Table of Content

- What is the home loan balance transfer?

- What are its Features?

- Why apply for home loan transfer? / What are its benefits?

- 6 Key things to consider before opting for a home loan transfer

- Why many of them are not opting for a home loan balance transfer?

- Conclusion

Are you paying a high-interest rate on your home loan?

Are you burdened with a heavy interest rate on your home loan?

Do you feel you’ll not be able to pay off your home loan?

Do you wish to transfer it to a lender offering a lower interest rate?

If Yes, then this article is for you.

This article will tell you all about a home loan balance transfer.

“It is the debtor that is ruined by hard times.” -Rutherford B. Hayes

“Debt can turn a free, happy person into a bitter human being.” -Michael Mihalik

“In the long run we shall have to pay our debts at a time that may be very inconvenient for our survival.” -Norbert Wiener

A mortgaged house is a liability in your balancesheet and an asset in the bank’s balancesheet. Only if you own the house without debt, then it is actually your asset. So you need to find ways to come out of your home loan asap. Home loan balance transfer may help you.

What is the home loan balance transfer?

A home loan balance transfer is a process of transferring your outstanding loan amount to another lender for a lower rate and other such benefits. This is also called as refinancing.

What are its Features?

- A home loan balance transfer is treated as a new loan.

- There is a fee to be paid on the loan transferred to the new lender.

- The balance transfer can be availed only after a predetermined time, as mentioned in the loan agreement.

- Once the transfer is completed, the transferred principal amount and applicable charges are payable to the new lender.

- The new lender transfers your outstanding principal amount to the existing lender.

- Most lenders check your track record of repayments and credit score before approving such transfer.

Why apply for home loan transfer? / What are its benefits?

- Lower interest rate/ reduces the interest outflow.

- It saves money.

- It reduces your EMI tenure.

- It can also be availed for the attractive benefits offered by the new lender.

6 Key things to consider before opting for a home loan transfer

1. Negotiate the interest rate: Before transferring, your loan to a new lender, ask your existing lender, if they could lower the interest rate. If you have a good repayment track record, your lender may consider your request, after checking your credit rating and loan repayment capacity.

2. Transfer charges: Home loan balance transfer has a lot of charges such as pre-closing charges, processing fees, application fees, administration charges, inspection fees, etc. There will be charges by both your existing and new lender. Also, find if there are any hidden charges. Use a home loan balance transfer calculator to find if it’s worth shifting your home loan.

3. Eligibility: Find if you are eligible to opt for a home loan balance transfer. Each lender may have different eligibility criteria. Thus find if you’re eligible.

4. Terms & Conditions involved: Make sure to go through all the terms and conditions before you transfer your home loan.

5. The full debt amount: Check if the new lender accepts the outstanding loan amount. Suppose you have a loan of Rs. 12 lacs and the bank limit is only up to Rs. 10 lacs. Then there is no use of the balance transfer.

6. The tenure left: In most cases, house loan balance transfer at the end of the tenure will not be of much use. Whereas it is more beneficial when there are many years left for the loan period to end.

One question you may have in mind is: Why many of them are not opting for a home loan balance transfer?

The reason is that it’s time-consuming and involves tedious procedures and formalities like documentation but if you would know the amount you would save by a home loan balance transfer, you may be ready to spend time on this, as it

- reduces your interest rate,

- reduces your tenure by a certain number of months and

reduces the overall cost of the loan.The second question you may have in mind is: Is it really worth it?

To know if the transfer is worth your time and effort, we have provided a customizable and user-friendly “Home loan balance transfer calculator”. By just calculating, you will know how much you will save on interest and the number of months by which your tenure will reduce.

What if you will be saving an equivalent of six months’ salary or more? (i.e, for eg: what if your savings through home loan balance transfer is approximately around Rs. 6 lakhs or more?) You never know. If yes, won’t you spend your time on it?

So check out the “Home loan balance transfer calculator”.

Here is an example of how the home loan balance transfer calculator works.

Example: You take a loan of Rs. 20 lakhs for 20 years @ 9% rate of interest.

Just enter them in the 1st sheet of the “Home loan balance transfer calculator”.

Enter them in the light yellow highlighted boxes, the rest is calculated automatically.

Enter,

- The loan amount,

- The loan term (years) and

- The rate of interest

You will automatically get the monthly EMI in the “Home loan balance transfer calculator”.

You will automatically get the monthly EMI in the “Home loan balance transfer calculator”.

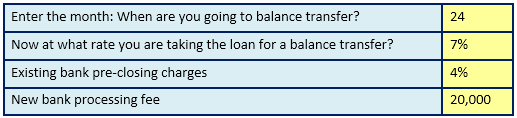

Now enter,

- the month in which you are planning to transfer the balance loan

- The rate of interest which the new lender is offering

- Pre-closing charges

- New bank processing fee

You would automatically get the below details in the “Home loan balance transfer calculator”.

You would automatically get the below details in the “Home loan balance transfer calculator”.

Hence you will come to know,

- The interest saved with the balance transfer

- and the no. of months reduced in the loan period

Here you will be saving Rs.6,93,471 on interest and the loan tenure reduces by 32 months.

Don’t you think, it is better to transfer the loan balance, in this case?

If your case is a similar one, then home loan balance transfer is totally worth it, i.e, it is more beneficial if you transfer your home loan when there are many years left for the loan period to end.

Now we will see the workings, which are available on the 2nd sheet of the “Home loan balance transfer calculator”.

When you transfer your balance loan amount in the 24th month, your outstanding loan amount increases (because of the charges), but decreases gradually from the next month onwards. As the interest rate is lesser, there is a drastic decrease in the interest amount.

Conclusion

From this article, you would have known if home loan transfer is worth it or not. Make your calculations and then decide whether to use home loan transfer or not. Once you find it is beneficial, do not put off but try transferring your outstanding loan to the new lender offering a lower interest rate as soon as possible.

If you have any comments or questions, write them in the comment box below.

Or are you interested in creating a Comprehensive Financial Plan for your financial goals?

Skip the queue by registering for your 30 Minute FREE Financial Plan Consultation. Click the ‘‘BOOK YOUR SLOT NOW!’’ button below.

Good Information

Thank you

Great Work.. Thank you very much.