Is the Bajaj Allianz Life Smart Pension Plan truly a smart way to secure your retirement — or just another ULIP in disguise?

Is the Bajaj Allianz Life Smart Pension Plan your golden ticket to a worry-free retirement — or a bet on market performance during your golden years?

Can the Bajaj Allianz Life Smart Pension Plan provide the post-retirement peace you’re hoping for — or will market-linked risks steal that comfort?

In this article, we’ll break down the plan, exploring its features, benefits, drawbacks, and provide a detailed illustration to help you decide.

Table of Contents:

What is the Bajaj Allianz Life Smart Pension?

What are the features of the Bajaj Allianz Life Smart Pension?

Who is eligible for the Bajaj Allianz Life Smart Pension?

What are the benefits of the Bajaj Allianz Life Smart Pension?

What are the investment strategies and fund options in the Bajaj Allianz Life Smart Pension?

What are the charges in the Bajaj Allianz Life Smart Pension?

Grace Period, Discontinuance and Revival of the Bajaj Allianz Life Smart Pension

Free Look Period for the Bajaj Allianz Life Smart Pension

Surrendering the Bajaj Allianz Life Smart Pension

What are the advantages of the Bajaj Allianz Life Smart Pension?

What are the disadvantages of the Bajaj Allianz Life Smart Pension?

Research Methodology of Bajaj Allianz Life Smart Pension

Benefit Illustration – IRR Analysis of Bajaj Allianz Life Smart Pension

Bajaj Allianz Life Smart Pension Plan Vs. Other Investments

Bajaj Allianz Life Smart Pension Plan Vs. Pure-term + PPF/Equity Mutual Fund

Final Verdict on Bajaj Allianz Life Smart Pension

What is the Bajaj Allianz Life Smart Pension?

The Bajaj Allianz Life Smart Pension is a Unit-Linked, Non-Participating, Individual Pension Plan. It is designed to help you systematically build your retirement corpus while offering the potential for market-linked growth, along with protection against uncertainties in life.

What are the features of the Bajaj Allianz Life Smart Pension?

- Offers the potential to grow your retirement corpus through market-linked returns.

- Variant 2: Assure includes a Waiver of Premium feature, ensuring the Bajaj Allianz Life Smart Pension Plan policy continues even if the life assured passes away.

- Choose from a variety of fund options tailored to your risk appetite and return expectations.

- Allows partial withdrawals from your retirement corpus during critical life events or medical emergencies.

- Enjoy the freedom to switch between funds anytime, with no extra charges.

- Eligible for tax benefits on premiums paid and benefits received, as per current tax laws.

Who is eligible for the Bajaj Allianz Life Smart Pension?

| Parameter | Variant 1: Classic | Variant 2: Assure |

| Minimum Age at Entry | 18 years | 18 years |

| Maximum Age at Entry | 65 years | 55 years |

| Minimum Age at Vesting | 45 years | 45 years |

| Maximum Age at Vesting | 75 years | 70 years |

| Policy Term (subject to minimum and maximum vesting age) | 10 years to 57 years | 10 to 52 years |

| Premium Payment Term | Single Pay | Limited Pay: 5 years to (Policy Term minus 1) |

| Limited Pay: 5 years to (Policy Term minus 1) | Regular Pay: Equal to Policy Term | |

| Regular Pay: Equal to Policy Term | ||

| Premium Frequency & Minimum Premium | Single Pay: ₹ 20,000 | |

| Limited & Regular Pay: Yearly: ₹ 12,000 | ||

| Half-Yearly: ₹ 6,000 | ||

| Quarterly: ₹ 3,000 | ||

| Monthly: ₹ 1,000 | ||

| Top-up Premium: ₹ 5,000 | ||

| Maximum Premium | As per Board Approved Underwriting Policy (BAUP) | |

What are the benefits of the Bajaj Allianz Life Smart Pension?

