Are you looking forward to investing in SBI Life Smart Privilege Plan?

Do you believe that this plan will offer you the perfect blend of both Insurance and Investment benefits?

But is it true that SBI Life Smart Privilege Plan is a smart solution for your financial goals and needs?

Are you in a dilemma about whether SBI Life Smart Privilege Plan gives you the returns that you calculate for your future?

The core desire or financial goal of every breadwinner is to make their family financially secure even in their absence.

Will SBI Life Smart Privilege Plan provide a smart solution for your family’s financial goals and needs?

In this article, let’s do a comprehensive Analysis of the SBI Life Smart Privilege Plan and discuss its Advantages (Pros) and Disadvantages (Cons) in detail.

In this SBI Life Smart privilege review, we also calculate the Internal Rate of the plan and compare it with other investment products to help you make informed investment decisions.

In this Article:

1.What is SBI Life Smart Privilege Plan?

2.What are the Eligibility Criteria of SBI Life Smart Privilege Plan?

3.What are the Key Features of SBI Life Smart Privilege Plan?

4.Various Fund Options In SBI Life Smart Privilege Plan

5.Benefits of the SBI Life Smart Privilege Plan

6.SBI Smart Privilege Plan Benefit Illustration

7.Various Charges in SBI Life Smart Privilege Plan

8.SBI Life Smart Privilege Plan – Pros and Cons

9.SBI Life Smart Privilege Plan VS Other Investments

10.SBI Life Smart Privilege Plan VS PPF / Equity Mutual Fund?

11.SBI Smart Privilege Plan – Good or Bad

12.How to Surrender / Cancel Your SBI Life Smart Privilege Plan?

13. SBI Life Smart Privilege for NRI Investors – Is It Suitable?

14. Who Should Avoid SBI Smart Privilege Plan?

15.Final Verdict on SBI Life Smart Privilege Plan?

What is SBI Life Smart Privilege Plan?

SBI Life Smart Privilege Plan is a Unit-Linked Investment Insurance Plan (ULIP) believed to be specifically designed for this purpose.

At least that is how it is presented to the investors.

SBI Life Smart Privilege is a Long Term Investment Product with a minimum policy term being 5 years.

By the end of this review, you will have absolute clarity on whether SBI Life Smart Privilege Plan is good or bad —the actual benefits and returns from the policy.

And whether or not you have alternatives that are better in every aspect.

When evaluating what is SBI smart privilege, it is important to understand that this is a market-linked ULIP where returns depend on fund performance and not guaranteed interest rates like traditional SBI life fixed deposit plan options.

Without any further ado, let’s start with the eligibility and other features of the SBI Life Smart Privilege plan.

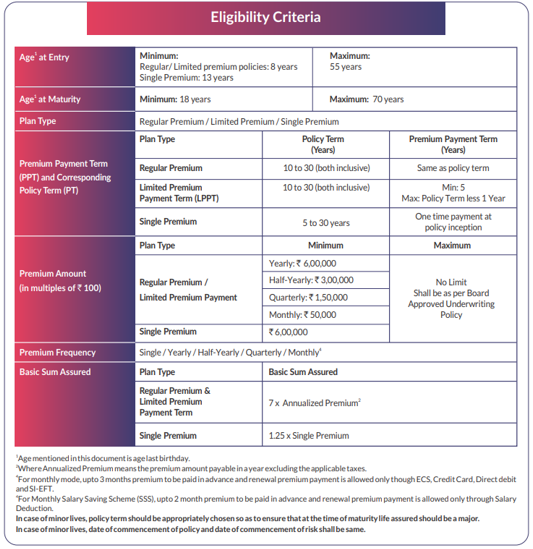

What are the Eligibility Criteria of SBI Life Smart Privilege Plan?

The lowest policy term available for SBI Life Smart Privilege is 5 years, and it differs based on the different plan options and eligibility criteria.

The table below the different eligibility criteria for different plan options and other features of the SBI Life Smart privilege plan.

What are the Key Features of SBI Life Smart Privilege Plan?

- You have the flexibility to choose between Single Pay/ Limited Pay options.

- No premium allocation charge from the 6th policy year onwards.

- loyalty additions start from the end of the 6th policy year.

- The policyholder gets the option of unlimited free switches between the available 11 funds like midcap funds, balanced funds, equity funds, etc.

- There are a total of 11 Fund Options available under SBI Smart Privilege.

- SBHI Life Smart privilege offers unlimited Free Switches.

- Tax benefit under section 80C of the Income Tax Act, 1961. The maximum deduction that can be claimed under this section during a financial year is Rs.1,50,000.

Take a look at this short video that covers all of the essential features of the SBI Life Smart Privilege plan.

