Is the PNB MetLife TULIP Plan the ultimate solution for your long-term financial goals, or could it be just another overhyped ULIP?

Is the PNB MetLife TULIP Plan the key to unlocking financial security, or should you explore other options?

Does the PNB MetLife TULIP Plan strike the perfect balance between investment growth and insurance coverage, or is there a catch?

In this article, we take a closer look at the plan’s features, benefits, drawbacks, and the overall cost involved to help you decide if it’s the right fit for your financial goals.

Table of Contents

What is the PNB MetLife TULIP?

What are the features of the PNB MetLife TULIP?

Who is eligible for the PNB MetLife TULIP?

What are the benefits of the PNB MetLife TULIP?

What are the investment strategies and fund options in the PNB MetLife TULIP?

What are the charges in the PNB MetLife TULIP?

Grace Period, Discontinuance, and Revival of PNB MetLife TULIP

Free Look Period for PNB MetLife TULIP

Surrendering PNB MetLife TULIP

What are the advantages of the PNB MetLife TULIP?

What are the disadvantages of the PNB MetLife TULIP?

Research Methodology of PNB MetLife TULIP

Benefit Illustration – IRR Analysis of PNB MetLife TULIP

PNB MetLife TULIP Vs. Othe Investments

PNB MetLife TULIP Vs. Pure-term + ELSS

Final Verdict on PNB MetLife TULIP

What is the PNB MetLife TULIP?

PNB MetLife Term with Unit Linked Insurance Plan is an Individual, Unit-Linked, Non-Participating, Savings Life Insurance plan. The plan offers the potential for significant long-term wealth growth through the diverse portfolio of funds.

What are the features of the PNB MetLife TULIP?

- Provides substantial life insurance coverage to financially protect your family against unexpected events

- Offers the potential to grow your investments through market-linked returns

- Allows you to choose from 17 fund options tailored to your risk appetite

- Returns a portion of the premium allocation and mortality charges at set intervals during the PNB MetLife TULIP Plan policy term

- Option to boost your coverage with the PNB MetLife Linked Accidental Death Benefit Rider

- Enjoy possible tax benefits on premiums paid and policy benefits, subject to current tax laws

Who is eligible for the PNB MetLife TULIP?

| Parameters | Minimum | Maximum |

| Entry Age (Yrs) | 18 | 65 |

| Maturity Age (Yrs) | 33 | 85 |

| Premium paying term (Yrs) | 5,6 and 10 | |

| Policy term (Yrs) | 15 and 20 | |

| Premium (Yrs) | Annualised – 36,000 | No Limit |

| Half-yearly – 18,000 | ||

| Quarterly – 9,000 | ||

| Monthly – 3,000 | ||

| Rider Options | PNB MetLife Linked Accidental Death Benefit Rider (UIN: 117A024VO1) | |

What are the benefits of the PNB MetLife TULIP?

1.Death Benefit

The benefit payable on the death of the Life Assured shall be the Higher of:

- Fund value as at the date of intimation of death

- Sum assured less all partial withdrawals made during the last two years immediately preceding the date of death of the life assured

- 105% of the Total premiums received up to the date of death

Where the Sum assured is defined as the Sum assured cover multiplied by the Annualised premium

2.Maturity benefit

The Maturity benefit is the amount payable to the Life assured on maturity of the policy at the end of the PNB MetLife TULIP Plan Policy term. It is equal to the Total fund value in the unit account determined using the net asset value on the maturity.

What are the investment strategies and fund options in the PNB MetLife TULIP?

PNB MetLife TULIP offers you the flexibility to choose from 3 fund management strategies as mentioned below:

- Self-managed Strategy

- Systematic Transfer Strategy

- Life Stage Strategy

Self-managed Strategy

This strategy enables you to manage your savings actively. Under this strategy, you can save premiums among 17 funds in proportion of your choice.

You have the option of switching among the funds as mentioned below, and may choose the premium redirection option for your future premiums, depending on your changing risk appetite and market conditions. The details of various funds are mentioned in the table below:

| Asset Category | |||||

| S. No | Fund Name | Equities | Debt | Money Market | Risk Profile |

| 1 | Mid-cap fund | 60-100% | 0 | 0-40% | Very High Risk |

| 2 | Premier Multi cap fund | 60-100% | 0 | 0-40% | Very High Risk |

| 3 | Virtue II fund | 60-100% | 0 | 0-40% | Very High Risk |

| 4 | Crest (Thematic Fund) | 60-100% | 0 | 0-40% | Very High Risk |

| 5 | Flexi cap fund | 60-100% | 0 | 0-40% | Very High Risk |

| 6 | Multiplier III | 60-100% | 0 | 0-40% | Very High Risk |

| 7 | Sustainable Equity fund | 60-100% | 0 | 0-40% | Very High Risk |

| 8 | India Opportunities Fund | 60-100% | 0 | 0-40% | Very High Risk |

| 9 | Balanced Opportunities Fund | 40-75% | 25-60% | 0-35% | Medium Risk |

| 10 | Balancer II fund | 0-60% | Govt & debt Securities -0-60% | 0-40% | Medium Risk |

