Table of Content:

2) What is Max Life Flexi Wealth Advantage Plan?

3) Variants of Max Life Flexi Wealth Advantage Plan

4) Features of Max Life Flexi Wealth Advantage Plan

- Return of All Charges

- Guaranteed Loyalty Additions to Boost up your fund value

- Auto debit booster

- Option to choose from flexible plan options

- Option of Whole Life Cover and wealth accelerate

- Option to choose your Sum Assured cover Multiple

- Option to avail regular systematic money withdrawal as per your desire: Smart withdrawal

- Unlimited free switches and premium redirection

- Tax Benefits

- Optional Waiver of Premium Cover

5) Benefits of Max Life Wealth Advantage Plan

6) Additional Benefits of Max Life Wealth Advantage Plan

- Max Life Waiver of Premium Benefit

- Smart Withdrawal

- Switch

- Premium Redirection

- Partial Withdrawal

- Increase or decrease in premium payment term

- Increase in Policy Term

- Decrease in Sum Assured

- Settlement Option

- Premium Reduction

- Additional rider benefit

7) Investment Strategies of Max Life Flexi Wealth Advantage Plan

- Self-Managed Portfolio Strategy

- Systematic Transfer Plan

- Lifecycle-Based Portfolio Strategy

- Trigger-Based Portfolio Strategy

- Dynamic Fund Allocation (DFA) Strategy

8) Charges of Max Life Flexi Wealth Advantage Plan

- Premium Allocation Charge

- Policy Administration Charges (for all years)

- Fund Management Charge

- Mortality Charge on Death Benefit

- Mortality Charge on Max Life Waiver of Premium (WOP) benefit

- Surrender/Discontinuance Charge

- Switch Charge

- Premium Redirection Charge

- Partial Withdrawal Charge

- Smart Withdrawal Charge

- Miscellaneous Charge

- Alteration Charge

Max Life Flexi Wealth Advantage Plan Risks and Hidden Costs

9) Research Methodology on Max Life Flexi Wealth Advantage Plan

10) Max Life Flexi Wealth Advantage Plan: Analysis with Illustration

11) Example-1: Max Life Flexi Wealth Advantage Plan (Wealth Variant)

12) Example-2: Max Life Flexi Wealth Advantage Plan (Whole Life Variant)

13) IRR of Max Life Flexi Wealth Advantage Plan: Wealth Variant Option

14) Max Life Flexi Wealth Advantage Plan’s Wealth Variant option vs. PPF + Term Insurance

15) Max Life Flexi Wealth Advantage Plan’s Wealth Variant option vs. ELSS + Term Insurance

16) IRR of Max Life Flexi Wealth Advantage Plan: Whole Life Variant Option

17) Max Life Flexi Wealth Advantage Plan’s Whole Life Variant Option vs. PPF + Term Insurance

18) Max Life Flexi Wealth Advantage Plan’s Whole Life Variant Option vs. ELSS + Term Insurance

19) Advantage of Max Life Flexi Wealth Advantage

20) Lock-in Period and Liquidity in Max Life Flexi Wealth Advantage Plan

21) The disadvantage of Max Life Flexi Wealth Advantage Plan

22) Cancelling Max Life Flexi Wealth Advantage Plan

23) Surrendering the Max Life Flexi Wealth Advantage Plan

24.) Who Should Avoid Axis Max Life Flexi Wealth Advantage Plan?

25) Final Verdict of Max Life Flexi Wealth Advantage Plan

1. Introduction

Your income may differ from your friends.

You may be interested in some other profession.

Everyone will not have the same financial goals!

Because you are not your friends or your relatives.

You are your own person.

That’s what Max Life Flexi Wealth Advantage Plan claims, it can help you throughout your financial journey and can help you to achieve your goals as per your needs.

But, is that true?

Will Max Life Flexi Wealth Advantage Plan can help you to grow your wealth in a long term?

Let’s discover the answer here!

Here in this article, we are going to do in-depth research on Max Life Flexi Wealth Advantage Plan and review the plan completely to discover the answer.

2. What is Max Life Flexi Wealth Advantage Plan?

The Max Life Flexi Wealth Advantage Plan allows you to build a wealth portfolio for yourself and your loved ones while meeting all of your financial goals and milestones.

Max Life Flexi Wealth Advantage Plan is a ULIP plan, meaning it combines life insurance with market-linked investments, making it suitable for long-term wealth creation along with protection.

This Max Life Flexi Wealth Advantage plan accelerates your wealth-creation goals by offering a variety of important features and perks such as Loyalty Additions, Charge Refunds, Auto Debit Boosters, and so on.

Policyholders can use the Max Life Flexi Wealth Advantage Plan calculator to estimate potential returns, explore Wealth Variant and Whole Life Variant options, and simulate different investment fund allocations.

With the Max Life Flexi Wealth Advantage Plan, you can now achieve your investing and wealth-creation objectives by putting your money in a personalized plan that allows you to remain in charge of your financial journey.

Furthermore, the Max Life Flexi Wealth Advantage plan claims that this structure can suit your changing financial demands as you progress through different phases of life.

Before evaluating the Max Life Flexi Wealth Advantage Plan review, investors should first understand what this product actually is.

This is a ULIP plan offered by Axis Max Life Insurance that combines life insurance coverage with market-linked investment options.

3. Variants of Max Life Flexi Wealth Advantage Plan:

The Max Life Flexi Wealth Advantage Plan offers two variants to choose from.

- Wealth Variant-Where you can choose the premium payment as a single pay, limited pay, and regular pay.

- Whole Life Variant-This variant only offer a limited premium payment option.

If the Policyholder and the Life Insured are not the same people, you can choose the Waiver of Premium (WOP) benefit.

At the outset, the Waiver of Premium Benefit will be accessible exclusively for limited and regular pay policies.

