2 in 1 is always an enticing offer.

And when it comes to investments, Protection, and Capital Growth attract investors.

ULIPs promise the investors this option of life risk cover as well as capital growth.

ICICI Prudential Elite Life Super Plan is one such ULIP to promise not only financial security but life cover.

What are the pros(advantages) and cons(disadvantages) of this ICICI Prudential Elite Life Super Plan?

Let’s analyze the different benefits provided by this plan from the policy details in the official brochure. We shall find out whether the ICICI Prudential Elite Life Super plan is a good or bad option in your investment portfolio.

Let’s get started!

Table of Contents:

1.)5 Steps of ICICI Pru Elite Life Super Plan Working Analysis

2.)Eligibility And Features of ICICI Pru Elite Life Super Plan Analysis

3.)Portfolio Strategies of ICICI Pru Elite Life Super Plan Analysis

4.)Funds of ICICI Pru Elite Life Super Plan Review

5.)ICICI Pru Elite Life Super Plan Review of Benefits

- i.)Death Benefits review

- ii.)Maturity Benefits review

6.)ICICI Pru Elite Life Super Plan: Review of Returns

7.)Review of Charges in ICICI Pru Elite Life Super Plan

- i)Premium Allocation Charge illustration

- ii.) Fund Management Charge

- iii.) Policy Administration Charge – Analysis

- iv.) Mortality Charges – Analysis

8.)Taxation of ICICI Pru Elite Life Super Plan Review

9.)Pros(advantages) of ICICI Pru Elite Life Super Plan

10.)Cons(disadvantages) of ICICI Pru Elite Life Super Plan

11.)ICICI Pru Elite Super Plan vs PPF: Review with Illustration

12.)ICICI Pru Elite Super Plan vs ELSS Mutual Fund: Review with Illustration

13.)Verdict on ICICI Pru Elite Super Plan: Good or Bad?

14.)How to surrender your ICICI Pru Elite Life Super Plan? An Analysis

15.)Conclusion

ICICI Pru Elite Life Super, being a ULIP, carries investment risks since it invests in the equity market.

It is often true that risk and return go hand in hand.

But can the ICICI Pru Elite Life Super plan deliver returns justifying the investment risks in it?

Should you invest in the ICICI Pru Elite Life Super plan for your financial goals?

In this ICICI Prudential Elite Life Super Plan review, we will analyze this ULIP in detail.

And we will have the answers to help you make the right choice. Let’s start with…

1.)5 Steps of ICICI Pru Elite Life Super Plan Working: Analysis

2.)Eligibility and Features of ICICI Pru Elite Life Super Plan: Analysis

ICICI Pru Elite Life Super plan offers flexibility with options in premium payment, policy term, and a wide range of eligibility ages.

The policy features are shown in the table below.

Other Features of ICICI Pru Elite Life Super Plan: Analysis

- It requires a minimum of ₹2 lakhs to invest in this ULIP.

- Tax benefit up to ₹1.5 lahks per annum, u/s 80C on premium paid by the policyholder.

- Accidental death rider option is available under this policy.

- The policyholder has the option to secure their family members’ future under “Marriage Woman’s Property Act (MWPA).

Read more about the policy features in: ICICI Pru Elite Life Super Plan Policy Brochure PDF.

3.)Portfolio Strategies of ICICI Pru Elite Life Super Plan: Review

There are 4 portfolio strategies in this policy to help policyholders plan their investments.

They are as follows,

i.) Target Asset Allocation Strategy: Analysis

It allows the investors to decide the asset allocation ratio based on their risk appetite. The funds will automatically rebalance every quarter to maintain the chosen asset allocation ratio.

ii.) Trigger Portfolio Strategy2: Analysis

In this strategy, the policyholder gets to take advantage of market volatility. And buy when the market is low and sell when the market is high.

iii.) Lifecycle-Based Portfolio Strategy 2: Analysis with illustration

Your financial needs and priorities are bound to change with age. There are some key features to this strategy.

a.) Age-Based Management: In this strategy, the investments will be distributed between 2 funds (Multi-Cap Growth Fund and Income Fund) based on your age. With the increasing age, the fund will be rebalanced as shown below.

b.) Quarterly Rebalancing: On the last day of each policy quarter, units are rebalanced between the funds to achieve the asset allocation as per the table above.

c.) Fund Safety: Over the last 10 quarters of the policy, the entire fund in the Multi-cap Growth Fund is systematically transferred to the Income Fund.

iv.) Fixed Portfolio Strategy: Analysis

The policyholder can choose to invest in any of the funds available under this policy.It gives you the liberty to choose any asset allocation actively by switching between the funds.

