HDFC Click 2 Protect 3-D Plus is a popular Term Insurance plan by HDFC Life Insurance. In this policy, the 3D are Death, Disability and Disease; policy ensures the protection against these 3Ds.

In this post, we will review this policy and analyze whether this policy is a good fit for you?

Also, we will explore each plan option in greater detail and will help you to choose the best suitable one.

Let’s discover HDFC Life Click-2-Protect 3-D Plus.

Key features

- This policy gives the protection against 3 Ds, that is, Death, Disability, and Disease. It simply means that the basic life cover is inbuilt with accidental and critical illness riders.

- It provides 9 different plan options, you can choose anyone based on your requirement. They have features shown in the figure below. We will discuss each of them in detail in the later sections in this post.

- You can get the whole life cover in the Life long protection and 3D Life Long Protection option.

- All the future premiums are waived off on Accidental Total Permanent Disability (inbuilt with all 9 options) and on the diagnosis of Critical Illness (available under 3D Life option and 3D Life long protection option).

- This policy offers special premium rates for female policyholders and non-tobacco users.

- Life stage protection feature offers to increase the insurance cover on certain key milestones (such as child-birth) without medicals.

- Flexibility to increase your cover every year through top-up options. This option can be exercised only at the policy inception.

- The policy offers a 30-Days Free Look period.

- Tax Benefits on the premiums and the pay-outs under Section 80C and 10(10D) of the Income Tax Act.

Basic Eligibility

HDFC Life Click 2 Protect 3D Plus: Illustration

In this example, we will explore the benefits of all the 9 options. We will calculate the premium amount you need to pay in all 9 options. Then we will also do a detailed analysis of the shortlisted options in the next section.

Let’s say Mr. X is 30 years old (male and non-smoker) and choosing life cover Rs. 1 Crore. His premium payment term will be 30 years, and in case of whole life options, the premium payment term will be 35 years (refer eligibility criteria shown in the previous section).

- Accidental permanent disability cover is chosen as Rs 10 Lacs for the policy term.

Note: you can make of this Online Calculator for the premium calculations customized for your needs.

If he chooses to pay the premiums annually/monthly with the cover of Rs. 1 Crore, and he wants lumpsum payouts from the policy. Mr. X will be provided by the 4 options described below:

You can also watch HDFC Life Click 2 Protect 3-D Plus vlog post below

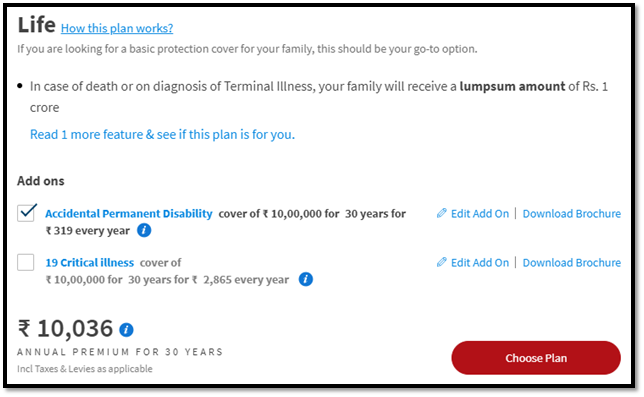

Life Option:

Snapshot shown below is taken from HDFC Life Click 2 Protect 3D Plus online calculator. As you can see that Mr. X has to pay the annual premium of Rs. 10,036/-

Below are the benefits Mr. X will get under the Life option:

- In case of death or on the diagnosis of Terminal Illness, the family of Mr. X will receive a lumpsum amount of Rs. 1 crore.

- In case of an accident leading to permanent disability, all the future premium payments will be waived off.

There is an option to pay Rs. 319 per annum for Accidental Permanent Disability rider for the cover amount of Rs. 10 Lacs for 30 years. If you don’t need it, you have the flexibility to opt-out of this add-on.

