Can the IndiaFirst Life TULIP Pro Plan truly help you build long-term wealth while providing life insurance, or is it just another ULIP with limited advantages?

Does the IndiaFirst Life TULIP Pro Plan offer the right balance of investment growth and financial protection, or are there better options available?

Is the IndiaFirst Life TULIP Pro Plan a smart choice for achieving your financial goals, or could its costs and features impact your returns?

In this article, we take a detailed look at the plan’s features, benefits, returns, and limitations to help you evaluate whether it is the right choice for your financial needs and make a well-informed investment decision.

Table of Contents:

What is the IndiaFirst Life TULIP Pro Plan?

What are the features of the IndiaFirst Life TULIP Pro Plan?

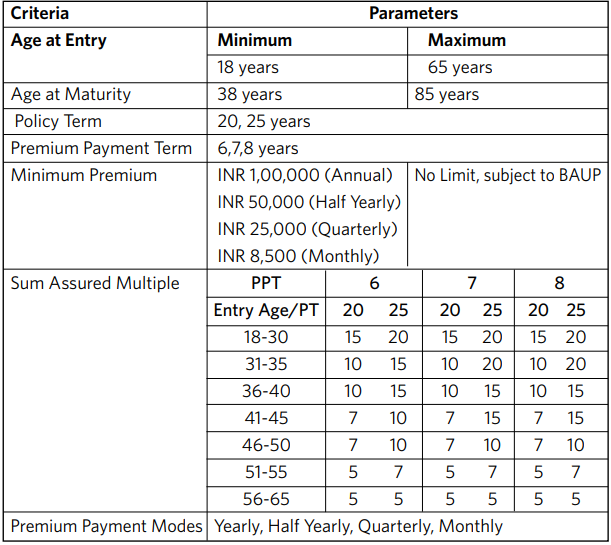

Who is eligible for the IndiaFirst Life TULIP Pro Plan?

What are the benefits of the IndiaFirst Life TULIP Pro Plan?

What are the investment strategies and fund options of IndiaFirst Life TULIP Pro?

What are the charges of the IndiaFirst Life TULIP Pro?

Grace Period, Discontinuance and Revival of the IndiaFirst Life TULIP Pro Plan

Free Look Period for the IndiaFirst Life TULIP Pro Plan

Surrendering the IndiaFirst Life TULIP Pro Plan?

What are the advantages of the IndiaFirst Life TULIP Pro Plan?

What are the disadvantages of the IndiaFirst Life TULIP Pro Plan?

Research Methodology of IndiaFirst Life TULIP Pro Plan

Benefit Illustration – IRR Analysis of IndiaFirst Life TULIP Pro Plan

IndiaFirst Life TULIP Pro Vs. Other Investments

IndiaFirst Life TULIP Pro Vs. Pure-term + Equity Mutual Fund

Final Verdict on IndiaFirst Life TULIP Pro Plan

What is the IndiaFirst Life TULIP Pro Plan?

IndiaFirst Life TULIP Pro Plan is a non-par, unit-linked, individual savings life insurance plan. It provides life cover for those who want term-like protection as well as maximise returns on their savings and create additional wealth for a comfortable life ahead. Rider cover adds to the protection.

What are the features of the IndiaFirst Life TULIP Pro Plan?

- Offers life insurance coverage of up to 20 times the annual premium.

- Pays the fund value as the maturity benefit at the end of the policy term.

- Provides a choice of 10 fund options to suit different risk appetites.

- Enhances savings through the Return of Premium Allocation Charge and Return of Mortality Charge.

- Allows unlimited free fund switches and premium redirection to help optimise your investment portfolio.

- Offers tax benefits, subject to prevailing tax laws.

- Enables additional protection through the Term Rider, Accidental Death Benefit Rider, and Total & Permanent Disability Rider.

- Provides multiple investment strategies to help maximise long-term wealth creation.

Who is eligible for the IndiaFirst Life TULIP Pro Plan?

What are the benefits of the IndiaFirst Life TULIP Pro Plan?

1. Death benefits

In the untimely event of the life assured’s demise while the IndiaFirst Life TULIP Pro Plan policy is in force or from the due date of the first unpaid premium till the expiry of the grace period, the Nominee(s)/Appointee/Legal Heir, as the case may be, will receive the death benefit under the policy equal to the higher of

- Fund value as on the date of receipt of intimation of death or

- Sum assured or

- 105% of the total premiums paid.

The amount of Sum Assured on death shall be reduced to the extent of the partial withdrawals made during the two years immediately preceding the date of death of the Life Assured.