Continue reading this article for more information to help you decide whether this SBI life policy is a good or bad investment choice for you.

Various Fund Options in SBI Life Smart Privilege Plan

SBI Smart Privilege plan enables the investors to choose from 11 different fund options.

The Risk profile and Asset Allocation varies according to the fund of your choice.

These funds range from low to medium-risk bond funds to high-risk pure equity funds.

So choose a fund that you feel is suitable for your financial needs and requirements.

The different funds offered by the SBI Life Smart Privilege plan are shown in the table below.

|

S.no |

Name of the fund |

Equity & Equity Related Instruments |

Debt Instruments |

Money Market Instruments |

Risk Profile |

|

1 |

Top 300 Fund |

60-100% |

0-40% |

0-40% |

High |

|

2 |

Balanced Fund |

40-60% |

0-40% |

20-60% |

Medium |

|

3 |

Bond Fund |

– |

60-100% |

0-40% |

Low to Medium |

|

4 |

Equity Optimiser Fund |

60-100% |

0-40% |

0-40% |

High |

|

5 |

Bond Optimiser Fund |

0-25% |

75%-100% |

0-25% |

Low to Medium |

|

6 |

Money Market Fund |

– |

0-20% |

80-100% |

Low |

|

7 |

Equity Fund |

80-100% |

0-20% |

0-20% |

High |

|

8 |

Growth Fund |

40-90% |

10-60% |

0-40% |

Medium to High |

|

9 |

Pure Fund |

80-100% |

– |

0-20% |

High |

|

10 |

Midcap Fund |

80-100% |

0-20% |

0-20% |

High |

|

11 |

Corporate Bond Fund |

70-100% |

0-30% |

0-30% |

Low to Medium |

|

Discontinued Policy Fund |

– |

60-100% |

0-40% |

Low |

The minimum and maximum percentage contributions of different funds are calculated in the above table.

Among all options, the SBI life smart privilege midcap fund often attracts investors seeking higher growth, but a closer look at SBI smart privilege midcap fund review and performance trends shows that higher volatility can impact consistency of returns over time.

Benefits of the SBI Life Smart Privilege Plan

Since SBI Life Smart Privilege is a ULIP policy, you can receive the policy benefit is either a death benefit or a Maturity (read survival) benefit.

a) SBI Life Smart Privilege Plan Death Benefit: On the unprecedented demise of the policyholder while the policy is active, the beneficiary or nominee will receive the highest of the below:

- Fund Value as on the date of death intimation or

- The basic sum assured less APW (Applicable Partial Withdrawals),

OR - 105% of total premiums received up to the date of death less APW

In the case of minor lives, the date of commencement of policy and date of commencement of risk can be the same and the policyholder/proposer can be parents or legal guardian, which shall be as per board-approved underwriting policy.

The nominee or the beneficiary (legal heir) has the option to receive death benefit by choosing from the 2 options available.

1. Receive death benefit as a lump sum or

2. In instalments over 2 to 5 years under “settlement option”. It can be done as yearly, half-yearly, quarterly, or monthly pay-outs as required.

(During the settlement period, the policyholder has to bear the investment risk in the investment portfolio).

b) SBI Life Smart Privilege Plan Maturity Benefit:

On surviving the policy term, the policyholder will receive the accumulated fund value as a lump sum.

However, under the settlement option, the policyholder can receive the maturity benefit in instalments.

Let’s take a deeper look into the maturity benefits by calculating the IRR of SBI Life Smart Privilege to, analyse its effectiveness.

SBI Smart Privilege Plan Benefit Illustration

As we have seen in SBI Life Smart Privilege Plan the investors can choose from 11 different funds.

Since it is said that Equity Funds have the potential to deliver higher returns.

Let’s find out the Internal Rate of Return (IRR) of SBI Life Smart Privilege Plan by opting for an Equity Fund as an example.

Suppose an investor buys the SBI Life Smart Privilege plan with a policy term of 15 years and invests ₹6 lakhs per annum.

And here 100% of exposure is to only be given to equity funds under the SBI Life Smart Privilege Plan.

