Life Insurance!

When you read it, what came to your mind?

Did you think of an insurance plan that promises a sum assured against life and a Lumpsum at maturity?

You probably have a couple of them in your portfolio, too. It is an investment while also securing your life. It was claimed to be a “genius product”.

It also reminds me of another genius discovery—Radium.

A century ago, cosmetics and healthcare products had radium in them. The manufacturers pushed these products to consumers, claiming—“It can make your skin glow in dark”—“It can cure illness as bad as cancer”.

It was portrayed as a—“miracle element”—just the same way.

Radium charged products were a must-have in every household until the radiation poisoning took its time to kill them inside out.

—One solution to all problems.

Does it sound familiar?

Today, the way investment insurance policies and ULIPs are being marketed—as one product for all your financial needs—they must be the radium in the world of personal finance. Especially the ULIPs, it is claimed to be the readymade financial plan for all.

Just because a product is termed “safe” and a majority is buying it, it does not mean it is safe.

Table of Contents:

A Slow Poison that is Investment Insurance

Over the years, insurance companies, their agents and advertisers have romanticized the investment insurance plans.

To increase the sale of insurance, they presented the insurance plans with tax benefits and the supposed investment benefits, and still do. They leverage the word “assured”, “guaranteed” and the excellent marketing skills developed over the years to sell a product.

In reality, they locked-up your savings for a meager life cover with no respectable appreciation. Investment insurance policies deceive on three different fronts. They are Insurance, Investment, and Tax Benefits. In life insurance, in case of death, your nominee gets paid but if you survive, you would get nothing. In order to get back something, people opt for life insurance policies that return a certain sum even if you survive.

But Insurance is not an investment. We are often sold insurance as an investment product instead of a protection product. Insurance is to protect your family from the uncertainty of your death. While investment is to accumulate wealth to meet your financial goals or to earn a regular income.

What happens when you mix insurance and investment?

What happens when you mix insurance and investment?

- You become underinsured.

- You won’t be able to accumulate sufficient wealth to meet your financial goals.

- The cost of insurance reduces your returns.

So, when you attempt to achieve more than one financial goal with a single product it becomes complicated. This also makes it harder to assess whether it’s a good deal. Hence focusing on one goal is better.

Insurance agents would say that Endowment policies offer both insurance and investment. In reality, an endowment policy yields only 5-6 % and as an insurance product, it doesn’t offer adequate life cover.

Let me lay the facts down before you.

It is evident from the table that investment insurance instruments are the poorest performers in all aspects.

- They offer very low sum assured for the premiums paid, which makes them a questionable insurance product.

- Investment insurance policies are only one of the many investment instruments which offer tax benefits under section 80C.

- As shown in the table above, returns on ELSS mutual funds are way better than investment insurance policies, even if their returns are taxable.

Let’s see an example,

Imagine a person who wants to invest and have his life covered. Let’s call him Sugan.

Sugan is just 30 years old and wants to invest ₹100,000 a year. See, what different options he has to choose from.

Note: For a fair comparison with the Endowment Plan, the contribution to PPF is limited to only 10 years.

Note: For a fair comparison with the Endowment Plan, the contribution to PPF is limited to only 10 years.

Of the ₹1 Lakh, ₹12,250 is paid as the policy premium for the term plan and the rest is invested in Mutual Funds.

Here, if Sugan chooses the term plan along with Mutual Fund investment, he’d easily get ₹67 Lakhs at the end of 20 years. The return from Mutual Funds is almost twice that of ULIP’s return.

In case of his death, his family would receive a sum assured of ₹25 Lakhs from the insurance policy, in addition to the Mutual Fund value.

Revive Your Dying Insurance Portfolio

Getting to know the right and wise things is always exciting and often enlightening. Just as the old saying goes,

But what is the point of knowing that investment insurances stunt your investments if you don’t have the power to get rid of them?

Savings insurances and ULIPs: You buy it once. You have to pay a hefty sum as the premium. Now that you know savings insurance plans and ULIPs are not good for your financial plan, you want to remove them from your portfolio.

But you’re concerned about the Surrender charges and the loss of investment you will be facing.

And accepting loss should be the last thing for a wise investor. It’s the fundamental rationale, isn’t it?

In some rare situations, accepting a loss will fetch you good rewards than denying it. And more importantly, it will season you as an investor.

Get out of your dilemma in 3-steps

- Identifying Your Escape Options

- The Axing of Investment Draining Policies

- It is here, you must realize the importance of calculated risk.

i) Identifying Your Escape Options

You may have had legitimate reasons to buy these savings-cum-insurance policies.

In the past, traditional insurance policies were relevant and “wealth growing” was not a thing. Personal finance was all about savings and savings alone, then.

But financial planning is all about the financial future, isn’t it?

I want you to take a look at your insurance portfolio. How many savings-cum-insurance policies do you have?

—Is it one or two? Is it more than two?

Regardless, you still have a way out of these financial drains.

With your insurance plan, you may either,

i) Surrender Your Policy or

ii) Make it a Paid-up Policy or

iii) Continue Your Policy.

There are some technical hurdles. But the biggest is, as discussed earlier, to endure the loss.

Yet, if you work around these hurdles and tweak up your financial plan, you can come out on top successfully.

ii) The Axing Of Investment Draining Policies

Even though there are three different options to optimize your insurance portfolio, not all options are equally adverse.