The plan also offers flexibility through limited pay options, whole life coverage, and switching between funds, which enhances its appeal as a long-term wealth solution.

You can choose your premium band using the Max Life Flexi Wealth Advantage Plan brochure PDF for guidance.

You can choose your premium band from the below table.

4. Features of Max Life Flexi Wealth Advantage Plan:

i. Return of All Charges:

Max Life Wealth Advantage Plan may refund all of them or some of the charges deducted from the ULIP along with your fund value.

ii. Guaranteed Loyalty Additions to Boost up your fund value:

From the end of the 8th policy term onwards you can avail Guaranteed Loyalty Additions benefit.

iii. Auto debit booster:

You can enjoy the additional benefits at the end of the 5th policy term (exclude the 1st premium) through an auto-debit booster.

iv. Option to choose from flexible plan options:

You can choose two variants and multiple premium payment term and policy term that suits your requirements.

You can also, choose between 5 investment strategies and 11 investment fund options.

v. Option of Whole Life Cover and wealth accelerate:

This whole life variant option begins from the 5th policy term onwards. It allows you to protect your loved ones and helps you to create your wealth till 100 years of age.

vi. Option to choose your Sum Assured Cover Multiple:

You can choose life cover from multiple options of 1.25, 7, 10, and 25 times depending on your premium.

vii. Option to avail regular systematic money withdrawal as per your desire: Smart withdrawal

During your policy term at any time in the Whole Life variant, you can do a regular withdrawal under this smart withdrawal option.

viii. Unlimited free switches and premium redirection:

You can avail unlimited free switches and premium redirection under this benefit.

ix. Tax Benefits:

As per the tax law, you can avail of tax benefits on your premium paid and other benefits you received.

Max Life Flexi Wealth Advantage Plan tax benefits include deductions under Section 80C and tax-free maturity under Section 10(10D), subject to prevailing tax laws.

x. Optional Waiver of Premium Cover:

This option ensures that, in the event of the policyholder’s untimely death, provided the risk cover under the Policy is in force, WOP has been chosen at the time of inception, and WOP cover is active on the date of death of the policyholder, the Company will fund all future outstanding premiums of the base policy only (No additional riders chosen) as and when due under the policy, preserving all the promised benefits under the policy.

5. Benefits of Max Life Wealth Advantage Plan

i. Death Benefit:

Irrespective of whether Waiver of Premium Benefit is opted or not opted at inception:

If the policyholder passes away unfortunately during the policy term, then the nominee will get the highest of the following.

- Sum Assured minus any partial withdrawal if any

- Fund value as on the death of the policyholder

- 105% of the premium paid

If Waiver of Premium (WOP) Benefit is selected at commencement and WOP cover is current on the policyholder’s death date:

All future outstanding premiums of the base insurance shall be funded by the Company as and when due under the policy, and all committed policy benefits shall remain in effect.

ii. Maturity Benefit:

On maturity, the policyholder will receive the Maturity Benefit that has not to exercise the settlement option or equal to the fund value as on the date of maturity.

The fund value will be calculated by using the below option.

Fund Value = Summation of Number of Units in Fund(s) multiplied by the respective NAV of the Fund(s) as on the date of maturity.

iii. Survival Benefit:

1.) Guaranteed Loyalty Additions:

According to the premium band option you choose, you can avail yourself of the Guaranteed Loyalty Additions.

This shall be added to your fund value at the end of the 8th policy term onwards and will continue each year.

2.) Auto Debit Booster:

If you pay any of the first 5 premium payment terms (exclude the 1st premium term) through auto-debit mode, then you can get 0.75% of your premium added to your fund value at the end of the 5th policy term.

Max Life Flexi Wealth Advantage Plan calculator or illustration helps investors understand projected returns, premium commitment, and maturity benefits under different scenarios.

6. Additional Benefits of Max Life Wealth Advantage Plan:

i. Max Life Waiver of Premium Benefit:

You can choose this option only at the beginning of the policy term especially when the policyholder and the life insured are not the same people.

When the policyholder dies, the Company will fund all future outstanding premiums of the base policy as and when they become due under the policy.

All future benefits under the Policy will be paid to the Claimant as and when they become due, just as if the Policyholder was still alive and had paid the Premiums.

ii. Smart Withdrawal:

The policyholder can choose this option to systematically withdraw the money from their fund value.

But this option is only available in the whole variant option.

However, the policyholder can withdraw only if the all-due premiums are paid and the fund value is greater or equal to the minimum death benefit.

The minimum death benefit is 105% of the premiums paid.

iii. Switch:

You can do many switches as you want between the available funds during the policy term.

There is no limit for the switches. The minimum switch amount in Max Life Wealth Advantage Plan is Rs. 5000.

You will not be able to use this option during the first five years of the policy’s discontinuation term. During the settlement period, switches will be permitted.

iv. Premium Redirection:

There is no limit for premium redirection and the policyholder doesn’t have to pay any charges.

But the policyholder needs to notify the insurance company before the premium due regarding the premium amount/the proportion of the premium that needs to pay for each fund during the time of redirection.

v. Partial Withdrawal:

The policyholder cannot access the partial withdrawal during the first five policy terms.

After that, the policyholder will be allowed 12 partial withdrawals per policy term.

The minimum partial withdrawal amount in Max Life Wealth Advantage Plan is Rs. 5000 and the maximum amount is 25% of the fund value as of the date of partial withdrawal.

Partial withdrawal is not allowed during the settlement period.

Max Life Flexi Wealth Advantage Plan allows partial withdrawals after the lock-in period, offering liquidity through features like systematic withdrawal facility (SWF).

vi. Increase or decrease in premium payment term:

This plan is not available in the single premium term option.

The policyholder can access the option only after the first five years of the policy term by notifying the company after paying all the due premiums.

This option is subject to the Premium Payment Term option available in the variant chosen by the policyholder.

vii. Increase in Policy Term:

The policyholder who chooses the single premium term and whole variant option cannot access this benefit.