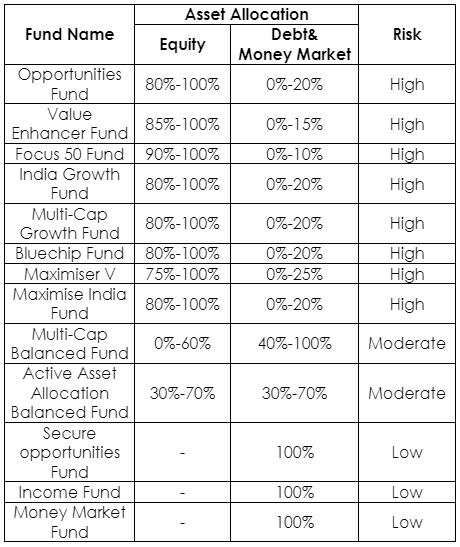

4.)Funds of ICICI Pru Elite Life Super Plan: Review

In addition to the range of options in the policy features, the ICICI Pru Elite Life Super Plan also offers a range of investment funds.

5.)Benefits Review of ICICI PRU Elite Life Super Plan:

Being an investment insurance plan, ICIC Pru Elite Life Super has two different benefit options.

It is either the nominee who will receive the death benefit on the policyholder’s death. Or the policyholder will receive the fund value on maturity.

i.)Death Benefit: Review

If the policyholder, unfortunately, dies while the policy is active, the nominee will receive the highest of,

- The Sum Assured

- Minimum Death Benefit (105% of total premium paid)

- The Fund value

The nominee will also receive the top-up sum assured (if any).

ii.)Maturity Benefit: Review

Once the policy matures, the policyholder will receive the fund value including top-up fund value(if any).

The policyholder can choose to receive this benefit as either a lump-sum payout or a structured payout with a settlement option.

With the settlement option facility, the policyholder can choose to get paid either monthly, quarterly, half-yearly, or yearly (through ECS) over 1 to 5 years, after maturity.

During this period, the policyholder also gets an option to withdraw the entire fund value. During this period, no loyalty additions or wealth boosters will be added under any circumstances.

Partial withdrawals and switches are also not allowed under this policy during the settlement period.

With that said, one question remains.

What kind of return can you expect from ICICI Pru Elite Life Super policy?

6.)ICICI Pru Elite Life Super Plan: Review of Returns

Since this is a complicated product, the returns you see is not what you get.

For example, if the fund of your choice is earning a return at, say, 10% CAGR, the return rate in the investor’s hands will always be less than that.

It is because of all the hidden charges levied in this policy.

Let’s calculate the actual returns an investor might get by investing in this policy with an example.

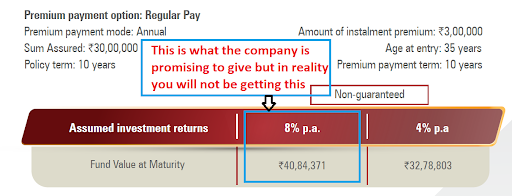

The official policy brochure suggests a long-term return at 8% CAGR. And based on that, an approximate maturity value is presented.

But let’s calculate the actual IRR ourselves to be sure.

Let’s take the ICICI Pru Elite Life Super policy with an annual premium of ₹3,00,000. And the policy term is 10 years.

For this policy, ICICI Pru suggests a fund value at maturity of ₹40,84,371. It is assuming the funds in this policy are giving an 8%CAGR.

