Beginning around the age of 60 or 65. The retirement phase marks a transition from full-time work to relying on savings and investments for expenses.

A stable income source is vital for a comfortable lifestyle during retirement, and many opt for Fixed Deposits (FDs) due to their simplicity, fixed payouts, and convenience. Is it enough? This article delves into alternative investment strategies beyond FDs to enhance the effective management of the retirement corpus for a more comfortable post-retirement life.

Let’s begin!

Table of Contents

1.What is a Smart Investment?

2. Assumptions for the workings

3. The Four Scenarios

A Scenario 1: ₹ 1 Crore in Fixed Deposit

B. Scenario 2: ₹ 1 Crore in Debt Mutual Fund (SWP)

C. Scenario 3: Equity (60): Debt (40)

D. Scenario 4: ₹ 1 Crore in Equity Mutual Fund

4. Conclusion

1. What is a Smart Retirement Investment?

Many retirees fall into the trap of opting for investment vehicles that promise predictable returns. Given their reduced or non-existent regular income, they prioritize options with low risk. Can these returns adequately cover expenses like food, healthcare, and leisure activities?

The retirement corpus, which is the result of years of hard work, needs to be managed carefully to ensure it lasts throughout our retirement. Which investment options can effectively achieve this objective?

Let’s analyze four distinct scenarios with illustrations to gain a clearer understanding.

2. Assumptions For The Workings

- Accumulated retirement corpus – ₹ 1 Crore.

- Retirement Age – 60 Years

- Life Expectancy – 85 Years

- Initial Living Expenses – ₹ 6 Lakhs per annum

- Inflation – 6% p.a.

- FD interest – 7% p.a.

- Equity Mutual Fund (CAGR) – 12% p.a.

- Debt Mutual Fund (CAGR) – 7%

- The tax liability is assumed as nil, since under the new tax regime, a resident individual with taxable income up to Rs. 7,00,000 can avail of a rebate of Rs. 25,000 or the amount of tax payable, whichever is lower.

3.The Four Scenarios

Scenario 1: ₹ 1 Crore in Fixed Deposit

Assume you invest a corpus of ₹ 1 crore in a Fixed deposit scheme and earn a regular income of 7%. This will earn you ₹ 7 Lakhs per annum. Assume you have an annual expense of ₹ 6 Lakhs per annum. And inflation is 6% p.a.

| Scenario 1 | Fixed Deposit |

| Retirement Corpus | 1,00,00,000 |

| Interest Rate | 7% p.a. |

| Annual Income | 7,00,000 |

| Initial Annual Expense | 6,00,000 |

| Inflation | 6% p.a. |

| Year | Opening Balance | Interest Income | Annual Expenses | Surplus / Deficit | Closing balance |

