Will investing in the Max Life Smart Wealth Annuity Guaranteed (SWAG) Pension plan be the best strategy to combat inflation?

Does Max Life Smart Wealth Annuity Guaranteed (SWAG) Pension Plan help you take care of all your post-retirement needs?

We strive diligently to meet our financial requirements and attain personal aspirations. However, a crucial aspect of life should be prioritized which is proper retirement planning. To enjoy a stress-free retirement, it becomes imperative to have a regular stream of income.

Whether buying Max Life Smart Wealth Annuity Guaranteed (SWAG) Pension Plan is a good decision to lead a peaceful retirement Life?

This article analyses the Max Life Smart Wealth Annuity Guaranteed (SWAG) Advantages (Pros) and Disadvantages (Cons) to help you understand the plan better.

By reviewing the Benefit Illustration of this policy you will be able to gain some critical insights which will help you make those informed investment decisions.

Let’s get started.

Table of Contents

1.)What is the Max Life SWAG Pension Plan?

2.)What are the Features of the Max Life SWAG Pension Plan?

3.)Who is Eligible to invest in the Max Life SWAG Pension Plan?

4.)Max Life SWAG Pension Plan Annuity plans in detail

5.)Max Life SWAG Pension Plan Grace period, Discontinuance, Reduced Paid-up, and Revival

6.)Max Life SWAG Pension Plan Free Look period

7.)Surrendering Max Life SWAG Plan

8.)Advantages of Max Life SWAG Pension Plan

9.)Disadvantages of Max Life SWAG Pension Plan

10.)Max Life SWAG Pension Plan Research Methodology

- Max Life SWAG Pension Plan Benefit Illustration – IRR Analysis

- Max Life SWAG Pension Plan VS Other Investments

11.)Inflation- adjusted regular income

12.)Final Verdict on Max Life SWAG Pension Plan

1.)What is the Max Life SWAG Pension Plan?

Max Life SWAG Pension Plan is a Non-Linked Non-Participating Individual/ Group General Annuity Savings Plan.

The brochure propagates that it is a one-stop Solution to all your retirement needs that ensures peace of mind in your golden years with a secure and regular stream of income for your entire lifetime.

2.)What are the Features of the Max Life SWAG Pension Plan?

- Enjoy guaranteed lifelong income

- Wide range of annuity variants to suit your retirement needs

- Option to choose premium payments either single premium or limited premium

- Plan your retirement early with the deferred annuity variants and choose when you want to start receiving a guaranteed income stream.

- Get back the part or the entire premium amount upon death or upon reaching a significant age milestone, as chosen at inception

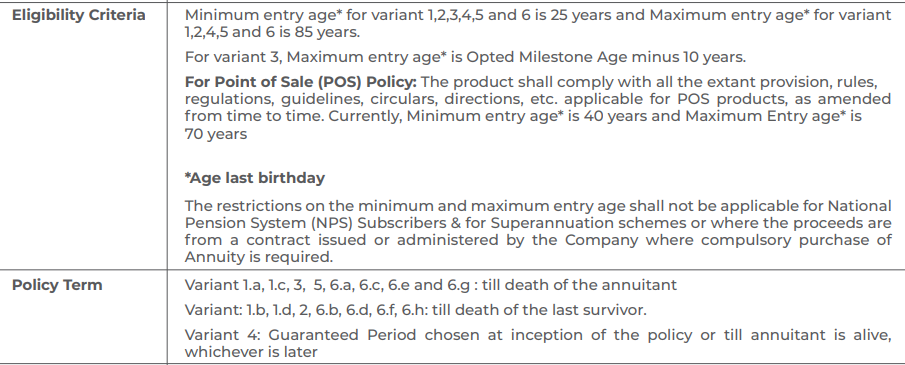

3.)Who is eligible to invest in the Max Life SWAG Pension Plan?

4.)Max Life SWAG Pension Plan Annuity plans in detail

The following table consolidates the various annuity plans available under the Max Life SWAG Pension plan.

