A majority of our financial life is spent looking for opportunities to create wealth that will serve us for a lifetime.

However, what’s equally important is to find investment instruments that can give capital protection and also beat inflation. Such investment opportunities are almost impossible to find.

In This Article:

1. Features of ICICI Prudential Guaranteed Wealth Protector Plan

2. Fund Options in ICICI Pru Guaranteed Wealth Protector Plan

3. Benefits of ICICI Prudential Guaranteed Wealth Protector Plan

4. ICICI Pru Guaranteed Wealth Protector Review of Benefits with Illustration

5. Charges in ICICI Pru Guaranteed Wealth Protector

6. Comparison of ICICI Pru Guaranteed Wealth Protector Benefits against PPF

7. Comparison of ICICI Pru Guaranteed Wealth Protector Benefits against ELSS Mutual Fund

8. How to Surrender Your ICICI Pru Guaranteed Wealth Protector?

9. Verdict

It demands you to be well-planned and vigilant while investing.

ICICI Guaranteed Wealth Protector is a unit linked insurance policy that promises the potential for high returns, by investing a portion of the premium in equity, while also promising capital guarantee and life cover.

Is capital guarantee even possible along with the potential for high returns?

Can the ICICI Pru Guaranteed Wealth Protector deliver what it claims to offer?

Let us find out in this detailed ICIC Pru Guaranteed Wealth Protector Review.

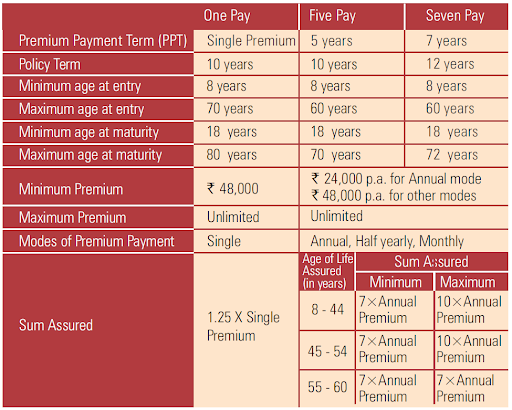

Features & Eligibility-ICICI Pru Guaranteed Wealth Protector Plan

ICICI Pru Guaranteed Wealth Protector comes with 3 policy options in terms of the premium payment.

Investors may choose to pay their premium as a single payment or over a 5 or 7 year period.

The ICIC Pru Guaranteed Wealth Protectors offers a policy term of 10 years for One Pay and 5 Pay options, whereas the 7 Pay option has a policy term of 12 years. There are no other policy term options available in this policy.

The following table shows the eligibility criteria and other features of the ICICI Pru Guaranteed Wealth Protector.

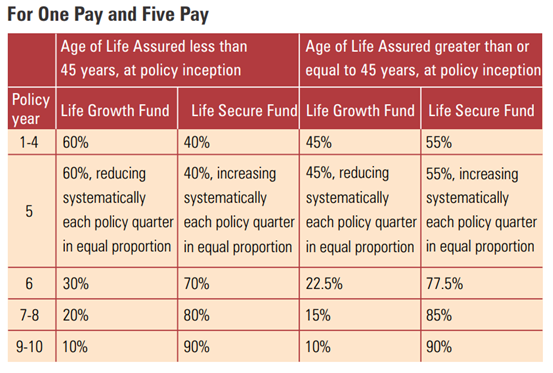

Fund Options in ICICI Pru Guaranteed Wealth Protector Plan:

The ICICI Pru Guaranteed Wealth Protector Plan offers only 2 different fund options.

The Life Growth Fund is meant for capital growth by investing predominantly in equity & related securities. Meanwhile, the Life Secure Fund is meant for capital protection by investing in fixed-income securities.

The ICICI Pru Guaranteed Wealth Protector plan does not give many fund options to the investor. In addition, it restricts the investors by following its own investment strategy.