The policyholder can access this benefit after the lock-in period of 5 years and pay all the due premiums.

This benefit is subject to the premium payment term available under the variant option chosen by the policyholder.

viii. Decrease in Sum Assured:

You can modify the cover multiples at any point throughout the insurance term (provided you have completed one policy term). The modification will take effect on the next policy anniversary.

The premium payable will not change as a result of the change in the cover multiple.

ix. Settlement Option:

If the settlement option is selected, the policy will continue after the maturity date for a period not exceeding 5 years from the maturity date.

The first instalment will be paid out on the Date of Maturity.

You will not be able to make partial or smart withdrawals during the settlement time, but Switches will be permitted.

All inherent investing risks will continue to be faced by the investor. During this period, only fund management charges, switching charges (if any), and mortality charges on death benefits would be deducted.

x. Premium Reduction:

The policyholder can decrease the premium amount up to 50% after the completion of the first five policy years.

This benefit can be accessed only after paying all the due premiums.

xi. Additional rider benefit:

Max Life Flexi Wealth Advantage Plan provides Max Life Critical Illness and Disability Secure Rider (UIN: 104A034V01)

This rider provides a benefit upon diagnosis of any of the critical illnesses covered.

7. Investment Strategies of Max Life Flexi Wealth Advantage Plan:

Max Life Flexi Wealth Advantage Plan provides you with five investment strategies that you can choose from.

- Self-Managed Portfolio Strategy

- Systematic Transfer Plan

- Lifecycle-Based Portfolio Strategy

- Trigger-Based Portfolio Strategy

- Dynamic Fund Allocation (DFA) Strategy

i. Self-Managed Portfolio Strategy:

In this option, the policyholder can choose the allocation of the fund.

In this strategy, you can manage your investments by choosing amongst the following ten (10) investment funds in the proportion of your choice.

ii. Systematic Transfer Plan:

The Systematic Transfer Plan allows the policyholder to duplicate the rupee cost averaging approach on the policy holder’s annualised premium.

First, units will be acquired in Secure Plus, then on each consecutive monthly anniversary, units available in Secure Plus Fund will be progressively moved to Growth Super Fund based on the following formula:

[1 / (13 – month number in the policy year)].”

iii. Lifecycle Based Portfolio Strategy:

Based on the life change, the policyholder can choose the funds to create a balance between equity and debt.

The investments are distributed between Fund 1 and Fund 2 with their proportions varying as per your different life stages.

Fund options for Fund 1:

a) Growth Super Fund

b) Growth Fund

c) Diversified Equity Fund

Fund options for Fund 2:

a) Secure Fund

b) Conservative Fund

c) Secure Plus Fund

iv. Tigger-Based Portfolio Strategy:

This investment strategy can help you to secure your gains”. Primarily the investment strategy distributes the equity and debt ratio of 75%:25% proportion.

At each monthly anniversary of the policy, the portfolio will be rebalanced and funds will be re-allocated depending on a pre-defined trigger event.

Fund options for Fund 1:

a) Growth Super Fund

b) Growth Fund

c) Diversified Equity Fund

Fund options for Fund 2:

a) Secure Fund

b) Conservative Fund

c) Secure Plus Fund

v. Dynamic Fund Allocation (DFA) Strategy:

This strategy can help the policyholder to strike the right balance between debt and equity by rebalancing on yearly basis till the end of the policy maturity.

The funds will be divided between the Growth Super Fund and the Secure Fund in a predetermined proportion that varies according to the number of years before the maturity.

8. Charges of Max Life Flexi Wealth Advantage Plan:

i. Premium Allocation Charge:

This charge will be allocated as % of each premium paid. The charge will be charged differently based on the variants.

For a single premium payment, the charge will be 5%.

For limited pay and Regular pay, the premium allocation charges will be changed as the following table.

ii. Policy Administration Charges (for all years):

The policy administration charge will be deducted as a percentage of an annualized premium paid or a single premium term.

This charge will be deducted between 6 and the 10th policy term. This charge is subject to the cap of Rs. 500.

From the 73rd month onwards the charge will be inflated by 5% per annum.

iii. Fund Management Charge:

The Fund Management Charge will be calculated as a percentage on daily basis from the fund value before adjusting the NAV.

This will be deducted annually as per the following table.

iv. Mortality Charge on Death Benefit:

The fee is calculated per 1000 of the Sum at Risk and is determined by the gender and age of the life covered.

v. Mortality Charge on Max Life Waiver of Premium (WOP) benefit:

On each monthly anniversary, mortality is calculated using the ‘Sum at Risk’ by cancelling units from the unit account.

The fee will be charged when the policyholder reaches the age of life insured and it will be deducted during the base policy’s premium payment period.

It will come to an end after the WOP benefit has been activated.

vi. Surrender/Discontinuance Charge:

For single premium policies, the surrender/discontinuance charge will be deducted as below,

For limited/regular premium policies the charge will be deducted as below,

vii. Switch Charge:

The switching charges are free in this policy.

viii. Premium Redirection Charge:

There is no charge for premium redirection in this policy.

So, the policyholder can access unlimited premium redirection.

ix. Partial Withdrawal Charge:

There are 12 partial withdrawals are allowed per policy term.

The policyholder can access this partial withdrawal free of cost.

x. Smart Withdrawal Charge:

There is no charge for smart withdrawal.

xi. Miscellaneous Charge:

There is no miscellaneous charge in this policy.

xii. Alteration Charge:

There is no charge for any alteration in sum assured, premium payment term, or policy term.

Although the Max Life Insurance Flexi Wealth Advantage Plan promotes a return of charges feature, the refunded charges do not compound over the investment period, which reduces the real value of that benefit.

Max Life Flexi Wealth Advantage Plan Risks and Hidden Costs

While the Max Life Flexi Wealth Advantage Plan provides flexible investment options and life cover, it is important to be aware of the potential risks and hidden costs associated with the plan before investing.

