Every investor has heard this statement at some point:

“The Nifty has delivered around 12% CAGR over the long term.”

Sounds reassuring, doesn’t it?

Naturally, most people assume that if the market delivers 12%, they too should earn something close to that number over time.

But reality tells a very different story.

If average market returns are so “normal,” why do so many investors struggle to build meaningful wealth?

Why do many enter the market enthusiastically, only to exit disappointed after a few years?

And why do only a small percentage of investors truly benefit from long-term compounding?

The answer lies in one uncomfortable truth:

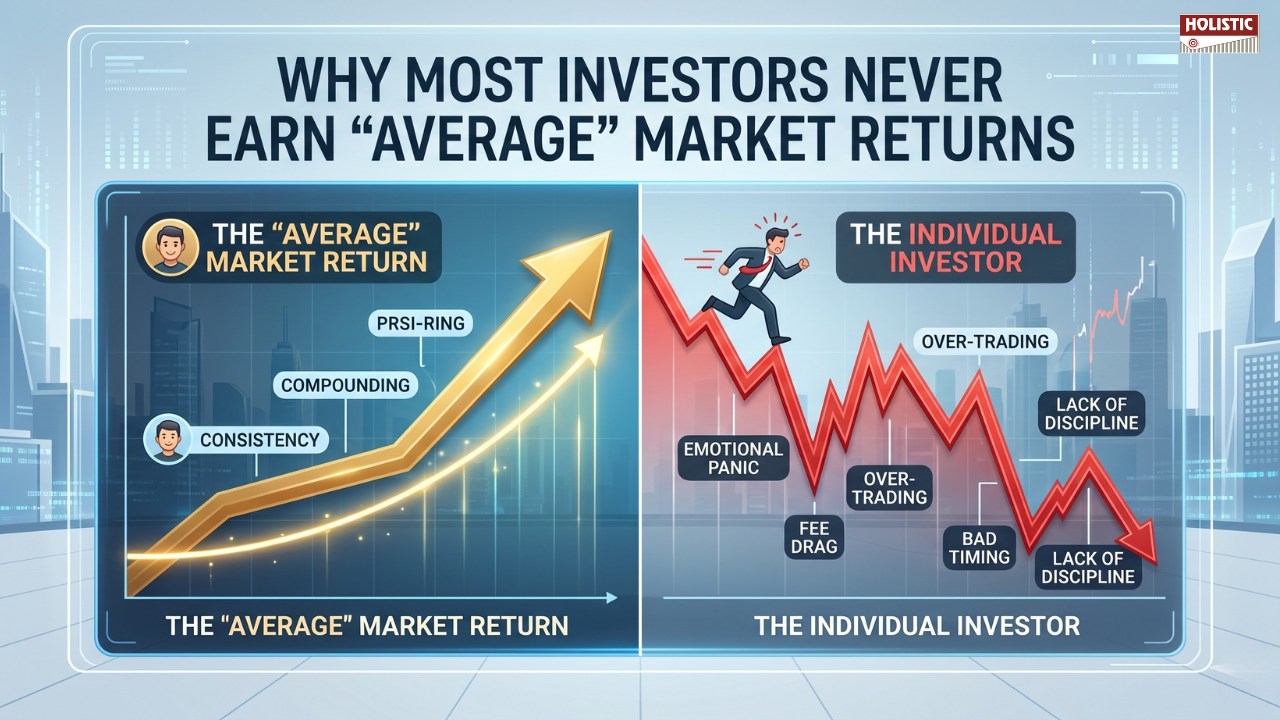

The average return of the market is not the same as the average return earned by investors.

And understanding this difference may completely change the way you think about investing.

Table of Contents:

- The Dangerous Illusion of “Average Returns”

- Why Historical Returns Cannot Predict Your Future

- The Hidden Truth: Returns Are Never Equally Distributed

- Why Investor Behaviour Matters More Than Market Performance

- Understanding Sequence Risk and Survival

- The Real Reason Most Investors Fail to Build Wealth

- Why SIP Works Even Without Guaranteeing Returns

- Discipline, Not Intelligence, Builds Long-Term Wealth

- Conclusion: The Market Rewards Those Who Stay

The Dangerous Illusion of “Average Returns”

The biggest mistake investors make is treating historical market returns like future promises.

When we say the Nifty delivered around 12% CAGR historically, we are talking about a backward-looking number.

It simply describes what happened over a particular period in the past.

But markets do not move in straight lines.

Future returns may be:

- Higher than historical averages

- Lower than historical averages

- Or similar averages achieved through a completely different journey

This distinction matters more than most people realize.

A historical CAGR is not a guarantee. It is merely a reference point.

Yet many investors unknowingly convert:

- Historical data → into expectations

- Expectations → into certainty

- Certainty → into entitlement

That’s where disappointment begins.

