“A good financial plan is a ‘roadmap’ that shows us exactly how the choices we make today will affect our future.” – Alexa Von Tobel

Everyone dreams to have a stable financial life charted out. The problem arises when the dreamers are more than the planners.

Most of us would have splurged a lot in our 20s or wouldn’t have felt the need to save.

It’s when our late 30’s or early 40’s seem to be nearing. We start worrying about saving for our future.

This is where timely financial planning for 40 year olds in India becomes critical.

If you fall anywhere between this category. No need to worry, you still have the time to catch up.

Before starting the process of Financial Planning, it’s important to review the last 10 years of your life.

Let’s do a simple exercise:

- How will you rate the last 10 years of your financial life?

- Do you think you could’ve saved enough over the years?

- What healthy money habits do you wish you had cultivated over the years?

- Do you think you should’ve started investing early?

- What percentage of your portfolio has beaten inflation?

- What mistake do you think you could’ve handled better while dealing with your finances?

- Have you started planning financially for your retirement?

- What do you think you could’ve avoided in your financial planning?

- What do you think has worked best so far in your personal finance?

The question, “How to become financially stable in your late 30s and early 40s?” might even make you anxious thinking about your Financial Future.

If you’re wondering where should I be financially at 35, now is the time to find out.

It’s definitely overwhelming to sit down and plan for your financially secure future.

As there is a plethora of resources available on the Internet, it’s normal to get confused.

But let us go through a simplified process of your financial planning especially when you start to financially plan in your 30s & 40s.

This is your comprehensive financial planning guide—suitable whether you’re 35 or 45.

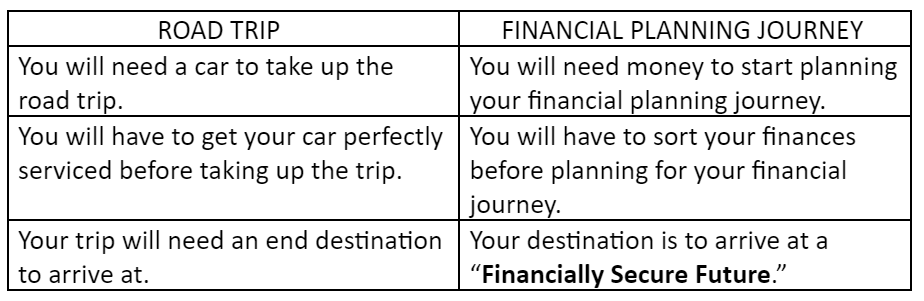

Financial planning is very much like taking a road trip

Let’s understand how both could be similar:

Now, to help you navigate this path full of ups and downs. You will need a road map.

If you feel you started your financial journey without a road map and got lost…

No need to worry!!!

Because no matter how far you are into the journey, it’s always possible to course correct.

At this stage, identifying your financial goals by 35 and reassessing your risk profile becomes essential.

Building a clear investment portfolio for a 35-year-old in India helps set the tone for wealth creation while balancing stability.

Table of Contents:

1.How to Assess Your Financial Health in Your 30s–40s.

2.Handling your Savings Efficiently in your 30s – 40s.

3.Build an Emergency Fund in your 30s – 40s.

4.Planning for your Children’s Education in your 30s – 40s.

5.Risks of Property Investment in your 30s – 40s.

6.Seek the help of a Financial Planner.

7. Select the Right Investment Avenues in your 30s-40s:

8.Planning your Retirement in your 30s – 40s.

1).How to Assess Your Financial Health in Your 30s–40s

Before you dive into planning, it’s important to pause and evaluate where you currently stand financially.

Think of this as taking a quick pit stop before resuming your journey — it helps you refuel, recalibrate, and realign your goals.

Start by calculating your net worth — subtract your total liabilities (like loans and EMIs) from your total assets (like savings, investments, and property).

A positive and growing net worth each year indicates that you’re on the right track.

Next, review your savings rate. Ideally, you should be saving at least 20–30% of your monthly income.

If your expenses are eating into your savings, it’s time to rework your budget or cut back on non-essentials.

Pay attention to your debt-to-income ratio.

If your loan EMIs take up more than 30% of your monthly income, your financial flexibility may be limited.