A. Investment-Linked Risk:

Being a Unit Linked Insurance Plan (ULIP), the returns on this plan are market-linked.

This means the fund value can fluctuate based on the performance of the underlying equity or debt funds.

Even with strategies like Lifecycle-Based Portfolio or Dynamic Fund Allocation (DFA), there is no guarantee of positive returns, especially during market downturns.

B. Limited Liquidity During Lock-in Period:

The plan has a mandatory lock-in of 5 years.

During this period, partial withdrawals or smart withdrawals are not allowed, which can be a disadvantage for investors seeking short-term liquidity.

C. Hidden Charges Impacting Fund Value:

While the plan advertises benefits like return of all charges, it is crucial to understand that this refund does not earn additional returns.

Over long durations, the time value of money reduces the effective benefit of these charge reversals.

Other costs, like mortality charges, policy administration charges, and fund management charges, are deducted from the fund and can gradually reduce the overall fund accumulation.

D. Complexity of Investment Strategies:

The availability of five investment strategies and multiple fund options can confuse new investors.

Choosing the wrong allocation or not actively managing the portfolio may lead to lower returns than expected.

E. Settlement Period Risk:

If you opt for a settlement option after maturity, the fund continues to be subject to market risks.

While this allows flexibility in pay-outs, it also means the investor bears the risk of market fluctuations during the settlement period.

F. Cost of Riders and Add-Ons:

Optional add-ons like Waiver of Premium (WOP) or Critical Illness Rider increase the premium cost.

Though they provide additional protection, they can reduce the effective investment corpus over the policy term.

G. Inflation Risk:

Even with best-case scenario returns, the plan may not always outpace inflation, especially if market performance underperforms.

This can reduce the real purchasing power of your maturity corpus over time.

9. Research Methodology on Max Life Flexi Wealth Advantage Plan:

Now, we have seen all the necessary details that we need to know about Max Life Flexi Wealth Advantage Plan.

Compare to other Unit Linked Insurance Plans, Max Life Flexi Wealth Advantage Plan’s charges are limited.

But, we cannot say whether this plan is good or bad only based on the details.

So, let’s see the analysis of the Max Life Flexi Wealth Advantage plan and how it delivers returns before concluding.

This section is especially useful for investors looking for a detailed max life flexi wealth advantage plan review based on real return analysis rather than just features.

10. Max Life Flexi Wealth Advantage Plan: Analysis with Illustration:

11. Example-1: Max Life Flexi Wealth Advantage Plan (Wealth Variant)

Source: Max Life

As you can see in the above illustration now, let’s see the two different scenarios that can explain Max Life Flexi Wealth Advantage Plan’s Wealth Variant Option.

Scenario: 1 Survival Benefit

At the end of the 10th policy term (when the policy matures), Mr. Sharma will get the survival benefit as mentioned below,

Scenario: 2 In the event of unfortunate death

If Mr. Sharma passes away during the 3rd policy term, then his nominee will get the death benefit as calculated in the following table,

12. Example-2: Max Life Flexi Wealth Advantage Plan (Whole Life Variant)

The above illustration is an example of the Max Life Flexi Wealth Advantage Plan.

Scenario-1: Survival Benefit

If Mr. Sharma passed the maturity period and has celebrated his 100th birthday, then he will get the survival benefit as below,

Scenario-2: In the event of an unfortunate death

If Mr. Sharma passes away before completing his policy term, then the death benefit will be calculated as,

Death benefit = Highest sum assured or 105% of the premium paid or the fund value

![]()

13. IRR of Max Life Flexi Wealth Advantage Plan: Wealth Variant Option

Now, let’s see the IRR of Max Life Flexi Wealth Advantage Plan’s Wealth Variant.

Many investors compare these returns using the Max Life Flexi Wealth Advantage Plan calculator to simulate different outcomes.

Let’s see the IRR for both worst-case and best-case scenarios.

Now, let’s take the assumed gross return as 4% in the worst-case scenario.

If we purchase the policy for Rs. 1, 00, 000 for 20 years, then

As you can see in the above illustration, in the worst-case scenario, Max Life Flexi Wealth Advantage Plan’s Wealth Variant option gives us an IRR of 2.75%.

At the end of the policy term, we will get Rs. 26, 90, 510 as maturity benefit and Rs. 7, 00, 000 as the death benefit.

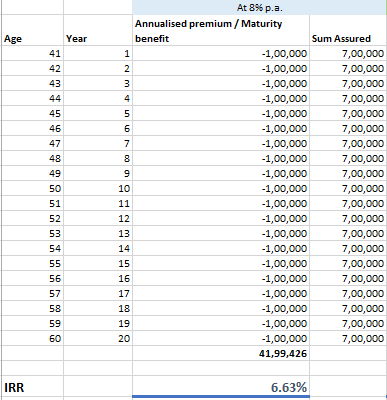

Now, let’s see the best-case scenario of Max Life Flexi Wealth Advantage Plan’s Wealth Variant option.

Here let’s take the assumed gross return as 8%.

As you can see in the above illustration, in the best-case scenario of the Max Life Flexi Wealth Advantage Plan’s Wealth Variant option, we will get an IRR of 6.63%.

At the end of the policy term, we will get Rs. 41, 99, 426 as maturity benefit and Rs. 7, 00, 000 as the death benefit.

|

Investment Options |

IRR (Internal Rate of Return) |

Maturity benefit |

Death benefit |

|

Wealth Variant assumed gross return of 4% |

2.75% |

26,90,510 |

7,00,000 |

|

Wealth Variant assumed gross return of 8% |

6.63% |

41,99,426 |

7,00,000 |

Investors can use Max Life Flexi Wealth Advantage Plan calculator or Max Life Flexi Wealth Advantage Plan NAV today to simulate different fund performance scenarios and optimize investment decisions.

