For decades, retirement planning in India followed a predictable script.

Work for 30–35 years.

Save diligently.

Retire with a lump sum and depend on fixed income sources.

But that script no longer works.

Today, the real challenge isn’t just building a retirement corpus—it’s ensuring that your money lasts as long as you do.

Because here’s the uncomfortable truth:

Running out of money in retirement is a far bigger risk than not saving enough.

So, once you’ve accumulated your savings, the most critical question becomes:

How should you withdraw your money to create a steady, tax-efficient income?

Table of Contents:

- The Changing Reality of Retirement in India

- Building a Corpus Is Only Half the Job

- The Big Question: How Should You Withdraw Your Money?

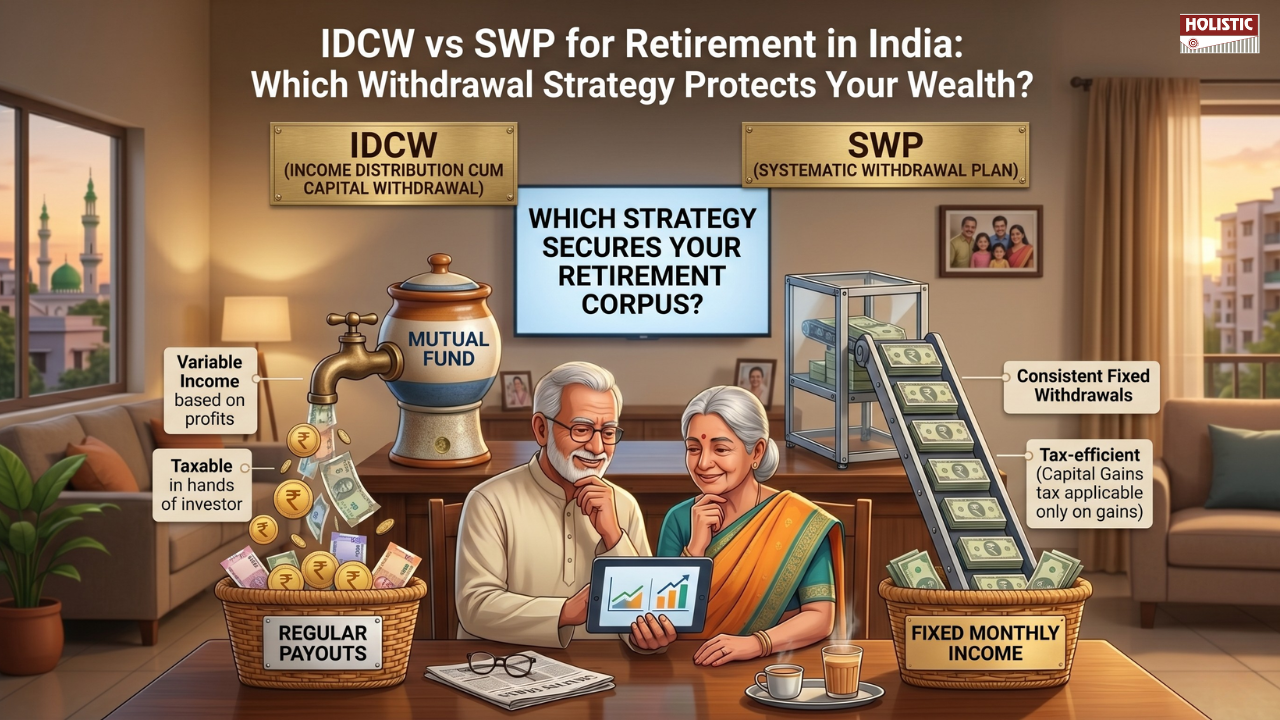

- What is IDCW and How Does It Work?

- The Limitations of IDCW for Retirement Income

- What is SWP and Why Is It Gaining Popularity?

- SWP vs IDCW: A Clear Tax Comparison

- Why Tax Efficiency Can Make or Break Your Retirement Plan

- Creating a Sustainable Monthly Income Strategy

- The Importance of Asset Allocation in Retirement

- A Sample ₹1 Crore Retirement Portfolio

- How to Generate Monthly Income Without Stress

- The 4 Pillars of a Strong Retirement Plan

- Common Mistakes Retirees Must Avoid

- Final Thoughts: Choosing the Right Withdrawal Strategy

The Changing Reality of Retirement in India

A generation ago, retirees had multiple safety nets:

- Government pensions

- Joint family support

- Lower cost of living

- Limited lifestyle expectations

Today, most of these have disappeared.

Instead, retirees face:

- Rising inflation

- Increasing healthcare costs

- Longer life expectancy

- Greater financial independence

Even a ₹1 Crore retirement corpus, which once seemed sufficient, now raises a serious concern:

Will this money last for the next 20–25 years?

Building a Corpus Is Only Half the Job

Let’s assume you’ve done everything right.

You’ve accumulated ₹1 Crore by the time you retire.

That’s a significant achievement.

But now comes the harder part—turning that lump sum into a predictable monthly income.

Suppose your monthly expense is ₹60,000.

That’s ₹7.2 lakh annually.

Now the question becomes:

How do you withdraw this amount without depleting your savings too quickly or paying unnecessary taxes?

This is where the debate between IDCW vs SWP for retirement becomes crucial.

