Can the Kotak SmartLife Plan truly help you build long-term wealth while protecting your family’s future, or is it just another insurance product with limited investment potential?

Does the Kotak SmartLife Plan offer the right balance between life insurance and wealth creation, or are there better alternatives available?

Is the Kotak SmartLife Plan a smart choice for achieving your financial goals, or could its features and charges limit your long-term returns?

Let’s take a closer look at the plan’s features, benefits, and drawbacks to understand whether it aligns with your long-term financial objectives.

Table of Contents:

What is the Kotak SmartLife Plan?

What are the features of the Kotak SmartLife Plan?

Who is eligible for the Kotak SmartLife Plan?

What are the benefits of the Kotak SmartLife Plan?

Grace Period, Discontinuance and Revival of the Kotak SmartLife Plan

Free Look Period for the Kotak SmartLife Plan

Surrendering the Kotak SmartLife Plan

What are the advantages of the Kotak SmartLife Plan?

What are the disadvantages of the Kotak SmartLife Plan?

Research Methodology of Kotak SmartLife Plan

Benefit Illustration – IRR Analysis of Kotak SmartLife Plan

Kotak SmartLife Plan Vs. Other Investments

Kotak SmartLife Plan Vs. Pure-term + PPF/Equity Mutual Fund

Final Verdict on the Kotak SmartLife Plan

What is the Kotak SmartLife Plan?

Kotak SmartLife Plan is a Participating Non-Linked Life Insurance Individual Savings Product.

It will provide you with the option either to receive Cash bonus payouts every year, right from the end of the 1st policy year onwards, to take care of interim financial requirements, or to utilise such Cash bonuses for accumulating and creating a corpus to fulfil bigger goals and plan for a stress-free life.

What are the features of the Kotak SmartLife Plan?

- Provides life insurance protection up to the age of 75 years.

- Offers the flexibility to choose between two bonus options: Cash Payout or Paid-Up Additions.

- Enables you to receive the selected bonus option from the end of the first policy year, either monthly or annually.

- Allows you to enhance your coverage with optional riders by paying an additional premium.

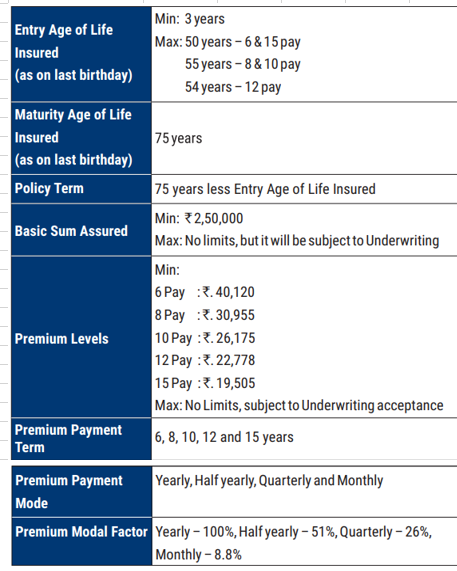

Who is eligible for the Kotak SmartLife Plan?

What are the benefits of the Kotak SmartLife Plan?

1. Death Benefit

If all the due Premiums have been paid, the death benefit shall be:

Cash Bonus Payout option:

- Sum Assured on death PLUS Interim bonus, if any PLUS

- Terminal bonus, if any PLUS

- Present Value of outstanding monthly cash bonus payout for the remaining months of the policy year of the death of the Life Insured, if monthly frequency is opted under Cash Bonus

Paid-Up Addition option:

- Sum Assured on death PLUS

- Accrued Paid-up Additions, if available PLUS

- Interim bonus, if any PLUS

- Terminal bonus, if any

Where Sum Assured on death is higher of:

- 11 times of Annualised Premium (including extra premium, if any) OR

- Basic Sum Assured, which is the guaranteed maturity benefit OR

- 105% of all premiums paid (including extra premium, if any) till the date of death

2. Survival Benefit

The Survival Benefit shall be payable as per the chosen Bonus option, as explained below:

Cash Payout option:

Under this option, at the end of each policy year, starting from the end of the 1st policy year, Cash Bonus, if declared, will get paid out till end of the Kotak SmartLife Plan policy term or death or surrender, whichever is earlier.