1. Vesting Benefit

On survival of life assured till the date of vesting, Fund Value as on the vesting date shall be payable, provided all the due premiums are paid by you and the Bajaj Allianz Life Smart Pension Plan policy is in force.

Options to avail the Vesting Benefit

On the date of vesting, you will have the following options:

- To utilise the entire Vesting Benefit to purchase an immediate annuity or deferred annuity from the Bajaj Allianz at the then prevailing annuity rate. You shall have an option to purchase an immediate annuity or deferred annuity from another insurer at the then prevailing annuity rate, by utilising not more than 50% of the entire proceeds of the policy net of commutation.

- To commute/ withdraw up to 60% of the entire Vesting Benefit and utilise the balance amount to purchase an immediate annuity or deferred annuity from the Bajaj Allianz at the then prevailing annuity rate. You shall have an option to purchase an immediate annuity or a deferred annuity from another insurer at the then prevailing annuity rate, by utilising not more than 50% of the proceeds of the policy net of commutation.

2. Death Benefit

Variant 1: Classic

In the unfortunate event of the death of the life assured during the Bajaj Allianz Life Smart Pension Plan policy term, the nominee shall get: The Higher of:

- Fund Value

- Guaranteed Death Benefit

The policy shall terminate on the date of intimation of the death of the life assured. The proceeds from the policy will be utilised as per the options mentioned in ‘Options to avail Death Benefit’.

Variant 2: Assure

In the unfortunate event of the death of the life assured during the Bajaj Allianz Life Smart Pension Plan policy term, the nominee shall get the Guaranteed Death Benefit as a lump sum immediately on death.

The policy shall continue till the end of the policy term, and the company shall fund all future due premiums after the date of death of the life assured.

At the end of the Bajaj Allianz Life Smart Pension Plan Policy Term, Fund Value shall be payable to the nominee, and the policy terminates. The proceeds from the policy will be utilised as per the options mentioned in ‘Options to avail Death Benefit’.

Options to avail the Death Benefit

The nominee shall have the following options:

- Withdraw the entire proceeds as a lump sum.

- To utilise the entire proceeds or part thereof for purchasing an annuity (immediate or deferred) from the Bajaj Allianz Life at the then prevailing rate.

- Withdraw the proceeds in instalments over a maximum period of five years (Settlement option)

What are the investment strategies and fund options in the Bajaj Allianz Life Smart Pension?

At policy inception, you will have the option to choose any one of the following portfolio strategies:

- Investor Selectable Portfolio Strategy

- Auto Transfer Portfolio Strategy

A. Investor Selectable Portfolio Strategy

This strategy enables you to manage your money actively. Under this strategy, you can choose to save your money in any of the following funds in proportion to your choice.

|

|

|

Asset Allocation |

|

||

|

S.no |

Fund Name |

Equity |

Debt |

Money Market |

Risk profile |

|

1 |

Liquid Pension Fund II |

Nil |

40-100% |

0-60% |

Low |

|

2 |

Bond Pension Fund II |

Nil |

40-100% |

0-60% |

Low |

|

3 |

Asset Allocation Pension Fund II |

40-90% |

0-60% |

0-50% |

Moderate |

|

4 |

Pure Stock Pension Fund II |

75-100% |

0-25% |

0-25% |

High |

|

5 |

Flexi Cap Pension Fund |

85-100% |

0-15% |

0-15% |

High |

|

6 |

Nifty 200 Alpha 30 Index Pension Fund |

85-100% |

0-15% |

0-15% |

High |

|

7 |

Nifty 500 Multifactor 50 Index Pension Fund |

65-100% |

0-35% |

0-35% |

Very High |

|

8 |

BSE 500 Enhanced Value 50 Index Pension Fund |

65-100% |

0-35% |

0-35% |

Very High |

|

9 |

Nifty Alpha 50 Index Pension Fund |

65-100% |

0-35% |

0-35% |

Very High |

|

10 |

BSE 500 Dividend Leaders 50 Index Pension Fund |

65-100% |

0-35% |

0-35% |

Very High |

B. Auto Transfer Portfolio Strategy

This strategy helps you to save your money systematically by automatically switching it every month from low-risk funds (s) to high-risk/moderate-risk funds of your choice. Under this portfolio strategy, you have to choose the following:

- The low-risk fund (i.e. Bond Fund or Liquid Fund) and

- The fund(s) to which the money will be transferred every month

At the start of each month of the Bajaj Allianz Life Smart Pension Plan policy, a proportion of Fund Value in the bond fund and/or liquid fund as on that date will be switched to the other fund/s (available in the product) as specified by you.

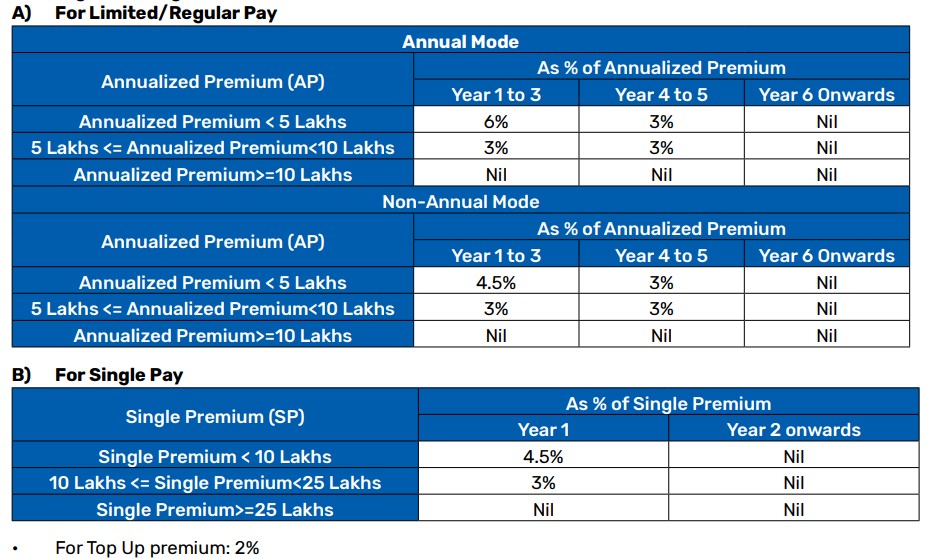

What are the charges in the Bajaj Allianz Life Smart Pension?

i.) Premium Allocation Charge

A certain percentage of each premium will be allocated to purchase units at the prevailing unit price, and the balance shall be taken as Premium Allocation Charge.

ii.) Policy Administration Charge

This charge will be deducted at each monthly anniversary by cancellation of units at the prevailing unit price.

|

|

As a % p.a. of Annualized premium |

||

|

Mode |

1th to 5th year |

6th to 10th year |

11th year onwards |

|

Regular/ Limited pay |

0.175% |

0.250% |

Nil |

|

Annualized Premium< 5Lakhs |

Rs.500 p.m. |

Nil |

|

|

Single Premium< 10 Lakhs |

0.09% |

Nil |

|

|

Single Premium>=10 Lakhs |

Rs.500 p.m. |

Nil |

|

iii.) Fund Management Charge

|

Fund |

Fund Management Charge per annum |

|

Liquid Pension Fund II |

0.95% |

|

Bond Pension Fund II |

0.95% |

|

Asset Allocation Pension Fund II |

1.35% |

|

Pure Stock Pension Fund II |

1.35% |

|

Flexi Cap Pension Fund |

1.35% |

|

Nifty 200 Alpha 30 Index Pension Fund |

1.35% |

|

Nifty 500 Multifactor 50 Index Pension Fund |

1.35% |

|

BSE 500 Enhanced Value 50 Index Pension Fund |

1.35% |

|

Nifty Alpha 50 Index Pension Fund |

1.35% |

|

BSE 500 Dividend Leaders 50 Index Pension Fund |

1.35% |

iv.) Mortality Charge

Mortality Charge will be deducted at each monthly anniversary by cancellation of units at the prevailing unit price. Female Life Assured will be eligible for an age-setback of 3 years.