| 11 | Protector II fund | 0 | Govt & debt Securities -0-60% | 0-40% | Low Risk |

| 12 | Bond opportunities fund | 0 | 80-100% | 0-20% | Low Risk |

| 13 | Liquid fund | 0 | 0 | 100% | Low Risk |

| 14 | Small-cap fund | 60-100% | 0 | 0-40% | Very High Risk |

| 15 | Bharat Manufacturing Fund | 60-100% | 0 | 0-40% | Very High Risk |

| 16 | Bharat Consumption Fund | 60-100% | 0 | 0-40% | Very High Risk |

| 17 | Nifty 500 Momentum 50 Index Fund | 60-100% | 0 | 0-40% | Very High Risk |

The Systematic Transfer Strategy helps safeguard your wealth against market volatility and is available only if you have opted for a Regular Pay or Limited Pay policy with annual frequency as the premium payment mode.

This strategy ensures a gradual exposure to equity from debt in a phased manner through equal instalments over 12 months. All instalment premiums will be invested in the Protector II Fund (debt-oriented fund).

This amount will be systematically transferred to the Premier Multi-cap Fund (equity-oriented fund) over the 12-month PNB MetLife TULIP Plan Policy period.

At policy inception, your premium, net of allocation charge is distributed between two funds, Premier Multi-cap Fund (equity-oriented fund) and Protector II Fund (debt-oriented fund), based on your attained age.

As you move from one age band to another, your funds are re-distributed based on your age. The age-wise portfolio distribution is shown in the table.

| AGE OF POLICYHOLDER (YEARS) | PREMIER MULTI-CAP FUND | PROTECTOR II FUND |

| Up to 30 | 70% | 30% |

| 31 – 40 | 60% | 40% |

| 41 – 50 | 50% | 50% |

| 51 – 60 | 40% | 60% |

| 61 – 70 | 20% | 80% |

| 71+ | 10% | 90% |

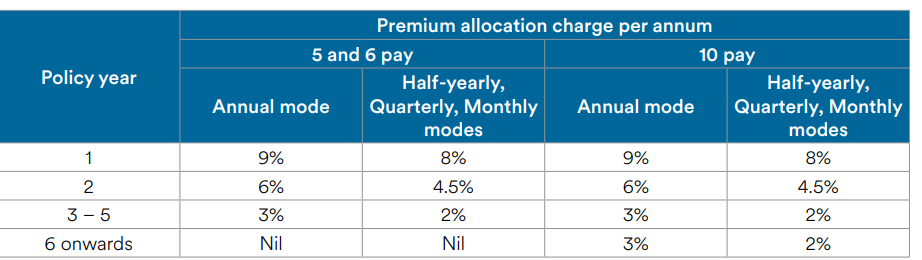

What are the charges in the PNB MetLife TULIP?

A).Mortality charges

Mortality charge will be based on the Plan Option, attained age of the Life Insured, Rate as per the Mortality Charge Table, and the applicable Sum at Risk.

| AGE (YRS) | 30 | 40 | 50 | 60 |

| MALE | 1.2701 | 2.184 | 5.7668 | 14.5106 |

| FEMALE | 1.2142 | 1.7654 | 4.1184 | 11.6025 |

B).Partial Withdrawal charge

Partial Withdrawals are free of any charge.

C).Premium Allocation Charge

These are expressed as a percentage of the premium, and it is deducted from the premium amount at the time of premium payment; and balance units are allocated in the chosen funds thereafter.

D).Policy Administration charge

The Policy Administration charge is 2% p.a. of the annualised premium, increasing at 5% p.a. Policy Administration Charges would be deducted throughout the PNB MetLife TULIP Plan policy term. These charges would not exceed Rs 500 per month.

E).Fund management charge

| S No | Fund Name | Charge per annum |

| 1 | Protector II fund | 1.00% |

| 2 | Bond opportunities fund | 1.00% |

| 3 | Liquid fund | 1.00% |

| 4 | Balancer II fund | 1.15% |

| 5 | Balanced Opportunities Fund | 1.15% |

| 6 | Multiplier III | 1.25% |

| 7 | Premier Multi cap fund | 1.25% |

| 8 | Mid-cap fund | 1.25% |

| 9 | Crest (Thematic Fund) | 1.25% |

| 10 | Flexi cap fund | 1.25% |

| 11 | Virtue II fund | 1.25% |

| 12 | India Opportunities Fund | 1.35% |

| 13 | Sustainable Equity fund | 1.35% |

| 14 | Small-cap fund | 1.25% |

| 15 | Bharat Manufacturing Fund | 1.25% |

| 16 | Bharat Consumption Fund | 1.25% |

| 17 | Nifty 500 Momentum 50 Index Fund | 1.25% |

| Discontinued Fund | 0.50% |

F).Discontinuance charges

The Discontinuance Charges are expressed either as a percentage of the fund value (FV) or as a percentage of the annualised premium (AP) or Single Premium. It depends on the premium amount, the year of discontinuance and the premium paying term.