You also have the option to choose Cash Payout on a monthly basis, which shall be calculated as : (102.25% * Yearly Cash Bonus Payout) / 12

The first monthly Cash Bonus Payout (if any) under this option shall start from the first policy anniversary date.

Paid-Up Addition option:

Under this option, at the end of each policy year, starting from the end of the 1st policy year – Cash Bonus, if declared, will be utilised to purchase Paid-Up Additions (additional Sum Assured).

The “Cash Bonus” for Basic Sum Assured and Paid-Up Additions will be declared separately, which in turn will be utilised to purchase Paid-Up Additions at the end of the policy year. Paid-Up Additions are additional guaranteed benefits payable on death or maturity.

Paid- Up Addition will be calculated as: [Paid-Up Addition Factor for the attained age X Cash Bonus]

3. Maturity Benefit

On survival till the end of the policy term and all due premiums are paid, the following Maturity Benefit will be payable, and the Kotak SmartLife Plan policy will be terminated.

Under the Cash Bonus Payout option: Basic Sum Assured PLUS Cash Bonus, if any, PLUS Terminal bonus, if any

Under the Paid-Up Addition option: Basic Sum Assured PLUS Cash Bonus, if any, PLUS Accrued Paid-up Addition, if available, PLUS Terminal bonus, if any

Grace Period, Discontinuance and Revival of the Kotak SmartLife Plan

Grace Period

There is a grace period of 30 days from the due date for payment of premium for the yearly, half-yearly and quarterly modes, and 15 days for the monthly mode.

Discontinuance

Lapse: If Premiums are discontinued at any time during the first policy year, the Kotak SmartLife Plan policy shall lapse at the end of the grace period, and no benefits will be payable.

Reduced Paid Up Policy: After the policy acquires Surrender Value, if the subsequent premiums are not paid within the grace period the policy will be converted into a Reduced Paid-Up policy by default.

Revival

A lapsed / Reduced Paid Up policy can be revived within five years from the due date of the first unpaid premium

Free Look Period for the Kotak SmartLife Plan

The Policyholder is offered a 30-day free-look period to review the terms and conditions of the Policy (except for policies having a policy term of less than a year) beginning from the date of receipt of the Policy Document in electronic form.

In case the Policyholder is not agreeable to any terms and conditions of the Policy or otherwise; then subject to no claims having been made hereunder, the Policyholder may choose to return the Policy to the Insurer for cancellation.

Surrendering the Kotak SmartLife Plan

The policy acquires a Guaranteed Surrender Value (GSV) after payment of full premiums for two consecutive policy years.

Special Surrender Value (SSV) is acquired after completion of the first policy year, provided premiums due for at least 1 policy year have been paid in full. On Surrender, the higher of SSV or GSV will be payable.

What are the advantages of the Kotak SmartLife Plan?

- Allows a one-time switch from the Cash Payout option to the Paid-Up Addition option on any policy anniversary during the policy term.

- Offers premium discounts for higher sum assured policies and for female policyholders.

- Provides the option to avail a policy loan of up to 50% of the policy’s surrender value, subject to the policy terms.

What are the disadvantages of the Kotak SmartLife Plan?

- The sum assured may not be adequate to meet the family’s essential financial needs.

- The returns are suboptimal for a long-term investment.

Research Methodology of Kotak SmartLife Plan

Like most traditional endowment plans, the Kotak SmartLife Plan combines life insurance with savings by offering life cover throughout the policy term along with a Survival or maturity benefit.

The Kotak SmartLife Plan policyholder pays premiums for a limited period and receives either regular payouts or a lump sum at maturity.

However, to determine whether the plan is financially worthwhile, it is essential to evaluate its Internal Rate of Return (IRR).

Benefit Illustration – IRR Analysis of Kotak SmartLife Plan

Consider the illustration from the policy brochure.

A 35-year-old male purchases the Kotak SmartLife Plan with a sum assured of ₹10.35 lakhs, a 40-year policy term, and an annual premium of ₹94,140 payable for 10 years.

|

Male |

35 years |

|

Sum Assured |

₹ 10,35,540 |

|

Policy Term |

40 years |

|

Premium Paying Term |

12 years |

|

Annualised Premium |

₹ 94,140 |

The maturity benefit includes vested bonuses, with projections based on assumed investment returns of 4% and 8%.

