The first wave of AI and automation disruptions has created a substantial impact on our economy.

Many people have lost their jobs.

If you have lost your job or if you are being paid less, you can understand the painful situation better than us.

There are many others like you. You would be undergoing a lot of financial stress and emotional trauma.

There would be panic, pressure, and responsibilities especially if you’re the breadwinner of your family.

Reports have highlighted cases of stress and extreme distress due to sudden layoffs or fear of losing employment in the tech-driven economy.

With the sudden loss of income, thinking of managing your living, buying necessities, and paying off loans and insurance becomes difficult.

If you’ve been exploring ways for how to generate income without a job or how to invest so you don’t have to work, this guide will help you rebuild your confidence and cash flow through simple, smart, and low-risk investments.

The good news is that while AI and automation are reshaping the workforce, opportunities exist to earn steadily through smart investments and diversified income sources.

This article will help you invest and earn a regular income for two years.

We are glad you’re reading through to find solutions to your problem. You’ve taken the right step.

Table of Contents:

- Have you heard of Oseola McCarty’s story?

- Analyze Your Spending Before and After Job Loss

- How did you spend your money before?

- How are you spending your money now after the job loss?

- Here’s how to face the job cut and generate regular income for two years

Have you heard of Oseola McCarty’s story?

This is an inspiring story of a young girl who started saving as a child, heeding to her mother’s words.

She wasn’t in a great job, and so her earnings were also less.

She neither had job security nor a guaranteed regular income.

Regardless of all this, she did it through the tragedies, some of the worst economic crises in American history, she was able to withstand them.

Not only that she made it through all these but she also had a sum of $280,000 in her bank account during the time she retired, i.e. in 1995.

She, even as a child, was only concerned about saving for her future.

The question is if she can, why can’t you? Or why won’t you?

You can read her full story here,

Like McCarty, you too can start small — whether it’s your first income, or you’re trying to survive after a job loss due to AI, automation, or corporate restructuring, consistent saving and investing can change your future.

Analyze Your Spending Before and After Job Loss

Now, to know how to invest, first, let’s analyze your spending habits before your job disruption and after.

How did you spend your money before?

Before the rise of AI-driven layoffs and automation in the workplace, you would have spent money on shopping, restaurants, entertainment, beauty parlours, movies at theatres, gym, tours, events, attractions, and other such recreational activities.

You would have spent on them lavishly.

How are you spending your money now after the job loss?

After the job loss, or a reduction in income, and with the closure of almost all activities, you have stopped spending on many but there would still be some expenses that you cannot stop like your daily provisions, rents, loans, insurances, etc.

Read through this article to know how to generate regular income for 2 years and also pay off your outstanding expenses.

Also, watch the video here!

If you’re living in metro cities like Chennai, calculate your fixed monthly expenses in Chennai or according to living expenses in the city you live in before planning new investments — this ensures your survival fund is realistic.

Here’s how to face the job cut and generate regular income for two years

Follow these simple and practical steps.

1. Estimate

2. Invest

3. Stop worrying

4. Get help

You will learn from the four steps, how to reduce your unwanted expenses, and how to invest for a regular income.

1. Estimate

What should you estimate?

Estimate how much money you need for expenses like essentials, loans, insurance payments, etc.

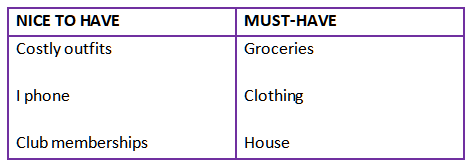

First, we will see the difference between Nice to have and the must-have expenses.

⭐ Nice to have, Must-have

What is nice to have and what is must-have?

“What you need and what you want aren’t the same things” – Cherise Sinclair

Must have are the needs and these are the essentials.

Nice to have are wants. These should be avoided as they are not essentials during this time.

Cut down these non-essential expenses, it can be subscriptions, memberships, etc. all those without which you can survive. Do this at least during this time of uncertainty.

Benefit: This will allow you to save money for other necessary items like groceries, rent, utilities, etc.

Here is a link to the Expense Planner Calculator, you can download this.

Where Can I Park My Money Without Loss?

For people who have lost jobs or people facing salary cuts, safety of capital is crucial.

You can park your money without loss in:

- Liquid mutual funds (for short-term needs)

- Recurring deposits or POMIS (Post Office Monthly Income Scheme)

- Senior Citizen Savings Scheme (if applicable for family elders)

- PPF or NPS, for tax-free and inflation-beating long-term growth

These options ensure your funds are accessible and your capital stays intact while generating income.