There is an option to pay Rs. 319 per annum for Accidental Permanent Disability rider for the cover amount of Rs. 10 Lacs for 30 years. If you don’t need it, you have the flexibility to opt-out of this add-on.

Also, there is an additional option to choose the cover for 19 critical illnesses. The amount of the cover will be Rs. 10 Lacs and you have to pay Rs. 2,865/- p.a. along with your premium to get its benefit. But should you opt for it?

We will give our analysis in the next section.

The image shown below highlights the 19 critical illnesses.

3D Life Option

In this case, Mr. X has to pay the premium amount of Rs. 10,453 per annum. And, below are the benefits he will get in this option:

- In situations when Mr. X falls ill of any of the 34 critical illnesses, all the future premium payments will be waived off for him.

- In case of death or on the diagnosis of Terminal Illness, the family of Mr. X will receive a lumpsum amount of Rs. 1 crore.

- In case of an accident leading to permanent disability, all the future premium payments will be waived off.

Below is the image showing 34 critical illnesses covered in the 3D Life option:

Extra Life Option:

In this case, Mr. X has to pay the annual premium of Rs. 15,835/- and below are the benefits he will get:

- In case of death due to an accident, the family of Mr. X will receive the chosen additional amount of Rs. 1 Crore. This is the unique feature of this option.

- In case of death or on the diagnosis of Terminal Illness, the family of Mr. X will receive a lumpsum amount of Rs. 1 crore.

- In case of an accident leading to permanent disability, all the future premium payments will be waived off.

Return of Premium Option:

This is a unique option in this policy. Here, Mr. X has to pay the annual premium of Rs. 25,287 and below are the benefits he will get:

- He will get back all the premiums he has paid, in case of survival at the end of the policy term.

- In case of death or on the diagnosis of Terminal Illness, the family of Mr. X will receive a lumpsum amount of Rs. 1 crore.

- In case of an accident leading to permanent disability, all the future premium payments will be waived off.

Now, which option out of above 4 will be more suitable for you? It seems difficult to decide with the first look, we will do a detailed analysis of each benefit is clubbed with the above 4 options.

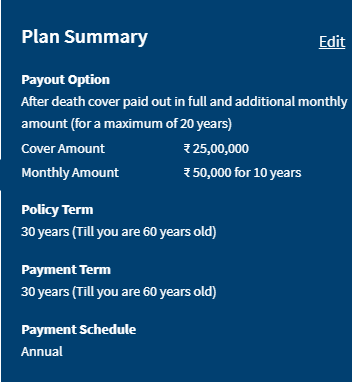

If you choose your payouts to be “Lumpsum + Monthly”, you will be provided with the 2 options described below:

Let’s say Mr. X is choosing Rs. 25 Lacs as a lumpsum payment and Rs. 50,000 as a monthly income for a period of 10 years, all the considered parameters are shown below

Income Option

In this case, Mr. X has to pay the annual premium of Rs. 8,485/- and below are the benefits he will get:

- In case of death or on the diagnosis of Terminal Illness, the family of Mr. X will receive a lumpsum amount of Rs. 25 Lacs.

- Along with a lumpsum amount of Rs. 25 Lacs, the family of Mr. X will also receive the regular monthly income of Rs 50,000 for a period of 10 years. You also have an option to increase this monthly income annually (up to 10% to ensure your family keeps pace with inflation).

- In case of an accident leading to permanent disability, all the future premium payments will be waived off.

Extra Life income option

It has all the same features as the Income option, the extra added feature is the cover for accidental death.

- In case of death due to an accident, the family of Mr. X will receive an additional amount of Rs. 25 Lacs as the lump sum and the monthly amount of Rs. 50,000.

In this option, he needs to pay the premium of Rs. 12,943 annually.

In case there is no death due to an accident, it works the same as the Income option.