If you think, you will get a reasonable investment return in the Max Life Flexi Wealth Advantage Plan’s Wealth Variant option, then before deciding let’s compare this plan with other investment products.

14. Max Life Flexi Wealth Advantage Plan’s Wealth Variant option vs. PPF + Term Insurance:

Now, let’s take PPF here.

Annual Contribution: Rs. 1, 00, 000

Tenure: 20 years

Term Insurance:

Sum Assured: Rs. 7, 00, 000

Annual Premium: Rs. 5, 500

PPF Contribution: Rs. 94, 500

Interest Rate: 7.10% without taking any risk

|

Term Insurance + PPF |

|||

|

Age |

Year |

Term Insurance premium + PPF |

Death benefit |

|

40 |

1 |

-1,00,000 |

7,00,000 |

|

41 |

2 |

-1,00,000 |

7,00,000 |

|

42 |

3 |

-1,00,000 |

7,00,000 |

|

43 |

4 |

-1,00,000 |

7,00,000 |

|

44 |

5 |

-1,00,000 |

7,00,000 |

|

45 |

6 |

-1,00,000 |

7,00,000 |

|

46 |

7 |

-1,00,000 |

7,00,000 |

|

47 |

8 |

-1,00,000 |

7,00,000 |

|

48 |

9 |

-1,00,000 |

7,00,000 |

|

49 |

10 |

-1,00,000 |

7,00,000 |

|

50 |

11 |

-1,00,000 |

7,00,000 |

|

51 |

12 |

-1,00,000 |

7,00,000 |

|

52 |

13 |

-1,00,000 |

7,00,000 |

|

53 |

14 |

-1,00,000 |

7,00,000 |

|

54 |

15 |

-1,00,000 |

7,00,000 |

|

55 |

16 |

-1,00,000 |

7,00,000 |

|

56 |

17 |

-1,00,000 |

7,00,000 |

|

57 |

18 |

-1,00,000 |

7,00,000 |

|

58 |

19 |

-1,00,000 |

7,00,000 |

|

59 |

20 |

-1,00,000 |

7,00,000 |

|

60 |

41,94,722 |

||

|

IRR |

6.62% |

||

At the end of the 20 years, here we will get an IRR of 6.62%.

We will get Rs. 41,94,772 as investment return without taking any investment risk.

So, compare to Max Life Flexi Wealth Advantage Plan’s Wealth Variant option, PPF gives us a better result.

|

Investment Options |

IRR (Internal Rate of Return) |

Maturity benefit |

Death benefit |

|

Wealth Variant assumed gross return of 4% |

2.75% |

26,90,510 |

7,00,000 |

|

Wealth Variant assumed gross return of 8% |

6.63% |

41,99,426 |

7,00,000 |

|

PPF |

6.62% |

41,94,722 |

7,00,000 |

Now, let’s see what we will get if we invest I n a risk-oriented investment product.

15. Max Life Flexi Wealth Advantage Plan’s Wealth Variant option vs. ELSS + Term Insurance:

Let’s take ELSS for example.

Annual Contribution: Rs. 1, 00, 000

Tenure: 20 years

Term Insurance:

Sum Assured: Rs. 7, 00, 000

Annual Premium: Rs. 5, 500

ELSS Contribution: Rs. 94, 500

Assumed Interest Rate: 12% with risk

|

Term insurance + ELSS |

|||

|

Age |

Year |

Term Insurance premium + ELSS |

Death benefit |

|

40 |

1 |

-1,00,000 |

7,00,000 |

|

41 |

2 |

-1,00,000 |

7,00,000 |

|

42 |

3 |

-1,00,000 |

7,00,000 |

|

43 |

4 |

-1,00,000 |

7,00,000 |

|

44 |

5 |

-1,00,000 |

7,00,000 |

|

45 |

6 |

-1,00,000 |

7,00,000 |

|

46 |

7 |

-1,00,000 |

7,00,000 |

|

47 |

8 |

-1,00,000 |

7,00,000 |

|

48 |

9 |

-1,00,000 |

7,00,000 |

|

49 |

10 |

-1,00,000 |

7,00,000 |

|

50 |

11 |

-1,00,000 |

7,00,000 |

|

51 |

12 |

-1,00,000 |

7,00,000 |

|

52 |

13 |

-1,00,000 |

7,00,000 |

|

53 |

14 |

-1,00,000 |

7,00,000 |

|

54 |

15 |

-1,00,000 |

7,00,000 |

|

55 |

16 |

-1,00,000 |

7,00,000 |

|

56 |

17 |

-1,00,000 |

7,00,000 |

|

57 |

18 |

-1,00,000 |

7,00,000 |

|

58 |

19 |

-1,00,000 |

7,00,000 |

|

59 |

20 |

-1,00,000 |

7,00,000 |

|

60 |

69,24,652 |

||

|

IRR |

10.77% |

||

As you can see in the above illustration, we will get an IRR of 10.77% in ELSS.

After taking the risk at the end of the 20 years, we will get Rs. 69,24,652 as maturity value after deducting the taxes.

|

Investment Options |

IRR (Internal Rate of Return) |

Maturity benefit |

Death benefit |

|

Wealth Variant assumed gross return of 4% |

2.75% |

26,90,510 |

7,00,000 |

|

Wealth Variant assumed gross return of 8% |

6.63% |

41,99,426 |

7,00,000 |

|

ELSS (post-tax) |

10.77% |

69,24,652 |

7,00,000 |

So, compare to Max Life Flexi Wealth Advantage Plan’s Wealth Variant option, ELSS gives us a better result even after taking the risk.

Equity-linked comparisons are often benchmarked against Max Life Ulip Plan returns to assess if ULIPs justify their costs.