See the tables below for the “Guaranteed Wealth Protector Strategy” followed by the policy under different policy options.

The drawback of “Guaranteed Wealth Protector Strategy” is explained in the benefits review section.

Benefits of ICICI Prudential Guaranteed Wealth Protector Plan:

Like any other investment insurance policy, the ICICI Pru Guaranteed Wealth Protector offers the Death benefit and Maturity Benefits.

a) Death Benefit

In case of the policyholder’s death during the policy term, the nominee will receive the highest of the following

- Sum Assured

- Minimum Death Benefit (105% of total premium paid)

- Fund Value

b) Maturity Benefit

If the policyholder sustains the entire period of the policy, then the policyholder will get the highest of the following –

- Loyalty Additions and Wealth Booster (including Fund value)

- Assure Benefits (101% of single premium in case of one pay and 101% of all the premium paid in case of five and seven pay.)

c) Wealth Booster

At the end of the 10th policy year, extra units are added to the policy as Wealth Boosters.

The extra units are calculated as a percentage of the average units of the fund on the last day of the last eight policy quarters.See the table below for the wealth booster percent of different policy options.

f) Surrender Benefit

Policyholders can surrender the ICICI Pru Guaranteed Wealth Protector plan only after the completion of 5 years of the term. On surrendering, the policyholder will receive the fund value as on date.

ICICI Pru Guaranteed Wealth Protector Review of Benefits with Illustration

Any investment insurance can offer a range of benefits under different conditions to lure in customers.

But from an investor’s perspective, what matters most is the potential return from the investment on policy maturity. Keeping that in mind, let’s put the ICICI Pru Guaranteed Wealth Protector to test by calculating the potential returns from this policy.

Let’s say you are buying the ICICI Pru Guaranteed Wealth Protector plan with the 7 Pay policy option. And you are paying ?1 lakh per annum as the policy premium.

In this case, assuming the funds in this policy are earning at 8% CAGR, you will receive the maturity amount of ?11.01 Lakhs. This data is as per the policy brochure from the official ICICI Prudential website.

See the illustration of premium payment and the maturity benefit cash flow in the table below.

See or download the policy brochure for more details from the official website here: ICICI Pru Guaranteed Wealth Protector PDF.

A Maturity benefit of ?11 Lakhs for an investment of ?7 Lakhs may look like a good investment. But when we look at the cash flow and calculate the IRR, it is not the case.

An IRR of 5.1% for 12 long years is a below-average return for the investment options available today. Because the ICICI Pru Guaranteed Wealth Protector is a ULIP policy, it is a poor investment option for the risk and the illiquidity involved.

Even Fixed Deposits offer a better return rate for far lesser investment risk.

Drawbacks of the “ICICI Pru Guaranteed Wealth Protector Strategy”:

The ICICI Pru Guaranteed Wealth Protector is an equity market-linked investment insurance. And since the equity markets are very volatile, a market crash in the long-term is inevitable.

In such a volatile scenario, the most nonsensical “strategy” is to follow a pre-set asset allocation strategy like in the ICICI Pru Guaranteed Wealth Protector.

For example, in the 7Pay policy option, 30% of the equity investment is allocated to the Debt fund (Life Secure Fund) during the 7th year alone.

Now imagine the market crashes by 38% during that period. Any rational investor will know that you should not sell your equity holdings until the market recovers.

But in the case of ICICI Pru Guaranteed Wealth Protector, your policy will book loss by selling your equity holdings. It is against the fundamentals of investing principles.

The “Guaranteed Wealth Protector Strategy” is a riskier strategy for any investor.

Along with these, one of the many reasons for this below-average return rate, “Guaranteed Wealth Protector Strategy” is the different charges in this policy.

Take a quick look at the different charges in ICICI Pru Guaranteed Wealth Protector affecting the potential returns.

Charges in ICICI Pru Guaranteed Wealth Protector

a) Premium Allocation Charge:

It is levied on the premium amount at the time of premium payment and units are allocated in the funds thereafter. The premium allocation charges are as follows:

- For One Pay Option: the premium allocation charge is 3%.