However, the calculation of the actual return rate is shown in the table below.

|

|

|

At 4% p.a. |

At 8% p.a. |

||

|

Age |

Year |

Annualised premium / Maturity benefit |

Death benefit |

Annualised premium / Maturity benefit |

Death benefit |

|

30 |

1 |

-3,00,000 |

30,00,000 |

-3,00,000 |

30,00,000 |

|

31 |

2 |

-3,00,000 |

30,00,000 |

-3,00,000 |

30,00,000 |

|

32 |

3 |

-3,00,000 |

30,00,000 |

-3,00,000 |

30,00,000 |

|

33 |

4 |

-3,00,000 |

30,00,000 |

-3,00,000 |

30,00,000 |

|

34 |

5 |

-3,00,000 |

30,00,000 |

-3,00,000 |

30,00,000 |

|

35 |

6 |

-3,00,000 |

30,00,000 |

-3,00,000 |

30,00,000 |

|

36 |

7 |

-3,00,000 |

30,00,000 |

-3,00,000 |

30,00,000 |

|

37 |

8 |

-3,00,000 |

30,00,000 |

-3,00,000 |

30,00,000 |

|

38 |

9 |

-3,00,000 |

30,00,000 |

-3,00,000 |

30,00,000 |

|

39 |

10 |

-3,00,000 |

30,00,000 |

-3,00,000 |

30,00,000 |

|

40 |

|

32,78,803 |

|

40,84,371 |

|

|

|

|

|

|

|

|

|

|

IRR |

1.61% |

|

5.54% |

|

In the above illustration, the net return rate is calculated at 5.54%.

I think it is evident that the 8% CAGR by the fund is wildly misleading to the buyers of this policy.

Compare the 5.54% return to what is presented by ICICI Pru in the image below.

Occasionally the fund may earn more than 8%CAGR based on the market conditions. Even then, returns as low as this cannot even beat the inflation rate over the long term.

And considering the risk levels, and the illiquidity taken by the investor, it is not worthy investing in such products.

Another point of concern is that what you see is not what you get in the ICICI Pru Elite Life Super plan.

And as the fund earning rises, so does the charges, since they are fixed as a percentage of the premium and total fund value.

Here are the different charges under the ICICI Pru Elite Life Super.

7.)Review of Charges in ICICI PRU Elite Life Super Plan:

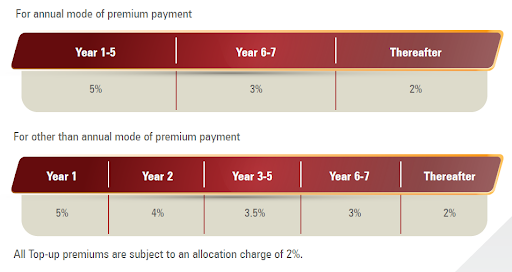

i.) Premium Allocation Charge illustration

It depends on 2 factors—Premium Payment Option and Premium Payment Mode.

Premium Allocation Charge is deducted before the allocation of fund units. Hence it takes a significant portion of your investment capital.

Based on the premium payment option, the charges are:

- Single Pay: 3% of the total premium.

- Limited and Regular Pay

ii.) Fund Management Charge

Fund Management Charge is levied as a percentage of the fund value, and deducted from the NAV (Net Asset Value) daily.

iii.) Policy Administration Charge – Analysis

It is levied every month by the cancelation of your fund units—regardless of the market conditions.

You should also remember that this charge will be taken throughout the policy term.

For single pay, the policy administration charge is ₹60 per month (₹720 p.a.) for the first 5 policy years.

For Limited and Regular pay, the charge is ₹350 per month (₹4200 p.a.) throughout the policy term.

iv.) Mortality Charges – Analysis

The mortality charge is levied to provide life cover to the policyholder.

ICICI Pru Elite Life Super plan does it by redeeming your fund units every month.

The risk charge is calculated based on the sum assured. And the risk charge will continue to increase per thousand rupees increase in the Sum Assured.

Indicative annual charges per thousand life cover for a healthy male and female life are as shown below:

| Age (Years) | Male (₹) | Female (₹) |

|---|---|---|

| 30 | 1.06 | 1.02 |

| 40 | 1.81 | 1.55 |

| 50 | 4.95 | 3.99 |

| 60 | 11.54 | 9.95 |

Interestingly enough, as per IRDA rules, your Sum Assured can never be lesser than 10x your annual premium.