Try to repay high-interest debts first to free up cash flow.

Also, ensure that you have a sufficient emergency fund.

A minimum of 3 to 6 months’ worth of expenses should be parked in liquid instruments such as savings accounts or liquid mutual funds — accessible, yet not easily spent.

Don’t forget insurance. A solid term plan (10–15 times your annual income) and health cover (₹5–10 lakh for a family) are essential safety nets that protect your long-term goals.

Lastly, look at your investment diversification.

Are you overly dependent on one type of asset, like real estate or gold?

A healthy mix of equity, debt, and other instruments ensures stability and growth.

Reassess your finances every year — update your goals, track your progress, and adjust your investments accordingly.

This simple step can make your financial roadmap for your 30s and 40s more structured and resilient.

2). Handling your Savings Efficiently in your 30s – 40s:

A trip is something that would constantly bombard you with unexpected expenses such as sudden hunger pangs even if you just finished lunch or one of your tires might get punctured. It may not always be under your control.

Just like how in life, you might have to deal with sudden job loss, accidents, natural disasters, etc…. and leave you with expenses you never anticipated in the first place.

As much as it’s hard to think about certain situations, we still need to assess if your family would be able to sustain itself financially if you as the breadwinner of the house died.

This is why it’s more than important to have a savings fund you can rely on.

This step becomes especially crucial in financial planning for 45-year-olds who may have higher dependents and lower risk appetite.

First, you need to create a cash flow table to analyse your expenses from your income. The next step is to start saving immediately.

Initially, you could invest your savings in fixed-income securities to have assured liquid able investments as a way to keep your life rolling even under emergencies.

As you move toward your 40s, aim to allocate funds across diversified asset classes — equity, debt, and hybrid funds — to achieve an ideal investment portfolio for a 40-year-old in India that balances safety and growth.

To ease with you the process, you can download our “Investible Surplus Calculator” in which you can analyse your expenses and income to figure out your surplus.

You can use this calculation to invest when starting your investment journey in your late 30s or your early 40s.

This tool complements age-wise financial planning strategies, whether you’re just starting or playing catch-up.

Make a Budget

This helps you to narrow down on your expenses, see where your expenditure is high. This way you can streamline your expenses and can reduce them in the long run.

Example: Paying bills on time, using public transport, shopping during sale period, budgeting your grocery needs.

These small steps matter immensely in financial planning for families in India, especially when juggling multiple responsibilities.

A good benchmark is to save at least 30% of your income by your mid-30s and channel it into long-term goals such as retirement or your child’s education.

This ensures your financial goals by 35 are well on track.

What sort of an investor are you?

You need to answer this question before we move ahead – What sort of an investor are you?

Investing = Income – Expenses

Income – Investing = Expenses

If you are investing after spending, then you are not a disciplined investor. Most probably, you have not decided your goal. You need to sit, prioritise your goals and start investing.

This is often the case with individuals beginning financial planning for 30 year olds in India, where impulsive spending precedes goal-based investing.

If you are investing before spending, you seem to be a disciplined investor. There are chances that you may also not have prioritised your goals.

This approach aligns better with building a holistic financial plan and achieving your long-term goals.

By your 40s, your focus should shift toward consolidating assets and ensuring your financial planning for 40-year-olds in India includes adequate insurance, retirement corpus growth, and estate planning.

3). Building an Emergency Fund in your 30s – 40s:

With the rise of the Internet, so has the rise of Internet banking. Even for a cup of chai, we tend to transfer money through the Internet.

Imagine being somewhere on a road trip without an internet connection? or eating somewhere where they only accept liquid cash?

For emergencies like this, we tend to keep a few loose changes in our pockets. Your emergency fund requires the same function but it needs to be worth more than a few loose changes.

Ideally, your emergency fund needs to consist of cash that could cover at least 6 months’ worth of expenses.

This is a must-have step in financial planning for low income households too, not just for high earners.

Creating an emergency corpus is the foundation of a strong financial plan at 35 or 40, especially for those balancing home loans, education expenses, and long-term savings.

You can keep this fund in liquid funds, short-term deposits, or a separate savings account to maintain liquidity and safety.

If you’re a salaried professional in your 30s or 40s, emergency fund planning should precede all forms of wealth creation or equity investment.