Now, let’s say Mr. X choose ‘only monthly’ income payout option. Other details are shown below:

Income Replacement Option

Mr. X is 30 years old, if he dies when he is 50 years, then his family will receive the lump sum amount of Rs.6 Lacs – which is 12 times the monthly income for his family, he has opted for. (in this case Rs. 50,000)

For the remaining policy term of 10 years, his family will receive a monthly income of Rs. 50,000.

Another benefit of this policy includes the waiver of future premiums in case of an accident leading to permanent disability.

You have the flexibility to choose the monthly income for your family in your absence as per your requirement and also you also have an option to increase this monthly income annually by 10% (fixed) to ensure your family keeps pace with inflation.

In this option, Mr. X has to pay the annual payment of Rs. 7,354/-

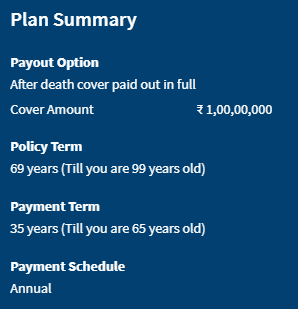

If Mr. X chooses for whole life option, other parameters are shown below:

He has to choose any one of the below options:

He has to choose any one of the below options:

Life long protection option

The main features of this option are:

- Cover for the whole life.

- In case of death or on the diagnosis of Terminal Illness, the family of Mr. X will receive a lumpsum amount of Rs. 1 crore.

- In case of an accident leading to permanent disability, all the future premium payments will be waived off.

To avail of these features in this option, Mr. X has to pay the annual premium of Rs. 76,024/-

3D Life Long protection option

Features in this option are the same as that of Life long protection option. With an additional cover of 34 Critical Illnesses, that is, in case of the diagnosis of any listed critical illness, all the future premiums will be waived off.

To avail of these features in this option, Mr. X has to pay the annual premium of Rs. 80,681/-