The returns illustration from the official SBI Life Smart Privilege Plan Calculator is shown in the table below.

|

Male |

30 years |

|

Sum Assured |

₹ 1,05,00,000 |

|

Policy Term |

20 years |

|

Premium Paying Term |

20 years |

|

Annualised Premium |

₹ 15,00,000 |

|

At 4% p.a. |

At 8% p.a. |

||||

|

Age |

Year |

Annualised premium / Maturity benefit |

Death benefit |

Annualised premium / Maturity benefit |

Death benefit |

|

30 |

1 |

-15,00,000 |

1,05,00,000 |

-15,00,000 |

1,05,00,000 |

|

31 |

2 |

-15,00,000 |

1,05,00,000 |

-15,00,000 |

1,05,00,000 |

|

32 |

3 |

-15,00,000 |

1,05,00,000 |

-15,00,000 |

1,05,00,000 |

|

33 |

4 |

-15,00,000 |

1,05,00,000 |

-15,00,000 |

1,05,00,000 |

|

34 |

5 |

-15,00,000 |

1,05,00,000 |

-15,00,000 |

1,05,00,000 |

|

35 |

6 |

-15,00,000 |

1,05,00,000 |

-15,00,000 |

1,05,00,000 |

|

36 |

7 |

-15,00,000 |

1,05,00,000 |

-15,00,000 |

1,05,00,000 |

|

37 |

8 |

-15,00,000 |

1,05,00,000 |

-15,00,000 |

1,05,00,000 |

|

38 |

9 |

-15,00,000 |

1,05,00,000 |

-15,00,000 |

1,05,00,000 |

|

39 |

10 |

-15,00,000 |

1,05,00,000 |

-15,00,000 |

1,05,00,000 |

|

40 |

11 |

-15,00,000 |

1,05,00,000 |

-15,00,000 |

1,05,00,000 |

|

41 |

12 |

-15,00,000 |

1,05,00,000 |

-15,00,000 |

1,05,00,000 |

|

42 |

13 |

-15,00,000 |

1,05,00,000 |

-15,00,000 |

1,05,00,000 |

|

43 |

14 |

-15,00,000 |

1,05,00,000 |

-15,00,000 |

1,05,00,000 |

|

44 |

15 |

-15,00,000 |

1,05,00,000 |

-15,00,000 |

1,05,00,000 |

|

45 |

16 |

-15,00,000 |

1,05,00,000 |

-15,00,000 |

1,05,00,000 |

|

46 |

17 |

-15,00,000 |

1,05,00,000 |

-15,00,000 |

1,05,00,000 |

|

47 |

18 |

-15,00,000 |

1,05,00,000 |

-15,00,000 |

1,05,00,000 |

|

48 |

19 |

-15,00,000 |

1,05,00,000 |

-15,00,000 |

1,05,00,000 |

|

49 |

20 |

-15,00,000 |

1,05,00,000 |

-15,00,000 |

1,05,00,000 |

|

50 |

4,19,57,263 |

6,57,50,750 |

|||

|

IRR |

3.10% |

6.99% |

|||

From the official SBI Life Smart Privilege Plan Calculator, the maturity benefit illustration for the SBI Life Smart Privilege plan suggests that the policyholder will earn a maturity benefit of ₹6.57 Crores.

This return is calculated by assuming that the underlying fund earns @ 8% CAGR.

However, it should not have misunderstood as the IRR earned by the policyholder.

When we consider the different charges levied by the policy, the actual return rate in the hands of the policyholder is only 6.99%.

For 15 years Long Term Investment product with a big capital of ₹6 lakhs per annum, a return rate of 6.99% is below par and mediocre.

This Benefit Illustration clearly indicates that this SBI Life Smart Privilege Plan will not be a suitable investment product for your Long Term Financial Goals.

Furthermore, there is a High Agent Commission in this plan which makes it even more unattractive for Long Term Investors.

To achieve Long Term Financial Goals, you need an investment vehicle that surpasses inflation rate comfortably.

While the SBI life smart privilege maturity calculator provides an estimate of future value, it is based on assumed rates of return and does not account for real market fluctuations or policy-level deductions.

You can also use the SBI smart privilege returns calculator to estimate different premium scenarios, but it is important to understand that the SBI smart privilege returns shown in the illustration may differ significantly from actual outcomes due to policy charges and fund performance variations.

Many investors rely on SBI smart privilege calculator or smart privilege returns calculator tools, but these tools do not fully reflect the long-term impact of policy charges on final maturity value.

Various Charges in SBI Life Smart Privilege Plan

Like any other ULIP, the SBI Life Smart Privilege plan comes with a range of charges hidden under its benefits.

We have reviewed each charge separately for your better understanding

Here is the list of different charges of the SBI Life Smart Privilege Plan that may affect your calculated returns.

Premium Allocation Charge:

It is charged at 2.5% of the premium amount throughout the first 5 years of the policy term. No premium Allocation charge after the 6th Policy year.

Policy Administration Charge:

The Policy administration for SBI smart privilege as of now is subject to a cap of 500 rupees per month. However, the charges can be revised upon approval of IRDAI.

