How to select the best term insurance plan?

You have so many insurance options available in the market so, how would you know which is the best term insurance plan to buy?

Do you pay a higher premium or a lower premium for your term insurance?

Are you sure that the company will settle down your claims or not?

Are you still confused to choose which will be the best insurance plan?

If so, then have a look over this and know more about term insurance plans. It will guide you to choose the best term insurance plan this year.

In this post, we will discuss all the essential elements that you must consider before finally buying your Term Insurance Policy!

Table of Contents:

1.)Why do investors prefer TERM insurance?

2.)How old the insurance company is?

3.)Which mode of buying the policy is considered?

4.)Do you consider Premium against the size of the life cover?

5.)Claim settlement ratio

6.)Tele-medical Examination

7.)Don’t hide your health issues and habits you have

8.)Are you one who is excited about term insurance plan riders?

9.)Buy a Best Term insurance plan till your retirement

10.)Better to purchase earlier

11.)Small Insurance Cover is not the best Insurance Cover

12.)Private Insurance Companies: Are they trustworthy?

13.)Term Insurance Policies Vs Other Insurance Policies

14.)Conclusion

1. Why do investors prefer TERM insurance?

Term insurance is a basic form of insurance. It is a type of life insurance that provides you coverage for a certain period of time.

Which is the best Term Insurance Plan is the question that gets asked the most.

But why do you need term insurance?

– Are you one of the breadwinners of the family?

– Are you serving a loan or liability?

– Are you looking for a High cover at a Low Premium?

If yes, then term Insurance will be your choice.

Term insurance is an important step in your financial planning.

In case of your demise during the policy term, the claim amount from the insurance company will financially protect your family throughout their lifetime.

It also helps them to take care of liabilities and loans. It also offers a high cover for a relatively smaller premium.

The number of people who opt for Term Insurance plans in India has risen from 39% to 43%. The question that bugs all of them is….

“How do I choose the best term insurance plan in India?”

Read further to find the answer.

What are the Features of Term Insurance:

Affordability:

The most salient feature of Term Insurance is its affordability. The premium for the plan is the cheapest as compared to other insurance policies.

Online and Offline Purchase:

- Term policies can be purchased very easily offline (like brokers, agents, etc.) and online. Also, online term policies are 40% to 60% cheaper than offline term insurance plans since there is no intermediary commission and other related charges.

Flexible-Premium Payment Option:

- Term Insurance policies are flexible and provide a premium option of monthly, quarterly, annually or semi-annually.

Death Benefit:

- Term insurance gives purely death benefits to the insured.

Tax-Free:

- Term insurance is completely tax-free, i.e., beneficiaries don’t have to pay any taxes on the claim amount of death benefit.

Example of Term insurance

Is term insurance a good idea?

Let us see an example that clarifies why you need term insurance.

Mr. Leo is the breadwinner of his family, his wife is a homemaker, and he has 2 children.

He is planning to purchase a Best-term plan at the age of 28.

His annual income is Rs.6,00,000, and he retires at the age of 58 years.

So, he takes a plan for a Sum Assured of Rs.55,00,000, and it is valid for 30 years.

What would be his premium?

Do you think he needs to pay a huge premium every year?

As per the calculations, Rs.5968/- (including taxes) will be his premium annually. Less, isn’t it?

If he passes away before 58 years, then his family members will be paid a Sum Assured of Rs.55,00,000, which is higher than his premium payment for 30 years (i.e., approx. Rs.1,79,040). There is no maturity benefit under this term policy.

How much term insurance will I need?

10 essential things to remember while buying term insurance

To choose the right Term Insurance, every investor needs to be aware of these 10 essential things. This can act as a checklist to choose the right term insurance plan.

2. How old the insurance company is?

Another question that gets asked the most is

Which company provides the best Term Insurance?

Even though the answer to this question is subjective, there is a common thread by which you can judge the best insurance company.

You can choose a plan based on the year of establishment of insurance companies. Because there are only 24 companies in India.

So how to find the best insurance plan from the best insurance company?

Eg: Mr. Gowtham is planning to choose a school for his daughter’s education. He made research based on the reputation of the school, well-qualified professors, long-term positions etc. It made him help her daughter with good knowledge.

Likewise, if you choose a term plan based also on how old the company is, it will be a solid decision.

3. Which mode of buying the policy is considered?

While purchasing a term plan, determine whether you are buying the plan online or offline. In the case of a term plan, buying online is more advantageous and economical.

Because there will not be any charge of commission since there are no intermediaries involved while buying the plan.

4. Do you consider Premium against the size of the life cover?

The premium value may differ from one company to another on term insurance plans.

Compare the premiums for the size of the life cover offered by the insurance company. This should be ideally large to cover all your debts as well as aid your loved ones to lead a comfortable lifestyle in case of your demise.