The lump sum amount payable at the time of death will be payable either as a lump sum payout or in monthly instalments

2. Survival Benefit

In case Life Assured survives until the end of the specified period (other than maturity), Return of Premium Allocation Charges, i.e., Y% (as mentioned below) of Premium Allocation Charges (PAC) collected, shall be added to the Fund Value as specified below

|

Policy Year (Specified Period) |

Policy Term | |

| 20 years | 25 years | |

| 15 | 100% |

100% |

|

20 |

200% | 200% |

| 25 | NA |

300% |

3. Maturity Benefit

In case Life Assured survives till the end of IndiaFirst Life TULIP Pro Plan Policy Term, the Fund Value, as on the Maturity Date or as per the Settlement Option chosen, PLUS Return of Mortality Charges, i.e., (100% of Mortality Charges collected during the Policy Term), shall be payable.

The amount payable under the Return of Mortality Charges, including any extra mortality charged, if any, shall exclude any GST and cess with respect to Mortality Charges that have been deducted.

What are the investment strategies and fund options of IndiaFirst Life TULIP Pro?

IndiaFirst Life Term TULIP Pro boasts of multiple investment strategies. You can choose and opt for any one of the strategies below to ensure that you are getting the optimum returns out of your premiums.

A. Self-Managed Strategy

Under this option, you get access to 10 segregated funds below, control over how to utilise your premiums and full freedom to switch from one fund to another.

You can choose to put your premiums in one, multiple or all of these options based on your risk appetite and needs.

|

|

Asset Allocation | ||||

| S. No | Fund Name | Equity | Debt | Money Market |

Returns and Risk Profile |

|

1 |

Equity1 | 80-100% | 0 | 0-20% | High |

| 2 | Debt1 | 0 | 70-100% | 0-30% |

Moderate |

|

3 |

Multi-Cap Equity Fund | 70-100% | 0 | 0-30% | Very High |

| 4 | Value Fund | 70-100% | 0 | 0-30% |

Very High |

|

5 |

Macro Trends Fund | 70-100% | 0 | 0-30% | High |

| 6 | Equity Elite Opportunities | 60-100% | 0 | 0-40% |

High |

|

7 |

Liquid 1 Fund | 0 | 0-20% | 80-100% | Low |

| 8 | Flexi Cap Equity Fund | 65-100% | 0% | 0-35% |

Moderate to High |

|

9 |

Sustainable Equity Fund | 80-100% | 0 | 0-20% | Moderate to High |

| 10 | Large Cap Equity Fund | 80-100% | 0 | 0-20% |

High |

B. Age-Based Investment Strategy

Your premium after deduction of applicable charges will be distributed between Equity1 Fund, Debt1 Fund and Value Fund based on your age.

As you grow older and move from one band to another, your funds are redistributed. This strategy will balance your portfolio and adjust the risk exposure as you grow older. The age-wise fund distribution is shown in the table below.

|

Age (Years) |

Equity 1 | Debt1 | Value |

| Upto25 | 40% | 30% |

30% |

|

26-35 |

35% | 40% | 25% |

| 36-45 | 30% | 50% |

20% |

|

46-55 |

25% | 60% | 15% |

| 56-65 | 20% | 70% |

10% |

|

66-70 |

15% | 80% | 5% |

| 71 & above | 5% | 90% |

5% |

C. Smart Switch Strategy:

This investment strategy is designed to systematically move your savings into low-risk fund options near maturity to safeguard your returns. In this strategy, you may choose to save in any or all of the 10 available fund options.

When you choose this strategy, funds are systematically moved to the Liquid 1 Fund in the last 5 policy years to ensure your hard-earned money is secure from any sudden market dips.

The movement to the Liquid 1 Fund will happen in the manner specified as per the table below –

|

Start of Policy Year |

Fund allocation in Chosen Funds | Liquid1 Fund Allocation |

| T-4 | 80% |

20% |

|

T-3 |

70% | 30% |

| T-2 | 40% |

60% |

|

T-1 |

10% | 90% |

| T | 0% |

100% |

What are the charges of the IndiaFirst Life TULIP Pro?

i. Fund Management Charge (FMC)

The fund management charge for the various funds offered under this plan is 1.35% per annum. The fund management charge applicable for the discontinuance fund is 0.50% p.a. on the discontinuance fund value.

ii. Mortality Charge

The mortality charges are based on the age and sex of the life assured. The Annual mortality charge rates are guaranteed for the entire duration of the IndiaFirst Life TULIP Pro Plan policy.