Based on your premium payment, deferment period, and return of premium – the annuity amount varies. One has to be cautious while choosing the variant.

| Variant | Sub-variant | Annuity | Return of premium | |

| Immediate Annuity | Single Life without Death Benefit | Lifetime | No | |

| Joint Life without Death Benefit | Till the death of the last survivor | No | ||

| Single Life with Death Benefit | Lifetime | Certain percentage | ||

| Joint Life with Death Benefit | Till the death of the last survivor | Certain percentage on the first death and the balance on the last death | ||

| Immediate Annuity with a chosen proportion of Annuity to Last Survivor | Joint Life without Death Benefit | 100% till first death The revised percentage for the second survivor |

No | |

| Joint Life with Death Benefit | 100% of the Total premium | |||

| Immediate Annuity with Early Return of Premium | Single Life with Death Benefit | In Lifetime a Certain percentage of early return of premium |

Balance percentage of premium | |

| Immediate Annuity for Guaranteed Period and Life thereafter | Single Life without Death Benefit | Till the end of the guaranteed period or death whichever is earlier | No | |

| Increasing Immediate Annuity | Single Life Increasing Annuity Each Year with Death Benefit | Increase (1-6%) every year | 100% of the Total Premium | |

| Single Life Increasing Annuity Every 3 Years with Death Benefit | 15% (simple increase) every 3 years | 100% of the Total Premium | ||

| Deferred Annuity | Single Life with Death Benefit till Deferment Period – Single Premium | Start after the deferment period till the lifetime | Only during deferment period – Death benefit – 105% of Total Premium | |

| Joint Life with Death Benefit till Deferment Period – Single Premium | Start after the deferment period till the last survivor | |||

| Single Life with Death Benefit for Life – Single Premium | Start after the deferment period till the lifetime | 105% of Total Premium | ||

| Joint Life with Death Benefit for Life – Single Premium | Start after the deferment period till the last survivor | |||

| Single Life with Death Benefit till Deferment Period – Limited Premium | Start after the deferment period till the lifetime | Only during deferment period – Death benefit – 105% of Total Premium | ||

| Joint Life with Death Benefit till Deferment Period – Limited Premium | Start after the deferment period till the last survivor | |||

| Single Life with Death Benefit for Life – Limited Premium | Start after the deferment period till the lifetime | 105% of Total Premium | ||

| Joint Life with Death Benefit for Life – Limited Premium | Start after the deferment period till the last survivor | |||

5.)Max Life SWAG Pension Plan Grace period, Discontinuance, Reduced Paid-up and Revival

(Applicable only for limited premium variants)

Grace Period

If the installment premium is not received by the due date, a grace period of 15 days will be given for the payment of the due installment premium for the monthly premium payment mode.

30 days will be given for payment of the due installment premium for quarterly, semi-annually, and annual premium payment modes.

Discontinuance

In the premium discontinuance scenario, if the premium for the first two policy years is unpaid, then the policy will terminate without any future benefits.

Reduced Paid-up

The policy will automatically become reduced paid-up, if it gains surrender value (after paying at least two full years’ worth of premiums) and if no more premiums are paid by the Grace Period’s expiration.

Revival

A Lapsed policy or a policy under Reduced Paid Up (RPU) Mode can be revived for full benefits within five years from the due date of the first unpaid Premium.

6.)Max Life SWAG Pension Plan Free Look Period

If the policyholder disagrees with any of those terms and conditions, then he/she has the option to return the policy, within a period of 15 days (30 days starting from the date of receipt for policies purchased through online platforms namely electronic policies).

For further clarification regarding terms and conditions, you can refer to the Max Life SWAG Pension Plan Policy Brochure

7.)Surrendering Max Life SWAG Plan

The Surrender value is applicable for the immediate annuity with death benefit variants, deferred annuity with death benefit variants, and during the deferment period under deferred annuity with death benefit till deferment period variants.

No Surrender value is available for without death benefit variants of Immediate Annuity variants. For single premium policies, the policy can be surrendered anytime, and for limited premium policies, after payment of 2 full years’ premium, the policy can be surrendered.

8.)Advantages of Max Life SWAG Pension Plan

- Wide range of annuity plans to choose from.

- Advanced annuity option is available under select variants.

- Premium payment, deferment period, and annuity frequency can be chosen as per convenience.

- Ensure consistent payments at regular intervals, for a minimum defined period, irrespective of the survival of the annuitant

- Stay ahead of inflation and boost your annual income with increasing annuity variants

- Ease the financial burden on your loved ones by enhancing your regular income to 110% after your demise

9.)Disadvantages of Max Life SWAG Pension Plan

- An annuity is fully taxable.

- The plan can be surrendered only under select variants.

- Some of the options like Step-up annuity, and return of premium are available under select variants.

10.)Max Life SWAG Pension Plan Research Methodology

Annuity plans are one of the most preferred investment options for retirees. Regular and steady income is the most attractive feature of annuity plans.

Other than the cash flow pattern, the investment plan should be analysed in terms of returns and liquidity. Now, let us estimate the returns for the Max Life SWAG pension plan using the benefit illustration given in the policy brochure.