These are only illustrative assumptions and are neither guaranteed nor indicative of the actual returns.

|

At 4% p.a. |

At 8% p.a. |

||||

|

Age |

Year |

Annualised premium / Maturity benefit |

Death benefit |

Annualised premium / Maturity benefit |

Death benefit |

|

35 |

1 |

-94,140 |

10,35,540 |

-94,140 |

10,35,540 |

|

36 |

2 |

-94,140 |

10,35,540 |

-94,140 |

10,35,540 |

|

37 |

3 |

-94,140 |

10,35,540 |

-94,140 |

10,35,540 |

|

38 |

4 |

-94,140 |

10,35,540 |

-94,140 |

10,35,540 |

|

39 |

5 |

-94,140 |

10,35,540 |

-94,140 |

10,35,540 |

|

40 |

6 |

-94,140 |

10,35,540 |

-94,140 |

10,35,540 |

|

41 |

7 |

-94,140 |

10,35,540 |

-94,140 |

10,35,540 |

|

42 |

8 |

-94,140 |

10,35,540 |

-94,140 |

10,35,540 |

|

43 |

9 |

-94,140 |

10,35,540 |

-94,140 |

10,35,540 |

|

44 |

10 |

-94,140 |

10,35,540 |

-94,140 |

10,35,540 |

|

45 |

11 |

-94,140 |

10,35,540 |

-94,140 |

10,35,540 |

|

46 |

12 |

-94,140 |

10,35,540 |

-94,140 |

10,35,540 |

|

47 |

13 |

0 |

10,35,540 |

0 |

10,35,540 |

|

48 |

14 |

0 |

10,35,540 |

0 |

10,35,540 |

|

49 |

15 |

0 |

10,35,540 |

0 |

10,35,540 |

|

50 |

16 |

0 |

10,35,540 |

0 |

10,35,540 |

|

51 |

17 |

0 |

10,35,540 |

0 |

10,35,540 |

|

52 |

18 |

0 |

10,35,540 |

0 |

10,35,540 |

|

53 |

19 |

0 |

10,35,540 |

0 |

10,35,540 |

|

54 |

20 |

0 |

10,35,540 |

0 |

10,35,540 |

|

55 |

21 |

0 |

10,35,540 |

0 |

10,35,540 |

|

56 |

22 |

0 |

10,35,540 |

0 |

10,35,540 |

|

57 |

23 |

0 |

10,35,540 |

0 |

10,35,540 |

|

58 |

24 |

0 |

10,35,540 |

0 |

10,35,540 |

|

59 |

25 |

0 |

10,35,540 |

0 |

10,35,540 |

|

60 |

26 |

0 |

10,35,540 |

0 |

10,35,540 |

|

61 |

27 |

0 |

10,35,540 |

0 |

10,35,540 |

|

62 |

28 |

0 |

10,35,540 |

0 |

10,35,540 |

|

63 |

29 |

0 |

10,35,540 |

0 |

10,35,540 |

|

64 |

30 |

0 |

10,35,540 |

0 |

10,35,540 |

|

65 |

31 |

0 |

10,35,540 |

0 |

10,35,540 |

|

66 |

32 |

0 |

10,35,540 |

0 |

10,35,540 |

|

67 |

33 |

0 |

10,35,540 |

0 |

10,35,540 |

|

68 |

34 |

0 |

10,35,540 |

0 |

10,35,540 |

|

69 |

35 |

0 |

10,35,540 |

0 |

10,35,540 |

|

70 |

36 |

0 |

10,35,540 |

0 |

10,35,540 |

|

71 |

37 |

0 |

10,35,540 |

0 |

10,35,540 |

|

72 |

38 |

0 |

10,35,540 |

0 |

10,35,540 |

|

73 |

39 |

0 |

10,35,540 |

0 |

10,35,540 |

|

74 |

40 |

0 |

10,35,540 |

0 |

10,35,540 |

|

24,73,177 |

69,18,218 |

||||

|

|

IRR |

2.29% |

5.34% |

||

- At the 4% illustration rate, the projected maturity benefit is ₹24.73 lakhs, translating to an IRR of just 2.29% as per the Kotak SmartLife Plan maturity calculator—lower than the interest earned on many savings accounts.

