Do you know your EPF account, through its scheme called EDLI, provides you with the insurance cover up to Rs.6 Lacs??

In this scheme, you don’t have to invest a single dime from your pocket!!

Yes, it is true…

The Government of India has introduced the Employee Deposit Linked Insurance Scheme (EDLI) in 1976. Through this scheme, it is possible to get an adequate insurance cover with the value up to Rs. 6 Lacs!!

All the EPF members will automatically become a member of EDLI.

As you know, the long term security measures are becoming necessary for every individual due to various uncertainties of life in the modern world.

In this article, we will discuss EDLI in greater detail.

Understanding the purpose of EDLI benefits helps employees realise how this EPF insurance cover strengthens long-term financial security.

Table of Contents:

- So, what is EDLI?

- Key Features of the EDLI Scheme

- Contribution of an Employer towards Employee’s EPF account

- Eligibility Criteria to avail EDLI benefits

- Does EDLI Cover Retired Employees?

- How to Claim EDLI Benefits?

- Documents Required for pay-out under EDLI

- Calculation of EDLI Pay-out

- Limitations of the EDLI Scheme – When It Does Not Apply

- Conclusion

1. So, What is EDLI?

The EDLI is an insurance cover provided by the Employees Provident Fund Organisation(EPFO) for all the salaried employees in the private sector, who are members of the EPF scheme.

The limit of the benefit is decided by the last drawn salary of the employee.

EDLI is applicable to all organizations registered under the Employees Provident Fund (EPF) and Miscellaneous Provisions Act, 1952.

All such organizations must subscribe to this scheme and offer life insurance benefits to its employees.

The EDLI scheme works in combination with EPF and EPS.

This makes EDLI a crucial part of the EPF–EPS–EDLI structure, offering a complete package of employee protection under EPFO regulations.

2. Key Features of the EDLI Scheme

i) All the EPF members are automatically enrolled in an EDLI Scheme.

ii) All employees with a “Basic Salary+DA” equal to or under Rs. 15,000/- per month can avail the benefits of the EDLI Scheme.

iii) In case the “Basic Salary + DA” goes above Rs. 15,000 per month, the maximum benefit is capped at Rs.6,00,000/-. The detailed calculation will be described in the later section.

iv) All the Insurance benefits under the EDLI Scheme can be availed by the family members, nominee or the legal heirs of the EDLI member.

v) There is no minimum service period for availing the EDLI benefits.

vi) An employee doesn’t need to contribute any amount to EDLI. The entire contribution to EDLI is to be made by the employer and no hidden fee can be deducted from the employee’s salary.

vii) Maximum contribution of the employer towards EDLI is capped at Rs. 75 per month.

viii) There is an additional bonus of Rs.1,50,000/- available under the EDLI.

ix) An employer can opt for another group insurance scheme, but the benefits offered must be equal to or more than those offered under EDLI.

x) The claim amount under ELDI is 30 times the average monthly salary (Basic Pay + DA) in the past 12 months.

Many employees also check the “EDLI contribution rate” or “EDLI charges”, but remember that employees pay nothing—only the employer contributes 0.5%.

These features highlight how the EDLI scheme advantages give employees automatic life coverage without any personal contribution.

3. Contribution of an Employer towards Employee’s EPF account

As mentioned earlier, the EDLI corpus is maintained entirely by an employer.

0.5% of your ‘Basic Pay + DA’ will be deposited to your EDLI account by the employer.

The prime objective of the EDLI scheme is to offer financial security to the family members of the policy-holder.

EDLI Scheme is transferable with any change in the job. The new employer will continue to make payments on the existing account, defined under a single UAN.

For more insights and clarity on your EPF Account, you can read this Comprehensive guide on EPF. Here you will learn all the features and benefits of your EPF account.

This employer contribution is what many refer to as “EDLI in salary”, though it does not reduce the employee’s take-home salary.

The role of employers under EDLI ensures that workers continue receiving coverage even during job changes through the unified UAN system.

4. Eligibility Criteria to avail EDLI benefits

Following persons are eligible to apply for claiming insurance benefits under the EDLI Scheme:

- Members of the family (Nominees) nominated under the EPF Scheme.

- In case of no nomination, the members of the family including spouse and children less than 25 years of age will avail the EDLI benefits.

- In case, the deceased has no family and no nomination, legal heir will receive EDLI benefits based on the family situation of the EDLI member.

- Guardian of a minor nominee/family member/legal heir

These eligibility rules ensure that EDLI insurance benefits always reach the rightful dependent or legal heir without complications.

5.Does EDLI Cover Retired Employees?

The Employees’ Deposit Linked Insurance (EDLI) benefit is designed exclusively for active members of the EPF and EPFO-linked establishments, which means the insurance protection remains valid only as long as the employee is in active service.

Once a person retires and stops contributing to EPF, the EDLI coverage also stops automatically, because the scheme is directly linked to monthly PF contributions made by the employer.

This is why EDLI does not provide life insurance coverage after retirement, even though the member may continue receiving benefits from the EPS-95 pension scheme.

To remain eligible for EDLI benefits in death cases, a member must have been employed in an EPF-covered organization at the time of death or must have contributed to EPF in the 12 months immediately preceding the date of death.

For families, it becomes important to understand that EDLI eligibility arises only when the member was active under the PF system; once service ends, the employer’s EDLI contribution also comes to an end, making the employee ineligible for the insurance pay-out.

This is why individuals considering retirement should explore separate life insurance coverage, as EDLI cannot function as a replacement beyond the period of employment.