16. IRR of Max Life Flexi Wealth Advantage Plan: Whole Life Variant Option

Now, let’s calculate the IRR Max Life Flexi Wealth Advantage Plan’s Whole Life Variant Option in both the best-case scenario and the worst-case scenario by using the return calculator provided by Max Life.

In the worst-case scenario, let’s take the assumed gross return as 4%,

We will get an IRR of 3.23% in the Max Life Flexi Wealth Advantage Plan’s Whole Life Variant Option.

At the end of the policy term, we will get Rs. 2, 02, 42, 191 as maturity benefit.

Now, let’s see the IRR in the best-case scenario of Max Life Flexi Wealth Advantage Plan’s Whole Life Variant Option.

Here, let’s take the assumed gross return as 8%.

As you can see in the above illustration, in the Max Life Flexi Wealth Advantage Plan’s Whole Life Variant Option, we will get an IRR of 7.17% in the best-case scenario and at the end of the policy term, we will get Rs. 14, 30, 74, 775 as maturity benefit.

|

Investment Options |

IRR (Internal Rate of Return) |

Maturity benefit |

Death benefit |

|

Whole life Variant assumed gross return of 4% |

3.23% |

2,02,42,191 |

14,00,000 |

|

Whole life Variant assumed gross return of 8% |

7.17% |

14,30,74,775 |

14,00,000 |

Looking only at the Max Life Flexi Wealth Advantage Plan NAV today can create a misleading impression about performance.

A higher NAV does not automatically indicate better future returns.

Investors should evaluate Max Life flexi wealth plan fund performance over longer periods and compare it with mutual fund alternatives offering similar equity exposure.

Now, let’s see what result we will get if we invest the same in the risk-free investment products.

17. Max Life Flexi Wealth Advantage Plan’s Whole Life Variant Option vs. PPF + Term Insurance:

Annual Contribution: Rs. 2, 00, 000

Investment tenure: 20 years

Term Insurance:

Sum Assured: Rs. 14, 00, 000

Annual Premium: Rs. 11, 000

PPF Contribution: Rs. 1, 50, 000

Since the maximum limit is Rs. 1, 50, 000 in PPF, let’s invest the remaining amount in FD which is Rs. 39, 000

Interest Rate in PPF: 7.10% without Risk

Assumed Interest Rate in FD: 5%

|

Term Insurance + PPF |

|||

|

Age |

Year |

Term Insurance premium + PPF |

Death benefit |

|

40 |

1 |

-2,00,000 |

14,00,000 |

|

41 |

2 |

-2,00,000 |

14,00,000 |

|

42 |

3 |

-2,00,000 |

14,00,000 |

|

43 |

4 |

-2,00,000 |

14,00,000 |

|

44 |

5 |

-2,00,000 |

14,00,000 |

|

45 |

6 |

-2,00,000 |

14,00,000 |

|

46 |

7 |

-2,00,000 |

14,00,000 |

|

47 |

8 |

-2,00,000 |

14,00,000 |

|

48 |

9 |

-2,00,000 |

14,00,000 |

|

49 |

10 |

-2,00,000 |

14,00,000 |

|

50 |

11 |

-2,00,000 |

14,00,000 |

|

51 |

12 |

-2,00,000 |

14,00,000 |

|

52 |

13 |

-2,00,000 |

14,00,000 |

|

53 |

14 |

-2,00,000 |

14,00,000 |

|

54 |

15 |

-2,00,000 |

14,00,000 |

|

55 |

16 |

-2,00,000 |

14,00,000 |

|

56 |

17 |

-2,00,000 |

14,00,000 |

|

57 |

18 |

-2,00,000 |

14,00,000 |

|

58 |

19 |

-2,00,000 |

14,00,000 |

|

59 |

20 |

-2,00,000 |

14,00,000 |

|

60 |

21 |

0 |

14,00,000 |

|

61 |

22 |

0 |

14,00,000 |

|

62 |

23 |

0 |

14,00,000 |

|

63 |

24 |

0 |

14,00,000 |

|

64 |

25 |

0 |

14,00,000 |

|

65 |

26 |

0 |

14,00,000 |

|

66 |

27 |

0 |

14,00,000 |

|

67 |

28 |

0 |

14,00,000 |

|

68 |

29 |

0 |

14,00,000 |

|

69 |

30 |

0 |

14,00,000 |

|

70 |

31 |

0 |

14,00,000 |

|

71 |

32 |

0 |

14,00,000 |

|

72 |

33 |

0 |

14,00,000 |

|

73 |

34 |

0 |

14,00,000 |

|

74 |

35 |

0 |

14,00,000 |

|

75 |

36 |

0 |

14,00,000 |

|

76 |

37 |

0 |

14,00,000 |

|

77 |

38 |

0 |

14,00,000 |

|

78 |

39 |

0 |

14,00,000 |

|

79 |

40 |

0 |

14,00,000 |

|

80 |

41 |

0 |

14,00,000 |

|

81 |

42 |

0 |

14,00,000 |

|

82 |

43 |

0 |

14,00,000 |

|

83 |

44 |

0 |

14,00,000 |

|

84 |

45 |

0 |

14,00,000 |

|

85 |

46 |

0 |

14,00,000 |

|

86 |

47 |

0 |

14,00,000 |

|

87 |

48 |

0 |

14,00,000 |

|

88 |

49 |

0 |

14,00,000 |

|

89 |

50 |

0 |

14,00,000 |

|

90 |

51 |

0 |

14,00,000 |

|

91 |

52 |

0 |

14,00,000 |

|

92 |

53 |

0 |

14,00,000 |

|

93 |

54 |

0 |

14,00,000 |

|

94 |

55 |

0 |

14,00,000 |

|

95 |

56 |

0 |

14,00,000 |

|

96 |

57 |

0 |

14,00,000 |

|

97 |

58 |

0 |

14,00,000 |

|

98 |

59 |

0 |

14,00,000 |

|

99 |

60 |

0 |

14,00,000 |

|

100 |

17,73,16,914 |

14,00,000 |

|

|

IRR |

7.61% |

||

As you can see in the above illustration, we will get an IRR of 7.61%.