One may be worse than the other based on your current policy year. You may use a trial and error method to identify what suits your portfolio best.

We shall go through the different escape options that are available to you.

i) Surrendering Your Insurance Policy:

In simple terms, surrendering your policy would mean to give up your policy and get back the surrender value as on the date of surrender.

But there is more to it.

- Your policy has no surrender value if you surrender in the first year.

- Premium paid in the first year will not be accounted for surrender value calculation.

- After successful premium payment of every year, the surrender value will increase gradually coming up to 90% of the premium in the last year of the policy term.

For example:

Just as seen in the example above—Let’s say you have an endowment plan of 20 years policy term; with a premium paying term of 10 years. It offers a ₹25Lakhs Sum Assured and ₹22Lakhs at maturity.

To date, you have paid the premium of ₹1 Lakh per year, for 2 years. See the table below.

If you surrender your policy now, you will have to tank an apparent potential “loss” of ₹1.38 Lakhs.

If you surrender your policy now, you will have to tank an apparent potential “loss” of ₹1.38 Lakhs.

But, is this better than the other two options?

Let’s compare and find out.

ii) Make it a Paid-up Policy

It is similar to surrendering. Except, you get the “Special Surrender Value” at the end of the policy term.

If you convert your policy to a paid-up policy, you don’t have to pay further premiums. The special surrender value is usually higher than the surrender value.

- Your life cover amount will be reduced depending on the premiums paid.

- Paid-up value will be calculated based on Sum Assured and a factor based on the number of premiums paid.

- You will receive the paid-up value only after the completion of the policy term.

- Unlike Surrender Values, Paid-up values are not guaranteed.

In our example, if you convert your policy into a paid-up policy, your sum assured will be reduced and is calculated as:

If we count the inflation in @ 6%, which is higher than the bonuses and other appreciation, it is technically zero appreciation for your investment that is locked-up for 18 years.

If we count the inflation in @ 6%, which is higher than the bonuses and other appreciation, it is technically zero appreciation for your investment that is locked-up for 18 years.

Moreover, it is a common mistake among investors, to stop their premium payment when they adapt to better investment instruments such as Mutual Funds. As a result, the policy lapses into a paid-up policy, leaving a sum locked-up with the policy.

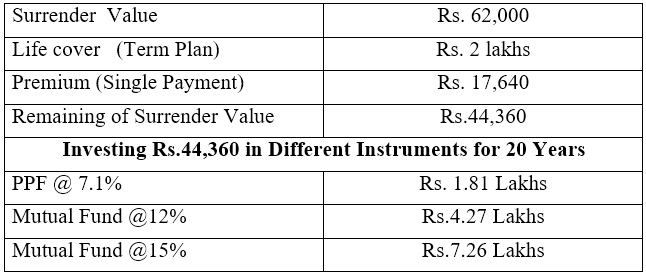

On the other hand, let’s see what happens if you surrender your policy and get the same life cover as the paid-up policy offers. And invest the remaining surrender value amount in different instruments.

From the table, even the term plan with PPF delivers the same as your insurance policy.

From the table, even the term plan with PPF delivers the same as your insurance policy.

Meanwhile, Mutual Fund investments are way beyond comparison. If you can get out of your comfort zone, the Mutual Fund will reward you the best.

But, is this it?

What Happens If You Surrender and Invest in Mutual Funds?

Continuing your insurance policy is—straight out—the least favorite option to choose.

We have seen surrendering your policy means “losing” a part of the premium, whereas making your policy paid-up gives it back to you.

But, what if you surrender your policy and invest the subsequent premiums along with the surrender value in Mutual Funds?

Could it nullify the potential “loss”? Could it deliver better than the paid-up option?

Let’s see what happens if you invest this surrender value and the rest of the premium in a mutual fund while having your life covered for ₹25 Lakhs.

In terms of PPF: If we consider the special surrender value, with the paid-up option, it is a close call.

In terms of PPF: If we consider the special surrender value, with the paid-up option, it is a close call.

That is assuming: your policy does not incur any charges and a good bonus is paid. If you continue your policy, you will be paying an 18% GST over and above your savings insurance premiums.

Taking these into account, PPF investment is a sure winner by a good margin.

But if you are serious about your financial plan—since you have read this far, I believe you are—you may invest in Mutual Funds.

Look at the numbers in the table, even an average performing mutual fund scheme delivers twice as good as any investment insurance policy.

If you can find a better fund and work on your risk tolerance, you may even get 300% better appreciation than that of an investment insurance policy.

Your Moment to Take Control

It is hard to deliberately surrender your policy.

It is a daring step, far from anyone’s comfort zone.

But, in the long-term perspective, it gives you better returns, almost 3 times better returns.

It allows you to acknowledge the mistake—and thrive in times of financial stress. It will present the opportunity to attain financial maturity. I believe this is the very definition and purpose of calculated risk.

Understanding insurance policies can be pretty tiring. Have any doubts on how to optimally terminate your “investment insurance policies”?

Ask us in the comments below—or reach out to us.

Claim your free 30-minute consultation by clicking “Register Now” below.

Your blog is a fantastic resource! The information is clear, concise, and incredibly helpful. Keep up the great work!