You should regularly distribute your income under expenses and savings. Your savings need to be categorized into various financial goals you see fit.

But your emergency fund should not be touched under any circumstance except in an emergency.

Maintaining a dedicated emergency corpus also helps you avoid taking high-interest personal loans or credit card debt, ensuring financial stability even during uncertain times.

4). Planning for your Children’s Education in your 30s – 40s:

Our children are growing up in a world where expectations different from yours are placed on them. It’s no longer adequate to be a degree holder.

Our children need to have double degrees and various skills to display on their resumes. Even that seems to fall short at times.

So, saving up for their education which might be more expensive in the future than in the present is crucial.

Growing up, they might also develop an interest in different niches and express a desire to study abroad.

If you’re looking at financial goals before 40, your child’s future education should top that list.

So, it’s more than necessary that you chart a financial plan that includes saving for your children’s future higher education and making sure you have made wise investments to back up their choices.

Just like when you go on a trip along with your kids, you will definitely plan something additional to accommodate their needs.

In the same way, you also need to additionally plan for your kid’s financial future and you need to put extra care while planning especially when you are starting to plan your children’s education in your late 30s or your early 40s

Start early by investing in child education mutual funds, SIPs, or goal-based investments that align with inflation and long-term growth.

If your goal is international education, explore options such as hybrid equity funds or equity savings schemes for tax efficiency and capital appreciation.

Financial planning for 40-year-olds in India often includes child-centric investments like Sukanya Samriddhi Yojana or Public Provident Fund for long-term safety.

5). Risks of Property Investment in your 30s – 40s:

Many people initially buy out a property somewhere that’s worth a huge amount of corpus. It’s a wise decision if they are going to be living there.

But due to what their career demands, they might be living someplace far away.

The property might be sitting somewhere idle and even if it gave out rental income, it still isn’t a sustainable investment in the long run.

Think about how much money would be spent on maintenance of the property, and taxes all for a small rental yield.

Instead, if the money was deposited in equity funds, the amount of surplus would’ve doubled in the long run.

This analysis is key in deciding the ideal investment portfolio for 45 year-olds in India where liquidity and compounding matter more than ownership.

A property might seem like a lucrative investment but mostly it springs up expenses you would not even have expected in the first place.

You can watch our video on “Is real estate a good investment?” To better understand its risks.

When comparing property vs mutual funds, remember that equity savings funds and hybrid funds often deliver higher liquidity and lower maintenance costs.

Avoid over-leveraging or depending entirely on real estate; diversify through equity savings, debt instruments, or low-risk mutual funds instead.

For individuals doing financial planning at 40, prioritizing liquidity over illiquid assets like property ensures flexibility during emergencies.

6). Seek the help of a Financial Planner:

While planning for a trip, we sought the help of a travel consultant. Especially if we are going somewhere we’ve never been before.

To help us book the cheapest flights at the ideal time and also to book hotels where they provide complimentary breakfast along with other customer service benefits which we could utilize to our utmost benefit, a travel consultant is the best choice to seek help from.

In the same way, an experienced financial planner with expertise in the field of finance will not only help you save money.

But will also help you take appropriate decisions concerning the financial goals you want to achieve in your late 30s and early 40s which will help you in the long run.

From setting financial goals for 35 year olds to building retirement readiness at 45, a financial planner adds clarity and structure to your journey.

A road trip is not about how fast you reach your destination instead it’s about how memorable your trip was. In the same way, a financial Planner will help your financial journey to become easier and to go smoothly.

Hiring a Financial Planner to plan and manage your Investment Portfolio in your late 30s or your early 40s will help you take off the stress of Financial Planning from your shoulders and help you relax about your Financial Future.

This is especially valuable if you’re unsure about your investment portfolio for 35-year-old or you’re just starting out with holistic financial planning.

A certified financial planner can help you choose between equity savings funds vs arbitrage funds, depending on your risk tolerance and time horizon.

They can also structure your portfolio for better tax efficiency and inflation-adjusted returns.

If you are planning for long-term goals like retirement or your child’s marriage, professional advice ensures your financial roadmap stays realistic and disciplined.

