Can the Canara HSBC IncomeNow Plan truly provide a dependable stream of income, or is it just another insurance product with limited long-term value?

Does the Canara HSBC IncomeNow Plan offer the financial stability you’re looking for, or are there better income-generating alternatives available?

Is the Canara HSBC IncomeNow Plan a smart choice for creating regular income, or do its benefits come with significant trade-offs?

In this article, we take an in-depth look at the Canara HSBC IncomeNow Plan, analysing its features, benefits, drawbacks, and overall suitability to help you make an informed decision.

Table of Contents:

What is the Canara HSBC IncomeNow?

What are the features of the Canara HSBC IncomeNow?

Who is eligible for the Canara HSBC IncomeNow?

What are the plan options in the Canara HSBC IncomeNow?

What are the benefits of the Canara HSBC IncomeNow?

Grace Period, Discontinuance and Revival of the Canara HSBC IncomeNow

Free Look Period for the Canara HSBC IncomeNow

Surrendering the Canara HSBC IncomeNow

What are the advantages of the Canara HSBC IncomeNow?

What are the disadvantages of the Canara HSBC IncomeNow?

Research Methodology of Canara HSBC IncomeNow

Benefit Illustration – IRR Analysis of Canara HSBC IncomeNow

Canara HSBC IncomeNow Vs. Other Investments

Canara HSBC IncomeNow Vs. Pure-term + Equity Mutual Fund

Final Verdict on the Canara HSBC IncomeNow

What is the Canara HSBC IncomeNow?

Canara HSBC IncomeNow is a Non-Linked, Non-Participating, Individual, Life Insurance, Savings cum Protection Plan. This plan combines guaranteed income, life cover and flexibility to help you achieve your goals.

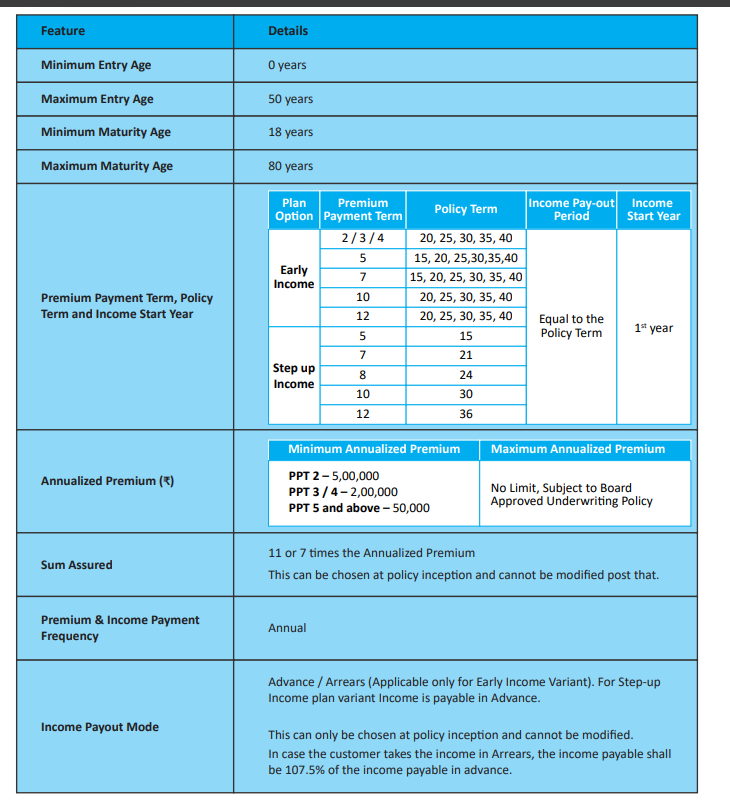

What are the features of the Canara HSBC IncomeNow?

- Guaranteed Maturity Benefit with Early Income: Receive a guaranteed lump-sum payout at policy maturity while enjoying a guaranteed income stream that can begin as early as the first policy month, offering both immediate liquidity and long-term financial security.

- Income That Keeps Pace with Rising Expenses: Choose a guaranteed income option that starts early and increases over time, helping you manage the impact of rising living costs.

- Flexible Life Cover with Higher Income: Opting for a lower life insurance cover can increase your guaranteed income, allowing you to prioritise savings and cash flow based on your financial needs.

- Savings Wallet and Premium Offset Facility: Your guaranteed income can either be accumulated in a Savings Wallet for future planned expenses or emergencies, or used to offset future premium payments, improving flexibility and reducing out-of-pocket premium costs.

- Tax Benefits: Eligible tax benefits may be available under the prevailing provisions of the Income Tax Act in India, subject to the applicable laws at the time.

Who is eligible for the Canara HSBC IncomeNow?

What are the plan options in the Canara HSBC IncomeNow?