Mortality charge = Sum at Risk (SAR) multiplied by the applicable mortality rate for the month, based on the attained age of the insured.

v.) Waiver of Premium (WOP) Charge

WOP Charge is only applicable for Variant 2: Assure. This Charge will be deducted at each monthly anniversary by cancellation of units at the prevailing unit price.

vi.) Discontinuance/Surrender Charges

Policy Discontinuance Charges are levied once time on the date of Policy Discontinuation. It depends on the premium amount and, year of discontinuance. There is no Policy Discontinuance Charges from the 5th policy year.

Inference from the charges: These charges act as an overhead cost for investors, something not typically found in other market-linked investment options. Over time, they can significantly erode your overall returns.

Grace Period, Discontinuance and Revival of the Bajaj Allianz Life Smart Pension

Grace Period

A grace period of 30 days for yearly, half-yearly & quarterly Premium payment frequency and 15 days is available for monthly premium payment frequency from the due date of premium payment.

Discontinuance

On Discontinuance of regular/ limited premiums due during the first five (5) policy years: the Regular/Limited Premium Fund Value less the discontinuance/surrender charge, along with Top-Up Premium Fund Value, if any, will be transferred to the Discontinued Pension Policy Fund.

The Fund management charges of the Discontinued Pension Policy Fund will be applicable during this period, and no other charges will be applied. The Discontinuance Value shall be payable as the surrender value at the end of the lock-in period of five (5) policy years.

On Discontinuance of regular/limited premiums due after the lock-in period of five (5) policy years: the policy will be, immediately & automatically, converted to a paid-up policy at the end of the grace period, with risk cover under the base policy to the extent of the paid-up death benefit and without any rider cover, Loyalty Additions, ROAC and Vesting Booster. The paid-up death benefit will be the Guaranteed Death Benefit.

Revival

A discontinued policy can be revived within three (3) years from the date of the first unpaid premium.

Free Look Period for the Bajaj Allianz Life Smart Pension

In the event you disagree with any of the Bajaj Allianz Life Smart Pension Plan policy terms or conditions, or otherwise and have not made any claim, you shall have the option to return the policy within 30 days beginning from the date of receipt of the policy document, whether received electronically or otherwise.

Surrendering the Bajaj Allianz Life Smart Pension

On surrender during the lock-in period of 5 years: The Regular/Limited/Single Premium Fund Value less the discontinuance/surrender charge, plus the Top Up Premium Fund Value, if any, all as on the date of surrender, will be transferred to the Discontinued Pension Policy Fund.

All risk and rider cover (if any) will be terminated immediately. The fund value credited to the Discontinued Pension Policy Fund will continue to be invested in this fund till the end of the lock-in period or the death of the life assured, whichever is earlier.

On surrender after the lock-in period of 5 years: The surrender value available will be Fund Value, if any, as on the date of surrender. The Bajaj Allianz Life Smart Pension Plan policy terminates, and the Fund Value as on the date of surrender must be utilised by you as per the options mentioned in ‘Options to avail Surrender Value’.

Options to avail Surrender Value

You will have the following options:

- To utilise the entire proceeds to purchase an immediate annuity or deferred annuity from the Bajaj Allianz at the then prevailing annuity rate. You shall have an option to purchase an immediate annuity or a deferred annuity from another insurer at the then prevailing annuity rate, by utilising not more than 50% of the proceeds of the policy net of commutation.

- To commute/ withdraw up to 60% of the entire proceeds and utilise the balance amount to purchase immediate annuity or deferred annuity from the Bajaj Allianz Life at the then prevailing annuity rate. You shall have an option to purchase immediate annuity or deferred annuity from another insurer at the then prevailing annuity rate, by utilising not more than 50% of the proceeds of the policy net of commutation

What are the advantages of the Bajaj Allianz Life Smart Pension?

