ICICI Pru’s Guaranteed Income For Tomorrow (GIFT) is a non-linked, participating life insurance plan.

It aims to help you achieve your life goals with its policy coverage and guaranteed benefits.

Keep reading this article as I delve deeper into if this life Insurance plan is worth buying or not.

Will this plan be a GIFT or a forfeit for your future?

Reading the official brochure of ICICI Pru’s Guaranteed Income For Tomorrow (GIFT) will give you an idea about the plan. But, only a comprehensive review by weighing its pros and cons can make you decide whether this plan is good or bad for your future!

We have opened the wrap of this ‘GIFT’ plan to see what’s inside!

But before starting the analysis of ICIC’S (GIFT) plan, let’s start with going over the policyonce.

TABLE OF CONTENTS:

1.) ICICI Pru Guaranteed Income For Tomorrow: Policy Features and Eligibility

2.) Other features of ICICI Pru Guaranteed Income For Tomorrow (GIFT)

3.) ICICI Pru Guaranteed Income For Tomorrow (GIFT): Review of Benefits

- ICICI Pru Guaranteed Income For Tomorrow Review of Death Benefits

- ICICI Pru Guaranteed Income For Tomorrow Review of Maturity Benefits

- ICICI Pru Guaranteed Income For Tomorrow Review of Survival Benefits

4.) ICICI Pru Guaranteed Income For Tomorrow: Review of IRR

5.) ICICI Pru Guaranteed Income For Tomorrow Plan: Good or Bad?

6.) ICICI Pru Guaranteed Income For Tomorrow Plan: Pros

7.) ICICI Pru Guaranteed Income For Tomorrow Plan: Cons

8.) Is there any better alternative to ICICI Pru Guaranteed Income For Tomorrow plan?

- Comparison of ICICI Pru Guaranteed Income For Tomorrow against Term Insurance + PPF

- Comparison of ICICI Pru Guaranteed Income For Tomorrow against Equity Mutual Fund

- ICICI Pru Guaranteed Income for Tomorrow vs ICICI Pru Guaranteed Income for Tomorrow ( Long Term)

- ICICI Pru Guaranteed Income for Tomorrow vs ICICI Pru Guaranteed Pension Plan Flexi

9.)ICICI Pru Guaranteed Income for Tomorrow vs Other Investments – Comparison Review

10.) Final Results from our research review on ICICI Pru Guaranteed Income for Tomorrow

11.) How to Surrender/cancel your ICICI Pru Guaranteed Income For Tomorrow

12.) ICICI Pru Guaranteed Income For Tomorrow: Final thoughts about the review

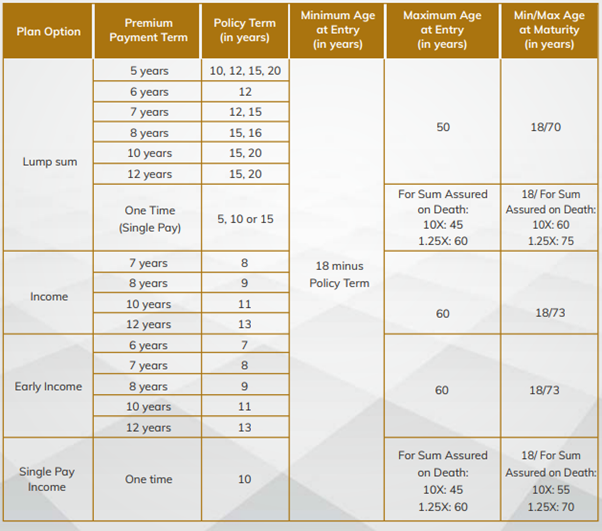

ICICI Pru Guaranteed Income For Tomorrow ( GIFT): Policy Features and Eligibility:

ICICI Pru Guaranteed Income For Tomorrow Insurance plan is a savings and protection-oriented plan.

It offers regular income and provides financial security to your family in your absence.

It is a traditional Life insurance policy that provides both the options of receiving your guaranteed income in the form of a lump sum or as regular income.

ICICI Pru Guaranteed Income For Tomorrow (GIFT) offers four options to receive the guaranteed income which are mentioned below:

- Early Income option.

- Income option.