Early Income – Start receiving guaranteed income from the very first policy year, paid throughout the Canara HSBC IncomeNow Plan policy term to meet your ongoing needs. Plus, enjoy a lump sum at maturity and comprehensive life cover for complete financial security and peace of mind.

Step-up Income – Start receiving guaranteed income from the very first policy year, with payouts that increase at regular intervals to keep pace with your growing needs. Plus, enjoy a lump-sum maturity benefit and life cover for complete financial security.

What are the benefits of the Canara HSBC IncomeNow?

1. Survival Benefit

Early Income

Survival benefit (i.e. Guaranteed Income as a % of Annualised Premium) shall be payable in advance/arrears (as chosen by You at inception of the policy) from the first policy year till the end of the Canara HSBC IncomeNow Plan Policy Term, provided the Policy is in force, all due premiums have been paid, and the Life Assured is alive on each Guaranteed Income Payout Date.

Step-up Income

Survival Benefit (i.e. Guaranteed Income as a % of Annualized Premium) shall be payable in advance from the first policy year till the end of the Policy Term provided the Canara HSBC IncomeNow Plan Policy is in force, all due premiums have been paid, and the Life Assured is alive on each Guaranteed Income Payout Date.

The Guaranteed Income payable will grow progressively:

- First one-third of the Policy Term (i.e. Premium Payment Term): The payable benefit shall be Guaranteed Income.

- Second one-third of the Policy Term (same tenure as Premium Payment Term): The income payable is enhanced and You shall receive 150% of the Guaranteed Income paid during the Premium Payment Term.

- Final one-third of the Policy Term (same tenure as Premium Payment Term): The income payable will be further enhanced & the income payable will be 200% of the Guaranteed Income paid during the Premium Payment Term.

2. Maturity Benefit

Upon survival till the end of the Policy Term, you will receive a lump-sum maturity benefit along with the balance in the Savings Wallet, if any.

Once these benefits are paid, the Policy Terminates and no further benefits are payable. The maturity benefit shall be payable provided the Canara HSBC IncomeNow Plan policy is in force and all due premiums have been paid.

3. Death Benefit

In the unfortunate event of the death of the Life Assured during the Canara HSBC IncomeNow Plan Policy Term, provided the policy is in force at the time of death, the benefit payable shall be the higher of:

- Sum Assured on Death; or

- Prevailing Surrender Value is payable

Where the Sum Assured on Death is the higher of the Sum Assured or 105% of the Total Premium Paid.

Sum Assured is equal to 11 or 7 times the Annualised Premium, as chosen by you at inception of the Policy.

Additionally, any balance available in the Savings Wallet is also payable along with the Death Benefit.

Grace Period, Discontinuance and Revival of the Canara HSBC IncomeNow

Grace Period

You are provided with a Grace Period of 30 days from the Premium due date to pay due premium due date to pay due premium.

Discontinuance

If at least one (1) full year’s premiums have been paid and subsequent premiums are not paid (i.e. the policy which acquired a surrender value), the policy shall not lapse by reason of the non-payment of future premiums; instead, the policy will be, immediately & automatically, converted to a paid-up policy at the expiry of the grace period.

Revival

You can request the revival of your Canara HSBC IncomeNow Plan policy at any time during the 5-year revival period from the due date of the first unpaid premium.

Free Look Period for the Canara HSBC IncomeNow

If You do not agree with the terms and conditions of the Policy or otherwise have not made any claim, you shall have the option to request for cancellation of the Policy by returning the Policy Document (if issued physically upon request) along with a written request stating the reasons for non-acceptance within the free-look period of 30 days from the date of receipt of the Policy Document, whether received electronically or otherwise (whichever is earlier).

Surrendering the Canara HSBC IncomeNow

You can surrender the policy at any time during the Canara HSBC IncomeNow Plan Policy Term after completion of the first policy year, provided one full year’s premium has been paid.

The Policy will acquire Surrender Value (i.e. both Guaranteed Surrender Value (GSV) and Special Surrender Value (SSV) as follows:

Premium Payment Term of 5 years or more: The GSV and SSV shall become payable after completion of the first policy year, provided one full policy year’s Premium has been received

Premium Payment Term of less than 5 years: The GSV and SSV will become payable immediately on receipt of one full policy year’s Premium.

What are the advantages of the Canara HSBC IncomeNow?

- Savings Wallet Facility: Instead of receiving your guaranteed income immediately, you can accumulate the payouts in a Savings Wallet and withdraw them later to meet future financial needs.

- Premium Offset Option: Use your accumulated income payouts to pay future policy premiums, helping reduce your out-of-pocket premium payments and simplify cash flow management.

