Can the IndiaFirst Life Growth of Life Dreams Plus Plan truly help you turn your financial dreams into reality, or is it just another market-linked insurance plan with average returns?

Does the IndiaFirst Life Growth of Life Dreams Plus Plan offer the ideal combination of wealth creation and life insurance, or are there better alternatives to consider?

Can the IndiaFirst Life Growth of Life Dreams Plus Plan deliver meaningful long-term wealth while protecting your loved ones, or does it require careful scrutiny before investing?

In this article, we take a detailed look at the plan’s features, benefits, and drawbacks to help you evaluate whether it is the right choice. You’ll also gain a better understanding of bundled insurance-cum-investment plans and whether they are suitable for your financial goals.

Table of Contents:

What is the IndiaFirst Life Growth of Life Dream Plus?

What are the features of the IndiaFirst Life Growth of Life Dream Plus?

Who is eligible for the IndiaFirst Life Growth of Life Dream Plus?

What are the benefits of the IndiaFirst Life Growth of Life Dream Plus?

Grace Period, Discontinuance and Revival of the IndiaFirst Life Growth of Life Dream Plus

Free Look Period for the IndiaFirst Life Growth of Life Dream Plus

Surrendering the IndiaFirst Life Growth of Life Dream Plus

What are the advantages of the IndiaFirst Life Growth of Life Dream Plus?

What are the disadvantages of the IndiaFirst Life Growth of Life Dream Plus?

Research Methodology of IndiaFirst Life Growth of Life Dreams Plus

Benefit Illustration – IRR Analysis of IndiaFirst Life Growth of Life Dreams Plus

IndiaFirst Life Growth of Life Dream Plus Vs. Other Investment

IndiaFirst Life Growth of Life Dream Plus Vs. Pure-term + Equity Mutual Fund

Final Verdict on IndiaFirst Life Growth of Life Dream Plus

What is the IndiaFirst Life Growth of Life Dream Plus?

IndiaFirst Life Growth of Life Dream Plus is a non-linked, participating, individual life insurance savings plan.

It offers a shorter pay commitment of Single Pay or Limited pay of 6, 8, 10 or 12 years and provides regular income in the form of Guaranteed Income PLUS Cash Bonus, if any, for 20, 30, 40 years OR for the whole of life till age 100, along with a flexibility to choose Life Cover depending on your needs across all life stages.

What are the features of the IndiaFirst Life Growth of Life Dream Plus?

- Two Plan Options: Choose between Immediate Income and Deferred Income, based on your financial needs. You can start receiving income as early as the end of the first policy month or defer it to a later date.

- Guaranteed Long-Term Income: Receive a guaranteed income for an extended period, with benefits available for up to 100 years, helping provide long-term financial security for your loved ones.

- Life Insurance Cover: Provides life insurance protection throughout the policy term to help safeguard your family’s financial future.

- Annual Bonus Eligibility: Participate in the insurer’s profits through Cash Bonus and Terminal Bonus, if declared.

- Goal Protection Benefit (GPB): In the event of the life assured’s death, all future premiums are waived, the death benefit is paid immediately as a lump sum, and the future policy benefits continue to be paid to the nominee as originally planned.

- ‘Save the Date’ Feature: Choose a specific date each year to receive your annual income, such as a birthday, anniversary, or any other special occasion.

- Special Discount for Women: Female policyholders are eligible for a discount on the first-year premium.

- Tax Benefits: Tax benefits on premiums paid and benefits received are available as per the prevailing tax laws.

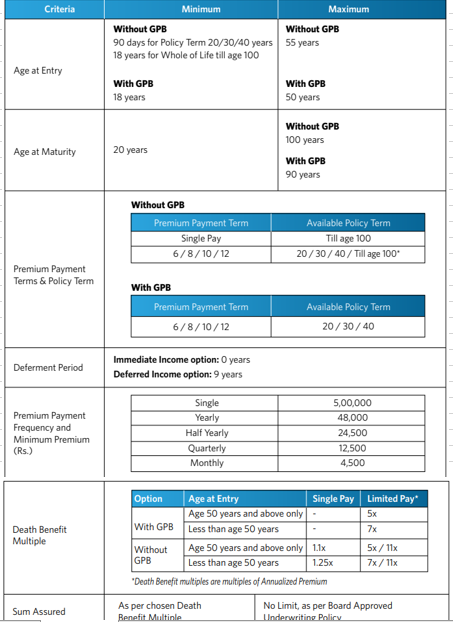

Who is eligible for the IndiaFirst Life Growth of Life Dream Plus?