- Lumpsum option

- One-time payment option.

The policy term and your premium paying term (PPT) differ from option to option along with the maximum eligibility age to avail of the maturity benefits in this life insurance plan.

So, let’s take a look at how this Plan works along with its payment options:

Download the ICICI Pru Guaranteed Income For Tomorrow brochure (pdf) to get more information.

Other features of ICICI Pru Guaranteed Income For Tomorrow (GIFT):

- It allows the option of taking a loan against policy to help you in case offinancial emergencies that we don’t calculate or predict

- It provides you with the option to choose a lump sum or regular income to receive the death and maturity benefits.

Now, let us go over the policy benefits to get clarity on the advantages it poses.

ICICI Pru Guaranteed Income For Tomorrow (GIFT): Review of Benefits

ICICI Pru Guaranteed Income For Tomorrow Review of Death Benefits:

If the person whose life is covered by the ICICI Pru Guaranteed Income For Tomorrow (GIFT) unfortunately passes away during the term of the policy, the insurance cover amount will be paid out as a lump sum to the person specified as the nominee in the policy.

This applies to all the payment options available in this Insurance policy.

But in both the Income option and Early Income option, there is another choice which the claimant of the policy can avail:

In case of the death of the policyholder during the Income Period, the nominee will continue to receive the income. The nominee also has the option to receive the future income as a lump sum, which shall be the present value of the future income discounted at a rate.

You can find out how exactly the death benefits would be distributed for each payment option below:

Lumpsum option:

For single pay, Life Insurance Benefit is the highest of:

- Sum Assured on Death

- 105% of Total Premiums Paid up to the date of death

- Sum Assured on Maturity X Death Benefit factor for Lump sum plan, where, Sum Assured on Death is 10 X Single Premium or 1.25 X Single Premium as chosen by you.

For other than single pay, Life Insurance Benefit is the highest of:

- Sum Assured on Death

- 105% of Total Premiums Paid up to the date of death

- Sum Assured on Maturity X Death Benefit factor for Lump sum plan, where,Sum Assured on Death is 10 X Annualised Premium

Income option:

Life Insurance Benefit is the highest of:

- Sum Assured on Death

- 105% of Total Premiums Paid up to the date of death

- Annual Guaranteed Income X Death Benefit factor for Income Plan, where, Sum Assured on Death is 10 X Annualised Premium.

Early Income:

Life Insurance Benefit is the highest of:

- Sum Assured on Death

- 105% of Total Premiums Paid up to the date of death

- Sum Assured on Maturity × Death Benefit factor for Lump Sum Plan, where the Sum Assured on Death is either 10 × Single Premium or 1.25 × Single Premium, as chosen by you.

Single pay income:

Life Insurance Benefit is:

-

-

- Sum Assured on Death or

- Surrender value

- Where, Sum Assured on Death is 10 X Single Premium

or

- 1.25 X Single Premium as chosen by you

-

ICICI Pru Guaranteed Income For Tomorrow (GIFT) Review of Maturity Benefits:

Let’s assume Akash, a 35-year-old male is paying ₹ 1,00,000 annual premiums in ICICI Pru Guaranteed Income For Tomorrow. He wants to create an alternate source of income as he is planning to retire early.

Now, let us go over each option to see how Akash paying the same premium would receive his maturity benefits but in different options and policy years.

Lumpsum option:

|

He pays a premium for |

He will receive a lump sum at the end of |

He will receive a guaranteed lump sum of |

|

5 years |

10 years |

₹ 6,91,788 |

|

7 years |

15 years |

₹ 12,57,177 |

|

8 years |

15 years |

₹ 14,23,372 |

|

10 years |

20 years |

₹ 22,28,260 |

|

12 years |

20 years |

₹ 25,71,345 |

Income option:

|

Pay for |

Income Period |

||

|

5 years |

7 years |

10 years |

|

|

7 years |

₹ 1,81,136 |

₹ 1,40,247 |

₹ 1,09,601 |

|

8 years |

₹ 2,11,575 |

₹ 1,65,169 |

₹ 1,29,400 |

|

10 years |

₹ 2,83,878 |

₹ 2,25,828 |

₹ 1,79,070 |

|

12 years |

₹ 3,57,716 |

₹ 2,88,074 |

₹ 2,31,608 |

Early Income Option:

|

Pay for |

Income from 2nd year till 7th year |

Income from 7th year till 12th year |

|

6 years |

₹ 15,000 |

₹ 1,02,176 |

|

Pay for |

Income from 2nd year till 8h year |

Income from 8th year till 14th year |

|

7 years |

₹ 20,000 |

₹ 1,03,200 |

|

Pay for |

Income from 2nd year till 9th year |

Income from 9th year till 16th year |

|

8 years |

₹ 20,000 |

₹ 1,07,751 |

|

Pay for |

Income from 2nd year till 11t year |

Income from 11t year till 20th year |

|

10 years |

₹ 25,000 |

₹ 1,13,871 |

|

Pay for |

Income from 27d year till 13h year |

Income from 13″ year till 24th year |

|

12 years |

₹ 25,000 |

₹ 1,25,225 |

ICICI Pru Guaranteed Income For Tomorrow (GIFT) Review of Survival Benefits:

ICICI Pru Guaranteed Income For Tomorrow (GIFT) plan also offers survival benefits for two of its payment options as part of its Life Insurance Policy. Keep reading to see for yourself how both the option’s survival benefits differ from each other.

1.) Early Income option:

This option offers Guaranteed Early Income which is a fixed percentage of the premium Akash pays in a year and is based on the number of years for which he chooses to pay the premiums as given in the table below:

2.) Single pay Income option:

This option only offers survival benefits instead of maturity benefits.

In that case, Akash needs to pay the premium of ₹ 1,00,000 only once and he can start receiving the guaranteed early income of ₹ 12,585 starting from the 2nd year onwards till the end of the 10th year of the policy term.

ICICI Pru Guaranteed Income For Tomorrow (GIFT): Review of IRR ( Interest Rate):

Now after reading through all the benefits this policy offers, to completely start reviewing how much exactly this policy is worth to invest your money, you need to be aware of its Internal Rate of Return (IRR)

Let’s go over the Internal Rate of Return of each payment option of ICICI Pru Guaranteed Income For Tomorrow policy offers:

Lumpsum option:

|

|

|

Lump Sum Option |

|

Age |

Year |

Annualised premium / Maturity benefit |

|

35 |

1 |

-1,00,000 |

|

36 |

2 |

-1,00,000 |

|

37 |

3 |

-1,00,000 |

|

38 |

4 |

-1,00,000 |

|

39 |

5 |

-1,00,000 |

|

40 |

6 |

-1,00,000 |

|

41 |

7 |

-1,00,000 |

|

42 |

8 |

-1,00,000 |

|

43 |

9 |

-1,00,000 |

|

44 |

10 |

-1,00,000 |

|

45 |

11 |

0 |

|

46 |

12 |

0 |

|

47 |

13 |

0 |

|

48 |

14 |

0 |

|

49 |

15 |

0 |

|

50 |

16 |

0 |

|

51 |

17 |

0 |

|

52 |

18 |

0 |

|

53 |

19 |

0 |

|

54 |

20 |

0 |

|

55 |

|

22,28,260 |

|

56 |

|

|

|

|

IRR |

5.23% |

Income option:

|

Income Option |

||

|

Age |

Year |

Annualised premium / Maturity benefit |

|

35 |

1 |

-1,00,000 |

|

36 |

2 |

-1,00,000 |

|

37 |

3 |

-1,00,000 |

|

38 |

4 |

-1,00,000 |

|

39 |

5 |

-1,00,000 |

|

40 |

6 |

-1,00,000 |

|

41 |

7 |

-1,00,000 |

|

42 |

8 |

-1,00,000 |

|

43 |

9 |

-1,00,000 |

|

44 |

10 |

-1,00,000 |

|

45 |

11 |

0 |

|

46 |

12 |

0 |

|

47 |

13 |

1,79,070 |

|

48 |

14 |

1,79,070 |

|

49 |

15 |

1,79,070 |

|

50 |

16 |

1,79,070 |

|

51 |

17 |

1,79,070 |

|

52 |

18 |

1,79,070 |

|

53 |

19 |

1,79,070 |

|

54 |

20 |

1,79,070 |

|

55 |

21 |

1,79,070 |

|

56 |

22 |

1,79,070 |

|

IRR |

4.97% |

Early Income option:

|

Early Income Option |

||

|

Age |

Year |

Annualised premium / Maturity benefit |

|

35 |

1 |

-1,00,000 |

|

36 |

2 |

-75,000 |

|

37 |

3 |

-75,000 |

|

38 |

4 |

-75,000 |

|

39 |

5 |

-75,000 |

|

40 |

6 |

-75,000 |

|

41 |

7 |

-75,000 |

|

42 |

8 |

-75,000 |

|

43 |

9 |

-75,000 |

|

44 |

10 |

-75,000 |

|

45 |

11 |

25,000 |

|

46 |

12 |

1,13,871 |

|

47 |

13 |

1,13,871 |

|

48 |

14 |

1,13,871 |

|

49 |

15 |

1,13,871 |

|

50 |

16 |

1,13,871 |

|

51 |

17 |

1,13,871 |

|

52 |

18 |

1,13,871 |

|

53 |

19 |

1,13,871 |

|

54 |

20 |

1,13,871 |

|

55 |

21 |

1,13,871 |

|

56 |

22 |

1,13,871 |

|

IRR |

4.4% |

Single Pay Option:

|

Single pay Income Option |

||

|

Age |

Year |

Annualised premium / Maturity benefit |

|

35 |

1 |

-1,00,000 |

|

36 |

2 |

0 |

|

37 |

3 |

12,585 |

|

38 |

4 |

12,585 |

|

39 |

5 |

12,585 |

|

40 |

6 |

12,585 |

|

41 |

7 |

12,585 |

|

42 |

8 |

12,585 |

|

43 |

9 |

12,585 |

|

44 |

10 |

12,585 |

|

45 |

11 |

12,585 |

|

IRR |

2.12% |

We have calculated the early income option and single payment option in the above tables.

As we have seen above, the IRR fluctuates somewhere between 3% to 5% as in most money-back Insurance policies.

It does seem like a better amount of IRR for the money you have invested.

But while looking through the long-term perspective, two question arises;

Will this be enough to beat inflation in the long run? And are the benefits offered in this policy sufficient?

These questions make you wonder if there are any other better choices that you can make instead of investing in the ICICI Pru Guaranteed Income For Tomorrow (GIFT) Life Insurance Policy.

So, let’s review and find if there are other better alternatives.

ICICI Pru Guaranteed Income For Tomorrow Plan (GIFT): Good or Bad?

To determine if this is a good investment or not?

We can perform our evaluation through a two-stage analysis.

In the first stage, let’s go over the pros and cons of this policy to understand if the pros outweigh the cons to get clarity in determining whether this is a good or bad plan.

In the second stage, we will compare this policy with two other Investment options. The second stage will truly be able to help us get to the heart of this analysis by analyzing if there are better options that will prove whether this plan is good or bad.

Do you prefer watching this review as a Youtube video?

ICICI Pru Guaranteed Income For Tomorrow Plan (GIFT) Plan Youtube review with an expert view on IRR(Interest Rate) analysis, calculated returns, and pros and cons with illustrations. Check out our video review below.

ICICI Pru Guaranteed Income For Tomorrow Plan (GIFT): Pros

-

- There are various payment options available to choose from. Depending on the individual’s comfort regarding the premium paying term & guaranteed income period, it can be chosen.

- Any time during the Income Period, you shall have the option to receive the Future Guaranteed Income as a lump sum, which shall be the present value of the future income discounted at a rate.

- You also have the option to customize the date you receive your Guaranteed Income for special occasions like your birthday or your wedding anniversary.

- In case of death of the Life Assured during the Income Period, the Claimant (nominee) will continue to receive the income. The Claimant shall have the option to receive the future income as a lump sum, which shall be the present value of the future income discounted at a rate.

- You also get the option to choose if you want to receive the Guaranteed income on a yearly or monthly basis.

- If you are not able to continue the policy after having completely paid premiums for 2 years, you have the option to surrender the policy.

- You can take a policy loan after your policy acquires a surrender value. 80% of the surrender value can be availed as the loan amount.

