“A housing loan is NOT a loan on your house;It’s a loan on your future income

that is secured by your house.”

Don’t you think owning a debt-free house, would make you feel much better?

Would you like to get over with the stress and burden?

Table of contents

- What is Home loan prepayment?

- Who is Eligible for Home Loan Prepayment?

- What is a Home Loan Prepayment penalty?

- Why do lenders charge prepayment fees on the home loan?

- What to consider before prepaying home loans?

- Advantages of Prepaying home loans

- Disadvantages of prepaying loans

- How can you Prepay your home loan?

- What is Lumpsum Prepayment?

- What is Top-up EMI Prepayment?

- Should You invest or make Home Loan Prepayment?

- Should you reduce the home loan’s tenure or the EMI?

- Conclusion

Let’s get started.

“It always seems impossible until it’s done.” – Nelson Mandela

Owning a debt-free house is always a dream. To make that dream come true, you can try prepaying your home loan.

You may have some questions in mind, like,

-

When will I be able to complete my home loan payment?

Will I be able to prepay my home loans?

How will I prepay my home loans?

Are there any advantages or disadvantages in prepaying the home loan?

Should I invest or make Home Loan Prepayment?

Should I reduce the home loan’s tenure or the EMI?

This article is here to help you with understanding the concept of Home loan prepayment.

‘You don’t have to be a miser, just be wiser with your money.’ —Dorethia Conner Kelly

What is Home loan Prepayment?

Home loan prepayment is when you prepay over and above your regular EMIs ahead of time. This prepayment can either be in part or full.

Who Is Eligible for Home Loan Prepayment?

Anyone willing to prepay home loans can do so if the lender allows it. Some lenders do not allow prepayment as it causes loss to them. So do check before you sign the home loan agreement. Also, find if there is a penalty for prepayment.

What is a Home Loan Prepayment Penalty?

A prepayment penalty is a fee or charges that you have to pay to the bank for prepayment.

Why Do Lenders Charge Prepayment Fees on Home Loan?

You may imagine, why should we pay a penalty for making prepayments?

This is because some loans are designed to last a certain number of years and earn interest in the bank for that tenure. So in case of prepayment, the bank may suffer a loss. So to safeguard them from any potential loss this charge is levied. But not all banks charge prepayment charges.

What to consider before prepaying home loans?

1. Retirement

If you are close to retirement, it is best to prepay as you may not have enough funds after you retire.

2. Future needs

Before you prepay, check if you have any needs for which you will require money in the future. By prepaying you may completely exhaust your savings. Hence your future needs are to be considered before prepaying.

3.Emergency

Make sure you have enough money for an emergency. If you have enough money for an emergency and also have health insurance, then go ahead and prepay.

4. Investments

If you invest your money instead of prepaying, would it be profitable? That is, compare your savings from prepayment and the returns you would get if you were to invest that sum. If the returns are higher then go ahead and invest instead of

prepaying.

5. Home Loan Balance Transfer

First, check if you have the option of doing a Home Loan Balance Transfer. Home Loan Balance Transfer means transferring your home loan to another lender offering a lower interest rate. If a Home Loan Balance Transfer is possible, then do it before you think of prepaying.

Now we will see the advantages and disadvantages of prepaying home loans.

Advantages of Prepaying home loans

- Prepaying home loans can free you from a big burden.

- You can save a lot on interest and the saved money can be used to meet your other financial needs or for investing elsewhere. This savings is indirectly income earned.

- The risk of losing ownership due to loan defaults gets mitigated.

- Your overall liability decreases as you prepay your loan. Your credit score will increase, thus improving your creditworthiness.

- If you anticipate that the home loan interest rates will increase in the future, it is beneficial to prepay.

Disadvantages of prepaying loans

- If you have a self-occupied property, you can claim up to Rs. 2 lakhs (on interest) as a deduction.

If you have a let-out property, you can claim the actual interest paid.For both self-occupied and let out property, you can claim up to Rs.1.5 lakh as a deduction (on principal).

These are the tax benefits that you may lose if you opt for home loan prepayment. - By prepaying, you may end up with no funds and it becomes difficult in case of emergencies.

- If you anticipate a decrease in home loan interest rates, it is better not to prepay.

Now we will see the ways in which you can prepay your home loan.

How can you Prepay your home loan?

Home loan prepayment can be done in two ways, either by,

1. Lump-sum prepayment (or)

2. Top-up EMI payment.

Now, we will see how these different methods of prepayment work.

Also read, “Warning: Don’t opt for EMI Moratorium! Discover why?”

1. What is Lumpsum Prepayment?

When you use a lump sum amount for one time prepayment, it is called as Lumpsum Prepayment. It may be the amount received as a bonus, increment, an amount from investment matured, or maybe a sum received as a gift.

Here is a link to the Lumpsum prepayment calculator.

This calculator will help you know the impact of prepayment, i.e. the amount you would be saving on interest and the months by which your tenure has reduced. We will find how this calculator works with the help of an example.