iii. Premium Allocation Charge

As % of Annualised Premium

For Annual Premium less than 2 Lacs

Year 1 – 9%, Year 2 – 6%, Years 3 to 5 – 3%, Year 6+ – Nil

For Annual Premium more than 2 Lacs

Year 1 – 6%, Year 2 – 4%, Year 3 to 5 – 3%, Year 6+ – Nil

iv. Policy Administration Charge

For the first 5 policy years – The charges are 1% of first year’s premium per annum subject to maximum of INR 6,000 per annum

v. Partial Withdrawal Charge

There are no partial withdrawal charges applicable.

vi. Revival Charge

There are no revival charges applicable.

vii. Switching Charge

You are allowed to make unlimited switches in a calendar month.

vii. Discontinuance charge

It depends on the year of discontinuance and the premium amount. There is no discontinuance charge from the 5th policy year.

Inference from the charges: Although the plan refunds certain charges, it doesn’t account for the time value of money. Moreover, some charges are deducted regularly throughout the IndiaFirst Life TULIP Pro Plan policy term. Over time, these ongoing deductions can significantly erode your investment value and reduce long-term returns.

Grace Period, Discontinuance and Revival of the IndiaFirst Life TULIP Pro Plan

Grace Period

A grace period of 30 days for payment of all premiums under quarterly, half-yearly, and yearly modes and 15 days under the monthly mode is given.

Discontinuance

Discontinuance of the Policy during the lock-in period: The policy shall be discontinued due to non-payment of premium, and the fund value, after deducting the applicable discontinuance charges, shall be credited to the discontinued policy fund and the risk cover shall cease.

At the end of the lock-in period, we will pay the proceeds of the discontinuance fund to you and terminate the IndiaFirst Life TULIP Pro Plan policy.

Discontinuance of the Policy after the Lock-in-period: The policy will be converted into a paid-up policy with reduced paid-up sum assured (original sum assured multiplied by the total number of premiums paid to the original number of premiums payable as per the terms and conditions of the policy).

Revival

Policy can be revived within the Revival Period of three years

Free Look Period for the IndiaFirst Life TULIP Pro Plan

You have a free look period of 30 (Thirty) days from the date of receipt of your Policy document, whether received electronically or otherwise, to review the terms and conditions of the IndiaFirst Life TULIP Pro Plan policy and in case you disagree with any of those terms and conditions, you shall have an option to return the policy.

Surrendering the IndiaFirst Life TULIP Pro Plan?

Surrender of the Policy during lock-in period: You also have the option to surrender the policy anytime, and the proceeds of the discontinued policy shall be payable at the end of the lock-in period or date of surrender, whichever is later.

Surrender of the Policy after the Lock-in-period: You also have the option to surrender the policy anytime, and we will pay the proceeds of the policy to you.

What are the advantages of the IndiaFirst Life TULIP Pro Plan?

- Offers a settlement option, allowing you to receive the maturity benefit in a phased manner.

- Provides enhanced insurance protection through optional riders available under the plan.

- Offers a premium discount for policies with an annualised premium of ₹2,00,000 or above.

- Allows unlimited fund switches throughout the policy term to align your investments with changing market conditions.

- Enables premium redirection, allowing future premiums to be allocated from one fund to another as per your investment strategy.

What are the disadvantages of the IndiaFirst Life TULIP Pro Plan?

- Policy loans are not permitted under this plan.

- Top-up premium is not allowed.

- The policy has a lock-in period of five years.

- Only the net premium, after deducting charges, is invested.

- The life cover provided is insufficient.

Research Methodology of IndiaFirst Life TULIP Pro Plan

Estimating the potential returns is essential when evaluating the IndiaFirst Life TULIP Pro, as it is a market-linked insurance plan.

Calculating the Internal Rate of Return (IRR) helps compare the plan with other investment alternatives and assess whether it delivers adequate value for the risk undertaken.

The following analysis is based on the benefit illustrations provided in the policy brochure.

Benefit Illustration – IRR Analysis of IndiaFirst Life TULIP Pro Plan

Consider a 35-year-old male purchasing the IndiaFirst Life TULIP Pro with a sum assured of ₹15 lakhs, a policy term of 25 years, a premium payment term of 6 years, and an annual premium of ₹1 lakh.

|

Male |

35 years |

|

Sum Assured |

₹ 15,00,000 |

| Policy Term |

25 years |

|

Premium Paying Term |

6 years |

| Annualised Premium |

₹ 1,00,000 |

Assuming all premiums are paid on time, the fund value becomes payable at the end of the policy term.