Even long-term index returns vary significantly depending on:

- Starting year

- Ending year

- Reinvestment assumptions

- Market cycles

So before expecting “average returns,” investors must first understand this:

Past performance explains history. It does not predict destiny.

Why Historical Returns Cannot Predict Your Future

Imagine two investors entering the market at different times.

One begins investing immediately after a major crash.

Another starts during a market euphoria phase.

Both may stay invested for ten years.

Yet their experiences—and returns—can look dramatically different.

This is because investing is deeply dependent on timing, behaviour, and emotional resilience.

The market itself may recover eventually.

But will the investor remain invested long enough to experience that recovery?

That is the real challenge.

The Hidden Truth: Returns Are Never Equally Distributed

Another major misconception is believing that market returns are distributed evenly among investors.

They are not.

In reality, investing outcomes often follow what economists describe as a power-law distribution or the Pareto Principle.

In simple terms:

A small percentage of investors capture a disproportionately large share of the total wealth created.

Why?

Because only a minority:

- Stay invested long enough

- Continue through crashes

- Avoid emotional decisions

- Maintain discipline consistently

Most investors interrupt the process somewhere along the way.

Some panic during corrections.

Some stop SIPs during bear markets.

Some chase trends and exit at the wrong time.

As a result, while the market may generate strong long-term returns overall, the actual experience of investors becomes highly unequal.

The “average” exists mathematically.

But very few investors truly live through the journey required to earn it.

Why Investor Behaviour Matters More Than Market Performance

Many people assume successful investing is mainly about intelligence.

But long-term investing has less to do with IQ and far more to do with behaviour.

Can you stay calm during a 30% fall?

Can you continue investing when headlines predict disaster?

Can you avoid comparing your portfolio daily?

That’s where wealth creation actually happens.

Because markets test patience far more than they test knowledge.

And unfortunately, patience is rare.

Understanding Sequence Risk and Survival

One of the most overlooked concepts in investing is sequence risk.

This simply means:

The order in which returns occur matters enormously to investors.

For example:

A market crash early in your investing journey may feel manageable if you continue investing regularly.

But the same crash near retirement—or during a job loss—can become emotionally and financially devastating.

This is why the market’s “average return” often differs from an individual investor’s lived experience.

The index survives every crisis:

- The 2008 crash

- The COVID collapse

- Sharp bear markets

- Geopolitical uncertainty

But individual investors may not.

Some exit permanently.

Some stop investing entirely.

Some lose confidence and never return.

And once the process breaks, compounding breaks too.

The Real Reason Most Investors Fail to Build Wealth

The biggest obstacle in investing is not volatility.

It is interruption.

Many investors start enthusiastically during bull markets but fail to continue when markets become uncomfortable.

This is precisely why long-term wealth creation looks simple in theory—but difficult in practice.

The formula itself is easy:

- Invest regularly

- Stay invested

- Allow compounding to work

But emotionally surviving decades of uncertainty is far harder than most expect.

Why SIP Works Even Without Guaranteeing Returns

This is exactly where SIPs (Systematic Investment Plans) become powerful.

Not because they guarantee returns.

And certainly not because they eliminate market risk.

Their true strength lies elsewhere.

A SIP creates:

- Discipline

- Continuity

- Participation

- Emotional structure

It transforms investing from a decision-driven activity into a habit-driven process.

And habits are easier to sustain during uncertainty.

When investors automate investing regularly:

- They reduce emotional timing decisions

- They continue through market volatility

- They participate across multiple market cycles

Over long periods, this dramatically improves the probability of capturing market-linked returns.

The beauty of SIP is not perfection.

The beauty is persistence.

Discipline, Not Intelligence, Builds Long-Term Wealth

The market does not consistently reward the smartest investors.

It often rewards the most disciplined ones.

The investors who quietly continue:

- During crashes

- During uncertainty

- During boredom

- During pessimism

These are usually the investors who eventually experience the power of compounding.

Not because they predicted markets perfectly—

But because they stayed long enough for time to work.

Conclusion: The Market Rewards Those Who Stay

The reason average market returns are difficult to earn has very little to do with mathematics.

It has everything to do with human behaviour.

Historical averages are not guarantees.

Investor outcomes are not equally distributed.

And the market’s journey is very different from the investor’s lived experience.

This is why investing success ultimately comes down to one simple ability:

Can you stay in the game long enough?

Because markets reward participation far more than prediction.

And in the end, wealth is rarely created by those who try to outsmart the market—

It is usually created by those who remain disciplined when others give up.

A Certified Financial Planner (CFP) can help investors build a disciplined strategy designed to survive market volatility and long-term behavioural challenges.

Leave a Reply