- High Premium Incentive: Policies with an annual premium of ₹1,00,000 or more are eligible for a higher premium mark-up, which can enhance the policy benefits.

- Loan Facility: You can avail of a policy loan of up to 80% of the surrender value, subject to the insurer’s terms and conditions.

What are the disadvantages of the Canara HSBC IncomeNow?

- Inadequate Life Cover: The sum assured may not be sufficient to provide adequate financial protection for your family’s long-term needs.

- Reduced Wealth Creation: Regular survival benefit payouts interrupt the power of compounding, limiting the long-term growth potential of your investments.

- Relatively Low Returns: The overall returns offered by the plan are modest and may not compare favourably with other long-term investment options that carry similar or even lower levels of risk.

Research Methodology of Canara HSBC IncomeNow

From a liquidity perspective, the Canara HSBC IncomeNow Plan offers guaranteed annual survival benefits along with a guaranteed maturity payout.

However, to assess its true investment potential, it is important to evaluate the returns using the Internal Rate of Return (IRR) rather than focusing solely on the guaranteed payouts. The following analysis is based on the benefit illustration provided in the policy brochure.

Benefit Illustration – IRR Analysis of Canara HSBC IncomeNow

Consider an example where a 35-year-old male pays an annual premium of ₹1,00,000 for 10 years under the Early Income Option.

The policy has a 25-year term with a sum assured of ₹11 lakhs. Beginning at the end of the first policy year, he receives a guaranteed annual survival benefit of ₹31,300 throughout the payout period.

At the end of the policy term, he also receives a guaranteed lump-sum maturity benefit.

|

Male |

35 years |

| Sum Assured |

₹ 11,00,000 |

|

Policy Term |

25 years |

| Premium Paying Term |

10 years |

|

Annualised Premium |

₹ 1,00,000 |

|

Age |

Year | Annualised premium / Maturity benefit | Death benefit |

| 35 | 1 | -1,00,000 |

11,00,000 |

|

36 |

2 | -68,700 | 11,00,000 |

| 37 | 3 | -68,700 |

11,00,000 |

|

38 |

4 | -68,700 | 11,00,000 |

| 39 | 5 | -68,700 |

11,00,000 |

|

40 |

6 | -68,700 | 11,00,000 |

| 41 | 7 | -68,700 |

11,00,000 |

|

42 |

8 | -68,700 | 11,00,000 |

| 43 | 9 | -68,700 |

11,00,000 |

|

44 |

10 | -68,700 | 11,00,000 |

| 45 | 11 | 31,300 |

11,00,000 |

|

46 |

12 | 31,300 | 11,00,000 |

| 47 | 13 | 31,300 |

11,00,000 |

|

48 |

14 | 31,300 | 11,00,000 |

| 49 | 15 | 31,300 |

11,00,000 |

|

50 |

16 | 31,300 | 11,00,000 |

| 51 | 17 | 31,300 |

11,00,000 |

|

52 |

18 | 31,300 | 11,00,000 |

| 53 | 19 | 31,300 |

11,00,000 |

|

54 |

20 | 31,300 | 11,00,000 |

| 55 | 21 | 31,300 |

11,00,000 |

|

56 |

22 | 31,300 | 11,00,000 |

| 57 | 23 | 31,300 |

11,00,000 |

|

58 |

24 | 31,300 | 11,00,000 |

| 59 | 25 | 31,300 |

11,00,000 |

|

60 |

10,31,300 | ||

| IRR |

4.20% |

Although the benefits are guaranteed, the investment generates an IRR of only 4.20% as per the Canara HSBC IncomeNow Plan maturity calculator over the 25-year policy term. For such a long investment horizon, this return is relatively low.

The annual survival benefit payouts reduce the amount that remains invested, interrupting the power of compounding and limiting the growth of the maturity corpus.

As a result, both the recurring income and the final maturity amount may be inadequate to meaningfully support major long-term financial goals.

Considering its modest returns and limited wealth creation potential, the Canara HSBC IncomeNow Plan may not be an ideal choice for investors seeking long-term capital growth or goal-based financial planning.

Canara HSBC IncomeNow Vs. Other Investments

The Canara HSBC IncomeNow Plan is unlikely to generate returns that outpace inflation over the long term.

Investors seeking better wealth creation and greater financial flexibility may benefit from following the time-tested approach of separating insurance from investments. Let us consider the same assumptions used in the previous illustration.

Canara HSBC IncomeNow Vs. Pure-term + Equity Mutual Fund

Instead of purchasing the IncomeNow Plan, assume a pure term insurance policy with a ₹11 lakh sum assured, costing ₹10,800 per year for 10 years.