The policy brochure provides benefit illustrations based on assumed gross investment returns of 4% and 8%.

These are only illustrative rates and are not guaranteed. The actual maturity benefit will depend on the future performance of the chosen funds.

|

At 4% p.a. |

At 8% p.a. |

||||

|

Age |

Year | Annualised premium / Maturity benefit | Death benefit | Annualised premium / Maturity benefit |

Death benefit |

|

35 |

1 | -1,00,000 | 15,00,000 | -1,00,000 | 15,00,000 |

| 36 | 2 | -1,00,000 | 15,00,000 | -1,00,000 |

15,00,000 |

|

37 |

3 | -1,00,000 | 15,00,000 | -1,00,000 | 15,00,000 |

| 38 | 4 | -1,00,000 | 15,00,000 | -1,00,000 |

15,00,000 |

|

39 |

5 | -1,00,000 | 15,00,000 | -1,00,000 | 15,00,000 |

| 40 | 6 | -1,00,000 | 15,00,000 | -1,00,000 |

15,00,000 |

|

41 |

7 | 0 | 15,00,000 | 0 | 15,00,000 |

| 42 | 8 | 0 | 15,00,000 | 0 |

15,00,000 |

|

43 |

9 | 0 | 15,00,000 | 0 | 15,00,000 |

| 44 | 10 | 0 | 15,00,000 | 0 |

15,00,000 |

|

45 |

11 | 0 | 15,00,000 | 0 | 15,00,000 |

| 46 | 12 | 0 | 15,00,000 | 0 |

15,00,000 |

|

47 |

13 | 0 | 15,00,000 | 0 | 15,00,000 |

| 48 | 14 | 0 | 15,00,000 | 0 |

15,00,000 |

|

49 |

15 | 0 | 15,00,000 | 0 | 15,00,000 |

| 50 | 16 | 0 | 15,00,000 | 0 |

15,00,000 |

|

51 |

17 | 0 | 15,00,000 | 0 | 15,00,000 |

| 52 | 18 | 0 | 15,00,000 | 0 |

15,00,000 |

|

53 |

19 | 0 | 15,00,000 | 0 | 15,00,000 |

| 54 | 20 | 0 | 15,00,000 | 0 |

15,00,000 |

|

55 |

21 | 0 | 15,00,000 | 0 | 15,00,000 |

| 56 | 22 | 0 | 15,00,000 | 0 |

15,00,000 |

|

57 |

23 | 0 | 15,00,000 | 0 | 15,00,000 |

| 58 | 24 | 0 | 15,00,000 | 0 |

15,00,000 |

|

59 |

25 | 0 | 15,00,000 | 0 | 15,00,000 |

|

60 |

9,60,128 |

21,93,726 |

|||

| IRR | 2.11% |

5.91% |

|||

- At an assumed 4% investment return, the projected fund value is ₹9.60 lakhs, translating to an IRR of just 2.11% as per the IndiaFirst Life TULIP Pro Plan maturity calculator, which is even lower than the interest offered by many savings bank accounts.

- At an assumed 8% investment return, the projected fund value increases to ₹21.93 lakhs, resulting in an IRR of 5.91% as per the IndiaFirst Life TULIP Pro Plan maturity calculator, which is comparable to, or in some cases lower than, the returns offered by bank fixed deposits.

Considering that your money remains invested for 25 years, the returns appear relatively modest. The plan exposes you to market risk without generating returns that adequately compensate for that risk.

In addition, the ₹15 lakh life cover is unlikely to provide sufficient financial protection for most families.

Overall, the combination of sub-optimal returns, disproportionate risk-reward, and inadequate insurance coverage makes the IndiaFirst Life TULIP Pro a less compelling option for achieving long-term financial goals.

IndiaFirst Life TULIP Pro Vs. Other Investments

Comparing alternative strategies makes it easier to evaluate whether a financial product truly delivers value.

Using the same assumptions as the previous example, let’s compare the IndiaFirst Life TULIP Pro with a strategy that separates insurance and investment.

IndiaFirst Life TULIP Pro Vs. Pure-term + Equity Mutual Fund

For the insurance component, we assume the purchase of a pure term life insurance policy with a sum assured of ₹15 lakhs, a policy term of 25 years, and a premium payment term of 5 years.