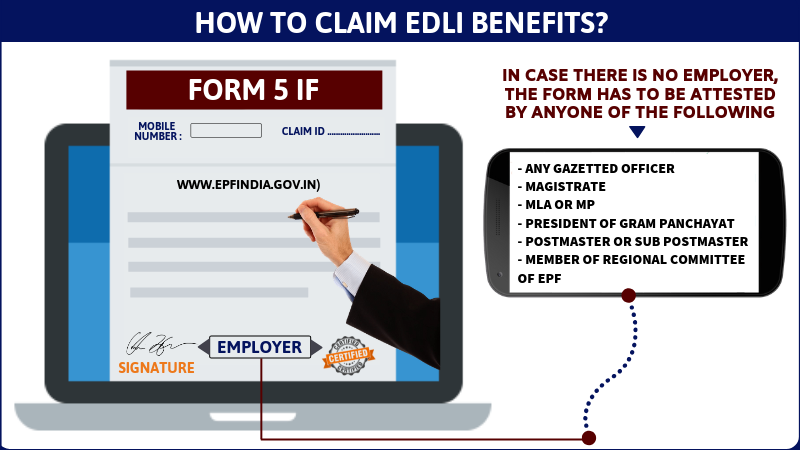

6. How to Claim EDLI Benefits?

Those who are eligible to avail EDLI benefits, as discussed in the above section has to fill the Form 5 IF, to get the insurance benefits after the death of the EDLI member.

The claim form has to be signed and certified by the employer.

In case there is no employer, the form has to be attested by anyone of the following:

- Any Gazetted Officer

- Magistrate

- MLA or MP

- Bank Manager (where the account was maintained)

- President of Gram Panchayat

- Chairman / Secretary / Member of Municipal or District Local Board

- Postmaster or Sub Postmaster

- Member of Regional Committee of EPF

➥ Form 5 IF can be filled along with the Form 20 towards EPF withdrawal claim in case of the deceased member.

➥ Form 5 IF can also be filled with Form 10C/Form10D to claim benefits of all the three schemes (EPF, EPS, and EDLI) in one go.

The claimant must submit all the documents along with the completed form to the regional EPF Commissioner’s Office for processing of the claim.

Any additional documents required by the authority must be furnished at earliest to process the claim.

Once all the documents are provided and the claim is accepted, the EPF commissioner must settle the claim within 30 days from the receipt of the claim.

Otherwise, the claimant is entitled to interest @12% p.a. Till the date of actual disbursal.

This smooth claim process reflects the EPFO’s streamlined EDLI settlement system, which ensures timely financial support to families.

7. Documents Required for pay-out under EDLI

The claimant has to submit the following documents along with the Form 5 IF to get the amount disbursed under the EDLI scheme:

- Death Certificate of the member

- Guardianship certificate if the claim on behalf of a minor family member/nominee/legal heir is by other than the natural guardian.

- Succession certificate in case of a claim by the legal heir.

- Copy of a cancelled cheque of the bank account in which the payment has opted.

- In case the member was last employed in the establishment exempted under the EPF Scheme 1952, the employer of such establishment should furnish the PF details of last 12 months under the Certificate part and also send an attested copy of the Member’s Nomination Form.

Keeping these documents ready helps families complete the EDLI claim documentation without delays.

8. Calculation of EDLI Pay-out

The nominee will receive the EDLI pay-out in the event of the death of an EDLI member. Insurance amount at pay-out is calculated as shown below:

[Average Monthly Salary of an Employee for the last 12 months] x 30 + Bonus Amount of ₹ 1,50,000/-]

Therefore, the insurance amount that the nominee of a deceased member gets is calculated as 30 times the average monthly salary in the last 12 months of employment, plus a bonus amount of up to ₹1,50,000 is also paid to the claimant under this scheme. The maximum average monthly salary is capped at ₹15,000/-

If the average monthly salary of an employee is ₹ 15,000

So, 30 times the salary will be 30 x ₹ 15,000 = ₹ 4,50,000

After adding the bonus of ₹1,50,000, the amount will become ₹6,00,000/-

Thus, the total amount payable under this scheme to the beneficiary is ₹ 6,00,000/-

This formula ensures that the EDLI pay-out calculation remains fair and directly linked to the employee’s last drawn salary.

9.Limitations of the EDLI Scheme – When It Does Not Apply

While the EDLI scheme offers valuable financial protection, there are several important situations where it does not apply, and employees often remain unaware of these exclusions.

The scheme is only available to EPF members, which means workers who are not enrolled in EPF or whose employers do not contribute correctly are automatically left out.

In addition, EDLI benefits cannot be claimed if the employee’s EPF account has been fully withdrawn before death, or if the member was not actively employed at the time of death.

Another practical limitation is that EDLI does not cover deaths due to natural disasters, accidents outside employment, or health-related causes in a special way—it provides the same flat structure, regardless of the cause of death.

The scheme also becomes ineffective when an employer opts for a Group Insurance Scheme (GIS) that offers equal or better coverage than EDLI, meaning EDLI will not pay out in such cases.

Furthermore, the benefit amount, capped by the statutory maximum, does not increase with inflation, making the financial support inadequate for many families today.

10. Conclusion

So, we hope that the above article has given you clear insights into the EDLI Scheme.

EPF is an excellent scheme which provides you with the Pension benefits through its EPS Scheme, and insurance benefits through its EDLI Scheme, without your single penny of investment in EPS or EDLI.

If you have any further queries on EDLI Scheme, feel free to post them below, in the comment section.

Understanding your EPF and EDLI benefits empowers you to secure your family’s future with confidence under the EPFO framework.

Sir, I have one questions that when I get the EDLI benefit (If I die while working in the office or when I will die in my house) both are applicable for EDLI benefit.

Partha Majumder

Kolkata

The nominee or the legal heir can claim within 30 days from the receipt of the claim.

GOOD SCHEME

Thank you for sharing your feedback!