Also, one of the traits of the best term insurance plan is the premium should be low and pocket-friendly for the coverage you opt for.

Download your Human Value Calculator here!

5. Claim settlement ratio

One of the major points to consider while choosing a term insurance plan is the claim settlement ratio.

The claim settlement ratio refers to the number of claims that the insurance company has paid following the death of the policyholders.

In other words, the percentage of death settlement claims settled by the insurance company in the past is known as a claim settlement ratio.

It can be computed as,

Claim Settlement ratio = a Total number of death claims settled / Total number of death claims received.

Eg: If a life insurance company receives death claims of 1000 and they settle 987 claims, then the claim settlement ratio would be 98.7%. Since the higher claim settlement ratio helps an individual to choose the best term insurance plan.

Will the IRDA Claim settlement ratio help in choosing the best term insurance?

Yes, claim settlement ratios are one of the factors to be considered while choosing the term plan.

The company which has settled the most claims can be called the best insurance company in this particular aspect even though it falls short in other categories.

Why are you buying life insurance? If I am not there my family will get the sum assured and have financial security.

But what will happen if your claim gets denied – the whole purpose of taking a term plan will be defeated. So, it’s better to check it rather than be sorry.

It will help the policyholders to choose which company has settled the maximum number of claims in that financial year.

Yes, the Higher the claim settlement ratio, the better the chances of availing the entire sum assured amount and in turn the best insurance plan from the best insurance company!

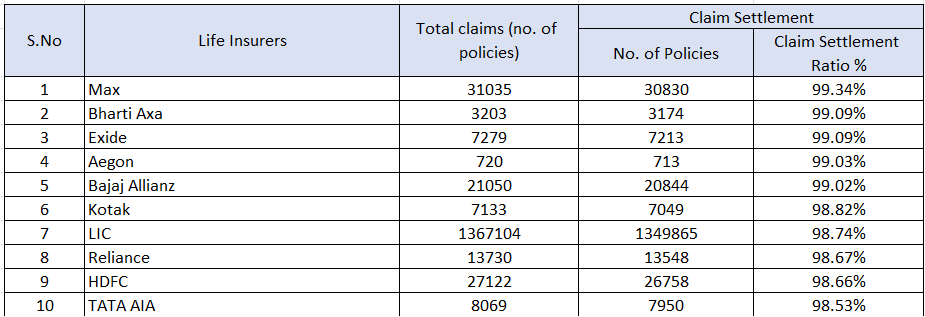

A tabulation showing different companies’ claim settlement rates in percentage.

Top Best Performance of Insurance Companies in 2021-2022 with respect to Their Claim Settlement Ratios:

In the above table, the Top-10 companies are listed based on their Claim Settlement Ratios.

The companies that have higher Claim Settlement in terms of % of Policies AND as % of Benefit amount can be considered best for buying term insurance policies.

We have already defined Claim Settlement Ratio as the % of policies.

Now let us understand the Claim Settlement Ratio as the % of the Benefit amount.

It means the amount of claim settled by the insurance company;

for example, if the insurance value is Rs. 1 crore in TATA AIA Insurance company, then it has successfully settled the 98.53% of the claimed amount of Rs 1 crores, that is Rs 98,53,000!

Below is the list of top 10 best insurance companies based on their Claim Settlement Ratios in terms of percentage of policies and benefit amount in Cr.

Top 10 Best insurance companies based on their Claim Settlement Ratios in terms of percentage of policies and benefit amount in Cr.

These are the top 10 best-term insurance companies in India based on their Claim Settlement Ratios.

6. Tele-medical Examination

What is telemedical in term insurance?

Never go for a telemedical examination. It may be considered to be the easiest process for you and your insurance companies.

But in the future, even the best insurance companies may find 1000 reasons to reject the claim on a health basis.

7. Don’t hide your health issues and habits you have

One of the worst things people do while purchasing the term plan is to hide the fact that you are a smoker or an alcoholic. Please don’t do that.

Your premium calculation will be based on this information if you hide or lie then later, there is a chance that the insurance company may reject your claims.

If you want the best Term Insurance plan, please be truthful about your habits and health condition.

This will benefit the insurance company as well as yourself because being truthful will avoid your claim from getting rejected.

8. Are you one who is excited about term insurance plan riders?

If so, please don’t get overexcited by term insurance plan riders. At times, investors choose riders just because it is available. Please check do you need those riders.

There is a common misconception among people that only insurance plans with riders are the best Insurance Policies!

Please compare term insurance plans with riders.

Because riders come with an additional cost. So, you need to make sure that it is adding real value to you or not.

Riders are mainly for those people whose life is highly risk-oriented.

For example, let us take Mahesh. He is working as a Marketing executive in Bangalore.