After 20 years, we will get Rs. 66,58, 288 as Maturity value in PPF and Rs. 13,54,050 in FD.

Since we purchase the plan for 60 years, now, we have the remaining 40 years with us.

In PPF, the maturity period is 20 years. So, since we cannot continue our contribution to PPF, we can move this investment to an RBI bond.

The interest rate of RBI bonds is 7.15%.

So, after 40 years, we will have Rs. 17,73,16,914 as maturity values.

|

Investment Options |

IRR (Internal Rate of Return) |

Maturity benefit |

Death benefit |

|

Whole life Variant assumed gross return of 4% |

3.23% |

2,02,42,191 |

14,00,000 |

|

Whole life Variant assumed gross return of 8% |

7.17% |

14,30,74,775 |

14,00,000 |

|

PPF |

7.61% |

17,73,16,914 |

14,00,000 |

|

PPF (1.5 Lakh for 20 years) |

66,58,288 |

||

|

Bank FD (39,000 for 20 years) |

₹13,54,050. |

||

|

RBI floating rate bond (Proceeds of PPF & FD for 40 years) |

₹17,73,16,913.94 |

So, compare to Max Life Flexi Wealth Advantage Plan’s Whole Life Variant Option we get a better result in PPF without taking any risk.

Now, let’s see what we will get if we invest in risk-oriented investment products.

18. Max Life Flexi Wealth Advantage Plan’s Whole Life Variant Option vs. ELSS + Term Insurance:

Annual Contribution: Rs. 2, 00, 000

Investment tenure: 20 years

Term Insurance:

Sum Assured: Rs. 14, 00, 000

Annual Premium: Rs. 11, 000

ELSS Contribution: Rs. 1, 89, 000

Assumed interest rate: 12% after taking the risk

|

Term insurance + ELSS |

|||

|

Age |

Year |

Term Insurance premium + ELSS |

Death benefit |

|

40 |

1 |

-2,00,000 |

14,00,000 |

|

41 |

2 |

-2,00,000 |

14,00,000 |

|

42 |

3 |

-2,00,000 |

14,00,000 |

|

43 |

4 |

-2,00,000 |

14,00,000 |

|

44 |

5 |

-2,00,000 |

14,00,000 |

|

45 |

6 |

-2,00,000 |

14,00,000 |

|

46 |

7 |

-2,00,000 |

14,00,000 |

|

47 |

8 |

-2,00,000 |

14,00,000 |

|

48 |

9 |

-2,00,000 |

14,00,000 |

|

49 |

10 |

-2,00,000 |

14,00,000 |

|

50 |

11 |

-2,00,000 |

14,00,000 |

|

51 |

12 |

-2,00,000 |

14,00,000 |

|

52 |

13 |

-2,00,000 |

14,00,000 |

|

53 |

14 |

-2,00,000 |

14,00,000 |

|

54 |

15 |

-2,00,000 |

14,00,000 |

|

55 |

16 |

-2,00,000 |

14,00,000 |

|

56 |

17 |

-2,00,000 |

14,00,000 |

|

57 |

18 |

-2,00,000 |

14,00,000 |

|

58 |

19 |

-2,00,000 |

14,00,000 |

|

59 |

20 |

-2,00,000 |

14,00,000 |

|

60 |

21 |

0 |

14,00,000 |

|

61 |

22 |

0 |

14,00,000 |

|

62 |

23 |

0 |

14,00,000 |

|

63 |

24 |

0 |

14,00,000 |

|

64 |

25 |

0 |

14,00,000 |

|

65 |

26 |

0 |

14,00,000 |

|

66 |

27 |

0 |

14,00,000 |

|

67 |

28 |

0 |

14,00,000 |

|

68 |

29 |

0 |

14,00,000 |

|

69 |

30 |

0 |

14,00,000 |

|

70 |

31 |

0 |

14,00,000 |

|

71 |

32 |

0 |

14,00,000 |

|

72 |

33 |

0 |

14,00,000 |

|

73 |

34 |

0 |

14,00,000 |

|

74 |

35 |

0 |

14,00,000 |

|

75 |

36 |

0 |

14,00,000 |

|

76 |

37 |

0 |

14,00,000 |

|

77 |

38 |

0 |

14,00,000 |

|

78 |

39 |

0 |

14,00,000 |

|

79 |

40 |

0 |

14,00,000 |

|

80 |

41 |

0 |

14,00,000 |

|

81 |

42 |

0 |

14,00,000 |

|

82 |

43 |

0 |

14,00,000 |

|

83 |

44 |

0 |

14,00,000 |

|

84 |

45 |

0 |

14,00,000 |

|

85 |

46 |

0 |

14,00,000 |

|

86 |

47 |

0 |

14,00,000 |

|

87 |

48 |

0 |

14,00,000 |

|

88 |

49 |

0 |

14,00,000 |

|

89 |

50 |

0 |

14,00,000 |

|

90 |

51 |

0 |

14,00,000 |

|

91 |

52 |

0 |

14,00,000 |

|

92 |

53 |

0 |

14,00,000 |

|

93 |

54 |

0 |

14,00,000 |

|

94 |

55 |

0 |

14,00,000 |

|

95 |

56 |

0 |

14,00,000 |

|

96 |

57 |

0 |

14,00,000 |

|

97 |

58 |

0 |

14,00,000 |

|

98 |

59 |

0 |

14,00,000 |

|

99 |

60 |

0 |

14,00,000 |

|

100 |

60,04,73,327 |

14,00,000 |

|

|

IRR |

10.11% |

||

As you can see in the above illustration, we will get an IRR of 10.11% in ELSS.

At the end of the 20 years, in the ELSS fund we will get Rs. 1,38,33,678 as investment return.