What are the benefits of the IndiaFirst Life Growth of Life Dream Plus?

At the inception of the IndiaFirst Life Growth of Life Dreams Plus Plan Policy, you have to choose from 2 plan Options. This plan option will determine when your Survival Benefits start:

Immediate Income option: Start receiving Survival Benefits from Policy Year 1. Get Maturity Benefit at the end of the Policy Term.

Deferred Income option: Start receiving Survival Benefits from Policy Year 10. Get Maturity Benefit at the end of the Policy Term. Also, you will have the option to choose the Goal Protection Benefit (GPB) for extra protection.

1. Survival Benefit

In both Plan options, you pay premiums for a certain period and receive a Survival Benefit till the end of the Policy Term as per the chosen Income Payment Frequency. The amount of Survival Benefit payable has two components:

- Guaranteed Income will be guaranteed throughout the Policy Term and will vary based on Age at Entry, Gender, Premium amount, Premium Payment Term, Policy Term & Plan option chosen.

- Cash Bonus, if any, will be payable along with Guaranteed Income and will depend on the company’s future performance.

2. Maturity Benefit

On reaching the end of the Policy Term, provided the IndiaFirst Life Growth of Life Dreams Plus Plan Policy is in force, and all due Premiums have been paid, the Policyholder will receive the sum of:

- Guaranteed Sum Assured on Maturity, PLUS

- Terminal Bonus, if any

3. Death Benefit

In the unfortunate event of the death of the Life Insured anytime during the Policy Term, provided the Policy is in force or fully paid-up, the Death Benefit shall be payable to the nominee. The Death Benefit will vary depending on the Goal Protection Benefit chosen.

Without Goal Protection Benefit:

On the death of Life Assured any time during the IndiaFirst Life Growth of Life Dreams Plus Plan policy term, provided all due premiums have been paid, the death benefit as given below is paid, and the policy terminates.

The death benefit payable will be the higher of:

- Sum Assured on Death

- 105% of Total Premiums Paid till date of death

- Higher of Guaranteed Surrender Value (GSV) and Special Surrender Value (SSV), PLUS Terminal Bonus, if any

With Goal Protection Benefit:

On the death of Life Assured any time during the IndiaFirst Life Growth of Life Dreams Plus Plan Policy Term, provided all due Premiums have been paid, and the Policy is in force, the Death Benefit as given below is payable. The death benefit payable will be the higher of:

- Sum Assured on Death

- 105% of Total Premiums Paid till date of death

- Higher of Guaranteed Surrender Value (GSV) and Special Surrender Value (SSV).

Grace Period, Discontinuance and Revival of the IndiaFirst Life Growth of Life Dream Plus

Grace Period

You are provided a Grace Period of 15 days under the monthly mode and 30 days for other premium payment modes in case you miss your due premium on the due dates.

Discontinuance

In the event of non-payment of due premiums within the grace period, the policy will lapse if it has not acquired a paid-up value. The risk cover will cease, and no further benefits will be payable in case of a lapsed policy.

In case of non-payment of premium within the grace period, the IndiaFirst Life Growth of Life Dreams Plus Plan policy will acquire paid-up value provided at least one full year’s premium has been paid.

Revival

You may revive your Policy within 5 years from the due date of first unpaid regular premium but before the Maturity Date.

Free Look Period for the IndiaFirst Life Growth of Life Dream Plus

You can return your policy within a free look period. In case you disagree with any of the terms and conditions and have not made any claim, you shall have the option of returning the policy for cancellation, stating the reasons for the same, within 30 days from receipt of your policy document, whether received electronically or otherwise.

Surrendering the IndiaFirst Life Growth of Life Dream Plus

You may surrender this Policy during the IndiaFirst Life Growth of Life Dreams Plus Plan Policy Term after the Policy has acquired the Surrender Value. Please remember, you cannot revive your Policy once it is surrendered.