| 1 | 1,00,00,000 | 7,00,000 | 6,00,000 | 1,00,000 | 1,00,00,000 |

| 2 | 1,00,00,000 | 7,00,000 | 6,36,000 | 64,000 | 1,00,00,000 |

| 3 | 1,00,00,000 | 7,00,000 | 6,74,160 | 25,840 | 1,00,00,000 |

| 4 | 1,00,00,000 | 7,00,000 | 7,14,610 | -14,610 | 1,00,00,000 |

| 5 | 1,00,00,000 | 7,00,000 | 7,57,486 | -57,486 | 1,00,00,000 |

| 6 | 1,00,00,000 | 7,00,000 | 8,02,935 | -1,02,935 | 1,00,00,000 |

| 7 | 1,00,00,000 | 7,00,000 | 8,51,111 | -1,51,111 | 1,00,00,000 |

| 8 | 1,00,00,000 | 7,00,000 | 9,02,178 | -2,02,178 | 1,00,00,000 |

| 9 | 1,00,00,000 | 7,00,000 | 9,56,309 | -2,56,309 | 1,00,00,000 |

| 10 | 1,00,00,000 | 7,00,000 | 10,13,687 | -3,13,687 | 1,00,00,000 |

| 11 | 1,00,00,000 | 7,00,000 | 10,74,509 | -3,74,509 | 1,00,00,000 |

| 12 | 1,00,00,000 | 7,00,000 | 11,38,979 | -4,38,979 | 1,00,00,000 |

| 13 | 1,00,00,000 | 7,00,000 | 12,07,318 | -5,07,318 | 1,00,00,000 |

| 14 | 1,00,00,000 | 7,00,000 | 12,79,757 | -5,79,757 | 1,00,00,000 |

| 15 | 1,00,00,000 | 7,00,000 | 13,56,542 | -6,56,542 | 1,00,00,000 |

| 16 | 1,00,00,000 | 7,00,000 | 14,37,935 | -7,37,935 | 1,00,00,000 |

| 17 | 1,00,00,000 | 7,00,000 | 15,24,211 | -8,24,211 | 1,00,00,000 |

| 18 | 1,00,00,000 | 7,00,000 | 16,15,664 | -9,15,664 | 1,00,00,000 |

| 19 | 1,00,00,000 | 7,00,000 | 17,12,603 | -10,12,603 | 1,00,00,000 |

| 20 | 1,00,00,000 | 7,00,000 | 18,15,360 | -11,15,360 | 1,00,00,000 |

| 21 | 1,00,00,000 | 7,00,000 | 19,24,281 | -12,24,281 | 1,00,00,000 |

| 22 | 1,00,00,000 | 7,00,000 | 20,39,738 | -13,39,738 | 1,00,00,000 |

| 23 | 1,00,00,000 | 7,00,000 | 21,62,122 | -14,62,122 | 1,00,00,000 |

| 24 | 1,00,00,000 | 7,00,000 | 22,91,850 | -15,91,850 | 1,00,00,000 |

| 25 | 1,00,00,000 | 7,00,000 | 24,29,361 | -17,29,361 | 1,00,00,000 |

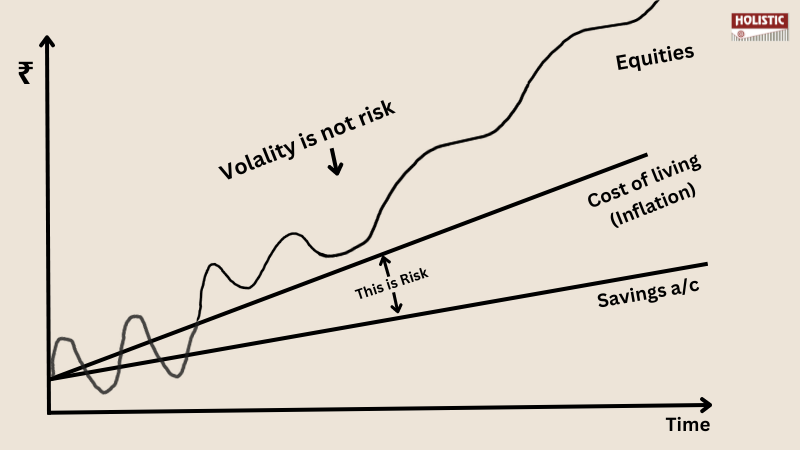

You will be happy during the initial years as the annual income will cover your expenses. But your expectations are shattered down the lane because due to inflation the expenses keep on rising but on the other hand your income is fixed!

Fixed deposits typically yield interest rates of 7% to 8% per year. Central banks adjust these rates as part of their monetary policy, and such changes directly influence the returns from fixed deposits.

What does this teach us?

Fixed deposit often fails to preserve the purchasing power of your funds!

The hard fact is that you cannot combat inflation with Fixed deposits in the long run!

Scenario 2: ₹ 1 Crore in Debt Mutual Fund (SWP)

Systematic Withdrawal Plan (SWP) allows investors to withdraw a fixed amount of money at regular intervals from their mutual fund investment. Let’s assume ₹ 1 Crore is invested in a Debt Mutual fund.

| Scenario 2 | Debt Mutual Fund SWP option |

| Retirement Corpus | 1,00,00,000 |

| CAGR | 7% |

| Initial Annual Expense | 6,00,000 |

| Inflation | 6% |

In SWP, you get the advantage of adjusting the withdrawal based on your needs. To meet your rising expenses, you can increase your annual withdrawal.