The annual premium works out to ₹25,900, leaving ₹74,100 each year available for investment based on your risk appetite.

|

Pure Term Life Insurance Policy |

|

| Sum Assured |

₹ 15,00,000 |

|

Policy Term |

25 years |

| Premium Paying Term |

5 years |

|

Annualised Premium |

₹ 25,900 |

| Investment |

₹ 74,100 |

Since the IndiaFirst Life TULIP Pro requires premiums for 6 years, while the term insurance premium ends in 5 years, the entire ₹1 lakh is invested in the 6th year under this alternative strategy.

The remaining amount can be invested in an asset class that matches your risk profile.

Conservative investors may prefer debt instruments such as the Public Provident Fund (PPF), while aggressive investors may opt for equity mutual funds.

For this comparison, an equity mutual fund has been considered, as it is also a market-linked investment.

|

Term insurance + Equity Mutual Fund |

|||

|

Age |

Year | Term Insurance premium + Equity Mutual Fund | Death benefit |

| 35 | 1 | -1,00,000 |

15,00,000 |

|

36 |

2 | -1,00,000 | 15,00,000 |

| 37 | 3 | -1,00,000 |

15,00,000 |

|

38 |

4 | -1,00,000 | 15,00,000 |

| 39 | 5 | -1,00,000 |

15,00,000 |

|

40 |

6 | -1,00,000 | 15,00,000 |

| 41 | 7 | 0 |

15,00,000 |

|

42 |

8 | 0 | 15,00,000 |

| 43 | 9 | 0 |

15,00,000 |

|

44 |

10 | 0 | 15,00,000 |

| 45 | 11 | 0 |

15,00,000 |

|

46 |

12 | 0 | 15,00,000 |

| 47 | 13 | 0 |

15,00,000 |

|

48 |

14 | 0 | 15,00,000 |

| 49 | 15 | 0 |

15,00,000 |

|

50 |

16 | 0 | 15,00,000 |

| 51 | 17 | 0 |

15,00,000 |

|

52 |

18 | 0 | 15,00,000 |

| 53 | 19 | 0 |

15,00,000 |

|

54 |

20 | 0 | 15,00,000 |

| 55 | 21 | 0 |

15,00,000 |

|

56 |

22 | 0 | 15,00,000 |

| 57 | 23 | 0 |

15,00,000 |

|

58 |

24 | 0 | 15,00,000 |

| 59 | 25 | 0 |

15,00,000 |

|

60 |

53,68,623 | ||

| IRR |

10.16% |

||

The investment grows to a pre-tax maturity value of ₹60.50 lakhs. After accounting for capital gains tax, the post-tax maturity value is ₹53.68 lakhs, delivering a post-tax IRR of 10.16%.

|

Equity Mutual Fund Tax Calculation |

|

|

Maturity value after 25 years |

60,50,498 |

| Purchase price |

4,70,500 |

|

Long-Term Capital Gains |

55,79,998 |

| Exemption limit |

1,25,000 |

|

Taxable LTCG |

54,54,998 |

| Tax paid on LTCG |

6,81,875 |

|

Maturity value after tax |

53,68,623 |

This comparison clearly highlights the advantage of separating insurance from investment. Not only does this approach generate significantly higher returns, but it also offers greater liquidity and flexibility.

By choosing dedicated products based on your risk appetite and investment horizon, you stand a much better chance of achieving your long-term financial goals.

Final Verdict on IndiaFirst Life TULIP Pro Plan

The IndiaFirst Life TULIP Pro is a Unit-Linked Insurance Plan (ULIP) that combines life insurance with market-linked investments.

Although it offers multiple fund options and investment strategies, many of the funds have similar asset allocations, limiting meaningful diversification.

Moreover, the life insurance cover is relatively low, making it inadequate to meet the long-term financial needs of most families and it also has a high agent commission.

The charges are moderately high compared to other market-linked investment products. Although certain charges are credited back to the fund at a later stage, investors lose the time value of money, as the deducted amounts miss the opportunity to compound throughout the policy term.

While the plan provides exposure to equity markets, its return potential does not justify the level of risk involved. Consequently, the overall risk-return trade-off remains unfavourable.

A more effective approach is to separate insurance from investment.

A pure-term life insurance policy provides adequate financial protection at a much lower cost, allowing the remaining amount to be invested in products that better suit your financial goals, investment horizon, and risk appetite.

This strategy offers the potential for higher returns, greater liquidity, and increased flexibility.

Before investing in any financial product, assess both its return potential and its suitability for your financial objectives.

Do Quora, Facebook, and Twitter have the final say when it comes to financial advice?

Consulting a Certified Financial Planner (CFP) can help you choose the right investment strategy and build a portfolio aligned with your goals, risk tolerance, and time horizon.

Leave a Reply