The amount payable on surrender will be the higher of Guaranteed Surrender Value (GSV) and Special Surrender Value (SSV), less any survival benefits already paid.

What are the advantages of the IndiaFirst Life Growth of Life Dream Plus?

- Goal Protection Benefit (GPB): In the event of the life assured’s death during the policy term, all future policy benefits continue to the nominee, ensuring the intended financial goal is not disrupted.

- Flexible Survival Benefit Payout: You can choose to receive the survival benefit on a special date of your choice instead of the policy anniversary.

- Special Discounts: Discounts are available for women policyholders and for paying premiums in advance.

- Higher Maturity Benefits for Higher Premiums: Policies with an annualised premium of ₹1,00,000 or more are eligible for higher enhancement factors on the Guaranteed Sum Assured on Maturity (GSAM).

- Optional Rider Benefits: You can enhance your coverage by opting for up to three riders, subject to eligibility and the plan’s terms and conditions.

- Loan Facility: The plan allows you to avail of a loan of up to 80% of the acquired surrender value, subject to the policy terms.

What are the disadvantages of the IndiaFirst Life Growth of Life Dream Plus?

- Early Income Reduces Wealth Creation: Opting for early income payouts limits the amount that remains invested, reducing the power of compounding and potentially lowering long-term wealth creation.

- Inadequate Life Cover: The sum assured offered under the plan may not be sufficient to meet your family’s long-term financial protection needs.

- Risk of Discretionary Spending: Regular income payouts may encourage unnecessary or discretionary spending instead of being used for long-term financial goals.

- No Flexibility to Defer Income: Once the income payout starts, it cannot be deferred or postponed based on changing financial needs.

Research Methodology of IndiaFirst Life Growth of Life Dreams Plus

The IndiaFirst Life Growth of Life Dreams Plus Plan offers regular income after the premium-paying term, with the survival benefits comprising both guaranteed income and bonuses.

Before investing, it is important to evaluate whether the plan delivers satisfactory long-term returns. Using the illustration provided in the IndiaFirst Life Growth of Life Dreams Plus Plan policy brochure, let’s analyse the estimated returns and compare them with other investment alternatives.

Benefit Illustration – IRR Analysis of IndiaFirst Life Growth of Life Dreams Plus

Consider a 50-year-old male who opts for the IndiaFirst Life Growth of Life Dreams Plus Plan with a 50-year policy term and a 10-year premium-paying term, paying an annual premium of ₹2 lakh.

The plan provides a sum assured of ₹22 lakh. He chooses Deferred Income Option.

|

Male |

50 years |

|

Sum Assured |

₹ 22,00,000 |

|

Policy Term |

50 years |

| Premium Paying Term |

10 years |

| Annualised Premium |

₹ 2,00,000 |

After completing the premium payments, he starts receiving annual survival benefits, including bonuses. At the end of the policy term, he receives the maturity benefit along with the terminal bonus.

The benefit illustration is based on assumed investment returns of 4% and 8%, which are only illustrative and not guaranteed. The actual benefits will depend on the insurer’s future bonus declarations.

|

At 4% p.a. |

At 8% p.a. |

||||

|

Age |

Year | Annualised premium / Maturity benefit | Death benefit | Annualised premium / Maturity benefit | Death benefit |