He needs to travel quite a lot of places in his professional life. So, the chances that he may die by accident are a little higher hence, he can choose an accidental death benefit rider to avail the additional benefit.

Likewise,

- If your family has a history of critical illness, then a critical illness rider is a must for you.

- If you are the sole breadwinner of the family, then the Income Benefit rider will support your family with regular income.

Hence, you need to consciously decide about buying the best term insurance plan with riders or without riders.

9. Buy a Best Term insurance plan till your retirement

A Best Term Insurance policy is one of the most cost-effective methods that provide financial support to one’s dependents and family in his/her absence.

It’s a well-known fact! Isn’t it?

The primary objective is to act as an income replacement tool.

It eliminates the financial burden on a family in case of an untimely death of the earning member. Hence, you mustn’t buy term insurance for the longest tenure i.e, if you are at age 30, you don’t have to buy term insurance till 80 years.

You only need to buy a term insurance plan until your retirement and not beyond that. After your retirement, there will not be any financial loss in case of any mishappening to you.

So, you can limit the period of your term insurance plan to your retirement age.

10. Better to purchase earlier

Earlier, if we purchase term insurance, the better it will be. The moment you satisfy the below two conditions, you need to go for a term insurance plan:

- You earn income.

- You have dependents.

Do not be very late to buy a term plan because as time passes, your premium amount will also increase depending on your age and health conditions.

Once you are clear that you require a certain amount of life cover, go ahead and complete the action as soon as possible. Otherwise, in case of any unfortunate mishappening to you, your family will financially suffer.

11. Small Insurance Cover is not the best Insurance cover

Term insurance would be suitable for a person with a low income and also a person who is the sole breadwinner in the family and has a moderate or high income.

But the important thing is people should take a policy with an ideal term insurance cover or a large insurance cover.

Taking a policy for a few lakhs will not be sufficient. I have seen people taking term insurance for an amount that is less than their annual income.

In case of any mishappening to you, do you expect your family to manage with an amount just equal to your one-year annual income?

So based on your current and future earning potential, you need to choose your ideal term insurance coverage.

Because that helps your family’s financial future in case of your unexpected demise. It helps them to pay their debts and take care of their kid’s education, marriage, etc.

12. Private Insurance Companies: Are they trustworthy?

Which is the best Term Insurance?

Based on the advantages and the operation procedure of a private insurance company given below, you will be able to figure out by yourself their trustworthiness, and it will also help you to make an informed decision whenever you plan to purchase them.

I.)Advantages of Private Insurance Companies as compared to Public Insurance Companies:

- Offers 24*7 Customer Services.

- Quick Claim Settlement

- Flexibility to track claim status.

- Purchase and renewal of most of the policies can be done online.

II.)Operates under the strict guidelines of IRDAI:

Insurance Regulation and Development Authority of India (IRDAI) is the most competitive and diligent regulatory body which governs and monitors various aspects of the Insurance industry.

It has strict guidelines for both public and private companies, which have to be followed by all insurance companies (public and private).

IRDAI strives for the best insurance companies in India that provide the most reliable and best insurance policies to its customers.

III.)IRDAI is responsible for the formation of Private Insurance Companies

One primary requirement for a Private Insurance Company is to deposit Rs. 100 crores to IRDAI as their entry cost. Such high entry costs avoid fraudulent and small players to start a private insurance company.

IV.)Conducting regular audits

IRDAI conducts regular audits and inspections of every insurance company regularly to keep a proper check on their functioning.

IRDAI monitors essential indicators such as Claim Settlement Ratio, Claim Repudiation, and Claim pending records.

These indicators shed light on the claim settlement practice of insurance companies.

V.)Regulation of exit of Private Insurance Company

The entry of any new player is tough, but exit is made next to impossible by the strict regulations of IRDAI.

According to IRDAI guidelines, if a company cannot continue functioning due to some unavoidable reasons, it is supposed to be merged with the existing Insurance Company of their choice.

So that the customers of the existing company are not left astray and feel cheated.

VI.)Insurance Ombudsman:

In case of any complaints and disputes, a policyholder can approach the Insurance Ombudsman. Their job is to settle the consumer’s grievances most efficiently and cost-effectively efficiently and cost-effectively.

13. Term Insurance Policies Vs Other Insurance Policies

Is term insurance good or bad?

Let us compare term insurance with other insurance plans to see whether term insurance is good or bad.

Term Insurance vs Traditional Insurance Policies (Endowment insurance)

The returns from traditional policies are very less. It is better to go for a combination of pure-term policy and PPF instead of traditional policies.

Instead of going for an endowment plan with a sum assured of Rs. 10 Lacs for a premium of Rs. 70000 for 15 years, the investor can opt for a term plan with 10 lacs sum assured for a premium of Rs.1500 and the balance Rs. 68500 can be invested in PPF.