In financial planning for 40-year-olds in India, expert advice bridges the gap between short-term stability and long-term wealth creation.

7). Select the Right Investment Avenues in your 30s-40s:

what are the investment avenues for you also depends upon whether you are a?

- High-risk taker

- Moderate risk taker

- Low-risk taker

It also depends on the time period for which you want to invest.

- For short-term goals (up to 1 year) like paying off a personal loan, sending kids to school and so on – Auto Sweep Facility, Fixed Deposits etc. are better avenues.

- Medium-term goals (up to 5 years) like buying a car, down payment for your home, going for a vacation etc. – the investment avenues are Recurring Deposits, Debt Mutual Funds etc.

- For long-term goals (10-15 years) like children’s education, marriage, retirement etc., Mutual Funds, PPF, and other debt avenues are better choices.

For tax savings purpose, you can also invest in ELSS Mutual Funds.

At this stage, understanding the difference between investment products like equity savings funds vs arbitrage funds becomes essential to align your goals with your risk profile.

While equity savings funds combine debt, arbitrage, and equity components for balanced growth, arbitrage funds exploit short-term market inefficiencies for relatively stable, tax-efficient returns.

If you prefer safer short-term investments, arbitrage funds may be ideal, while long-term investors may consider hybrid or balanced advantage funds for better capital appreciation.

When comparing equity savings fund taxation vs arbitrage fund taxation, note that both qualify as equity-oriented funds and enjoy favourable capital gains tax treatment when held for over one year.

How much amount is required for your short, medium and long-term goals is a big question?

You need to calculate each goal in their current value and then add inflation rate to it.

A recommended starting point is using the ‘100–age’ or ‘120–age’ rule as a baseline for equity allocation, particularly relevant in financial planning for 35-year-olds and 45-year-olds in India

You can also diversify across asset classes such as gold ETFs, government securities, and debt mutual funds to balance volatility and ensure inflation-adjusted growth.

For investors looking for low-risk, tax-efficient options, equity savings schemes and arbitrage funds often outperform traditional fixed deposits over time.

This strategic mix is key to achieving both capital safety and long-term wealth accumulation in your late 30s and early 40s.

8). Planning your Retirement in your 30s – 40s:

Retirement planning should also come under your overall financial planning. Imagine coming home after a trip with no resources or a plan to set your life forward.

Your retirement planning is to decide what to do after the trip ends.

When you start accumulating money for your long-term financial goals in your late 30s or your early 40s such as for your retirement, you can start to keep a higher equity exposure to achieve your ideal retirement.

You might be worried about the certain risks involved in investing a significant portion of your money in stocks but you will still be able to get a higher return than what you would’ve probably got by investing in fixed-income securities.

Industry-standard advice recommends gradually reducing equity exposure over time, such as allocating 55–60% equities and the balance in debt by your mid-40s balanced with risk tolerance

Retirement planning for 40-year-olds in India must focus on long-term compounding through SIPs in diversified equity funds while ensuring liquidity through debt instruments.

Those nearing retirement can consider balanced advantage funds or equity savings funds to reduce volatility while maintaining equity exposure.

Remember, the earlier you begin, the smaller your monthly investment required to build a ₹1 crore or ₹2 crore retirement corpus.

Tax-efficient investment options like NPS (National Pension System), PPF, and ELSS mutual funds can further enhance post-retirement income stability.

Equity in Your Retirement Portfolio:

Equity investments are perfect for long-term financial goals as Warren Buffet rightly said,

“If you aren’t willing to own a stock for 10 years,

Don’t even think about owning it for 10 minutes.”

In your sunset years, having a well-diversified portfolio yielding you better returns helps you completely enjoy and relax.

As you near your retirement age, it would be a wise move to transfer at least 70% of your portfolio to fixed-income securities by reducing your equity exposure to 30%. As this will help in rolling out a steady income which will also be able to provide you with inflation-beating returns.

At the end of the journey, a financially secure future would become a reality.

Being disciplined while sticking to your financial plan along with patiently moving forward with it would yield better results than you can imagine.

Your goal‐adjusted asset allocation should also consider that risk tolerance decreases with age; this calls for gradual rebalancing toward debt instruments over time

In your 30s, focus on aggressive equity exposure through index funds or large-cap mutual funds.