| 50 | 1 | -2,00,000 | 22,00,000 | -2,00,000 |

22,00,000 |

|

51 |

2 | -2,00,000 | 22,00,000 | -2,00,000 | 22,00,000 |

| 52 | 3 | -2,00,000 | 22,00,000 | -2,00,000 |

22,00,000 |

|

53 |

4 | -2,00,000 | 22,00,000 | -2,00,000 | 22,00,000 |

| 54 | 5 | -2,00,000 | 22,00,000 | -2,00,000 |

22,00,000 |

|

55 |

6 | -2,00,000 | 22,00,000 | -2,00,000 | 22,00,000 |

| 56 | 7 | -2,00,000 | 22,00,000 | -2,00,000 |

22,00,000 |

|

57 |

8 | -2,00,000 | 22,00,000 | -2,00,000 | 22,00,000 |

| 58 | 9 | -2,00,000 | 22,00,000 | -2,00,000 |

22,00,000 |

|

59 |

10 | -2,00,000 | 22,00,000 | -2,00,000 | 22,00,000 |

| 60 | 11 | 0 | 22,00,000 | 0 |

22,00,000 |

|

61 |

12 | 45,720 | 22,00,000 | 1,08,520 | 22,00,000 |

| 62 | 13 | 45,720 | 22,00,000 | 1,08,520 |

22,00,000 |

|

63 |

14 | 45,720 | 22,00,000 | 1,08,520 | 22,00,000 |

| 64 | 15 | 45,720 | 22,00,000 | 1,08,520 |

22,00,000 |

|

65 |

16 | 45,720 | 22,00,000 | 1,08,520 | 22,00,000 |

| 66 | 17 | 45,720 | 22,00,000 | 1,08,520 |

22,00,000 |

|

67 |

18 | 45,720 | 22,00,000 | 1,08,520 | 22,00,000 |

| 68 | 19 | 45,720 | 22,00,000 | 1,08,520 |

22,00,000 |

|

69 |

20 | 45,720 | 22,00,000 | 1,08,520 | 22,00,000 |

| 70 | 21 | 45,720 | 22,00,000 | 1,08,520 |

22,00,000 |

|

71 |

22 | 45,720 | 22,00,000 | 1,08,520 | 22,00,000 |

| 72 | 23 | 45,720 | 22,00,000 | 1,08,520 |

22,00,000 |

|

73 |

24 | 45,720 | 22,00,000 | 1,08,520 | 22,00,000 |

| 74 | 25 | 45,720 | 22,00,000 | 1,08,520 |

22,00,000 |

|

75 |

26 | 45,720 | 22,00,000 | 1,08,520 | 22,00,000 |

| 76 | 27 | 45,720 | 22,00,000 | 1,08,520 |

22,00,000 |

|

77 |

28 | 45,720 | 22,00,000 | 1,08,520 | 22,00,000 |

| 78 | 29 | 45,720 | 22,00,000 | 1,08,520 |

22,00,000 |

|

79 |

30 | 45,720 | 22,00,000 | 1,08,520 | 22,00,000 |

| 80 | 31 | 45,720 | 22,00,000 | 1,08,520 |

22,00,000 |

|

81 |

32 | 45,720 | 22,00,000 | 1,08,520 | 22,00,000 |

| 82 | 33 | 45,720 | 22,00,000 | 1,08,520 |

22,00,000 |

|

83 |

34 | 45,720 | 22,00,000 | 1,08,520 | 22,00,000 |

| 84 | 35 | 45,720 | 22,00,000 | 1,08,520 |

22,00,000 |

|

85 |

36 | 45,720 | 22,00,000 | 1,08,520 | 22,00,000 |

| 86 | 37 | 45,720 | 22,00,000 | 1,08,520 |

22,00,000 |

|

87 |

38 | 45,720 | 22,00,000 | 1,08,520 | 22,00,000 |

| 88 | 39 | 45,720 | 22,00,000 | 1,08,520 |

22,00,000 |

|

89 |

40 | 45,720 | 22,00,000 | 1,08,520 | 22,00,000 |

| 90 | 41 | 45,720 | 22,00,000 | 1,08,520 |

22,00,000 |

|

91 |

42 | 45,720 | 22,00,000 | 1,08,520 | 22,00,000 |

| 92 | 43 | 45,720 | 22,00,000 | 1,08,520 |

22,00,000 |

|

93 |

44 | 45,720 | 22,00,000 | 1,08,520 | 22,00,000 |

| 94 | 45 | 45,720 | 22,00,000 | 1,08,520 |

22,00,000 |

|

95 |

46 | 45,720 | 22,00,000 | 1,08,520 | 22,00,000 |

| 96 | 47 | 45,720 | 22,00,000 | 1,08,520 |

22,00,000 |

|

97 |

48 | 45,720 | 22,00,000 | 1,08,520 | 22,00,000 |

| 98 | 49 | 45,720 | 22,00,000 | 1,08,520 |

22,00,000 |

|

99 |

50 | 45,720 | 22,00,000 | 1,08,520 | 22,00,000 |

| 100 | 41,46,420 |

1,64,09,284 |

|||

|

IRR |

2.94% |

6.47% |

|||

Under the 4% illustration, the estimated annual income is ₹45,720, and the projected maturity benefit is around ₹41 lakh, resulting in an Internal Rate of Return (IRR) of 2.94% as per the IndiaFirst Life Growth of Life Dreams Plus Plan maturity calculator.