Max Life SWAG Pension Plan Benefit Illustration – IRR Analysis

A 60-year-old female buys Max Life SWAG – Immediate Annuity – Single life with Death benefit. She invests a single premium of rupees 1 crore and opts the for the return of 50% of the Total Premium upon on her demise.

This will provide her with a steady income of Rs.7,70,400 as long as she lives. Upon her death at age 80, the lumpsum death benefit of Rs.50 Lacs is paid to her nominee and the policy terminates.

| Female | 60 years |

| Single Premium | ₹ 1 Crore |

| Annuity | ₹ 7,70,400 |

| Pension plan | Immediate Annuity – Single Life with Death benefit |

| Age | Year | Single Premium / Annuity |

| 60 | 1 | -1,00,00,000 |

| 61 | 2 | 7,70,400 |

| 62 | 3 | 7,70,400 |

| 63 | 4 | 7,70,400 |

| 64 | 5 | 7,70,400 |

| 65 | 6 | 7,70,400 |

| 66 | 7 | 7,70,400 |

| 67 | 8 | 7,70,400 |

| 68 | 9 | 7,70,400 |

| 69 | 10 | 7,70,400 |

| 70 | 11 | 7,70,400 |

| 71 | 12 | 7,70,400 |

| 72 | 13 | 7,70,400 |

| 73 | 14 | 7,70,400 |

| 74 | 15 | 7,70,400 |

| 75 | 16 | 7,70,400 |

| 76 | 17 | 7,70,400 |

| 77 | 18 | 7,70,400 |

| 78 | 19 | 7,70,400 |

| 79 | 20 | 7,70,400 |

| 80 | 21 | 7,70,400 |

| 50,00,000 | ||

| IRR | 6.31% |

The IRR for this cash flow is 6.31%. Steady income with lower returns is not idle for a retiree. Because inflation eats away the purchasing power of annuity down the lane.

Even if you invest the corpus in bank FD, you earn better returns and you can enjoy liquidity. Here in Max Life SWAG, your corpus is tied up and you can’t redeem your corpus anytime (surrender is available only under select variants with restrictions).

Max Life SWAG Pension Plan VS Other Investments

There are various investment avenues available to secure a consistent income stream, particularly catering to the needs of senior citizens, which offer relatively higher interest rates.

| Alternate Investment option | Interest Rate |

| Senior Citizen Savings Schemes (SCSS) | 8.20% |

| Bank FD | 7% – 8% |

| RBI Floating Rate Bonds | 8.05% (Floating) |

These include the Senior Citizen Savings Scheme (SCSS) with an interest rate of 8.20%, Bank Fixed Deposits (FDs) ranging from 7% to 8%, and RBI Floating Rate Bonds at 8.05% (with a floating interest rate). SCSS and bank FDs assure fixed returns over the term, while the interest rate on RBI floating bonds may fluctuate.

However, these options overlook a crucial aspect: inflation. To ensure a regular income that keeps pace with inflation, it’s imperative to incorporate equity into the investment portfolio. By periodically rebalancing the portfolio every five or six years, one can potentially achieve returns adjusted for inflation.

11.)Inflation-adjusted regular income

Let us assume that 60% of 1 Crore is invested in Equity for wealth creation and the balance 40% in Debt for regular income needs. Equity return is assumed as 12% and debt return as 6%. Every 5 years debt portion is replenished from equity.

Also, every 5 years, your annual withdrawal increases by 6% to combat inflation. The first-year annuity amount is assumed similar to Max Life SWAG Pension Plan i.e., 7,70,400.

| Age | Equity Portion | Shift from Equity to Debt | Debt Portion | ||||

| Opening Balance | Yearly withdrawal | Closing Balance | Opening Balance | Yearly withdrawal | Closing Balance | ||

| 61 | 60,00,000 | – | 67,20,000 | – | 40,00,000 | 7,70,400 | 34,23,376 |

| 62 | 67,20,000 | – | 75,26,400 | – | 34,23,376 | 7,70,400 | 28,12,155 |

| 63 | 75,26,400 | – | 84,29,568 | – | 28,12,155 | 7,70,400 | 21,64,260 |

| 64 | 84,29,568 | – | 94,41,116 | – | 21,64,260 | 7,70,400 | 14,77,491 |

| 65 | 94,41,116 | – | 1,05,74,050 | – | 14,77,491 | 7,70,400 | 7,49,517 |

| 66 | 1,05,74,050 | 50,00,000 | 62,42,936 | 50,00,000 | 57,49,517 | 8,16,624 | 52,28,866 |