Fund Management Charges (FMC):

The SBI Smart privilege policy levies a predetermined percentage of the fund value as a fund management charge every year of the policy term.

|

S.no |

Name of the fund |

Fund Management Charge (p.a.) |

|

1 |

Top 300 Fund |

1.35% p.a. |

|

2 |

Equity Optimiser Fund |

1.35% p.a. |

|

3 |

Equity Fund |

1.35% p.a. |

|

4 |

Growth Fund |

1.35% p.a. |

|

5 |

Pure Fund |

1.35% p.a. |

|

6 |

Midcap Fund |

1.35% p.a. |

|

7 |

Balanced Fund |

1.25% p.a. |

|

8 |

Bond Fund |

1.00% p.a. |

|

9 |

Corporate Bond Fund |

1.15% p.a. |

|

10 |

Bond Optimizer Fund |

1.15% p.a. |

|

11 |

Money Market Fund |

0.25%p.a. |

|

Discontinued Policy Fund |

0.50% p.a. |

Discontinuance Charge:

Discontinued policies incur a charge as a percentage of the fund value in a staggered manner.

This percentage differs for each year for different policy options.

However, for the 5th policy year, there is no discontinuance charge.

Partial Withdrawal Charge:

The policyholder gets 2 free partial withdrawals in the same year.

For partial withdrawals above and beyond this limit, the policyholder will be charged ₹100 per withdrawal.

Switching Charge:

SBI Life Smart Privilege allows unlimited free switches between funds.

Premium Redirection Charge:

The Premium Redirection Charge of this SBI life smart privilege plan as of now is subject to a market cap of 500 rupees per transaction. However, charges can be revised on approval of IRDAI.

Mortality Charge:

It is deducted on the 1st business day of each policy month from the fund value by the cancellation of units.

Mortality charge varies depending on the age of the policyholder and the sum assured.

When evaluating SBI life smart privilege charges in detail, it becomes evident that these layered costs can significantly reduce the effective SBI smart privilege returns, especially in the initial years when allocation and administration charges are higher.

At this stage, many investors question is SBI smart privilege good as an investment option, and the answer largely depends on whether you prioritise convenience over return efficiency in long-term financial planning.

A deeper look into SBI life smart privilege charges shows that premium allocation charges, fund management charges, and mortality costs collectively reduce the effective SBI smart privilege returns over time.

SBI Life Smart Privilege Plan – Pros and Cons

Is the SBI Life Smart Privilege Plan really a privilege for you and your family?

To find out this, let us evaluate the pros and cons of this SBI Privilege Plan.

Advantages of the SBI Life Smart Privilege Plan

A. Tax Benefit – By purchasing this policy, the policyholder gets tax benefit u/s 80C of the Income Tax Act, 1945.

B. Grace Period – This 30 days’ grace period will be allowed for premiums paid yearly, half-yearly, and quarterly. Whereas, only 15 days will be allowed in the monthly premium phase.

C. Switching Option – Even during the policy term and settlement period, you can switch your investments among the 11 funds available to meet your changing investing needs.

D. Diverse Funds – SBI Life Smart Privilege Plan allows you to invest in diverse funds such as equity funds, midcap funds, balanced funds, etc.

Disadvantages of the SBI Life Smart Privilege Plan

- A premium top-up facility is not allowed in this policy under any circumstances.

- Under any circumstances, the policyholder cannot take a loan against this policy

- The funds under the SBI Life Smart Privilege plan lack the transparency that is offered by the standard mutual funds regulated by SEBI.

- The returns offered by the SBI Life Smart Privilege plan are below par.

You should look to gain insights of potential returns of the plan before choosing it as your investment vehicle.

To evaluate the returns from SBI Life Smart Privilege, let’s compare how this plan will fare against different investment options.

A closer look at SBI life smart privilege disadvantages highlights factors such as lock-in period, multiple charges, and relatively lower return potential compared to other market-linked investment options.

SBI Life Smart Privilege Plan Vs Other Investments

When we calculated the potential return of the SBI Life Smart Privilege Plan, we found out that it has offered only 6.74% IRR, even if the underlying funds earned 8% CAGR in the illustration above.

So now let’s do a comparison with other investments for investment choices.

SBI Life Smart Privilege Plan VS PPF / Equity Mutual Fund?

For life coverage, a pure-term insurance policy with a sum assured of ₹1 crore costs ₹7,500 annually for a 20-year term.

In comparison, the SBI Life Smart Privilege Plan premium was ₹15 lakhs.