- You can choose to postpone the vesting date of the policy, as long as you are below 60 years of age.

- Partial withdrawals are allowed only after completing 5 policy years.

- Top-Up premiums can be paid anytime during the Bajaj Allianz Life Smart Pension Plan policy term to enhance your investment.

- Flexibility to change your premium payment term based on your evolving needs.

- Option to reduce your premium amount and modify the payment frequency.

- Under the settlement option, the nominee can receive the death benefit in instalments instead of a lump sum.

What are the disadvantages of the Bajaj Allianz Life Smart Pension?

- The plan offers only the vested benefit at the end of the Bajaj Allianz Life Smart Pension Plan policy term.

- The sum assured under the plan is relatively low and may not provide adequate coverage.

- No loan facility is available under this plan.

- There is a 5-year lock-in period for surrender or partial withdrawals, applicable only during the accumulation phase

Research Methodology of Bajaj Allianz Life Smart Pension

The Bajaj Allianz Life Smart Pension Plan allows you to invest in market-linked funds to build your retirement corpus.

However, this accumulated corpus isn’t directly accessible to you—instead, it is used to generate a regular income during your retirement years. Therefore, evaluating the plan’s return potential is essential to gauge its effectiveness.

Benefit Illustration – IRR Analysis of Bajaj Allianz Life Smart Pension

Let’s analyse the Internal Rate of Return (IRR) based on the benefit illustration provided in the policy brochure. A 40-year-old male pays an annual premium of ₹2 lakhs for 10 years under a policy term of 20 years.

The accumulated corpus vests at the end of the policy term, at which point it must be used—either partially or entirely—to purchase an annuity.

| Male | 40 years |

| Sum Assured | ₹ 21,00,000 |

| Policy Term | 20 years |

| Premium Paying Term | 10 years |

| Annualised Premium | ₹ 2,00,000 |

The benefit illustrations provided in the brochure show two scenarios. At 4% p.a. growth, the vesting benefit is ₹31.70 lakhs, resulting in an IRR of 2.99% as per the Bajaj Allianz Life Smart Pension Plan maturity calculator.

At 8% p.a. growth, the vesting benefit is ₹57.23 lakhs, leading to an IRR of 6.89% as per the Bajaj Allianz Life Smart Pension Plan maturity calculator.

| At 4% p.a. | At 8% p.a. | ||||

| Age | Year | Annualised premium / Maturity benefit | Death benefit | Annualised premium / Maturity benefit | Death benefit |

