Every financial year, one important decision quietly impacts your take-home income:

Should you choose the old tax regime or the new tax regime?

At first glance, the choice may seem simple—one offers deductions, the other offers lower tax rates.

But is it really that straightforward?

The answer depends not just on your income, but on your financial habits, investments, and long-term goals.

Choosing the wrong regime could mean paying more tax than necessary—or worse, making financial decisions purely to save tax.

Table of Contents

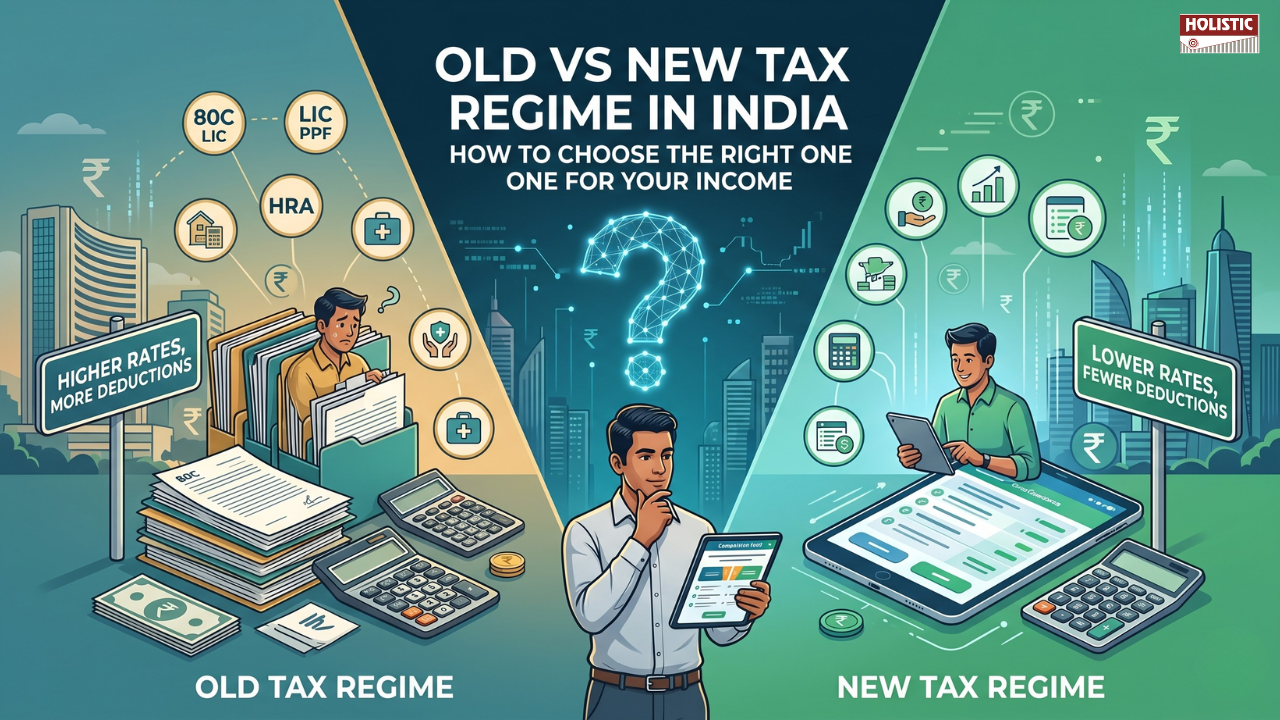

- Understanding the Two Tax Regimes in India

- The Old Tax Regime: Built for Savers and Planners

- The New Tax Regime: Simplicity and Lower Rates

- Key Differences: Old vs New Tax Regime Explained

- Who Should Choose the Old Tax Regime?

- Who Should Choose the New Tax Regime?

- A Practical Example: ₹10 Lakh Income Comparison

- The Hidden Mistake: Investing Only for Tax Saving

- How to Decide the Right Tax Regime Every Year?