- For Five and Seven Pay Option: It is levied as in the table below,

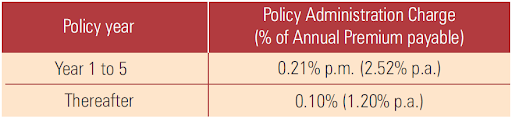

b) Policy Administration Charge:

It will be a maximum of ? 500 per month, taken every month by redemption of the fund units.

- For One Pay Option:It is ? 720 p.a. for the first five policy years.

- For Five and Seven Pay Option: The charges are as shown in the table below,

c) Mortality Charges:

It is levied every month by redemption units to provide life cover for the policyholder. The table shows the annual charges for sum assured of?10 Lacs, per thousand life cover.

Comparison of ICICI Pru Guaranteed Wealth Protector Benefits against PPF

In the Guaranteed Wealth Protector Review of benefits above, we calculated the actual Return Rate from the benefit as suggested by ICICI Pru illustration.

The conclusion was that the ICICI Pru Guaranteed Wealth Protector is a below-average investment option.

How true is that statement? Do the numbers support it?

Let’s find out by calculating the potential returns, assuming the same ?1 Lakhper annum for 7years is invested in PPF.

I am aware that PPF has a lock-in period of 15 years and one must invest a minimum of ?500 a year to keep it active. Also, the PPF interest rate for the Q2 2021-22 is set at 7.1%p.a.

Considering these factors, and to make this as close a fair comparison against the ICICI Pru Guaranteed Wealth Protector, the PPF investment is as shown in the table below.

In the table, you may notice that at the end of the 12th year (maturity period for the ICICI Pru GWP), your PPF investment could have earned an assured return of more than ?13 Lakhs.

It is ?2Lakhs more than the maturity benefit from the ICICI Pru Guaranteed Wealth Protector. Clearly, PPF is a better investment option.

The fact that the PPF investments are assured by the Govt. of India, unlike any ULIP policy, is an advantage.

Taxation factor: The ICICI Pru Guaranteed Wealth Protector premiums are tax exempted under section 80C of the Income Tax Act, 1961. Also, the maturity benefits are exempted u/s 10(10D), provided it meets the required conditions.

One of the best things about the PPF is that it has an EEE tax status. The investment, interest earned, and maturity benefits are all exempt from the income tax.

In the investment and the taxation aspects, PPF has an edge over the ICIC Pru Guaranteed Wealth Protector. However, PPF does not offer life cover like ICICI Pru Guaranteed Wealth Protector.

If life insurance is your major concern, you can buy a term insurance plan by paying a far lesser premium for the same sum assured.

You can have your life covered, earn better and assured returns than ICICI Pru Guaranteed Wealth Protector. If you are a risk-averse investor, consider the PPF+ a term insurance policy option first.

Comparison of ICICI Pru Guaranteed Wealth Protector Benefits against ELSS Mutual Fund

For this comparison, let’s consider an average ELSS Mutual Fund.

The risk potential of an ELSS Mutual Fund is practically the same as any ULIP policy since both invest in equity and related securities.

The investment is ? 1 Lakh per annum for 7 yearsand kept invested until the completion of the 12th year.

Assuming a conservative 12% CAGR for the ELSS mutual fund, the return is shown in the table below. The growth is assumed to be steady, rather than intermittent, for illustration purposes.

You can see, the fund value of the ELSS Mutual Fund is almost ?20 Lakhs by the end of the 12th year.

It is almost ?9 Lakhs more than the maturity benefit of ICICI Pru Guaranteed Wealth Protector illustration. In addition, it also has the lowest lock-in period of 3 years, in contrast with the 5 years of the ICICI Pru Guaranteed Wealth Protector.

Taxation of ELSS Mutual Fund & Post-Tax returns:

ELSS Mutual Fund gives tax benefits for investments up to ?1.5 Lakhs per annum, under section 80C of IT Act, 1961.