- Tax benefits may be applicable on premiums paid and benefits received as per the prevailing tax laws.

Icici Prudential – Apply and pay your premium online in 2024

-

ICICI Pru Guaranteed Income For Tomorrow Plan (GIFT): Cons

- You can’t avail yourself of any of the policy benefits if you stopped paying the premiums in the first two years.

- Your Premium, premium payment term and policy term was chosen at the inception of the policy and cannot be changed.

- The guaranteed income will not be sufficient to meet any expenses or financial goals you may have as prices are increasing due to inflation.

- Neither does it seems like an adequate insurance life cover nor does it offer inflation-beating returns in the long run.

The pros and cons offer only one perspective of seeing through this policy.

Do you know what would be a better way to calculate if this policy is good or bad?

It is through comparing other investment options, we can finally conclude whether this plan is as good as it sounds or as bad as we didn’t anticipate.

Let us move on to the second stage of our comparative analysis.

Is there any better alternative to ICICI Pru Guaranteed Income For Tomorrow (GIFT) plan?

Indeed, there are better alternatives to choose from.

For example, a term life insurance policy can provide you with this same or even greater risk of life coverage for lesser charges.

From a realistic perspective, term insurance should be considered a suitable life insurance coverage.

Let me explain why!

You can avail yourself of a huge value life cover than the one currently reviewed in this article for a much lower premium.

You can invest in other options like PPF with this same amount and still be able to afford the premiums of a high-value life cover with term insurance.

Keeping your investments and insurance separate will be more beneficial in your investment journey.

Let us compare ICICI Pru Guaranteed Income For Tomorrow against PPF to see if it is a better alternative.

Comparison of ICICI Pru Guaranteed Income For Tomorrow (GIFT) against Term Insurance + PPF:

Public Provident Fund (PPF) scheme is a long-term investment option provided by the Govt. of India.

As ICICI Pru Guaranteed Income For Tomorrow assures guaranteed returns, it would be best to compare it against PPF which also offers Guaranteed returns.

Let’s calculate the returns from Term insurance + PPF by investing the same amount for the same period as we did in ICICI’s GIFT illustration above.

Term Insurance + PPF

Age

Year

Term Insurance premium + PPF

Death benefit

35

1

-1,00,000

50,00,000

36

2

-1,00,000

50,00,000

37

3

-1,00,000

50,00,000

38

4

-1,00,000

50,00,000

39

5

-1,00,000

50,00,000

40

6

-1,00,000

50,00,000

41

7

-1,00,000

50,00,000

42

8

-1,00,000

50,00,000

43

9

-1,00,000

50,00,000

44

10

-97,500

50,00,000

45

11

-500

50,00,000

46

12

-500

50,00,000

47

13

-500

50,00,000

48

14

-500

50,00,000

49

15

-500

50,00,000

50

16

0

50,00,000

51

17

0

50,00,000

52

18

0

50,00,000

53

19

0

50,00,000

54

20

0

50,00,000

55

21

25,76,223

56

22

6.20%

IRR

We have calculated the IRR of Term Insurance + PPF in the above table.

Let us dig deep into evaluating how you can retain a better long-term investment through the combination of Term Insurance + PPF

Let’s just say that Akash invests the ₹ 1,00,000 corpus he’s planning to invest in ICICI Pru Guaranteed Income For Tomorrow in Term Insurance and PPF divided accordingly.

For example, let’s assume he takes up term insurance which provides a high-value life cover of ₹ 50,00,000 with an affordable premium of ₹ 12,700 annually for the next 10 years.

Now, he invests the balance amount of ₹ 87,300 in a PPF for the same next 10 years.

If he, unfortunately, passes away, his family will have the financial security of ₹ 50,00,000 to sustain themselves while ICICI’s Pru Guaranteed Income For Tomorrow life cover will only provide ₹ 10,00,000 to his family compared to the high-value cover of term insurance.

Now analyzing the guaranteed income benefits compared to his PPF investments, it’s clear that PPF will yield a higher IRR considering it gives out a return of 6.20% while ICICI’S Pru Guaranteed Income For Tomorrow only offers an average of 3% to 5% returns as you can reference this information in the above table.