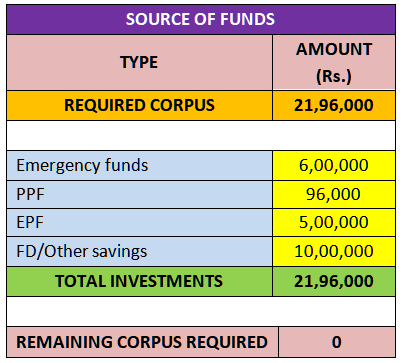

The first step is Estimation.

In the first sheet, we will estimate the amount required for 2 years.

To start with, first, enter your monthly expenses, automatically it will sum up the monthly expense, yearly expense, and the expense for 2 years, i.e. the amount required for 2 years. Here the monthly expense amounts to Rs.91,500 which leads to Rs. 10,98,000 per year and Rs.21,96,000 for 2 years respectively.

Here the monthly expense amounts to Rs.91,500 which leads to Rs. 10,98,000 per year and Rs.21,96,000 for 2 years respectively.

Make note of the amount you require for 2 years, in this case, it is Rs. 21,96,000.

- Insurance – Don’t forget to pay your insurance premiums.

- Loans

“Some debts are fun when you are acquiring them, but none are fun when you set about retiring them” – Ogden Nash

If you have loans, find how much is outstanding.

Try to pay off your debts, if that’s not possible, then try extending the loan tenure to lower the EMI, and in the worst case, you may use the EMI moratorium facility.

If you’re wondering, “Can I withdraw my PF amount while working?” — yes, under certain conditions, partial PF withdrawal is allowed for emergencies such as medical needs, home loans, or job loss situations.

2. Invest

“Never depend on a single income, make an investment to create a second source.” – Warren Buffet

Warren Buffet stated this long time ago, but it still makes sense.

It is good to make investments, so you always have a second source of income, especially during periods of job uncertainty due to AI, automation, or corporate restructuring.

Why Investing Is Important After Job Loss?

Losing your job due to AI disruption or salary cuts might have shaken your financial stability.

But have you ever wondered — what if you could still create a steady income stream even without a job?

Post-COVID investments are not just about growing wealth, but also about financial survival, stability, and flexibility.

a. Resources

During this crisis from where will you have money to make your investments?

You can use your emergency funds, fixed deposits, and other savings.

What if you haven’t saved?

If you haven’t saved anything, you can use your PPF and EPF amounts (Here a partial withdrawal is allowed).

Here, Rs. 21,96,000 that we found after estimation is the amount we require for the next 2 years.

Now let us find how to source this.

This step is called SOURCE OF FUNDS.

In sheet 1 of the calculator, on the right hand side, you can enter the amounts you have from your various investments.

Note: Please arrange funds to make this Remaining corpus required as zero.

b. Where to invest

Where should you make your investments for a regular income?

Choices can be deceiving and time-consuming and hence we have listed the investment options here below for your convenience.

⭐ Liquid funds

Liquid funds invest in high-quality short term debt mutual fund instruments.

It is to generate income in a very short-term with safety. As the name suggests it is highly liquid.

Liquid funds are ideal for those who want to survive job loss with mutual funds and maintain easy access to cash for monthly expenses in Chennai or any other city.

⭐ Bank fixed deposits (FD)

A bank FD pays a fixed rate of interest until given maturity date.

It provides a higher rate of interest than a regular savings account. It gives you an assured return.

This is one way of generating regular income. It helps the habit of saving and it is an appealing and secure option.

For eg: You invest Rs. 6 lacs @ 5% interest for 1 year.

By the end of one year, you would earn Rs. 6,30,000 (Principal and interest).

If you’re wondering where can I park my money without loss, FDs and short-term deposits remain the safest options during uncertain job periods.

⭐ SWPs (Systematic Withdrawal Plan) in Debt funds

This is a standing instruction given to the mutual funds, to credit a fixed sum every month to your bank account.

It allows you to stay invested and withdraw only periodically. There is a discipline in withdrawing.

For example: If you invest your money in a savings account, you may withdraw as and when you want and chances are high that you will overspend.

But if you opt for SWP’s in liquid funds, you will be credited a fixed sum every month and hence there will be control in your spending.

SWPs are a great choice if you’re looking to generate income without a job.

They create a sense of “salary replacement” through monthly pay-outs, helping you cover living costs even after job loss.

These are the options where you can park your funds, do not choose an easy option but rather the right option, by analyzing its pros and cons.

When you invest so you don’t have to work, focus on low-risk assets that can provide predictable cash flow — like SWPs, FDs, and dividend-paying mutual funds.

Benefit: You will be able to get a regular income for two years.

c. How to invest?

Now, this step is called “Investing in funds”. It is on sheet 2, on the calculator.