Please remember the bonus from insurance policies is of future value and will not have compounding benefits.

When a person dies in the earlier years of taking a policy, the beneficiary will get only the sum assured.

When you go for a combination of the best pure term insurance and PPF, in case of death, the beneficiary will get the sum assured from the best term plan and the accumulated money from PPF contributions.

So, the term insurance plan and PPF combination will give investors more benefits in both the situations of death and survival.

Also, the contribution to your PPF account is flexible. Based on the funds available, you can increase or reduce your contributions every year.

Term plus SIP is better than ULIP

Ulips has a complex way of charging fees to investors. They charge under multiple heads like policy administration charges, premium allocation charges, mortality charges…

Mutual Funds follow a very transparent way of charging fees. They charge only exit load and fund management charges.

These charges are very clearly mentioned in the SIP. These charges are easy to understand, even for a layman.

If you want to revamp your ULIP from one company to another company, the exit and entry costs will be higher.

In Mutual funds, the exit load is only 1% (and that too if you withdraw before 1 year of your investment), and there is no entry cost.

Because of these factors, it is better to invest in a combination of Term insurance and SIP instead of ULIPs.

Pure Term Insurance Policy VS Returns of Premium Term Insurance Policy

To read more about the Return of Premium in a Term Insurance Plan click here

Challenges in other insurance plans:

- Other insurance policies such as ULIP and endowment usually charge more premiums than the Term plan. The term plan has the cheapest premium as compared to other plans.

- Other plans have certain costs like commission charged throughout the policy, which will be higher than term insurance.

- Term insurance is flexible in that it can be canceled at any time if needed.

- Term plan is much easier to understand than other insurance plans, such as an endowment plan which combines risk cover with savings.

- Premium paid for term insurance is much less and eligible for tax benefits under Sec 80Cthan endowment policy.

14. Conclusion

Choosing the best term plan is a very good decision because it helps to secure the financial needs of your family after your demise. Also, it is very affordable since the premium is very less under this policy.

Private Insurance companies are equally trustworthy as Public Insurance Companies as both are regulated by IRDAI guidelines equally.

Overall, the best Term insurance policy ensures security, protection, and peace of mind for your family.

You can also opt for this term insurance plan with a combination of PPF and SIP, which may help you to get more returns on maturity.

There is a lot of free advice available on social media platforms like Quora, Twitter, Facebook, etc.

There are a lot of people who lose their hard-earned money every day from this advice. Consult a professional financial planner for safeguarding your wealth.

Our strategic team consists of industry veterans and experts with great knowledge of the insurance sector. Their hands-on experience in finance intricacies helps our clients leverage the potential available in the market and make a smart move with well-curated general and life insurance plans.

Any recommendations on top few term insurance plans with a combination of PPF and SIP, which may help you to get more returns on maturity?

Considering one sole working member in the family?

Hi, for personalized investment suggestions, you can contact our certified financial planner. Please click the link and fill out the 30-minute complimentary consultation form to book your appointment.

https://www.holisticinvestment.in/complimentary-financial-plan-consultation/

Will I get back with he premium paid after the end of the term if I am still alive

No, the premium will not be returned, you have to treat this as an expense.

I am 61 years old without having any health issues. I want to invest and also want life cover. Pl guide me the best way. I can invest upto 40000 per month. I don’t have any term plan.

I am 61 years old and have not taken any term plan since I had no health issues. Now after retirement I want to invest and also want life cover. Pl guid me how I should do.

Hi!

For personalized financial plan suggestions, you can sign up for our free 30-minute complimentary financial plan consultation.

Please click the link and get your appointment to talk with our Certified Financial Planners.

https://www.holisticinvestment.in/complimentary-financial-plan-consultation/

Hi!

For personalized financial plan suggestions, you can sign up for our free 30-minute complimentary financial plan consultation.

Please click the link and get your appointment to talk with our Certified Financial Planners.

https://www.holisticinvestment.in/complimentary-financial-plan-consultation/

I am 45 year old male and thinking of going for a term plan. Till what tenure do you suggest I take the term plan….

Also – can the term plan tenure be extended later. …?

Hi!

For personalized financial plan suggestions, you can sign up for our free 30-minute complimentary financial plan consultation.

Please click the link and get your appointment to talk with our Certified Financial Planners.

https://www.holisticinvestment.in/complimentary-financial-plan-consultation/

I purchased a term plan Bharti AXA. If anything happen with Bharti AXA in near future ( company will closed) then how my policy will run??what happen with my policy??

Bharathi Axa can not just like that close the company. They will be selling it to another life insurance company. The acquiring company will agree to honour the Bharathi Axa’s policy claims.

So there will not be any challenges.

Cheers!