Utilizing this method, it’s clear how ICICI’s Pru Guaranteed Income For Tomorrow only provides a maturity amount of ₹ 22.28 Lakhs after 20 years while this combination of Term Insurance + PPF provides a final maturity value that’s worth a corpus of ₹ 25.76 at the end of the same 20 years.

Also, it should be mentioned that PPF investments, Interest earned, and maturity amounts are all tax-free.

If you are a conservative investor who’s looking for guaranteed returns, this type of combination investment would be a good option for you. But if you are looking for a long-term investment where you are willing to take some investment risks, there is an even better alternative you can take upon.

Comparison of ICICI Pru Guaranteed Income For Tomorrow (GIFT) against Equity Mutual Fund:

Equity mutual funds are equity-linked mutual funds that predominantly invest in stocks.

Since this is a stock market-related investment, it comes with its own set of risks.

But as both the return and investment are linked, Equity mutual funds provide a higher rate of return on your investments.

If the investor’s risk tolerance is high, he can attempt investing in Equity mutual funds keeping in mind his long-term financial goals rather than the ICICI Pru Guaranteed Income For Tomorrow.

Let us just assume that Akash invests the same amount as seen in the ICICI Pru Guaranteed Income For Tomorrow plan illustration in an Equity Mutual Fund. A part of the investment capital—₹12,700—is deducted to provide the life cover with a term life insurance plan.

Let us assume a conservative 12% CAGR and calculate the returns from the Equity mutual fund scheme which are shown in the table below.

Term insurance + Equity Mutual Fund

Age

Year

Term Insurance premium + Equity Mutual Fund

Death benefit

35

1

-1,00,000

50,00,000

36

2

-1,00,000

50,00,000

37

3

-1,00,000

50,00,000

38

4

-1,00,000

50,00,000

39

5

-1,00,000

50,00,000

40

6

-1,00,000

50,00,000

41

7

-1,00,000

50,00,000

42

8

-1,00,000

50,00,000

43

9

-1,00,000

50,00,000

44

10

-1,00,000

50,00,000

45

11

0

50,00,000

46

12

0

50,00,000

47

13

0

50,00,000

48

14

0

50,00,000

49

15

0

50,00,000

50

16

0

50,00,000

51

17

0

50,00,000

52

18

0

50,00,000

53

19

0

50,00,000

54

20

0

50,00,000

55

21

47,87,760

56

22

10.35%

IRR

We have calculated the IRR of Term Insurance + Equity Mutual Fund in the above table.

Even after assuming a conservative return rate, the Equity Mutual Fund mutual fund has yielded far higher returns, despite the sizable investment risks involved.

From the above table, we can see that ICICI Pru Guaranteed Income For Tomorrow’s final maturity value is ₹ 22.28 Lakhs, while the Equity mutual fund’s final maturity value stands at ₹ 47.87 Lakhs

In comparison with the Equity mutual fund, there is a huge difference in the final maturity value. The approximate difference in value is ₹ 25.59 Lakhs

It is almost two times higher than the ICICI Pru Guaranteed Income For Tomorrow life insurance plan’s returns. Do you really want this ‘GIFT’ plan?

So, this combination of term insurance + Equity Mutual Fund mutual fund would be a good choice for a risk-tolerant investor.

( Interesting Fact: the minimum amount to invest in Mutual Fund SIP is ₹100 )

But as Equity mutual funds returns are not tax-free compared to ICICI Pru Guaranteed Income For Tomorrow, let us analyze the post-tax return rate of Equity mutual funds.

The Equity Mutual Fund scheme’s post-tax return rate is shown in the table below.

Equity Mutual Fund Tax Calculation

Maturity value after 20 years

53,29,154

Purchase price

8,73,000

Long-Term Capital Gains

44,56,154

Exemption limit

1,25,000

Taxable LTCG

43,31,154

Tax paid on LTCG

5,41,394

Maturity value after tax

47,87,760

We have calculated the post-tax maturity value in the above illustration

The post-tax returns are still higher than the returns offered in the ICICI Pru Guaranteed Income For Tomorrow Life Insurance plan despite the 12.5% LTCG tax.