The remaining corpus required here is Rs.21,96,000 for two years.

Now we will see how to invest for 1st-year income and 2nd-year income.

For 1st year income: The amount needed for the first year is Rs. 10,98,000.

Now let us see how to invest this amount. In the first year, the plan is to invest Rs. 10,98,000 in liquid funds and to withdraw Rs. 91,500 via SWP.

For 2nd year income: The amount needed for the second year is Rs. 10,98,000.

For 2nd year income: The amount needed for the second year is Rs. 10,98,000.

Let us find how to invest for the 2nd year’s income.

At the beginning of the first year itself. This money is idle for the first 12 months.

So we will invest this at the beginning of the first year itself in FD.

As and when it matures at the year end, we can reinvest to generate income for 2nd year.

There are two options for the second year.

Option 1(A) is to invest Rs.10,98,000 in fixed deposit and when it matures, the maturity amount (Rs.11,52,900) can be invested in liquid funds and withdrawn via SWP (Rs. 96,075). Though the required monthly income is Rs. 91,500, you can withdraw Rs. 96,075.

(You can enter the rate of interest, here it is 5%)

Option 1(B) is to withdraw only Rs. 91,500 monthly from the maturity amount as SWP and later withdraw Rs. 54,900 once(additional reserve).

Option 1(B) is to withdraw only Rs. 91,500 monthly from the maturity amount as SWP and later withdraw Rs. 54,900 once(additional reserve). The 2nd option to generate the second year income is to invest a slightly lesser amount at a discounted rate (Rs.10,43,100), which will mature to Rs. 10,98,000.

The 2nd option to generate the second year income is to invest a slightly lesser amount at a discounted rate (Rs.10,43,100), which will mature to Rs. 10,98,000.

Then it can be invested in liquid funds and withdrawn via SWP (Rs. 91,500).

You can download the calculator for planning income for 2 years here.

You can download the calculator for planning income for 2 years here.

If you’ve said “I lost my job and have no money”, start small — even a ₹500 SIP in mutual funds can help you stay invested and mentally focused on rebuilding.

Consider your first income after job loss as a seed to restart your investment journey.

Reinvest small returns instead of spending them.

And remember, even if you’re employed, you can withdraw your PF amount while working partially during emergencies — it’s better than taking high-interest personal loans.

3. Stop worrying

“Worry never robs tomorrow of its sorrow, it only saps today of its joy.” – Leo F. Buscaglia

Do not worry about the tax liability or other financial goals right now.

When the situation improves you can rethink about these.

Focus only on things that you can control now.

During uncertain times like job loss, worrying won’t pay your bills — but smart investing can.

If you’re wondering how to generate income without a job, start by exploring investments made to earn regular income through low-risk mutual funds and liquid assets.

Remember, even if you have lost your job and have no money, you can begin small — a disciplined SIP or SWP can be your steppingstone towards rebuilding financial confidence.

4. Get help

Can you get help during these times?

Yes, it’s never wrong to get help, find a mentor, and reach out. If you need to consult a financial advisor, please go ahead, don’t hesitate.

Benefit: You will be able to get proper guidance and you wouldn’t jump into wrong conclusions.

Professional financial advisors can help you choose the right retirement plans or pension schemes in India that allow partial withdrawals — like when you wonder, “can I withdraw my PF amount while working?” or how to reinvest it wisely during a crisis.

A Certified Financial Planner (CFP) can also teach you how to invest so you don’t have to work endlessly for income.

With a mix of mutual funds, debt instruments, and dividend-paying stocks, you can make your money work for you instead of the other way around.

Conclusion

Economic disruption from AI, automation, or corporate restructuring may affect your finances, but these challenges can be managed with smart planning

Do follow the above steps to earn a regular income for two years, reduce unnecessary expenses, and make informed investment choices.

Smart people would have started cutting down their unnecessary expenses and started investing.

Are you also one of them? Have you started investing?

Stay home! Stay safe! Wear mask! Get vaccinated!

Remember — every smart investment today can save you from panic tomorrow.

Whether it’s how to generate income without a job or job investment strategies to stay financially stable, the secret is to start now, stay consistent, and trust the process.

Even if you’re struggling after a job loss, it’s never too late to start your journey toward financial independence — your first income from investments may arrive sooner than you think.

Be proactive, not reactive — a holistic investment approach ensures that even during difficult times, your financial life stays balanced, sustainable, and growth-oriented.

If you have any comments or questions, write them in the comment box below.

Or are you interested in creating a Comprehensive Financial Plan for your financial goals?

Skip the queue by registering for your 30 Minute FREE Financial Plan Consultation. Click the ‘‘BOOK YOUR SLOT NOW!’’ button below.

Leave a Reply