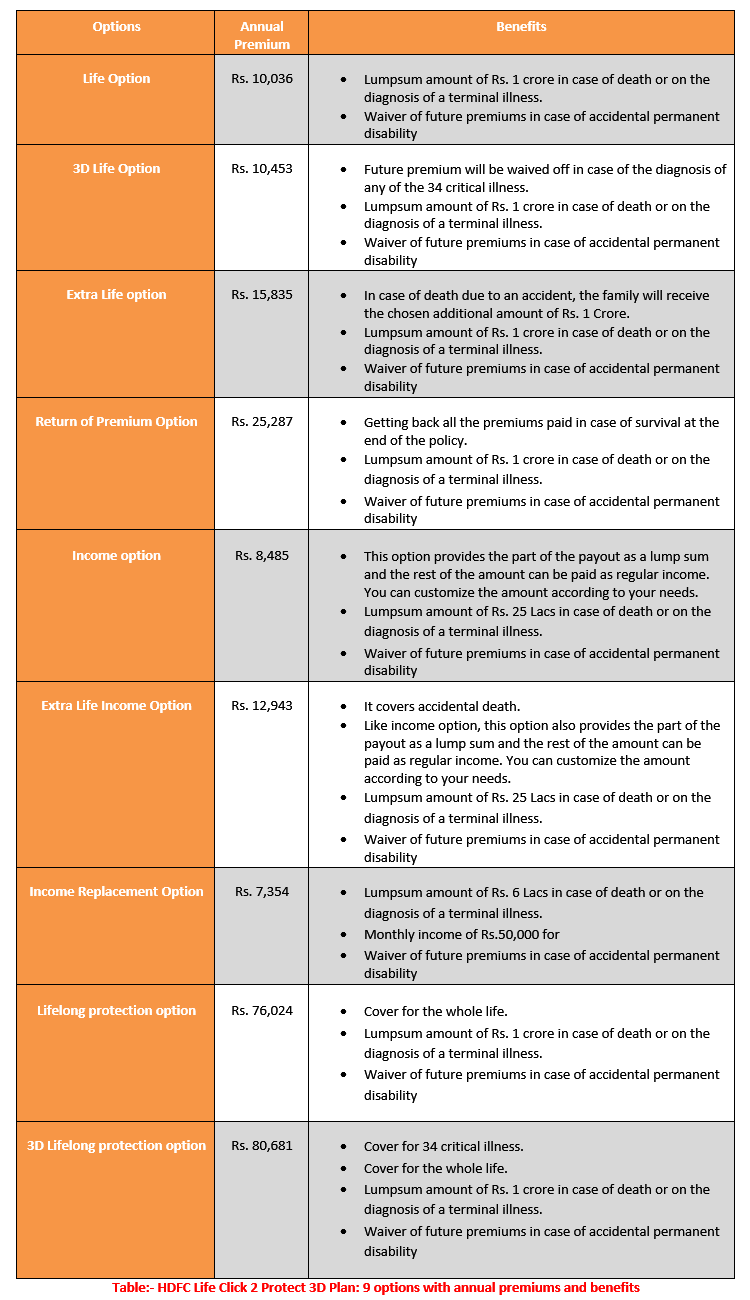

The table shown below summarizes the benefits under all 9 options, along with the annual premium paid in each case.

HDFC Life Click 2 Protect 3D Plus: Analysis and Review

Since this policy has 9 different options and each option offer a unique feature. So, it is easy to be lost while choosing the most suitable option for yourself.

In this section, we will explore each of these unique features and will help you to decide whether it is meeting your needs or not?

This is the list of the unique features provided by HDFC Life Click-2-Protect 3D Plan apart from basic Life Cover:

-

1. Waiver of future premiums due to accidental permanent disability – available for all options

2. Cover for 19-Terminal Illnesses – available for all options

3. 34-Critical illness waiver of premiums – available under the 3D option

4. Accidental death cover – available under extra life option

5. Return of premium in case of survival at the end of the policy.

6. The option of choosing “Lumpsum+Monthly” Payout option

7. Opting for Life-long insurance cover.

Now, let’s analyze each of these benefits

#1 Waiver of future premiums due to accidental permanent disability

Since the cost of adding the first benefit is only Rs. 319 per year. So, there is no harm in including this benefit in your base plan. You can consider this additional option.

#2 Cover of 19 Terminal Illnesses

In the illustrations, we have not considered this option for premium calculation. In case, if you add this option your annual premium will be increased by the annual amount of Rs. 2,865.

You can have it if you need it; it is NOT recommended though.

Probably you should consider taking its standalone cover from the Health Insurance company.

#3 Waiver of premiums due to 34-critical illnesses

This feature is available with the ‘3D option’ of this policy.

The premium amount for the Life option is Rs. 10,046 and for 3D Life option is Rs.10,453.

Paying the extra Rs. 400 per annum is not a harmful deal. You can consider opting for this feature.

Whereas, we suggest you get all the illnesses covered in the separate Health Insurance Cover.

#4 Accidental death cover

Accidental death cover is required for you, only if you do frequent traveling. If you need the accidental death cover, we recommend you to take it as stand-alone through any general insurance company instead of adding up with your term insurance. You can avoid complicating your Term Insurance plan as much as you can because your family will be using it in your absence, so make it much simplified.

#5 Return of Premium

It seems like a compelling option to consider. But have a look at its illustration in the previous section; you are paying Rs. 25,287 per annum which is 2.5 times as expensive as compared to the basic life cover option.

Let’s do some maths:

You are paying Rs. 25,287 per annum. In 30-year duration the total amount you have paid is Rs. 7,58,610.

In case of survival at the end of the policy term, that is, after 30 years, you will get this amount back after deductions due to any other additional rider, in our illustration we have opted for a premium waiver due to permanent accidental disability. The amount you may get will be somewhere around Rs. 7.4 Lacs!