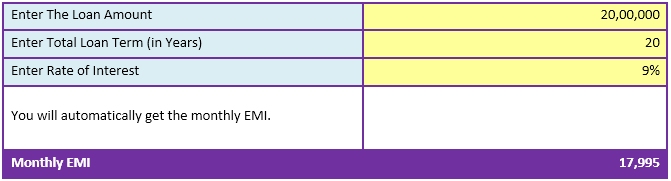

Example: You take a loan for Rs. 20 lacs, for a tenure of 20 years @ 9% interest.

Workings in the calculator: Just enter the below details, in the calculator.

- The loan amount,

- The loan tenure, and

- The rate of interest.

Now if you plan to prepay Rs. 3 lacs in the 24th month.

Just enter them.

- The month in which you are going to prepay and

- The amount you wish to prepay.

Entering the above details in the lumpsum prepayment calculator you will automatically get

- The actual interest payable.

- The interest to be payable after the lumpsum prepayment.

- The total interest saved with lumpsum prepayment and

- The no. of months decreased by lumpsum prepayment.

Here, in this case, the actual interest to be payable was Rs. 23,18,685, after the lumpsum prepayment, it becomes Rs. 14,44,997 and the amount you have saved on interest is Rs. 8,73,688 and the loan tenure also decrease by 65 months. This is how lumpsum prepayment works.

Now we will see the workings of Lumpsum EMI from Sheet 2 of the lumpsum prepayment calculator.

(In relation to the above example) We will see what happens when you prepay Rs.3 lacs as a lump sum in the 24th month. Look to the below table, when you prepay, your interest payable and the outstanding loan amount decreases drastically.

This is how Lumpsum Prepayment works.

You can download the lumpsum prepayment calculator here.

Now we will see what is Top-up EMI.

2. What is Top-up EMI Prepayment?

First, let’s see what EMI is.EMI stands for Equated Monthly Installment. Itis the

amount to be paid every month. Increasing your EMI’s on a yearly basis, at a certain percentage is called Top-up EMI Prepayment.

Say, for example, increasing the EMI amount by 5% every year… It can be done with an annual increment. This is a simple, easy and very practical way to prepay your house loan.

Here is a link to the Top-up EMI Prepayment calculator.

We will find how this calculator works with the help of an example.

Example: You take a loan for Rs. 20 lacs, for a tenure of 20 years @ 9% interest.

Just enter the below details in the Top-up EMI Prepayment calculator.

- The loan amount,

- The loan tenure, and

- The rate of interest.

Now enter in the Top-up EMI Prepayment calculator,

- The month in which you are going to top up the EMI and

- The percentage you would like to increase on EMI every year.

Entering the above details you would automatically get

- The actual interest that is payable.

- The interest to be payable with Top-up EMI.

- The total interest saved with Top-up EMI.

- And the no. of months decreased by Top-up EMI.

The actual interest to be payable was Rs. 23,18,685 and it becomes Rs. 15,24,372, after topup EMI payment and the amount you have saved on interest, is Rs. 7,94,313 and the loan tenure also decreases by 89 months.

This is how Top-up EMI works.

Now we will see the workings from sheet 2 of the Top-up EMI Prepayment Calculator. (In relation to the above example)

Look at the below table, to find what happens when you increase EMI by 5% from the 20th year. Your interest payable and outstanding loan amount decreases gradually.

This is how Top-up EMI Prepayment of housing loan works.

You can download the Top-up EMI Prepayment calculator here.

In both the prepayments, there is definitely an amount you would be saving on interest and also a reduction in the loan tenure. So, it is definitely beneficial.

Now we will see a few commonly asked questions.

Should You invest or make Home Loan Prepayment?

To know this find the maximum returns you will get per annum with an investment. Also, find how much you will be able to save per annum if you prepay in part or full. Find which is more profitable, the prepayment, or the investment, then choose accordingly.

Example: You have 3 lakhs of idle funds, you can use it for either prepayment or investment, but before that, compare the amount you receive from the investment and amount saved on home loan prepayment. Say you get Rs. 3,15,000 from the investment and you are saving Rs.4,20,000 from the home loan prepayment.

Which would you choose?

You would opt for the home loan prepayment. Likewise, you should check which is beneficial for you and opt for that which is beneficial.

Also read, “A Basic Checklist: 5 Key Aspects to Check in Any Investment Before You Invest”

Should you reduce the home loan’s tenure or the EMI?

Reducing home loan tenure instead of EMI will help reduce the total interest outflow. It is always advisable to increase the EMI amount as and when the salary increases. This will help you prepay your loan faster and would help you save on interest and also reduce your home loan tenure.

If you instead reduce your EMI, you will have to pay a lot more on interest, and the loan tenure also increases. Hence it’s beneficial to reduce your home loan tenure, not your EMI.

Don’t you think reducing your home loan tenure is more beneficial?

Conclusion

From this article, you would have got a better understanding of home loan prepayment. There are a lot of benefits to prepaying your home loans, but it’s also good to know the disadvantages before prepaying your home loan. Make a wise choice, considering all the above factors.

If you have any comments or questions, write them in the comment box below.

Or are you interested in creating a Comprehensive Financial Plan for your financial goals?

Skip the queue by registering for your 30 Minute FREE Financial Plan Consultation. Click the ‘‘BOOK YOUR SLOT NOW!’’ button below.

Leave a Reply