As you move into your 40s, gradually shift toward hybrid or arbitrage funds to preserve capital.

If you’re aiming for tax efficiency in your post-retirement years, consider investments in tax-free bonds or debt mutual funds with indexation benefits.

Retirement Example Calculation for Your 30s-40s:

With most of the people working in private sectors, there are no pension benefits available. Our EPFs also get consumed in most of the cases when we switch jobs.

How should we save for our retirement so that we are able to lead a decent lifestyle without being dependent on our children?

Let us assume my current age is 35, I want to retire at 55 and my life expectancy is 75 years and investment returns after retirement is 2%.

Expenses after retirement per month = Rs. 30,000 (according to current value)

Value of Rs. 30,000 after 20 years (assuming 6% inflation) = Rs. 96,000

You will require Rs. 1.9 Cr. at the time of retirement to ensure the same standard of living.

To accumulate this amount, you need to start investing Rs. 20,000 per month if your investment returns are 12% CAGR.

Now your asset allocation at the age of 35 can be 70% equity but it needs to be changed over a period of time and at the time of retirement, ideally, 70% allocation should be towards the debt instruments.

This calculation highlights the importance of compounding and early investing—beginning your SIPs or mutual fund investments at 35 drastically reduces the financial pressure at 50.

Including products like equity savings funds in your retirement plan can provide consistent returns with lower volatility than pure equity funds.

Common Financial Mistakes to Avoid in Your 30s and 40s

Your 30s and 40s are the most crucial decades to build wealth.

However, small missteps made during this period can cost you heavily later. Here are a few common mistakes to steer clear of:

- Delaying Investments: Waiting for the “right time” to invest means losing out on the power of compounding. Even small, consistent SIPs started early can make a huge difference.

- Not Having an Emergency Fund: Life is unpredictable — job loss, health issues, or sudden expenses can derail your goals if you don’t have a safety cushion.

- Living Beyond Your Means: Lifestyle inflation grows with income. Keep your expenses in check and avoid unnecessary EMIs or credit card debt.

- Ignoring Retirement Planning: Many assume retirement planning can wait. The truth? The earlier you start, the less you need to save each month.

- Lack of Insurance: Skipping life or health insurance exposes your family to financial stress during emergencies. It’s a must-have, not an option.

- Neglecting Tax Planning: Poor tax management reduces your take-home returns. Use tax-saving investments like ELSS, PPF, or NPS efficiently.

- Emotional Investing: Following market trends or tips without proper research can lead to heavy losses. Always align your investments with your risk profile and goals.

Avoiding these pitfalls ensures your financial plan stays strong, sustainable, and future-ready — no matter where you are in your 30s or 40s.

Re-assess your financial plan in Your 30s-40s

Now, take some time to re-assess your financial plan?

- How do you plan to implement your financial goals into becoming a reality?

- Do you have debts? How are you planning to become debt-free?

- How are you planning to save to reach your financial goals?

- How do you want the next 10 years of your financial life to be?

- What is your plan to have an inflation-beating return?

- What is your ideal retirement lifestyle? How do you plan to achieve that?

- How are you planning to go about your financial planning moving forward?

This Comprehensive Financial Planning Guide designed for 35 to 45 years old will help you customize and structure your Investment strategies best suited to execute in your late 30s to early 40s.

To help you ease your process of financial planning in your late 30s or your early 40s, we are happy to provide you with our “Net worth calculator”.

You can easily calculate your assets along with adjusting your liabilities to determine your net worth.

This will help you periodically review your net worth which in turn helps you plan your finances accordingly.

You can also use a SIP calculator or retirement corpus calculator to visualize how small monthly investments can lead to wealth creation over time.

Monitoring your portfolio performance every 6–12 months ensures that your investment mix remains aligned with your evolving financial goals.

For tailor-made outcomes, it’s a wise decision to seek the help of a financial planner who can customize a financial plan according to your financial goals.

If you are wondering where to approach a financial planner? Holistic has got you covered. Reach out to us if you think using professional strategies would help you yield great results.

Register on the below link to avail our 30 minutes’ complimentary financial consultation and get your doubts cleared by experienced professionals.

Leave a Reply