To balance the risk allocation, from the 21st year onwards we can move 70% of the corpus to RBI bonds and we can keep the remaining 30% in the ELSS or diversified equity funds.

If we allocate the 70:30 ratios without any additional contribution, then after 40 years, we will get Rs. 60,04,73,327 as investment value.

|

Investment Options |

IRR (Internal Rate of Return) |

Maturity benefit |

Death benefit |

|

Whole life Variant assumed gross return of 4% |

3.23% |

2,02,42,191 |

14,00,000 |

|

Whole life Variant assumed gross return of 8% |

7.17% |

14,30,74,775 |

14,00,000 |

|

ELSS (post-tax) |

10.11% |

60,04,73,327 |

14,00,000 |

|

ELSS (1.89 Lakh for 20 years) |

1,38,33,678.39 |

||

|

70% in RBI floating rate bond (for 40 years) |

₹38,61,71,159.67 |

||

|

30% in Equity funds (for 40 years) |

₹21,43,02,167.49 |

So, here compare to Max Life Flexi Wealth Advantage Plan’s Whole Life Variant Option, ELSS gives us better risk premium returns.

ELSS investment return can also help us to beat inflation.

Aggressive investors usually contrast this with equity exposure and Max Life High Growth fund performance to evaluate long-term potential.

19. Advantage of Max Life Flexi Wealth Advantage:

- Can get a return of all charges during maturity.

- Guaranteed Loyalty Additions and Auto Debit Boosters can help you to Increase the Value of Your Fund.

- Flexible Plan Variants (Wealth/Whole Life) with Multiple Premium Payment Term and Policy Term Options.

- Optional Premium Benefit Waiver.

- Option to choose between 5 investment strategies and 11 funds.

- Flexibility in Smart Withdrawal option.

- Free Switches and Premium Redirections are available.

- A settlement option can be availed during maturity.

20. Lock-in Period and Liquidity in Max Life Flexi Wealth Advantage Plan

The Max Life Flexi Wealth Advantage Plan comes with a 5-year lock-in period, as it is a ULIP.

During this time, you cannot freely withdraw your funds.

If you discontinue early, the amount is moved to a discontinued fund and paid only after the lock-in ends.

Even after 5 years, liquidity is limited.

Partial withdrawals are allowed but come with conditions like minimum balance requirements and restrictions that may affect your long-term returns.

Compared to options like mutual funds or ELSS, this plan offers lower flexibility and access to money.

So, it suits investors who can stay invested long-term without needing frequent liquidity—but may not be ideal if flexibility is a priority.

21. The disadvantage of Max Life Flexi Wealth Advantage Plan:

- No liquidity in the first 5 years of the policy.

- The loan option is not available.

- During the settlement period, the investor should bear the investment risk.

- Though all the charges are paid back during maturity. It is given back without any returns. After 10 or 20 years, because of the time value of money erosion, this payback of charges is really not an advantage. It is just a sales gimmick to make a false claim like charges are reversed and hence no charges.

Now, let’s see what you should do if you want to surrender or cancel the Max Life Flexi Wealth Advantage Plan.

22. Cancelling Max Life Flexi Wealth Advantage Plan:

You have the option to cancel your Max Life Flexi Wealth Advantage Plan during the free look period.

The free look period is 15 days from the date of policy purchased and it will be 30 days if you purchase the plan in electronic mode.

During this time, if you are not satisfied with the terms and conditions of the policy, then you can return the policy by stating your reason.

However, you will be refunded the premium only after deducting some expenses or charges.

Reviewing the official Max Life Flexi Wealth Advantage Plan brochure helps investors understand policy limitations before making a long-term commitment.

23. Surrendering the Max Life Flexi Wealth Advantage Plan:

You have the option to surrender the policy at any time by contacting the company.

The surrender benefit equals the Fund Value less any applicable Surrender / Discontinuance costs.

The policy can be Surrendered / Discontinued at any moment, however, the Surrendered / Discontinued value will be paid subject to policy provisions.

Detailed terms can be verified in the Max Life Flexi Wealth Advantage Plan brochure pdf or policy document.

For more details, you can read the Max Life Flexi Wealth Advantage Plan Brochure here.

24. Who Should Avoid Axis Max Life Flexi Wealth Advantage Plan?

This plan may not be suitable for investors who:

- Need liquidity in the first 5 years

- Want pure insurance at low cost

- Prefer transparent investment products

- Want higher long-term equity returns

- Do not fully understand ULIPs

For such investors, term insurance + mutual funds may be a simpler alternative.

25. Final Verdict of Max Life Flexi Wealth Advantage Plan:

Compare to other ULIPs, Max Life Flexi Wealth Advantage Plan did not give us a better return. Even the return cannot help us to beat the inflation in the long term.

It seems the Max Life Flexi Wealth Advantage Plan is providing flexible investment options but compared to other investments, it does not give the flexibility of liquidity during the lock-in period.

Even when evaluating the Axis Max Life Flexi Wealth Advantage Whole Life Limited Pay option, investors should assess whether combining insurance and investments in a single product aligns with their financial goals.

If we take it as an insurance plan, compare to other term insurance, this Max Life Flexi Wealth Advantage plan is very expensive and on the investment side, even after taking a risk, it does not give a better result in the long term.

Overall, while marketed aggressively as a Max Life Ulip Plan, the return profile suggests investors should carefully compare alternatives before investing.

So, simply Max Life Flexi Wealth Advantage Plan is not worth the money you spend in the long term.

Compared to ELSS + Term Insurance or PPF + Term Insurance, Max Life Flexi Wealth Advantage Plan may underperform in long-term IRR.

If you have any comments or questions, write them in the comment box below.

Or are you interested in creating a Comprehensive Financial Plan for your financial goals?

Skip the queue by registering for your 30 Minute FREE Financial Plan Consultation. Click the ‘Register Now!’ button below.

Leave a Reply