- At the 8% illustration rate, the projected maturity benefit is ₹69.18 lakhs, resulting in an IRR of 5.34% as per the Kotak SmartLife Plan maturity calculator, which is lower than the returns typically offered by bank fixed deposits.

Even after a 40-year investment horizon, the plan delivers returns that are unlikely to outpace inflation, limiting its ability to create long-term wealth.

At the same time, the life cover remains insufficient to provide adequate financial protection for a family.

Considering the combination of low returns and inadequate insurance coverage, the Kotak SmartLife Plan is unlikely to support long-term financial goals effectively and may weaken an overall financial plan.

Kotak SmartLife Plan Vs. Other Investments

For life insurance, a pure term policy is generally a more efficient choice. It is designed solely to provide financial protection by paying a death benefit to the nominee in the event of the policyholder’s demise.

Since it does not include a savings or investment component, the premiums are significantly lower, allowing you to invest the remaining amount separately to build wealth.

Kotak SmartLife Plan Vs. Pure-term + PPF/Equity Mutual Fund

A pure term policy with a ₹11 lakh sum assured costs approximately ₹16,700 per year, whereas the Kotak SmartLife Plan charges an annual premium of ₹94,140 for a ₹10.35 lakh sum assured.

By investing the annual premium savings according to your risk tolerance, you can potentially accumulate a substantially larger corpus over time.