By opting for a term plan, the remaining ₹14.92 Lakhs can be allocated to investments.

|

Pure Term Life Insurance Policy |

|

|

Sum Assured |

₹ 1,05,00,000 |

|

Policy Term |

20 years |

|

Premium Paying Term |

20 years |

|

Annualised Premium |

₹ 7,500 |

|

Investment |

₹ 14,92,500 |

|

Term Insurance + PPF |

Term insurance + Equity Mutual Fund |

||||

|

Age |

Year |

Term Insurance premium + PPF |

Death benefit |

Term Insurance premium + Equity Mutual Fund |

Death benefit |

|

30 |

1 |

-15,00,000 |

1,05,00,000 |

-15,00,000 |

1,05,00,000 |

|

31 |

2 |

-15,00,000 |

1,05,00,000 |

-15,00,000 |

1,05,00,000 |

|

32 |

3 |

-15,00,000 |

1,05,00,000 |

-15,00,000 |

1,05,00,000 |

|

33 |

4 |

-15,00,000 |

1,05,00,000 |

-15,00,000 |

1,05,00,000 |

|

34 |

5 |

-15,00,000 |

1,05,00,000 |

-15,00,000 |

1,05,00,000 |

|

35 |

6 |

-15,00,000 |

1,05,00,000 |

-15,00,000 |

1,05,00,000 |

|

36 |

7 |

-15,00,000 |

1,05,00,000 |

-15,00,000 |

1,05,00,000 |

|

37 |

8 |

-15,00,000 |

1,05,00,000 |

-15,00,000 |

1,05,00,000 |

|

38 |

9 |

-15,00,000 |

1,05,00,000 |

-15,00,000 |

1,05,00,000 |

|

39 |

10 |

-15,00,000 |

1,05,00,000 |

-15,00,000 |

1,05,00,000 |

|

40 |

11 |

-15,00,000 |

1,05,00,000 |

-15,00,000 |

1,05,00,000 |

|

41 |

12 |

-15,00,000 |

1,05,00,000 |

-15,00,000 |

1,05,00,000 |

|

42 |

13 |

-15,00,000 |

1,05,00,000 |

-15,00,000 |

1,05,00,000 |

|

43 |

14 |

-15,00,000 |

1,05,00,000 |

-15,00,000 |

1,05,00,000 |

|

44 |

15 |

-15,00,000 |

1,05,00,000 |

-15,00,000 |

1,05,00,000 |

|

45 |

16 |

-15,00,000 |

1,05,00,000 |

-15,00,000 |

1,05,00,000 |

|

46 |

17 |

-15,00,000 |

1,05,00,000 |

-15,00,000 |

1,05,00,000 |

|

47 |

18 |

-15,00,000 |

1,05,00,000 |

-15,00,000 |

1,05,00,000 |

|

48 |

19 |

-15,00,000 |

1,05,00,000 |

-15,00,000 |

1,05,00,000 |

|

49 |

20 |

-15,00,000 |

1,05,00,000 |

-15,00,000 |

1,05,00,000 |

|

50 |

6,62,49,967 |

10,91,34,380 |

|||

|

IRR |

7.06% |

11.17% |

|||

Investment choices can align with your risk tolerance:

– Risk-averse investors may prefer debt options like PPF.

– Risk-tolerant investors can explore equity-focused investments like Equity Mutual funds.

- PPF Investment:

The annual PPF investment threshold is ₹1.5 lakhs, but for this illustration, we assume the full balance is invested.

– Estimated Maturity Value: ₹6.62 crores

– IRR: 7.06%

This surpasses the 8% return scenario of the SBI Life Smart Privilege Plus despite being a low-risk debt instrument.

- Equity mutual fund Investment:

– Estimated Pre-tax Maturity Value: ₹12.04 crores

– Post-tax Maturity Value (after capital gains tax): ₹10.91 crores

– Post-tax IRR: 11.17%

|

Equity Mutual Fund Tax Calculation |

|

|

Maturity value after 30 years |

12,04,42,863 |

|

Purchase price |

2,98,50,000 |

|

Long-Term Capital Gains |

9,05,92,863 |

|

Exemption limit |

1,25,000 |

|

Taxable LTCG |

9,04,67,863 |

|

Tax paid on LTCG |

1,13,08,483 |

|

Maturity value after tax |

10,91,34,380 |

Both scenarios demonstrate that separating insurance from investment results in significantly higher returns compared to the SBI Life Smart Privilege Plan.

This approach highlights the advantages of using a pure-term insurance policy for protection and investing the surplus in more efficient financial instruments to maximize wealth accumulation.

When comparing SBI life smart privilege vs mutual fund, the difference in cost structure and transparency becomes clear, as mutual funds typically offer better flexibility and potentially higher risk-adjusted returns.

The intent of writing this post is to inform you about the investment aspects of this plan and to evaluate if SBI Smart Privilege Plan is a good or bad investment for you.