| 67 | 62,42,936 | – | 69,92,088 | – | 52,28,866 | 8,16,624 | 46,76,977 |

| 68 | 69,92,088 | – | 78,31,139 | – | 46,76,977 | 8,16,624 | 40,91,974 |

| 69 | 78,31,139 | – | 87,70,876 | – | 40,91,974 | 8,16,624 | 34,71,871 |

| 70 | 87,70,876 | – | 98,23,381 | – | 34,71,871 | 8,16,624 | 28,14,562 |

| 71 | 98,23,381 | 98,23,381 | -0 | 98,23,381 | 1,26,37,943 | 8,65,621 | 1,24,78,661 |

| 72 | -0 | – | -0 | – | 1,24,78,661 | 8,65,621 | 1,23,09,822 |

| 73 | -0 | – | -0 | – | 1,23,09,822 | 8,65,621 | 1,21,30,852 |

| 74 | -0 | – | -0 | – | 1,21,30,852 | 8,65,621 | 1,19,41,145 |

| 75 | -0 | – | -0 | – | 1,19,41,145 | 8,65,621 | 1,17,40,055 |

| 76 | -0 | – | -0 | – | 1,17,40,055 | 9,17,559 | 1,14,71,846 |

| 77 | -0 | – | -0 | – | 1,14,71,846 | 9,17,559 | 1,11,87,544 |

| 78 | -0 | – | -0 | – | 1,11,87,544 | 9,17,559 | 1,08,86,185 |

| 79 | -0 | – | -0 | – | 1,08,86,185 | 9,17,559 | 1,05,66,743 |

| 80 | 1,05,66,743 | 9,17,559 | 1,02,28,136 | ||||

| 81 | 1,02,28,136 | 9,17,559 | 98,69,212 | ||||

Here, the equity portion is completely transferred to debt at the age of 71. You can decide this based on your willingness to take risks. Even if we shift the entire corpus to debt, the corpus outlives you.

In the Max Life SWAG Pension plan, you get a 50% return on premium on death which is 50 lakhs. In this alternate investment strategy, at the age of 81, you are left with a corpus of 1 crore which is double that of the earlier scenario.

On the whole, in this alternate strategy, you get inflation-adjusted income and you can enjoy full liquidity in your investment. Both these aspects are missing in the Max Life SWAG Pension Plan.

i) Max Life SWAG Pension Plan VS Max Life Perfect Partner Super Plan

Will Max Life’s perfect partner Super Plan help you protect loved ones? To answer let’s start by understanding its key aspects.

- Premium Paying Term can be chosen according to your convenience- 7,10,15,20 years.

- Life Cover up to 75 years of age and maturity benefits at the end of 75 years.

- Bonus Options can be chosen at your convenience.

If you wish to know more about the Benefits, and advantages of this policy. We would recommend you to read our article on

Max Life Perfect Partner Super Plan Review – Should You Invest?

ii) Max Life SWAG Pension Plan VS Max Life Online Savings Plan

As the name suggests, will Max Life Online Savings Plan help you maximise your savings to accomplish your investment goals. Let’s start by analysing the basic features of this plan.

- It offers two variants.

- You have 11 Fund Options to choose from.

- Flexibility to choose between funds n number of times.

To get better insights on the plan’s suitability and IRR Analysis. We suggest you to read our blog post on :

Max Life Online Savings Plan Review: Should You Invest?

12.)Final Verdict on Max Life SWAG Pension Plan

Max Life SWAG Pension Plan offers a wide range of plan options covering immediate annuity, deferred annuity, with and without return of premium, Single and Joint Life.

Though there is plenty of options, the regular steady stream of income is the common feature. Only the amount of annuity differs based on the permutation and combination of other options chosen.

The steady source of income from the Max Life SWAG Pension plan can’t be considered a primary source of income, as your expenses will keep on increasing due to inflation.

Investing in Max Life SWAG Pension Plan can’t be a one-stop solution to park your retirement corpus. The High-Agent Commission is also another drawback you need to consider before purchasing the policy.

There are plenty of investment vehicles with better returns. These investment vehicles also offer a steady income. You should consider equity asset class to maintain your standard of living.

As discussed in the alternate investment strategy, you can split your retirement and invest in equity and debt. In this strategy, you get a regular stream of income, inflation-adjusted income and the corpus outlives you.

In general, Annuity plans are short-sighted. But Retirement planning requires a long-term approach.

Referring to Social Media Sites such as Quota, Facebook, Twitter, etc won’t help you choose the right investment product to fulfill all your post-retirement needs. So if you wish to have personalised retirement planning, consult a financial advisor.

Leave a Reply