|

Pure Term Life Insurance Policy |

|

|

Sum Assured |

₹ 11,00,000 |

|

Policy Term |

35 years |

|

Premium Paying Term |

10 years |

|

Annualised Premium |

₹ 16,700 |

|

Investment |

₹ 77,440 |

|

Term Insurance + PPF |

Term insurance + Equity Mutual Fund |

||||

|

Age |

Year |

Term Insurance premium + PPF |

Death benefit |

Term Insurance premium + Equity Mutual Fund |

Death benefit |

|

35 |

1 |

-94,140 |

11,00,000 |

-94,140 |

11,00,000 |

|

36 |

2 |

-94,140 |

11,00,000 |

-94,140 |

11,00,000 |

|

37 |

3 |

-94,140 |

11,00,000 |

-94,140 |

11,00,000 |

|

38 |

4 |

-94,140 |

11,00,000 |

-94,140 |

11,00,000 |

|

39 |

5 |

-94,140 |

11,00,000 |

-94,140 |

11,00,000 |

|

40 |

6 |

-94,140 |

11,00,000 |

-94,140 |

11,00,000 |

|

41 |

7 |

-94,140 |

11,00,000 |

-94,140 |

11,00,000 |

|

42 |

8 |

-94,140 |

11,00,000 |

-94,140 |

11,00,000 |

|

43 |

9 |

-94,140 |

11,00,000 |

-94,140 |

11,00,000 |

|

44 |

10 |

-94,140 |

11,00,000 |

-94,140 |

11,00,000 |

|

45 |

11 |

-94,140 |

11,00,000 |

-94,140 |

11,00,000 |

|

46 |

12 |

-94,140 |

11,00,000 |

-94,140 |

11,00,000 |

|

47 |

13 |

0 |

11,00,000 |

0 |

11,00,000 |

|

48 |

14 |

0 |

11,00,000 |

0 |

11,00,000 |

|

49 |

15 |

0 |

11,00,000 |

0 |

11,00,000 |

|

50 |

16 |

0 |

11,00,000 |

0 |

11,00,000 |

|

51 |

17 |

0 |

11,00,000 |

0 |

11,00,000 |

|

52 |

18 |

0 |

11,00,000 |

0 |

11,00,000 |

|

53 |

19 |

0 |

11,00,000 |

0 |

11,00,000 |

|

54 |

20 |

0 |

11,00,000 |

0 |

11,00,000 |

|

55 |

21 |

0 |

11,00,000 |

0 |

11,00,000 |

|

56 |

22 |

0 |

11,00,000 |

0 |

11,00,000 |

|

57 |

23 |

0 |

11,00,000 |

0 |

11,00,000 |

|

58 |

24 |

0 |

11,00,000 |

0 |

11,00,000 |

|

59 |

25 |

0 |

11,00,000 |

0 |

11,00,000 |

|

60 |

26 |

0 |

11,00,000 |

0 |

11,00,000 |

|

61 |

27 |

0 |

11,00,000 |

0 |

11,00,000 |

|

62 |

28 |

0 |

11,00,000 |

0 |

11,00,000 |

|

63 |

29 |

0 |

11,00,000 |

0 |

11,00,000 |

|

64 |

30 |

0 |

11,00,000 |

0 |

11,00,000 |

|

65 |

31 |

0 |

11,00,000 |

0 |

11,00,000 |

|

66 |

32 |

0 |

11,00,000 |

0 |

11,00,000 |

|

67 |

33 |

0 |

11,00,000 |

0 |

11,00,000 |

|

68 |

34 |

0 |

11,00,000 |

0 |

11,00,000 |

|

69 |

35 |

0 |

11,00,000 |

0 |

11,00,000 |

|

70 |

36 |

0 |

11,00,000 |

0 |

11,00,000 |

|

71 |

37 |

0 |

11,00,000 |

0 |

11,00,000 |

|

72 |

38 |

0 |

11,00,000 |

0 |

11,00,000 |

|

73 |

39 |

0 |

11,00,000 |

0 |

11,00,000 |

|

74 |

40 |

0 |

11,00,000 |

0 |

11,00,000 |

|

1,04,37,092 |

4,47,07,754 |

||||

|

|

IRR |

6.58% |

11.04% |

||

- For conservative investors, the surplus can be invested in a Public Provident Fund (PPF). After accounting for the PPF’s 15-year investment cycle and reinvestment over the policy term, the corpus grows to approximately ₹1.04 crore, delivering an IRR of 6.58%.

- For investors with a higher risk appetite, investing the surplus in an equity mutual fund results in a corpus of around ₹5.09 crore over 40 years. Even after capital gains tax, the post-tax value is approximately ₹4.47 crore, generating an IRR of 11.04%.

|

Equity Mutual Fund Tax Calculation |

|

|

Maturity value after 40 years |

5,09,39,193 |

|

Purchase price |

9,62,680 |

|

Long-Term Capital Gains |

4,99,76,513 |

|

Exemption limit |

1,25,000 |

|

Taxable LTCG |

4,98,51,513 |

|

Tax paid on LTCG |

62,31,439 |

|

Maturity value after tax |

4,47,07,754 |

This comparison highlights that separating insurance and investment can provide both adequate life cover and significantly better long-term wealth creation.

Compared to this approach, the Kotak SmartLife Plan offers lower insurance coverage and relatively modest returns, making it less suitable for investors seeking comprehensive financial protection and long-term wealth accumulation.

Final Verdict on the Kotak SmartLife Plan

The Kotak SmartLife Plan is a traditional endowment policy that offers flexibility in how you receive your benefits.

You may opt for periodic survival income or allow the payouts to accumulate and receive them as a lump sum at maturity. While this flexibility may be appealing, the plan fundamentally remains a low-return endowment policy.

Our analysis indicates that the plan generates modest returns that are unlikely to keep pace with inflation or support long-term wealth creation and it also has a high agent commission.

Moreover, the sum assured is relatively low and may not provide adequate financial protection for your family’s future needs. As a result, the plan falls short on both investment performance and insurance coverage.

A more effective strategy is to separate insurance from investment. Choose a pure term insurance policy to secure adequate life cover at a relatively low cost, and invest the premium savings in a diversified portfolio aligned with your risk tolerance, financial goals, and investment horizon.

This approach offers the potential for stronger long-term wealth creation while ensuring sufficient financial protection.

Rather than relying on traditional insurance-cum-investment products, adopting a goal-based investment strategy can significantly improve your chances of achieving your financial objectives.

Do Quora, Facebook, and Twitter have the final say when it comes to financial advice?

For a personalised financial plan tailored to your income, liabilities, and future goals, consider consulting a Certified Financial Planner.

Leave a Reply