Let us share our final thoughts about the same in the next section.

SBI Smart Privilege Plan – Good or Bad?

Considering and comparing the alternative options in all aspects, it’d be wise for an investor to Not Invest in the SBI Life Smart Privilege plan.

The following are 5 good reasons to avoid Investing in SBI Smart Privilege Plan.

- PPF investment with a Term Insurance plan is a better alternative for investors with no or lesser risk tolerance.

- On the other hand, the Equity Mutual Fund with Term Insurance plan is a better alternative for investors with a certain level of risk tolerance and investment discipline.

- One may argue that the SBI Life Smart Privilege Plan is more likely to generate higher returns. However, in reality the returns of SBI Smart Privilege are not even able to match with the Debt Instrument Return.

- Consider this, the SBI Life Smart Privilege Plan is a long-term commitment of at least 5 years. Even if you choose to discontinue your policy, your investments will be moved to the Discontinued Policy Fund, earning a bare minimum of 4% per annum.

- There is no systematic compulsion on the policy’s fund manager to perform at his best all the time. However, with Equity Mutual Funds, the investor invests in a different funds at any time. This compels the fund managers to deliver better returns consistently.

If you have already bought the SBI Life Smart Privilege plan, you may want to consider surrendering it.

However, it is always wise to consult your financial or investment advisor to plot the optimal strategy that fits your requirements.

Click Here for SBI Smart Privilege Plan (एसबीआई लाइफ स्मार्ट प्लेटिना प्लस कैलकुलेटर) Review in Hindi

How to Surrender Your SBI Life Smart Privilege Plan?

i. Surrendering During the Free-look Period:

This SBI Life Smart Privilege policy has a free look period of 15 days if the policy is bought physically and 30 days if the policy is bought via digital marketing.

ii. Surrendering After the Free-look Period:

You can surrender the SBI Life Smart Privilege policy at any time during the policy term, once surrendered the policy cannot be revived

Procedure to surrender/Cancel your SBI Life Smart Privilege Plan:

If the policyholder wants to surrender his/her SBI Life Smart Privilege policy, the policyholder needs to submit reason(s) for Policy surrender and the surrender form needs to be submitted at the nearest SBI Life Insurance Branch, along with the following documents. They are as follows –

- Original policy documents

- Cancelled cheque with the policyholder’s name on it

- In case the cancelled cheque does not have a pre-printed name, or account number, or a new account is mentioned on the cheque, then the passbook copy/bank statement having the pre-printed name and the account number is required for review.

- ID proof (PAN Card, Aadhaar Card, Passport, Driving License, Voters ID)

- Policy surrender or cancellation form

- Contact details

If you are exploring SBI investment plans for 5 years, 10 years or even longer durations, it is essential to compare alternatives, as SBI smart privilege plan returns may not always justify the long-term commitment required.

Understanding SBI smart privilege policy exit options is crucial, as surrendering early can significantly impact returns due to discontinuance charges and lock-in restrictions.

SBI Life Smart Privilege for NRI Investors – Is It Suitable?

For investors considering SBI smart privilege for NRI, the plan offers exposure to Indian markets through ULIP funds like the SBI life smart privilege midcap fund.

However, returns are market-linked and affected by policy charges.

NRIs should compare SBI smart privilege returns with global investment options, keeping in mind taxation, currency risk, and repatriation rules.

Overall, while the SBI life smart privilege plan provides a combined insurance-investment structure, its lock-in and cost structure may limit flexibility for NRI financial planning.

Who Should Avoid SBI Smart Privilege Plan?

While the SBI Life Smart Privilege Plan is positioned as a long-term market-linked product, it may not be suitable for every investor profile.

Individuals who are primarily focused on high returns and efficient wealth creation may find this plan limiting, as the overall SBI smart privilege returns tend to be moderated by multiple charges and structural constraints.

Over long durations, these costs can dilute the compounding effect, making it less attractive compared to more transparent investment avenues.

Investors who prefer low-cost and flexible investment options should also be cautious.

Unlike direct equity or mutual funds, this plan involves policy-level restrictions such as lock-in periods and limited liquidity.

Even though fund switching is allowed, the overall structure lacks the flexibility that many modern investors expect when managing their portfolios actively.

Those seeking pure life insurance coverage at minimal cost may not benefit fully from this plan either.

A significant portion of the premium goes toward charges rather than pure risk cover, meaning the actual insurance protection may not be adequate when compared to a standalone term insurance policy.

Additionally, individuals who want complete transparency and control over their investments may find ULIP-based products like this less suitable.

The returns depend not only on market performance but also on internal policy charges, fund management decisions, and other variables that are not always straightforward to track.