The Big Question: How Should You Withdraw Your Money?

If your retirement corpus is invested in mutual funds, you typically have two withdrawal options:

- IDCW (Income Distribution cum Capital Withdrawal)

- SWP (Systematic Withdrawal Plan)

At first glance, both seem similar.

Both provide cash flow.

Both can be used to generate income.

But under the surface, they work very differently—and the impact on your wealth can be substantial.

What is IDCW and How Does It Work?

IDCW, formerly known as the dividend option, is when a mutual fund distributes a portion of its profits to investors.

Sounds simple, right?

The fund earns profits → distributes them → you receive income.

But here’s what many investors overlook.

The pay-out is not guaranteed.

The timing is uncertain.

And most importantly:

The entire amount you receive is treated as taxable income.

The Limitations of IDCW for Retirement Income

IDCW may appear attractive because it feels like “passive income.”

But it comes with several drawbacks:

i. Unpredictable Cash Flow

Fund houses decide when and how much to distribute. What happens if markets underperform? Your income may stop or reduce significantly.

ii. Tax Inefficiency

The entire pay-out is added to your income and taxed as per your slab rate.

If you fall in the 30% tax bracket, a large portion of your income goes straight to taxes.

iii. Lack of Control

You have no say in the withdrawal amount or frequency.

For retirees who depend on stable income, this unpredictability can be problematic.

What is SWP and Why Is It Gaining Popularity?

A Systematic Withdrawal Plan (SWP) allows you to withdraw a fixed amount from your investment at regular intervals—usually monthly.

Unlike IDCW, SWP gives you control.

You decide:

- How much to withdraw

- When to withdraw

- How long to continue

But the real advantage lies in taxation.

When you withdraw via SWP, the amount consists of:

- Your invested capital (principal)

- Your gains (returns)

You are taxed only on the gains, not the entire withdrawal.

SWP vs IDCW: A Clear Tax Comparison

Let’s break it down with a simple example.

You withdraw ₹60,000 per month.

IDCW Scenario

- Entire ₹60,000 is taxable

- At a 30% tax slab → ₹18,000 goes as tax

SWP Scenario

- Assume ₹45,000 is principal and ₹15,000 is gain

- Only ₹15,000 is taxable

- Long-term capital gains up to ₹1.25 lakh annually are tax-free

Result?

Your tax liability could be close to zero.

That’s a massive difference over 20–25 years.

Why Tax Efficiency Can Make or Break Your Retirement Plan

In retirement, every rupee matters.

High taxes can silently erode your wealth over time.

Many retirees unknowingly choose options like IDCW or fixed deposits because they seem simple.

But simplicity often comes at a cost.

A tax-inefficient strategy can reduce your effective income significantly—forcing you to withdraw more and deplete your corpus faster.

Creating a Sustainable Monthly Income Strategy

A well-designed retirement income plan doesn’t rely on a single source.

Instead, it combines multiple streams to balance stability, growth, and liquidity.

Think of it as building a financial ecosystem rather than depending on one instrument.

The Importance of Asset Allocation in Retirement

Putting your entire ₹1 Crore into one asset class is risky.

Whether it’s:

- Fixed deposits

- Real estate

- Gold

- Equity

Overexposure to any single asset can create imbalances.

Diversification helps:

- Reduce risk

- Improve stability

- Ensure consistent income

A Sample ₹1 Crore Retirement Portfolio

Here’s a practical allocation approach:

- ₹30 lakhs in Fixed Deposits and Debt Funds (stability)

- ₹10 lakhs in Gold and REITs (diversification)

- ₹60 lakhs in Equity Mutual Funds (growth)

This structure balances safety with long-term growth.

How to Generate Monthly Income Without Stress

With the above portfolio, your ₹60,000 monthly income can be structured as:

- ₹40,000 from SWP in equity funds

- ₹15,000 from debt instruments and FD interest

- ₹5,000 from gold/REITs

Instead of relying on one source, you spread the risk.

And more importantly:

You maintain control.

The 4 Pillars of a Strong Retirement Plan

1. Inflation Protection

Your expenses will rise over time. Equity exposure helps your portfolio grow faster than inflation.

2. Longevity Planning

People are living longer. Your money needs to last longer too.

3. Emergency Fund

Keep 6–12 months of expenses in liquid instruments for unexpected situations.

4. Regular Review

Your retirement plan isn’t static. Review it annually and adjust withdrawals if needed.

Common Mistakes Retirees Must Avoid

- Relying only on fixed deposits

- Ignoring tax implications

- Withdrawing too much too early

- Not adjusting for inflation

- Avoiding equity completely

Each of these mistakes can shorten the lifespan of your retirement corpus.

Final Thoughts: Choosing the Right Withdrawal Strategy

Retirement planning doesn’t end when you accumulate wealth.

That’s where it truly begins.

The way you withdraw your money determines:

- How long your savings last?

- How much tax you pay

- How comfortable your lifestyle remains?

Between IDCW and SWP, the difference isn’t just technical—it’s transformational.

Because one gives you income.

The other gives you control, efficiency, and sustainability.

And in retirement, that makes all the difference.

A Certified Financial Planner (CFP) can help structure a tax-efficient withdrawal strategy tailored to your retirement goals.

Leave a Reply