| Age | Year | Opening Balance | Interest Income | Annual Expenses | Surplus / Deficit | Closing balance |

| 61 | 1 | 1,00,00,000 | 7,00,000 | 6,00,000 | 1,00,000 | 1,01,00,000 |

| 62 | 2 | 1,01,00,000 | 7,07,000 | 6,36,000 | 71,000 | 1,01,71,000 |

| 63 | 3 | 1,01,71,000 | 7,11,970 | 6,74,160 | 37,810 | 1,02,08,810 |

| 64 | 4 | 1,02,08,810 | 7,14,617 | 7,14,610 | 7 | 1,02,08,817 |

| 65 | 5 | 1,02,08,817 | 7,14,617 | 7,57,486 | -42,869 | 1,01,65,948 |

| 66 | 6 | 1,01,65,948 | 7,11,616 | 8,02,935 | -91,319 | 1,00,74,629 |

| 67 | 7 | 1,00,74,629 | 7,05,224 | 8,51,111 | -1,45,887 | 99,28,742 |

| 68 | 8 | 99,28,742 | 6,95,012 | 9,02,178 | -2,07,166 | 97,21,575 |

| 69 | 9 | 97,21,575 | 6,80,510 | 9,56,309 | -2,75,799 | 94,45,777 |

| 70 | 10 | 94,45,777 | 6,61,204 | 10,13,687 | -3,52,483 | 90,93,294 |

| 71 | 11 | 90,93,294 | 6,36,531 | 10,74,509 | -4,37,978 | 86,55,316 |

| 72 | 12 | 86,55,316 | 6,05,872 | 11,38,979 | -5,33,107 | 81,22,209 |

| 73 | 13 | 81,22,209 | 5,68,555 | 12,07,318 | -6,38,763 | 74,83,446 |

| 74 | 14 | 74,83,446 | 5,23,841 | 12,79,757 | -7,55,916 | 67,27,530 |

| 75 | 15 | 67,27,530 | 4,70,927 | 13,56,542 | -8,85,615 | 58,41,915 |

| 76 | 16 | 58,41,915 | 4,08,934 | 14,37,935 | -10,29,001 | 48,12,914 |

| 77 | 17 | 48,12,914 | 3,36,904 | 15,24,211 | -11,87,307 | 36,25,607 |

| 78 | 18 | 36,25,607 | 2,53,792 | 16,15,664 | -13,61,871 | 22,63,735 |

| 79 | 19 | 22,63,735 | 1,58,461 | 17,12,603 | -15,54,142 | 7,09,593 |

| 80 | 20 | 7,09,593 | 49,672 | 18,15,360 | -17,65,688 | -10,56,095 |

| 81 | 21 | -10,56,095 | -73,927 | 19,24,281 | -19,98,208 | -30,54,303 |

| 82 | 22 | -30,54,303 | -2,13,801 | 20,39,738 | -22,53,539 | -53,07,842 |

| 83 | 23 | -53,07,842 | -3,71,549 | 21,62,122 | -25,33,671 | -78,41,513 |

| 84 | 24 | -78,41,513 | -5,48,906 | 22,91,850 | -28,40,756 | -1,06,82,269 |

| 85 | 25 | -1,06,82,269 | -7,47,759 | 24,29,361 | -31,77,120 | -1,38,59,389 |

If the annual income is not sufficient to meet your expenses, then your capital starts depleting. The deficit is funded by your capital. Here, from the 5th year, the deficit gets adjusted by the Debt-opening balance.

Though you get inflation-adjusted income, your capital exhausts at the age of 80. A well-crafted retirement plan will make your retirement corpus sustainable for your lifetime. What’s the point in beating inflation if the corpus can’t withstand till your lifetime?

Debt Mutual funds can withstand and combat inflation to some extent. Sustaining the corpus till your lifetime is the major hurdle here. So, this scenario neither suits retirees.

Scenario 3: Equity (60): Debt (40)

₹ 60 Lakhs in Equity Mutual Fund

₹ 40 Lakhs in Debt Mutual Fund (SWP)

You split your retirement corpus into two buckets. While the debt portion offers regular income, the equity portion can provide higher returns over the long term, helping to offset inflation and maintain purchasing power.

| Scenario 3 | Equity: Debt |

| Retirement corpus | 1,00,00000 |

| Equity | 60,00,000 |

| Debt | 40,00,000 |

| Equity Return | 12% p.a. |

| Debt Return | 7% p.a. |

| Inflation | 6% p.a. |

40% in any debt mutual funds. They offer a guaranteed return of around 7% per annum. Invest the balance 60% of the corpus in equity mutual funds, which can yield around 12% p.a. Though they are dynamic in the short-term, the chance of capital appreciation is high in the long run.

Debt portion, allows you to withdraw in accordance to the rising expenses. Meanwhile, the equity portion appreciates in value. Similar to scenario 2, over some time your debt bucket exhausts. Whenever the debt portion is depleted, it is reimbursed from the equity portion.