The returns, on the other hand, are levied an LTCG tax at 10%, with an exemption of redemptions up to ?1Lakhs.

For example, from the table, the capital gain from the fund is ?12.9 Lakhs. Out of this, ?1 Lakh is exempted from LTCG tax. Hence, @ 10%, the tax payable will be only ?1.19 Lakhs.

I.e. even after the taxation, the return from an average performing ELSS Mutual Fund scheme would be around ?18 Lakhs.

It is still ?7 Lakhs more than the return from the ICICI Pru Guaranteed Wealth Protector plan. Moreover, if we consider the indexation benefits in this calculation, the tax payable will be even lesser and returns in the hands of the investor will be even more.

On the investment side, ELSS Mutual Fund investment is a far better option for the investors. As seen with the PPF, ELSS Mutual Fund does not offer the life cover either.

Alternatively, you can buy a term insurance plan for the same life cover as in the ICICI Pru Guaranteed Wealth Protector. Term insurance policies offer a higher sum assured amount for far less premium.

For a risk-tolerant investor, ELSS Mutual Fund along with a Term Insurance plan for life cover is a better option.

But what if you have already bought the ICICI Pru Guaranteed Wealth Protector?

If you have already bought this policy, surrendering it may still allow you to get the best from thesebetter alternate options.

How to Surrender Your ICICI Pru Guaranteed Wealth Protector?

If you’ve just bought this policy, you have an easy way out.

Surrendering during the Free-look Period:

IRDA gives the policyholders the option of surrendering the policy to the company within 15 days from the date of purchase. It is 30 days if the policy is purchased online.

Your premium amount will be returned to you minus any stamp duty charges and a little risk cover charge during this period.

Surrendering after the Free-look Period:

You cannot surrender your ICICI Pru Guaranteed Wealth Protector policy since ULIP policies have a lock-in period of 5 years. You can surrender it on completion of 5 policy years.

However, the market scenario also plays a role in the surrender amount you get.

Hence,it is strongly recommended to consult a Certified Financial Planner or a Financial Advisor to make the right decision so you don’t lose money.

Steps to surrender ICICI Pru Guaranteed Wealth Protector

To surrender your ICICI Pru Guaranteed Wealth Protector, you need to submit a filled surrender form along with the documents listed below at the nearest ICICI Pru branch.

- Original policy documents

- Cancelled cheque/Bank statement with the policyholder’s name on it

- ID proof such as (PAN Card, Aadhaar Card, Passport, Driving License, Voters ID)

- Policy surrender or cancellation form

- Latest contact details

Verdict

By now, I presume that you are already aware of the right decision.

Do Not Invest in ICICI Pru Guaranteed Wealth Protector policy when you have better investment and insurance options.

It is below average as an investment; also as an insurance product. PPF with guaranteed returns gives better returns, even if by a small margin. Considering the risk factor, PPF is better than it appears.

On the higher risk category, on equal terms, an average performing ELSS Mutual Fund outranks the ICICI Pru Guaranteed Wealth Protector by a big margin.

Before investing in any instrument, analyse the product before you invest.

Ask the right questions and look for better alternatives. If you find it too complicated to make a quick rational decision, consult your financial advisor.

You can also register for our FREE 30 Minute Consultation by clicking the button below and talk to a Certified Financial Planner.

Thanks for the detailed review of this worst product which I had bought in 2016.

I invested Rs.1.2 lakhs / year for 5 years (i.e: 6 L altogether) . 7 years have gone.

Without knowing this much fact, I was attracted by the marketing executive’s key word: ‘ Rs.12 L death benefit’.

Due to my health condition at that time, I took this bad decision. Now I have realised after your article that this is the worst product. Can you please suggest me some other better investment with this 6 L / (+some 66K is gained as the interest now). Thanks in advance. Any charges for your services, I will be happy to bear.