This is even lower than the interest rate offered by a typical savings account.

Under the 8% illustration, the estimated annual income increases to ₹1.08 lakh, with a projected maturity benefit of ₹1.63 crore.

Even then, the plan generates an IRR of only 6.47% as per the IndiaFirst Life Growth of Life Dreams Plus Plan maturity calculator, which remains lower than the returns currently offered by many bank fixed deposits.

Moreover, the regular income paid under the plan is fixed and does not increase with inflation, reducing its purchasing power over time.

Although the policy provides income for an extended period of 50 years, the overall returns are relatively modest.

Considering its limited life insurance cover, low return potential, and the impact of inflation on fixed payouts, the IndiaFirst Life Growth of Life Dreams Plus Plan may not be a suitable option for investors seeking long-term wealth creation and adequate financial protection.

IndiaFirst Life Growth of Life Dream Plus Vs. Other Investment

The return analysis shows that the IndiaFirst Life Growth of Life Dreams Plus Plan offers relatively modest returns. The same premium can potentially generate similar cash flows more efficiently through an alternative strategy.

Instead of combining insurance and investment in a single product, separating these two components can provide better flexibility, higher returns, and adequate financial protection. Let us examine this using the same premium from the previous illustration.

IndiaFirst Life Growth of Life Dream Plus Vs. Pure-term + Equity Mutual Fund

A pure-term life insurance policy with a sum assured of ₹22 lakh requires an annual premium of ₹38,900 for a 20-year policy term with a 10-year premium-paying term.

This leaves ₹1,61,000 each year available for investment based on the investor’s risk appetite.

|

Pure Term Life Insurance Policy |

|

|

Sum Assured |

₹ 22,00,000 |

| Policy Term |

20 years |

|

Premium Paying Term |

10 years |

| Annualised Premium |

₹ 38,900 |

|

Investment |

₹ 1,61,100 |

Conservative investors may prefer debt-oriented options such as the Public Provident Fund (PPF), while investors with a higher risk tolerance may opt for equity mutual funds.

For this comparison, we have considered the equity mutual fund route.