Lastly, investors with short- to medium-term financial goals should avoid this plan.

Given the lock-in period and gradual impact of charges, it may not deliver optimal results within a shorter investment horizon, making it less aligned with near-term financial planning needs.

Conclusion

SBI Life Smart Privilege plan is an attractive ULIP policy for an uninformed investor.

But as a good investor, you should be skeptical about everything before choosing your investment product.

The purpose of this SBI Life Smart Privilege plan review is to help you find that conviction before you make any investment decision.

The illustration of the SBI Life Smart Privilege plan benefits and the illustration of the returns from the alternate options is evidence enough.

Think twice and again before you invest in any ULIP product and consult a financial advisor before you make that final call.

Some investors also evaluate SBI life smart privilege plus and smart privilege plus SBI life variants, but these plans follow a similar ULIP structure where returns are influenced by internal charges and fund performance.

Investors who seek high growth, low-cost structures, and greater transparency may find that SBI smart privilege plan is not the most efficient route for achieving long-term wealth creation goals.

Some investors also compare SBI life smart privilege plus review with this plan, but both variants follow a similar ULIP structure where returns are impacted by underlying charges and fund performance.

Please don’t conclude your review of the SBI Life Smart Privilege Plan by just surfing through social media sites like Quora, Facebook, Twitter, etc. It is always wise to take the help of a professional financial planner.

If you have any comments or questions, write them in the comment box below.

Are you interested in creating a Comprehensive Financial Plan for your financial goals?

Skip the queue by registering for your 30-minute FREE Financial Plan Consultation. Click the ‘‘BOOK YOUR SLOT NOW!’’ button below.

If I surender the policy after only 1 installment what amount can I get from 6lac

The surrender value depends on **when you surrender the policy**.

If you have paid only **one premium of ₹6 lakh** and surrender during the **first 5-year lock-in period**, you will **not receive the money immediately**. After deducting the applicable discontinuance charges, the balance amount is transferred to the Discontinued Policy Fund and will be paid only after completion of the lock-in period.

If you surrender **after the 5-year lock-in period**, you will generally receive the **prevailing fund value** (subject to policy terms and any applicable charges).

To give a more accurate estimate of how much you may receive, please share:

• Policy start year

• Current fund value

• Whether it is a Single Pay or Regular Pay policy

• Exact surrender date you are considering

Based on these details, we can help you estimate the likely surrender value.

I took the SBI Smart Privilege policy on 7th July 2021 with a yearly premium of Rs. 6 Lakh for 5 years of payment for a maximum 20-year period. In the next month i.e. July, the 4th premium is due but recently a financial planner told me to discontinue it as it has no longer remained a good one. He also said that no penalty would be imposed, and after 5 years, I’ll get the amount. He also suggested investing the remaining 2 installments of Rs. 6 lakh each in some good equity-based investment.

Please suggest what should i do now? whether to continue or discontinue it ? What would be current value as my plan is in BALANCED FUND and what would be the tentative value after 5 years and with the rate of interest ?

The Sbi smart privilege is far better than the comparisons given above, when the assurance value is the first highlight none others stand for comparison. Secondly this has lock in period for only 5 years and others have long term to wait for benefits, then it’s partially withdrawal others can’t. May be charges levied seem high but it’s it’s far better than other comparatives.

Pls calculate elss also at 8% CAGR and here the comparison with a classic product like ppf is not appropriate . One should be advised to continue investment of 1.50 lac in ppf and remaining in Ulip based product with additional benefit of insurance will definitely serve good .

While comparing with MF you have taken 12 percent assumed return why you have taken only 8 percent in case of smart previlige. I have seen policy holders getting 20percent return aswell. I don’t know how you drawn a comparison with ppf and smart previlige where return on smart previlige is not fixed and you haven’t made any try to show the returns received by the existing policy holders since it was mentioned in policy assumed rate at 8 percent you are trying to confirm that this fund cannot offer more than 8percent.

How logical it is?

Life Insurance policies usually project lower returns (~8%) because of higher fees and conservative growth strategies. In contrast, ELSS funds often target higher returns (~12%) due to their aggressive market exposure and lower expenses.

Comparing them at equal returns can be misleading; ULIP NAVs are pre-expense and don’t reflect actual net gains. Mutual Funds provide better transparency and net returns by post-expenses NAV, making them more attractive for growth-focused investors.

Hi Sir,

Greetings

Is the assured amount fixed for payout after policy term completion if I change my Fund type from Balanced to Equity Fund and irrespective of the Fund value based on market at maturity Policy Term

Dear sir,

I have taken the sbi life smart privilege policy plan of 10 years policy term with 5 years policy payment term of 10 lakhs each year for 5 years a. Sum assured is 70L.