In this scenario, every 6 years, 60 Lakhs are moved from equity to debt. This will fund your regular income needs. At the age of 78, the equity balance is fully shifted to debt. Under this scenario, your corpus outlives you.

The splitting of funds between equity and debt and also the shifting of funds (rebalancing) between equity and debt can be designed based on your personal risk tolerance. The given scenario is just an illustration. You can modify it based on your personal preferences.

This investment strategy,

- Offer regular income

- Protects the purchasing power of income

- The corpus outlives you

The best option for retirees is a perfect mix of different assets, adjusted regularly to match personal preferences, as shown in the above scenario.

Scenario 4: ₹ 1 Crore in Equity Mutual Fund

In the earlier scenario, equity mutual funds augmented your retirement income. The allocation of equity in the portfolio allows it to withstand inflation in the later years. In this scenario, the corpus is parked entirely in an equity mutual fund.

| Scenario 4 | Equity Mutual Fund SWP option |

| Retirement Corpus | 1,00,00,000 |

| CAGR | 12% p.a. |

| Initial Annual Expense | 6,00,000 |

Unlike fixed-income investments such as fixed deposits, equities do not guarantee the return of your initial investment. Equity markets are known for their volatility, which means that the value of your investment can fluctuate significantly over short periods. For the illustrative purpose the, annual growth is assumed as 12% p.a.

| Age | Year | Opening Balance | Yearly withdrawal | Closing Balance |

| 61 | 1 | 1,00,00,000 | 6,00,000 | 1,05,28,000 |

| 62 | 2 | 1,05,28,000 | 6,36,000 | 1,10,79,040 |

| 63 | 3 | 1,10,79,040 | 6,74,160 | 1,16,53,466 |

| 64 | 4 | 1,16,53,466 | 7,14,610 | 1,22,51,519 |

| 65 | 5 | 1,22,51,519 | 7,57,486 | 1,28,73,316 |

| 66 | 6 | 1,28,73,316 | 8,02,935 | 1,35,18,827 |

| 67 | 7 | 1,35,18,827 | 8,51,111 | 1,41,87,841 |

| 68 | 8 | 1,41,87,841 | 9,02,178 | 1,48,79,943 |

| 69 | 9 | 1,48,79,943 | 9,56,309 | 1,55,94,470 |

| 70 | 10 | 1,55,94,470 | 10,13,687 | 1,63,30,476 |

| 71 | 11 | 1,63,30,476 | 10,74,509 | 1,70,86,684 |

| 72 | 12 | 1,70,86,684 | 11,38,979 | 1,78,61,429 |

| 73 | 13 | 1,78,61,429 | 12,07,318 | 1,86,52,605 |

| 74 | 14 | 1,86,52,605 | 12,79,757 | 1,94,57,590 |

| 75 | 15 | 1,94,57,590 | 13,56,542 | 2,02,73,173 |

| 76 | 16 | 2,02,73,173 | 14,37,935 | 2,10,95,466 |

| 77 | 17 | 2,10,95,466 | 15,24,211 | 2,19,19,806 |

| 78 | 18 | 2,19,19,806 | 16,15,664 | 2,27,40,640 |

| 79 | 19 | 2,27,40,640 | 17,12,603 | 2,35,51,400 |

| 80 | 20 | 2,35,51,400 | 18,15,360 | 2,43,44,366 |

| 81 | 21 | 2,43,44,366 | 19,24,281 | 2,51,10,494 |

| 82 | 22 | 2,51,10,494 | 20,39,738 | 2,58,39,247 |

| 83 | 23 | 2,58,39,247 | 21,62,122 | 2,65,18,379 |

| 84 | 24 | 2,65,18,379 | 22,91,850 | 2,71,33,713 |

| 85 | 25 | 2,71,33,713 | 24,29,361 | 2,76,68,875 |

The above table depicts the equity growth over a long period. Despite the annual withdrawal, the growth is so rapid due to the compounding effect.