- Conclusion: Tax Planning Should Support Life Goals

Understanding the Two Tax Regimes in India

India currently offers two parallel tax systems for individuals:

- The Old Tax Regime, which allows multiple deductions and exemptions

- The New Tax Regime, which offers lower tax rates but removes most deductions

Both systems are valid. Both have their advantages.

The real question is:

Which one works better for you?

The Old Tax Regime: Built for Savers and Planners

The old tax regime rewards individuals who actively save and invest.

It allows deductions under various sections like:

- Section 80C (PF, PPF, ELSS, life insurance)

- Section 80D (health insurance)

- Home loan interest deductions

- Standard deduction and other exemptions

This structure encourages disciplined financial behaviour.

But there’s a trade-off.

Tax calculation becomes more detailed and sometimes complex.

You need proper documentation, planning, and tracking of investments throughout the year.

So, while it helps reduce taxes, it requires effort.

The New Tax Regime: Simplicity and Lower Rates

The new tax regime takes a different approach.

Instead of offering deductions, it provides lower tax rates across income slabs.

The idea is simple:

- No need to track investments for tax purposes

- No complicated calculations

- Straightforward tax filing

This makes it attractive for individuals who prefer clarity and ease.

However, the downside is clear—you lose most deductions, which could otherwise reduce your taxable income significantly.

Key Differences: Old vs New Tax Regime Explained

At its core, the difference comes down to one question:

Do you want deductions or simplicity?

- The old regime reduces taxable income through investments

- The new regime reduces tax rates but removes deductions

So, your choice depends on whether you already invest enough to benefit from deductions—or prefer a clean, no-hassle approach.

Who Should Choose the Old Tax Regime?

The old tax regime tends to work better for individuals who:

- Regularly invest in Provident Fund (PF) or Public Provident Fund (PPF)

- Pay life insurance premiums

- Invest in tax-saving instruments like ELSS

- Have a home loan with interest and principal repayments?

- Actively plan their taxes and want to maximize deductions

If your financial life already includes these components, the old regime can significantly reduce your tax liability.

Who Should Choose the New Tax Regime?

The new tax regime is more suitable for individuals who:

- Do not have major tax-saving investments

- Prefer flexibility instead of locking money into specific instruments

- Want a simple and quick tax filing process

- Are early in their careers with fewer financial commitments

For such individuals, lower tax rates without conditions can be more beneficial.

A Practical Example: ₹10 Lakh Income Comparison

Let’s consider an individual earning ₹10 lakh annually.

Under the old regime:

- If they claim deductions through investments and expenses, their taxable income reduces

- This can significantly lower the final tax payable

Under the new regime:

- No deductions are applied

- Tax is calculated directly using lower slab rates

So, which is better?

It depends entirely on how much deduction the individual can claim.

If deductions are substantial, the old regime wins.

If deductions are minimal, the new regime becomes more efficient.

The Hidden Mistake: Investing Only for Tax Saving

Here’s where many people go wrong.

They invest not because it aligns with their goals—but simply to save tax.

This leads to:

- Buying unnecessary insurance policies

- Locking money in low-return instruments

- Ignoring liquidity and flexibility

Ask yourself:

Are you investing for your future—or just to reduce this year’s tax?

Tax saving should be a by-product of good financial planning—not the primary goal.

How to Decide the Right Tax Regime Every Year?

There is no permanent “best” regime.

Your choice should evolve with your life stage.

A simple approach is:

- Calculate your taxable income under both regimes

- Include all eligible deductions in the old regime

- Compare the final tax payable

- Choose the option that gives you the lowest tax

This exercise may take some effort—but it ensures you make an informed decision.

Conclusion: Tax Planning Should Support Life Goals

The debate between old vs new tax regime is not about which system is better universally.

It’s about which system is better for you.

If you are a disciplined investor, the old regime rewards you.

If you prefer simplicity and flexibility, the new regime supports you.

But remember:

Your financial plan should not revolve around taxes.

Taxes should fit into your financial plan.

Because in the long run, wealth is built not by saving tax—but by making smart financial decisions.

A Certified Financial Planner (CFP) can help you evaluate both tax regimes and align your tax strategy with your overall financial goals.

Leave a Reply