ICICI Pru Guaranteed Income for Tomorrow vs ICICI Pru Guaranteed Income for Tomorrow ( Long Term)

(Long Term) Plan option. you can choose to pay premiums for 7 or 10 years (PPT) and also can receive Guaranteed Income for 15, 20, 25, or 30 years and the policy term is PPT+1+Income Period with the life cover for the entire policy term.What is the Assured Income with 110% ROP (Return of Premium) plan option?The advantage here is that you can choose to pay premiums for 7, 10, or 12 years (PPT).You can choose to receive Guaranteed Income for 15, 20, 25 or 30 years.And also, you will get 110% of the Total Premiums paid (Terminal Benefit). This will be given at the end of the policy term along with the last income installment.

Read the official ICICI Pru Guaranteed Income for Tomorrow ( Long Term) Brochure (pdf)

ICICI Pru Guaranteed Income for Tomorrow vs ICICI Pru Guaranteed Pension Plan Flexi

The ICICI Pru Guaranteed Pension Plan Flexi is designed to create lifelong income after your retirement without any worries.

ICICI Pru Guaranteed Pension Plan Flexi gives you the flexibility to choose your premium payment term, deferment period, and frequency of annuity.

This ICICI Pru Guaranteed Pension Plan Flexi gives you 9 different Annuity options to choose from.

To know everything about this plan please read the official

ICICI Pru Guaranteed Pension Plan Flexi Brochure (pdf)

To read the complete policy review with IRR analysis and precise calculation of returns with illustration click below.

ICICI Pru Guaranteed Pension Plan Flexi-Review (2024): Should you buy this plan or not?

ICICI Pru Guaranteed Income for Tomorrow vs Other Investments – Comparison Review

After a thorough and detailed analysis of other investment options.

ICICI Pru Guaranteed Income for Tomorrow (GIFT) seems to perform poor when compared to ELSS and PPF.

This is marketed as a money-back plan to avoid taxes.

ELSS and PPF are far better options and the calculated returns are higher combined with good fund performance.

Don’t get carried away by new plans in the market. Always compare and review it with other investment options.

Most of the time, after a comprehensive review, Term Insurance + PPF or ELSS seem to be better options.

Final Results from our research review on ICICI Pru Guaranteed Income for Tomorrow:

ICICI Pru Guaranteed Income For Tomorrow may seem appealing to many investors because of its guaranteed returns,

But after analyzing this policy with other better alternatives for both conservative and risk-tolerant investors, it’s evident we needn’t invest in this plan.

But, why are they still trying to sell this ‘GIFT’ plan to you? Because of the ‘GIFT’ the agents get. Yes! The agent commission is so high in this policy.

Please be careful of anyone who vehemently sells this to you.

The other alternatives offer you both an insurance and an investment option which keeps your insurance and investment separate making it a better choice.

By choosing this plan and combining your investment and insurance in one policy, you are at the risk of loss with inadequate life coverage and returns that will not even beat inflation in the long run.

If you feel the returns from ICICI Pru Guaranteed Income For Tomorrow which ranges from 3% to 5% according to its payment options are sufficient for you, then you can still opt for this plan after careful thought given over the discussed points.

If you have purchased this policy and thinking about course-correcting your investments,

Then your way out would be to start by surrendering your ICICI Pru Guaranteed Income For Tomorrow plan.

How to Surrender/cancel your ICICI Pru Guaranteed Income For Tomorrow:

If the policyholder is not satisfied with the policy, they have the option to surrender their policy as ICICI allows the policyholders to surrender it during the free-look period with zero to minimal charges.

Surrendering during the Free-look period:

The Free-look period refers to the first 15 days from the date the policy is purchased.

If you are not satisfied with the policy’s “Terms and conditions”, you can return the policy to the company along with the policy document within 15 days from the date of receipt of the policy bond.

But if you bought the policy through distance marketing, you have 30 days of the free-look period to surrender the policy.

The company will terminate your policy and refund the premium deposited on the receipt as same.

Your premium would be deducted upon deposit based on some minimal charges like;

- Stamp duty under the policy,

- Expenses that are borne by the Company on medical examination if any

- The proportionate risk premium for the period of cover

Surrendering after the free-look period:

What if your policy is way past the free-look period?

In that case, you still have the option to surrender the policy on the below conditions:

- If the policyholder had chosen the single pay option as your premium payment option, they can surrender their policy at any time during the policy term.