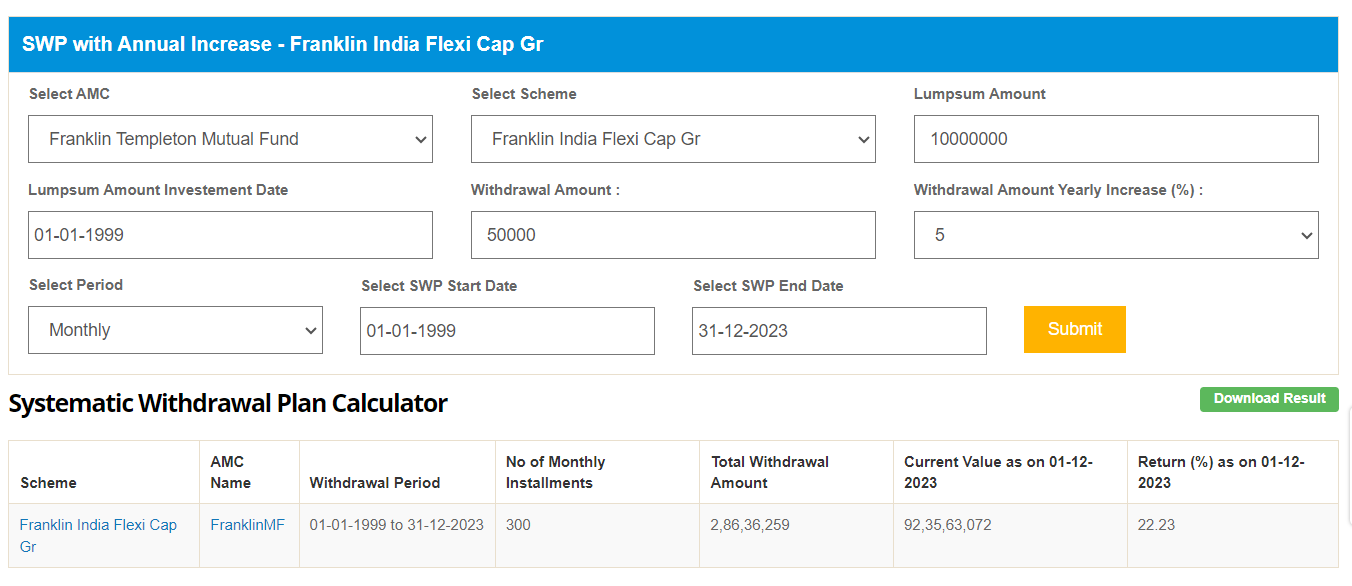

Now let us work out the calculation with real-time NAV. For calculation purposes, we have chosen the Franklin India Flexi Cap Fund.

| Lump Sum Investment | ₹ 1 Crore |

| Monthly SWP | ₹ 50,000 |

| Inflation (Annual Step-up) | 5% |

| Fund name | Franklin India Flexi cap |

Your retirement corpus of ₹ 1 crore is invested in the Franklin India Flexicap Fund. In the first year you withdraw ₹ 50,000 per month to manage the annual expenses of ₹ 6 Lakhs. Thereafter to combat inflation, the annual withdrawal is stepped up by 5%.

The period of withdrawal starts from the year 1999 to 2023. The final maturity value after 25 years is ₹ 92.35 crores. The CAGR for this scenario is 22.23%.

Courtesy: AdvisorKhoj

Parking your entire retirement corpus in the equity asset class can have several disadvantages, primarily related to the higher level of risk associated with equities. Following a market downturn, it may take a significant amount of time for equity markets to recover. A prolonged recovery period could impact your ability to meet your retirement income needs.

While equities have the potential to outpace inflation over the long term, there is no guarantee of returns every year. The volatility of equity markets can cause psychological stress and anxiety, especially for retirees.

Due to the higher level of risk, this scenario is not an advisable option. Moreover, practically this is not a viable option.

Conclusion

To conclude, Fixed income instruments offer safety and stability. But they may not be the one-stop solution for your regular income, especially in environments of low interest rates. As a result, retirees may need to explore alternative investment strategies to maximize their income potential while managing risk effectively during retirement.

To mitigate the risks, retirees need to diversify their investment portfolio across different asset classes, viz. equities and fixed income. Diversification can help spread risk and reduce the impact of market fluctuations on your retirement corpus. The calculation part reveals that Scenario 3 is the most suitable option for retirees where asset allocation and rebalancing strategies are employed.

Retirees need to carefully assess their risk tolerance, income needs, and investment goals before pursuing any alternative investment strategy. Please don’t get misled by information on social media platforms like Quora, Facebook, Twitter, etc. Consulting with a financial advisor can provide personalized guidance and help you develop a retirement investment strategy that aligns with your risk tolerance and financial goals.

Leave a Reply