Hence, there is a limit to how much you can reduce these hidden charges. And this number of hidden charges will continue to reduce your actual return rate from this policy.

8.)Taxation of ICICI Pru Elite Life Super Plan: Analysis

Insurance Policy Premiums up to ₹1.5 lakhs are exempt from taxation u/s 80C in a financial year.

Here, in the illustration, since the annual premium is ₹3 lakhs, the policyholder can claim tax benefit for only up to ₹1.5 lakhs per annum.

Also, ULIP policies usually claim the benefit of “tax-free” status on the returns.

However, The Finance Act 2021 changed it entirely.

The Finance Act 2021 ruled that ULIPs can claim tax exemption only if the annual premium is less than ₹2.5 Lakhs.

Anything more will be levied an LTCG tax of 12.5% on the gains from the ULIP investment.

Here, in the illustration above, the annual premium is ₹50000 over the limit. Hence, the gains are subject to LTCG tax treatment of @12.5%.

The policyholder will end up paying an LTCG tax of about ₹1.35 lahks on the ₹10.84 lakhs gains.

This would bring the total maturity value to just ₹39.48 Lakhs. It will further reduce the IRR from the ICICI Pru Elite Life Super Plan—lesser than 5.54%.

9.)Pros(advantages) of ICICI PRU Elite Super Plan:

a) Top Ups – Analysis

Above the base premium, a policyholder can invest an extra amount starting with a minimum of ₹2000. Each top-up premium paid will have a lock-in period of 5 years.

b) Loyalty Additions and Wealth Boosters: Analysis

The policyholder will be rewarded this benefit only if the premiums are paid on time and remain invested for a longer period.

c) Unlimited Free Switches: Analysis

The policyholder can switch units from one fund to another depending on their financial priorities if they choose a fixed portfolio strategy. There is no charge associated with this benefit, however, the minimum switch amount is ₹2000.

d) Partial Withdrawal Benefit: Analysis

Partial withdrawals are allowed only if the policy has completed 5 active years, provided the premiums are paid. And the total amount of the partial withdrawal cannot exceed 20% of the fund value in a policy year.

e) Increase or Decrease Sum Assured: Analysis

The policyholder has the option to increase or decrease their sum assured on a yearly basis. Under any circumstances, the increase and decrease in the sum assured will not change the annual premium.

f) Policy Revival: Analysis

Policyholders can revive their lapsed policy by paying the unpaid premiums. No interest or extra charge will be taken on payment of unpaid premiums.

10.)Cons(Disadvantages) of ICICI PRU Elite Super Plan:

- Under any circumstance, the policy will not guarantee returns.

- The fund management charge, policy administration charge, and switching charge may be increased to a maximum of ₹500 per month.

- The past performance of the funds is not an indicator of its future performance.

11.)ICICI PRU Elite Life Super Plan vs PPF: Review with Illustration

Let us now look at a table that shows the features comparison between ULIP and PPF.

You should notice that while the Elite Life Super Plan offers a life cover, PPF is an investment-only product.

Hence, for life cover, you can choose to buy a term insurance policy for an even higher Sum Assured for a far lesser premium amount.

And for investments, let us see what the PPF has in store for an investor.

We shall consider investing the limit of ₹1.5 lakhs per annum until maturity.

The interest rate in PPF for Q1 2025-26 is 7.1% p.a.

Even though PPF has a lock-in period of 15 years, let’s see the assured earnings at the end of the 15th year in PPF. See the compounding table below.

You can see that by the end of the 15th year, even after investing ₹7.5 lakhs lesser than in the ICICI Pru Elite Life Super plan, you will have an assured return of ₹40.7 lakhs.

Even though the investor cannot invest more than ₹1.5 lakhs per annum in PPF, it should not be a serious concern.

It is because—PPF or ULIP—section 80C allows only ₹1.5 lakhs tax-exemption. And the return from the PPF is tax-free, with returns assured by the Govt. of India.

Also, you have the room to explore better investment opportunities to invest the excess ₹7.5 lakhs.

Taxation of PPF Returns: Analysis

Under section 80C, investments up to ₹1.5 lakhs are tax-exempt for that financial year. But 80C does not apply when you redeem that investment.