- If the policyholder had chosen other premium payment options, they can still surrender their policy at any time during the policy term if they have completed paying two full years of premium.

But the policyholder can avail of the surrender value benefit only under this situation:

The Guaranteed Surrender Value (GSV) payable during the policy term is equal to the total premiums paid multiplied by the Guaranteed Surrender Value factor.

The Special Surrender Value (SSV) is for policies surrendering before the premium payment of five full policy years. It will be calculated as the Guaranteed Surrender Value Factor multiplied by total premiums paid which are multiplied by the Guaranteed Cash Value factor for Vested Bonuses.

So, before surrendering/canceling your policy, it is best to consult with your Financial Advisor to make the right decision.

Do you want to see and hear ICICI Pru Guaranteed Income For Tomorrow (GIFT) Plan Review in Hindi?

With an expert view of the precise illustrations and calculations, we have decoded every aspect of the official brochure. Click below for our Youtube Hindi Review.

ICICI Pru Guaranteed Income For Tomorrow: Final thoughts about the review:

The ICICI Pru Guaranteed Income For Tomorrow (GIFT) seems like an advantageous life insurance plan with various benefits displayed to us.

But as we have seen through ourselves by digging deep into reviewing this insurance product, we know now that it is not the best life insurance plan out there.

There are lots of other better alternatives where you can claim your life insurance with a high-value life cover and also invest in different streams according to your risk appetite.

So, at the end of this comprehensive analysis of ICICI Pru Guaranteed Income For Tomorrow, it’s clear how important it is to fully comprehend the financial product before investing

There is a lot of free advice available on social media platforms like Quora, Twitter, Facebook, etc.

We can avoid most of the pitfalls in our investment journey if we avoid trusting amateur advice and take the help of a professional financial planner.

If you have any comments or questions, write them in the comment box below.

Or are you interested in creating a Comprehensive Financial Plan for your financial goals?

If you have any comments or questions, write them in the comment box below.

Or are you interested in creating a Comprehensive Financial Plan for your financial goals?

Skip the queue by registering for your 30 Minute FREE Financial Plan Consultation. Click the ‘‘BOOK YOUR SLOT NOW!’’ button below.

I want to know a better Term Insurance

To find the best term insurance, consider factors like coverage amount, policy tenure, premium affordability, claim settlement ratio, and additional riders (like critical illness or accidental death benefit). Reviewing and comparing policies from reputable insurers can help you make an informed decision. For personalized advice and a tailored plan, register for a complimentary financial plan consultation at Holistic Investment https://www.holisticinvestment.in/complimentary-financial-plan-consultation/. We offer expert guidance to align insurance with your financial goals.

Hi Thanks for the insight.

Just one clarification on this ICICI Pru Guaranteed Income For Tomorrow {Yearly premium =ONE LAC Rupees}.

This one has 12 yrs premium paying term and 2 yrs of wait period and a low life cover of 10 lacs till 14 yrs (12 paying years + 2 yrs of wait period) and then it starts paying the assured TAX Free return of Rs, 1,52, 109 for next 25 yrs or a lump sum withdrawl of Rs. 38,02,725

So is there any scheme where for a yrly deposit of Rs. 1 Lac for 12 yrs + 2 yrs wait period gives me a higher return from the 14th year for 25 yrs or a lumpsum?

Kindly suggest.

Vincent Alexander Anthony

Pl review and advise whether this guaranteed income can be part of the debt investment for a person with debt : equity asset allocation of 65:35

For example. Debt instruments say

1. SCSS- 15L

2. PMVVY-15L

3. RBI floating rate bond-25L

4. Guaranteed income-30L

5 . Short term / corporate bond fund etc- 50L

ICICI Pru Guaranteed Income is a type of annuity plan that provides regular income for a specified period or for life. It can complement your existing debt investments like SCSS, PMVVY, RBI floating rate bonds, and corporate bond funds. However, it’s crucial to note that annuities typically have a longer-term commitment and may not offer liquidity compared to other debt instruments or bond funds. Evaluate based on your income needs, risk tolerance, and liquidity requirements before including ICICI Pru Guaranteed Income in your portfolio.