Now let’s take this scenario:

Out of Rs. 25,287, let’s say you buy a basic Life Option of this policy which costs Rs. 10,036. You are left with Rs. 15,251. If you invest this amount in PPF where you will get the guaranteed returns of 8%.

Investing Rs.15,251 per annum for 30 years will generate the guaranteed returns of Rs.18,65,897 (Obtained using PPF Calculator).

Now, it’s up to you to decide whether you want the reduced amount of your premium to be back or you want to get back ‘more than double’ amount by intelligently using your money.

So, don’t fall into the trap of ‘Premium Refund’ by paying higher premiums each year.

#6 Option of choosing “Lumpsum+Monthly” payout option

Receiving part of your money as a lump sum and part as monthly payout to your family, this way you are giving more control to the insurance company over your money. The company will pay out the monthly income to your family in their own ways, following their own rules, you won’t be having any control over your own money!!

Suppose your family may need some urgent money at any time, they cannot claim it since the payouts are monthly.

Therefore, you should avoid picking up such complex options.

#7 Opting Life Long Insurance cover

Term insurance is basically made for you if you are the sole breadwinner in your family, you can utilize its benefits till your retirement when your family is dependent on you.

There is no point in choosing for life long cover by paying higher premiums because there are other better alternatives available if you need higher corpus for your family in your old age post-retirement.

HDFC Life Click 2 Protect 3D Plus comes with two Life-long options; Life long protection and 3D Life long protection, as we saw in the illustration, their annual premiums are Rs. 76,024 and Rs. 80,681 respectively!!

Let’s say you pay the premium of Rs. 80,000 for 35 years, after 35 years your paid premiums sums to Rs. 28,00,000!!

Giving away Rs. 28 Lacs to the insurance company for the cover of Rs. 1 crore is illogical because there are better alternatives available to use your money wisely!!

Now, let’s take the scenario when out of your Rs. 80,000 annual premium, you pay Rs. 10,000 for basic Life Insurance option of this policy, and the remaining amount of Rs. 70,000 you invest in PPF, which gives 8% annual returns; so, after 35 years of being invested in PPF, you will generate a corpus of Rs. 1,30,27,150. (using PPF calculator)

You will get this return after 35 years, your death will no longer play any role to acquire this corpus, it is guaranteed and you are still insured for 35 years.

Now, after going through the analysis of each additional feature of this plan; let’s take some of the important questions on HDFC Life Click 2 Protect 3D Plan:

1. Is HDFC Life Click 2 Protect Plan good or bad?

Though its basic term plan is expensive as compared to the other term insurance plans, overall it is a good policy, you have the flexibility to choose or opt-out any option.

2. Which is the best option to choose among the various options available under HDFC Life Click 2 Protect plan?

You can consider the Basic Life option. In case if you need the cover against 34 critical illnesses, then you can consider the 3D Life option. Refer Analysis section for more details.

3. How to cancel HDFC Life Click 2 Protect 3D policy?

The policy provides the FREE Look-in period of 30-Days, where you will get your premium back without any loss. In case, if you want to cancel your policy beyond the Free Look period you can request for auto-debit deactivation by submitting the deactivation request at: service@hdfclife.com through your registered email id. For more details, you can read this product brochure.

Conclusion

We recommend you to take the basic Life Option if you are planning to take a new Term Insurance from HDFC Life.

You can also read the cheat sheet for selecting the right Term Insurance for you and the review of ICICI Pru iProtect Smart Policy, in case you want to explore more Term Insurance options.

We hope the information laid out in this article will allow you to understand each option of HDFC Life Click 2 Protect 3D +plan, and finally taking the right call in choosing any one of them.

In case you have any further doubts, you can ask them in the comment below.

Also, you can register for 30-min FREE Financial Planning consultation call by clicking the link below, we will guide you in choosing the right insurance and investment schemes, customized for your needs.

Leave a Reply