PPF is a government-backed, low-risk debt instrument, whereas the ULIP exposes the investor to market risk.

Scenario 2: Term Insurance + Equity Mutual Fund

If the annual surplus is invested in an Equity Mutual Fund, the corpus grows substantially over the same period.

Pre-tax maturity value: ₹5.04 crore

Post-tax maturity value: ₹4.43 crore

Post-tax IRR: 10.83%

This demonstrates the power of low-cost, market-linked investing when insurance and investments are kept separate.

| Equity Mutual Fund Tax Calculation | |

| Maturity value after 40 years | 5,04,82,454 |

| Purchase price | 9,61,000 |

| Long-Term Capital Gains | 4,95,21,454 |

| Exemption limit | 1,25,000 |

| Taxable LTCG | 4,93,96,454 |

| Tax paid on LTCG | 61,74,557 |

| Maturity value after tax | 4,43,07,897 |

The combination of a pure-term insurance policy and independent investments provides a superior financial outcome on multiple fronts.

It delivers adequate life cover, offers greater flexibility, and creates a significantly larger retirement corpus.

Even a conservative PPF-based strategy matches the ULIP’s return profile, while an equity mutual fund strategy comfortably outperforms it.

In comparison, the Pramerica Life Invest Shield Plan suffers from high embedded costs, lower effective returns, and a less favourable risk-reward trade-off.

For investors seeking meaningful wealth creation alongside sufficient life protection, a “Term Insurance + Investment” strategy remains a far more efficient and effective approach.

14.)Final Verdict on Pramerica Life Invest Shield Plan

The Pramerica Life Invest Shield Plan combines life insurance with market-linked investing, offering benefits such as fund value accumulation, persistency additions, maturity enhancements, and the refund of certain policy charges.

On the surface, these features may appear attractive to investors seeking both protection and wealth creation through a single product.

However, a closer examination of the plan’s projected returns paints a different picture.

Despite exposing investors to market risk, the plan’s numerous charges substantially dilute the investment returns.

As a result, the eventual corpus generated is unlikely to deliver meaningful inflation-adjusted wealth creation over the long term.

For most investors, the primary objective of a long-term investment should be to build a corpus capable of funding major life goals such as retirement, children’s education, or financial independence.

Based on the return analysis, the Pramerica Life Invest Shield Plan falls short of this objective.

The risk undertaken is not adequately compensated by the returns generated, resulting in an unfavourable risk-reward trade-off.

A more efficient approach is to separate insurance from investments.

A pure-term life insurance policy can provide adequate financial protection for dependents at a fraction of the cost, while the savings can be invested in suitable instruments such as mutual funds, PPF, or other goal-based investment avenues.

This strategy offers greater transparency, flexibility, and significantly better wealth-creation potential.

Before investing in any financial product, assess whether it aligns with your financial goals, risk appetite, liquidity needs, and investment horizon.

If required, seek guidance from a Certified Financial Planner (CFP) who can help design a diversified, goal-oriented financial plan tailored to your unique circumstances.

Leave a Reply