For example, ELSS MF has the 80C benefit when you invest, but returns/redemptions are taxable @ 10% on LTCG on specified conditions.

But PPF has an EEE status (exempt from investment, Exempt from interest earned, exempt from returns/redemption). So not even ₹1 goes as tax when investing in PPF; it is the EEE tax status.

Pros(advantages) of Investing in PPF:

- PPF returns beat inflation in the long term, even if by a little margin.

- The returns are assured.

- The returns are entirely tax-exempt.

PPF + a Term Insurance policy is a far better option for a conservative investor.

But if you are someone with good risk tolerance. Or someone looking for capital growth in addition to the stability offered by the PPF investment, you may consider investing in Equity Mutual Funds.

Here’s a comparison.

12.)ICICI Pru Elite Super Plan vs ELSS Mutual Fund: Review with Illustration

Below is a table of features comparison between ICICI Pru Elite Super Plan and ELSS Mutual Fund.

Now let us calculate the likely return from an ELSS Mutual Fund.

The investment is ₹3 Lac annually for 10 years—as it was with the ICICI Pru Elite Life Super plan example above.

We assume a very conservative 12% CAGR for the ELSS mutual fund—though equity funds deliver better returns. And the investment risk is the same as ICICI Pru Elite Super Plan since both are market-linked investments.

Here is the returns illustration from ELSS Mutual Fund.

|

|

|

Term insurance + ELSS |

|

|

Age |

Year |

Term Insurance premium + ELSS |

Death benefit |

|

30 |

1 |

-3,00,000 |

30,00,000 |

|

31 |

2 |

-3,00,000 |

30,00,000 |

|

32 |

3 |

-3,00,000 |

30,00,000 |

|

33 |

4 |

-3,00,000 |

30,00,000 |

|

34 |

5 |

-3,00,000 |

30,00,000 |

|

35 |

6 |

-3,00,000 |

30,00,000 |

|

36 |

7 |

-3,00,000 |

30,00,000 |

|

37 |

8 |

-3,00,000 |

30,00,000 |

|

38 |

9 |

-3,00,000 |

30,00,000 |

|

39 |

10 |

-3,00,000 |

30,00,000 |

|

40 |

|

55,49,953 |

|

|

|

|

|

|

|

|

IRR |

10.94% |

|

The maturity amounts the policyholder will receive by investing in ELSS is calculated to be almost ₹59 Lakhs (Pre-tax amount).

ELSS Mutual Fund return is approximately ₹18.1 lakhs more than the ICICI Pru Elite Life Super Plan.

However, I must agree that despite the ₹1.5lakh exemption u/s 80C, the return from the ELSS Mutual Fund is not entirely tax-free.

So can the LTCG tax make a difference in the ELSS Mutual Fund Returns?

Post-Tax Return from ELSS Mutual Fund: Analysis with Illustration

|

ELSS Tax Calculation |

|

|

Maturity value after 10 years |

58,96,375 |

|

Purchase price |

30,00,000 |

|

Long-Term Capital Gains |

28,96,375 |

|

Exemption limit |

1,25,000 |

|

Taxable LTCG |

27,71,375 |

|

Tax paid on LTCG |

3,46,422 |

|

Maturity value after tax |

55,49,953 |

The post-tax return is calculated at ₹55.49 lakhs from the ELSS Mutual Fund.

It is clear that even after a 12.5% LTCG Tax, the ELSS return is still ₹14.65 lakhs more than the ICICI Pru Elite Life Super plan.

The ICICI Pru Elite Life Super Pan and the ELSS Mutual Fund have the same risk and very similar tax implications. But even an average-performing ELSS fund offers better post-tax returns than the ULIP.

The Systematic Advantage of ELSS Funds: Analysis

Moreover, once you invest in a ULIP, you are locked there for at least 5 years. On the other hand, even though ELSS funds have a 3-year lock-in period, it does not mandate you to keep investing.

If you sense something is wrong with the fund, you can immediately move to a better-performing fund. You can continue investing there and redeem your money from the lagging fund once the lock-in period is over.

This sort of liberty in the hands of ELSS investors compels the fund managers to perform consistently. It is another advantage of ELSS Funds over any ULIP policy.