So my question is at the end of 5 years can i withdraw the money and is teh 70L only after 10 years ?

Tried reading through teh T & C but did not get a clear answer

Is it even worth continuing as the bank I deal with said it was good and went ahead?

Can I continue this policy or not as per your suggestion or should i cancel?

Consulting your financial planner is essential. They will compare the benefits of continuing with the policy versus surrendering it and investing in mutual funds. If you convert to a paid-up policy, you retain some insurance coverage and accrued benefits. If you surrender and invest in MFs, you could potentially achieve higher returns, but this carries more risk. Your planner can project both scenarios to help you make an informed decision.

Do we have to factor in capital gains tax? Is SBI Life Smart Privilege exempt from LTCG because it is a ULIP?

You are correct. ULIPs, including SBI Life Smart Privilege, are exempt from Long-Term Capital Gains (LTCG) tax. When comparing ULIPs with ELSS (Equity Linked Savings Schemes), we consider the potential tax benefits of ULIPs. ELSS, on the other hand, is subject to LTCG tax. Despite this tax implication, ELSS historically offers competitive returns post-tax, often making it an attractive option for investors seeking tax-efficient equity investments compared to ULIPs.

I have taken smart privillege which gives you insurance and a return assurance, whereas term insurance with no return on investments, also MF don’t give insurance. So if you don’t have insurance than what is good. Further u can partial withdraw from 6th year but ppf can you withdraw without reason. Pls reply

Why didnt you mention about guaranteed additions which are given once in every five years and who said that there is no loan provision on privilege policy?

In this you have taken SBI LIFE PRIVILEGE PLAN RETURNS @ 8% which is as per IRDA regulation,shown in their website but what is the actual return they have been giving for their Midcap Fund & Equity Fund ? While searching in google it is showing more than 15% .

In the comparison you have shown Mutual Fund ELSS return above 12% ,tell me what is the guarantee for the same?

So if a prudent investor invest in SBI LIFE MID CAP fund for long term certainly he will get Good returns equal to more than ELSS and PPF.

YOU ARE SIMPLY MISGUIDING PEOPLE WITH FAKE OR PREJUDICED COMPARISONS.

Mutual funds, particularly ELSS, historically deliver competitive returns, typically around 12%, reflecting actual earnings post-expenses. In contrast, ULIP returns often advertised are pre-expenses, potentially misleading investors. This transparency underscores mutual funds’ advantage, providing clarity on net returns after deducting costs. Prudent investors prioritize this transparency and potential for higher returns when choosing investments aligned with their long-term financial goals and risk tolerance.

in this plan you invest only for 5 years, and in PPF you invest for 14 years, how can you compare ???

Hi, there are various PPT options available. And we have taken 15 years of PPT as an example in this policy. That’s why we used PPF for comparison.

Dear sir,

I have taken sbi life smart privilege policy plan of 20 years policy term with 5 years policy payment term of 10lakhs each year for 5 years and they kept it on sbi life balanced fund. Sun assured is 1 cr. But as per them it will generate funds in 20 years and provide me 2.5 crore at the end.

Can I continue this policy or not as per your suggestion I want to decide for my second policy term payment.

Since you have already taken this insurance plan, then you have two options.

Option: 1 You can surrender and encash the policy. And reinvest the surrender value and future premium money with better investment plans like PPF or MF.

Option: 2 You can continue with the insurance plan until the policy matures.

It is advisable to work out the outcome of both options and proceed with the better option.

80% of the times, option 1 is better.

You can consult a financial planner to choose the better option.

Or

You can take advantage of our free complimentary financial plan consultation and talk to our financial planners.

Get your appointment here: https://www.holisticinvestment.in/complimentary-financial-plan-consultation/

You can switch to Equity or Midcap fund and wait for 5-6 years ,it will give you good returns above 10% .Don’t get panic with PREJUDICED COMPARISONS

Dear holistic investment team, you have consider return of 8% and drawn a conclusion. Have you seen the fund performances, just see and again write this column, thease are more than 16%!!!

This is the power of market link schemes with taking risk, PPF cannot generate return of more than 7.1%.

While ULIPs may advertise returns of 16% or higher, it’s crucial to note that these figures are typically pre-expenses. Mutual funds, especially ELSS, historically offer competitive returns around 12% post-expenses, reflecting actual earnings after deducting costs. This transparency is key for investors in making informed decisions about net returns. Prudent investors prioritize understanding the true post-expense returns to align investments with their long-term financial goals and risk tolerance. Therefore, while high pre-expense returns can be enticing, it’s essential to consider the transparency and clarity offered by mutual funds when evaluating investment options.