| 40 | 1 | -2,00,000 | 21,00,000 | -2,00,000 | 21,00,000 |

| 41 | 2 | -2,00,000 | 21,00,000 | -2,00,000 | 21,00,000 |

| 42 | 3 | -2,00,000 | 21,00,000 | -2,00,000 | 21,00,000 |

| 43 | 4 | -2,00,000 | 21,00,000 | -2,00,000 | 21,00,000 |

| 44 | 5 | -2,00,000 | 21,00,000 | -2,00,000 | 21,00,000 |

| 45 | 6 | -2,00,000 | 21,00,000 | -2,00,000 | 21,00,000 |

| 46 | 7 | -2,00,000 | 21,00,000 | -2,00,000 | 21,00,000 |

| 47 | 8 | -2,00,000 | 21,00,000 | -2,00,000 | 21,00,000 |

| 48 | 9 | -2,00,000 | 21,00,000 | -2,00,000 | 21,00,000 |

| 49 | 10 | -2,00,000 | 21,00,000 | -2,00,000 | 21,00,000 |

| 50 | 11 | 0 | 21,00,000 | 0 | 21,00,000 |

| 51 | 12 | 0 | 21,00,000 | 0 | 21,00,000 |

| 52 | 13 | 0 | 21,00,000 | 0 | 21,00,000 |

| 53 | 14 | 0 | 21,00,000 | 0 | 21,00,000 |

| 54 | 15 | 0 | 21,00,000 | 0 | 21,00,000 |

| 55 | 16 | 0 | 21,00,000 | 0 | 21,00,000 |

| 56 | 17 | 0 | 21,00,000 | 0 | 21,00,000 |

| 57 | 18 | 0 | 21,00,000 | 0 | 21,00,000 |

| 58 | 19 | 0 | 21,00,000 | 0 | 21,00,000 |

| 59 | 20 | 0 | 21,00,000 | 0 | 21,00,000 |

| 60 | 31,70,685 | 57,23,566 | |||

| IRR | 2.99% | 6.89% | |||

It’s important to note that these returns are not guaranteed. The final fund value is subject to market performance and other influencing factors.

Moreover, the IRRs shown here are notional because the corpus is assumed to be used for annuity purchase, and the actual returns will depend on the annuity rates prevailing at vesting.

According to the brochure, in 4% scenario, the estimated annuity is ₹2.21 lakhs per annum. At 8% scenario, the annuity comes to ₹4.00 lakhs per annum.

However, annuity rates are not fixed, and the usage of the accumulated corpus is restricted, limiting flexibility. These factors make the Bajaj Allianz Life Smart Pension Plan a less attractive investment option when compared to more transparent and flexible retirement planning tools.

Bajaj Allianz Life Smart Pension Plan Vs. Other Investments

The Bajaj Allianz Life Smart Pension Plan places restrictions on how you can utilise your accumulated retirement corpus.

To overcome this limitation, an alternative approach can be considered—one that separates insurance and investment, offering better returns and complete control over your funds.

Bajaj Allianz Life Smart Pension Plan Vs. Pure-term + PPF/Equity Mutual Fund

Let’s take the same example as before: A 40-year-old individual investing ₹2 lakhs annually for 10 years, with a policy term of 20 years. Instead of putting the full amount into a pension plan, the individual can first purchase a pure-term insurance policy with a sum assured of ₹21 lakhs.

This policy costs ₹19,600 annually for a 20-year term with a 10-year premium payment period. This leaves ₹1,80,400 from the annual budget, which can then be invested based on the individual’s risk appetite.

| Pure Term Life Insurance Policy | |

| Sum Assured | ₹ 21,00,000 |

| Policy Term | 20 years |

| Premium Paying Term | 10 years |

| Annualised Premium | ₹ 19,600 |

| Investment | ₹ 1,80,400 |

Risk-averse investors may opt for debt instruments like the Public Provident Fund (PPF), while those with a higher risk tolerance might prefer equity mutual funds.

| Term Insurance + PPF | Term insurance + Equity Mutual Fund | ||||

| Age | Year | Term Insurance premium + PPF | Death benefit | Term Insurance premium + Equity Mutual Fund | Death benefit |