From the annual outlay of ₹1,00,000, the remaining ₹89,200 is invested in an equity mutual fund, assuming the investor has the risk appetite for long-term equity investing.

|

Pure Term Life Insurance Policy |

|

|

Sum Assured |

₹ 11,00,000 |

| Policy Term |

25 years |

|

Premium Paying Term |

10 years |

| Annualised Premium |

₹ 10,800 |

|

Investment |

₹ 89,200 |

To replicate the cash flow offered by the Canara HSBC IncomeNow Plan, an annual withdrawal of ₹31,300 is made for 25 years, matching the plan’s guaranteed survival benefit.

At the end of the 25-year period, the remaining corpus is withdrawn as a lump sum, similar to the policy’s maturity benefit.

|

Age |

Year | Term Insurance premium + Equity Mutual Fund | Death benefit |

| 35 | 1 | -68,700 |

11,00,000 |

|

36 |

2 | -68,700 | 11,00,000 |

| 37 | 3 | -68,700 |

11,00,000 |

|

38 |

4 | -68,700 | 11,00,000 |

| 39 | 5 | -68,700 |

11,00,000 |

|

40 |

6 | -68,700 | 11,00,000 |

| 41 | 7 | -68,700 |

11,00,000 |

|

42 |

8 | -68,700 | 11,00,000 |

| 43 | 9 | -68,700 |

11,00,000 |

|

44 |

10 | -68,700 | 11,00,000 |

| 45 | 11 | 31,300 |

11,00,000 |

|

46 |

12 | 31,300 | 11,00,000 |

| 47 | 13 | 31,300 |

11,00,000 |

|

48 |

14 | 31,300 | 11,00,000 |

| 49 | 15 | 31,300 |

11,00,000 |

|

50 |

16 | 31,300 | 11,00,000 |

| 51 | 17 | 31,300 |

11,00,000 |

|

52 |

18 | 31,300 | 11,00,000 |

| 53 | 19 | 31,300 |

11,00,000 |

|

54 |

20 | 31,300 | 11,00,000 |

| 55 | 21 | 31,300 |

11,00,000 |

|

56 |

22 | 31,300 | 11,00,000 |

| 57 | 23 | 31,300 |

11,00,000 |

|

58 |

24 | 31,300 | 11,00,000 |

| 59 | 25 | 31,300 |

11,00,000 |

|

60 |

48,99,501 | ||

| IRR |

10.99% |

For this illustration, capital gains tax is considered only on the final maturity withdrawal, as the annual withdrawals fall within the ₹1.25 lakh annual capital gains exemption applicable under the assumed tax rules.

|

Equity Mutual Fund Tax Calculation |

|

| Maturity value after 25 years |

54,54,144 |

|

Purchase price |

8,92,000 |

| Long-Term Capital Gains |

45,62,144 |

|

Exemption limit |

1,25,000 |

| Taxable LTCG |

44,37,144 |

|

Tax paid on LTCG |

5,54,643 |

| Maturity value after tax |

48,99,501 |

Under these assumptions, the alternate strategy generates an Internal Rate of Return (IRR) of 10.99%, substantially higher than the 4.20% IRR offered by the Canara HSBC IncomeNow Plan.

An additional advantage is flexibility. If the annual withdrawals are not required, the invested corpus continues to compound, resulting in an even larger wealth accumulation over time.

This approach offers higher return potential, better liquidity, and complete control over your investments—advantages that the relatively rigid structure of the Canara HSBC IncomeNow Plan cannot provide.

Final Verdict on the Canara HSBC IncomeNow

The Canara HSBC IncomeNow Plan provides the option of receiving either early income or step-up income, along with a guaranteed lump-sum maturity benefit.

While the assurance of a regular income may appeal to investors seeking an additional cash flow, the plan falls short as a long-term wealth creation tool.

The returns are relatively low, and the life insurance cover offered is unlikely to provide adequate financial protection for most families.

A detailed evaluation reveals that the guaranteed benefits come at the cost of modest returns and limited growth potential. The combination of low life cover and suboptimal investment performance makes the plan less suitable for investors with long-term financial goals.

As a result, it may not be an efficient solution for either wealth accumulation or comprehensive financial security and it also has a high agent commission.

Before investing, it is important to first secure adequate financial protection through a pure term life insurance policy, which offers substantially higher coverage at a much lower cost.

The savings can then be invested in a well-diversified portfolio aligned with your risk appetite, investment horizon, and financial objectives. This approach provides greater flexibility, improved liquidity, and significantly better long-term return potential.

Do Quora, Facebook, and Twitter have the final say when it comes to financial advice?

For a personalised strategy, consider consulting a Certified Financial Planner (CFP).

A CFP can help assess your financial situation, determine the appropriate level of insurance coverage, and build a goal-based investment plan that is tailored to your unique needs, enabling you to achieve long-term financial security with confidence.

Leave a Reply