|

|

Term insurance + Equity Mutual Fund |

||

|

Age |

Year | Term Insurance premium + Equity Mutual Fund | Death benefit |

| 50 | 1 | -2,00,000 |

22,00,000 |

|

51 |

2 | -2,00,000 | 22,00,000 |

| 52 | 3 | -2,00,000 |

22,00,000 |

|

53 |

4 | -2,00,000 | 22,00,000 |

| 54 | 5 | -2,00,000 |

22,00,000 |

|

55 |

6 | -2,00,000 | 22,00,000 |

| 56 | 7 | -2,00,000 |

22,00,000 |

|

57 |

8 | -2,00,000 | 22,00,000 |

| 58 | 9 | -2,00,000 |

22,00,000 |

|

59 |

10 | -2,00,000 | 22,00,000 |

| 60 | 11 | 0 |

22,00,000 |

|

61 |

12 | 1,08,520 | 22,00,000 |

| 62 | 13 | 1,08,520 |

22,00,000 |

|

63 |

14 | 1,08,520 | 22,00,000 |

| 64 | 15 | 1,08,520 |

22,00,000 |

|

65 |

16 | 1,08,520 | 22,00,000 |

| 66 | 17 | 1,08,520 |

22,00,000 |

|

67 |

18 | 1,08,520 | 22,00,000 |

| 68 | 19 | 1,08,520 |

22,00,000 |

|

69 |

20 | 1,08,520 | 22,00,000 |

| 70 | 21 |

1,08,520 |

|

|

71 |

22 | 1,08,520 | |

| 72 | 23 |

1,08,520 |

|

|

73 |

24 | 1,08,520 | |

| 74 | 25 |

1,08,520 |

|

|

75 |

26 | 1,08,520 | |

| 76 | 27 |

1,08,520 |

|

|

77 |

28 | 1,08,520 | |

| 78 | 29 |

1,08,520 |

|

|

79 |

30 | 1,08,520 | |

| 80 | 31 |

1,08,520 |

|

|

81 |

32 | 1,08,520 | |

| 82 | 33 |

1,08,520 |

|

|

83 |

34 | 1,08,520 | |

| 84 | 35 |

1,08,520 |

|

|

85 |

36 | 1,08,520 | |

| 86 | 37 |

1,08,520 |

|

|

87 |

38 | 1,08,520 | |

| 88 | 39 |

1,08,520 |

|

|

89 |

40 | 1,08,520 | |

| 90 | 41 |

1,08,520 |

|

|

91 |

42 | 1,08,520 | |

| 92 | 43 |

1,08,520 |

|

|

93 |

44 | 1,08,520 | |

| 94 | 45 |

1,08,520 |

|

|

95 |

46 | 1,08,520 | |

| 96 | 47 |

1,08,520 |

|

|

97 |

48 | 1,08,520 | |

| 98 | 49 |

1,08,520 |

|

|

99 |

50 | 1,08,520 | |

| 100 |

3,56,55,482 |

||

|

|

IRR |

7.79% |

|

At the end of the accumulation phase, the equity mutual fund corpus is transferred to an investment earning 7% annually.

This corpus is then used to generate annual withdrawals that match the cash flows illustrated under the 8% return scenario of the IndiaFirst Life Growth of Life Dreams Plus Plan, with the remaining balance being fully redeemed at maturity.

The equity mutual fund investment accumulates to a pre-tax corpus of ₹31.66 lakh. After accounting for capital gains tax, the post-tax corpus is ₹29.87 lakh.

This amount is invested in a 7% return-generating instrument, from which annual withdrawals are made to replicate the plan’s income payouts, followed by complete redemption at maturity. This strategy delivers an Internal Rate of Return (IRR) of 7.79%.

|

Equity Mutual Fund Tax Calculation |

|

| Maturity value after 10 years |

31,66,353 |

|

Purchase price |

16,11,000 |

| Long-Term Capital Gains |

15,55,353 |

|

Exemption limit |

1,25,000 |

| Taxable LTCG |

14,30,353 |

|

Tax paid on LTCG |

1,78,794 |

| Maturity value after tax |

29,87,559 |

The effective return can be even higher if annual withdrawals are not required, as the corpus continues to compound.

More importantly, this approach offers significantly greater flexibility, allowing investors to withdraw money only when needed rather than receiving fixed payouts irrespective of their financial requirements.

Compared with this strategy, the IndiaFirst Life Growth of Life Dreams Plus Plan offers lower returns, limited flexibility, and less efficient long-term wealth creation.

Final Verdict on IndiaFirst Life Growth of Life Dream Plus

The IndiaFirst Life Growth of Life Dreams Plus Plan is a traditional insurance-cum-investment product that combines life cover with regular income. It allows you to receive periodic cash flows either immediately after the premium-paying term or at a deferred stage.

However, a significant portion of the survival and maturity benefits is non-guaranteed, as these depend on future bonus declarations.

In addition, the life insurance cover provided under the plan may not be sufficient to meet your family’s long-term financial needs and it also has a high agent commission.

The plan’s regular income feature also comes at a cost. Annual payouts interrupt the compounding of your investment, which can significantly reduce long-term wealth creation.

If your objective is to generate regular income, separating insurance from investment is generally a more efficient approach.

The combination of limited life cover, non-guaranteed benefits, and relatively modest returns makes the IndiaFirst Life Growth of Life Dreams Plus Plan a less suitable option for long-term investors.

To adequately protect your family’s financial future, consider purchasing a pure-term life insurance policy with sufficient coverage. For wealth creation, invest separately in products that match your risk appetite, financial goals, and investment horizon.

Instead of depending on insurance plans for regular income, building a well-diversified investment portfolio can provide greater flexibility, better return potential, and improved control over your cash flows.

Do Quora, Facebook, and Twitter have the final say when it comes to financial advice?

For a personalised financial strategy, consult a Certified Financial Planner (CFP) who can help you choose the right combination of insurance and investment products based on your individual needs and long-term objectives.

Leave a Reply