| 40 | 1 | -2,00,000 | 21,00,000 | -2,00,000 | 21,00,000 |

| 41 | 2 | -2,00,000 | 21,00,000 | -2,00,000 | 21,00,000 |

| 42 | 3 | -2,00,000 | 21,00,000 | -2,00,000 | 21,00,000 |

| 43 | 4 | -2,00,000 | 21,00,000 | -2,00,000 | 21,00,000 |

| 44 | 5 | -2,00,000 | 21,00,000 | -2,00,000 | 21,00,000 |

| 45 | 6 | -2,00,000 | 21,00,000 | -2,00,000 | 21,00,000 |

| 46 | 7 | -2,00,000 | 21,00,000 | -2,00,000 | 21,00,000 |

| 47 | 8 | -2,00,000 | 21,00,000 | -2,00,000 | 21,00,000 |

| 48 | 9 | -2,00,000 | 21,00,000 | -2,00,000 | 21,00,000 |

| 49 | 10 | -2,02,500 | 21,00,000 | -2,00,000 | 21,00,000 |

| 50 | 11 | -500 | 21,00,000 | 0 | 21,00,000 |

| 51 | 12 | -500 | 21,00,000 | 0 | 21,00,000 |

| 52 | 13 | -500 | 21,00,000 | 0 | 21,00,000 |

| 53 | 14 | -500 | 21,00,000 | 0 | 21,00,000 |

| 54 | 15 | -500 | 21,00,000 | 0 | 21,00,000 |

| 55 | 16 | 0 | 21,00,000 | 0 | 21,00,000 |

| 56 | 17 | 0 | 21,00,000 | 0 | 21,00,000 |

| 57 | 18 | 0 | 21,00,000 | 0 | 21,00,000 |

| 58 | 19 | 0 | 21,00,000 | 0 | 21,00,000 |

| 59 | 20 | 0 | 21,00,000 | 0 | 21,00,000 |

| 60 | 53,24,637 | 98,76,944 | |||

| IRR | 6.40% | 10.56% | |||

Although the PPF has a yearly investment cap of ₹1.5 lakhs, for illustration purposes, this scenario assumes the full ₹1,80,400 is invested, and minor adjustments can be made to align with the 15-year contribution rule.

After 20 years, the PPF investment grows to ₹53.24 lakhs, delivering an Internal Rate of Return (IRR) of 6.40%.

Though the corpus is lower than the projected corpus under the Bajaj Allianz Life Smart Pension Plan (assuming 8% returns), the real benefit is that the entire maturity amount is available for your use without any restrictions.

| Equity Mutual Fund Tax Calculation | |

| Maturity value after 20 years | 1,10,12,365 |

| Purchase price | 18,04,000 |

| Long-Term Capital Gains | 92,08,365 |

| Exemption limit | 1,25,000 |

| Taxable LTCG | 90,83,365 |

| Tax paid on LTCG | 11,35,421 |

| Maturity value after tax | 98,76,944 |

In contrast, equity mutual funds provide even more impressive results; the corpus grows to ₹1.10 crores over 20 years. After deducting long-term capital gains tax, the post-tax value comes to ₹98.76 lakhs, translating to a post-tax IRR of 10.56%.

This comparison clearly shows that the alternative strategy—combining a term plan with market-based investments—can deliver much better outcomes. It offers not only higher returns but also complete control and flexibility over how and when you access your money.

These advantages are crucial for effective retirement planning, and they are noticeably absent in the Bajaj Allianz Life Smart Pension Plan, which mandates annuity purchases and limits fund usage based on fixed rules and uncertain future rates.

Final Verdict on Bajaj Allianz Life Smart Pension

The Bajaj Allianz Life Smart Pension Plan offers the option to invest your savings in market-linked funds with the objective of building a retirement corpus. However, the accumulated corpus is not fully accessible to you at maturity.

Instead, it must be used—either wholly or in part—to purchase an annuity, subject to the annuity rates prevailing at the time.

While this plan facilitates the accumulation phase by helping you invest regularly, it does not adequately address the distribution phase, where steady post-retirement income is needed and it also has a high agent commission.

Importantly, the plan does not include the annuity product itself, nor does it guarantee the income that will be generated. This lack of clarity leaves investors uncertain about whether the annuity payouts will be sufficient to keep up with rising living expenses and inflation.

In contrast, a more flexible approach would be to invest independently, building a substantial retirement corpus outside of restrictive pension plans.

This corpus can then be strategically allocated across diversified asset classes—such as debt, equity, and hybrid instruments—to generate a regular, inflation-adjusted retirement income.

With proper portfolio rebalancing, you can adapt to changing market conditions and maintain the real value of your income throughout your retirement years.

Starting early in your career plays a vital role in retirement planning. The power of compounding significantly enhances wealth creation over time, making it easier to achieve your financial goals.

Do Quora, Facebook, and Twitter have the final say when it comes to financial advice?

For personalised guidance on estimating your retirement needs and choosing the right investment mix, consulting a Certified Financial Planner (CFP) can be a smart step toward securing your financial future.

Leave a Reply