Pros(advantages) of Investing in ELSS Mutual Fund:

- Consistent better returns than ULIPs

- Same risk level as ULIPs

- Similar tax implications

- Better post-tax returns than ULIPs

- Better liquidity than ULIPs

- More transparent portfolio

- No hidden charges

- Control over your investment choice

ELSS + a term insurance policy is a far better investment + insurance option than the ICICI Pru Elite Life Super Plan.

ICICI Pru Elite Super Plan vs ICICI Pru Guaranteed Income For Tomorrow

‘Guaranteed Income For Tomorrow’ is a non-linked, participating life insurance plan whereas ‘Elite Super Plan’ is a unit-linked insurance plan.

ICICI Pru Guaranteed Income For Tomorrow Review [2023]: Worth Buying Or Not?

ICICI Pru Guaranteed Income For Tomorrow Review: Worth Buying Or Not?/ Youtube Review /

13.)Verdict on ICICI Pru Elite Super Plan: Good or Bad?

Do Not Invest in ICICI Pru Elite Life Super Plan.

PPF is a better investment option for those investors with lower risk tolerance. When capital safety takes precedence, PPF should be your first choice in the long term.

Meanwhile, investors with risk tolerance can prefer ELSS Mutual Fund over any ULIP policy. It is the better choice when capital growth with some consistency takes precedence.

Moreover, ICICI Pru Elite Super plan demands long-term commitment and risk. The fund manager is not at all compelled to deliver his best when the investments are locked in for the long term.

Check out your alternate options before buying the ICICI Pru Elite Life Super Plan. It will help you make an informed decision.

But if you have already bought the policy, you still have a way out. Probably even make up for the lost time in the below-par product by investing in the alternatives.

14.)How to surrender your ICICI Pru Elite Life Super? An Analysis

You can surrender your ICICI Pru Elite Life Super policy only after the lock-in period of 5 years.

During the Free-look Period: Analysis

You can surrender your ICICI Pru Elite Life Super Plan during the free-look period.

It is 15 days (30 if bought online) from the date of commencement for the policyholder to review the policy terms. If you change your mind during this period, you can immediately surrender your policy. And the company will refund your premium amount minus any incurred charges.

After the Free-look period: Analysis

- Surrendering during the 5 Years Lock-in Period:

Surrendering your ICICI Pru Elite Life Super Plan will only make it a paid-up policy.

On submitting the surrender request during the lock-in period, your funds are moved to the Discontinued Policy Fund. That is after the deduction of discontinuance charges.

You will receive your fund value after the completion of the Lock-in period

- Surrendering after the 5 Years Lock-in Period – Analysis

You can surrender your Elite Life Super Plan any time after the lock-in period.

The policyholder will get fund value including top-up fund value (if any).

To surrender the policy, follow the step below:

Submit a surrender request with the surrender form at the nearest ICICI Pru Branch, along with the following documents.

- Original policy documents

- Canceled cheque with the policyholder’s name on it

- In case the canceled cheque does not have your name and account number printed on it, the passbook copy/bank statement with the name and the account number is required

- ID proof (PAN Card, Aadhaar Card, Passport, Driving License, Voters ID)

- Policy surrender or cancellation form

- Latest contact details

15.)Conclusion:

I hope this ICICI Pru Elite Life Super plan review has thrown enough light on areas that mislead investors.

Like many policies in the bazaar it is overly charged. Even for a ULIP: and does not serve the investors but those that sell them.

That is why insurance agents will try to push you this plan, for their agent commission!

Hence, do your due research. Analyse the product; write down the numbers. And never mix life insurance with investments.

Keep them separate, and you will have a far better chance of achieving your financial goals faster. And keep your life secured sufficiently.

If you have any comments or questions, write them in the comment box below.

Or are you interested in creating a Comprehensive Financial Plan for your financial goals?

Are you someone who is searching for financial planning solutions on social media platforms like Facebook, Twitter, Quora etc?

A professional financial planner can lead you through a comprehensive financial plan.

Skip the queue by registering for your 30 Minute FREE Financial Plan Consultation. Click the ‘‘BOOK YOUR SLOT NOW!’’ button below.

Leave a Reply