G).Switching charges

You can make unlimited switches in a Policy Year free of any charge.

Inference from the charges: The PNB MetLife TULIP Plan comes with considerable charges for a market-linked product. While certain charges are refunded at regular intervals, some charges are levied throughout the PNB MetLife TULIP Plan policy term.

These high costs reduce the effective amount invested, which can negatively impact your overall returns. Consequently, your long-term maturity benefits may be significantly lower.

Grace Period, Discontinuance, and Revival of PNB MetLife TULIP

Grace period

A grace period of 30 days (15 days for the monthly mode) from the due date of unpaid Premium will be allowed to pay all your due Premiums.

Discontinuance

In case of discontinuance of policy during the lock-in period: the policy will move to the Discontinued Status.

The Fund Value as on the date of discontinuance shall be transferred to the Discontinued Policy Fund after deducting the applicable discontinuance charge, and all risk cover(s) under the Policy shall cease.

At the end of the lock-in period, the proceeds of the discontinuance fund shall be paid to the policyholder, and the policy shall terminate.

In case of discontinuance of the policy after the lock-in period, the policy shall attain reduced Paid-up Status with reduced Paid-up Sum Assured.

The Paid-up sum assured is given as the original sum assured multiplied by the total number of premiums paid to the original number of premiums payable as per the terms and conditions of the policy.

Revival

The Policyholder has the option to revive the policy within a revival period of three years from the date of discontinuance of the PNB MetLife TULIP Plan policy.

Free Look Period for PNB MetLife TULIP

If you have any objections to the terms and conditions of Your Policy, you may cancel the policy within 30 days from the date of receipt of the Policy Document, whether received electronically or otherwise.

Surrendering PNB MetLife TULIP

During the first five policy years, on receipt of surrender intimation, the Fund Value after deduction of the applicable Discontinuance Charge shall be transferred to the Discontinued Policy Fund. The proceeds of the discontinued policy shall be paid at the end of the lock-in period.

Only fund management charges will be deducted from this fund during this period.

After Completion of the first five years, on receipt of surrender intimation, you will be entitled to the total Fund Value under the policy.

What are the advantages of the PNB MetLife TULIP?

- Flexibility: You have the option to reduce your Sum Assured, modify the Premium Paying Term or policy term, and lower your Instalment Premium after the first five policy years.

- Premium Redirection: Adjust your investment strategy by redirecting future premiums to different funds as your financial goals or market outlook change.

- Fund Switching: You can switch your investments—either partially or fully—between the available segregated funds under the self-managed option.

- Partial Withdrawals: After completing the five-year lock-in period or once the Life Assured turns 18 (whichever is later), you may withdraw a portion of the fund value.

- Flexible Payment Modes: Choose to pay your Instalment Premiums annually, semi-annually, quarterly, or monthly. You can switch between these payment modes at any time during the policy term.

What are the disadvantages of the PNB MetLife TULIP?

- No Loan Option: The PNB MetLife TULIP Plan policy does not allow you to borrow against its value.

- Mandatory Lock-In: A five-year lock-in period applies before any withdrawals can be made.

- Reduced Investable Amount: Only the net premium, after deducting various charges, is invested in the selected funds.

- Restricted Life Cover: The life insurance component may fall short of providing adequate financial protection for your dependents.

Research Methodology of PNB MetLife TULIP

When assessing a market-linked product, estimating potential returns is crucial—it enables comparison with other investment options and helps you make informed financial decisions. Let’s evaluate a quote from the PNB MetLife portal.

Benefit Illustration – IRR Analysis of PNB MetLife TULIP

A 35-year-old male opts for the plan with a sum assured of ₹15 lakhs. The PNB MetLife TULIP Plan policy term is 20 years, and the premium is paid for 10 years at ₹1,00,000 annually. At maturity, the accumulated fund value will be paid out.

| Male | 35 years |

| Sum Assured | ₹ 15,00,000 |

| Policy Term | 20 years |

| Premium Paying Term | 10 years |

| Annualised Premium | ₹ 1,00,000 |

The brochure illustrates projected outcomes based on assumed gross investment returns of 4% and 8% per annum. These figures are purely indicative—the actual returns are not guaranteed and may vary depending on market performance.

| At 4% p.a. | At 8% p.a. | ||||

| Age | Year | Annualised premium / Maturity benefit | Death benefit | Annualised premium / Maturity benefit | Death benefit |

| 35 | 1 | -1,00,000 | 15,00,000 | -1,00,000 | 15,00,000 |

| 36 | 2 | -1,00,000 | 15,00,000 | -1,00,000 | 15,00,000 |

| 37 | 3 | -1,00,000 | 15,00,000 | -1,00,000 | 15,00,000 |

| 38 | 4 | -1,00,000 | 15,00,000 | -1,00,000 | 15,00,000 |

| 39 | 5 | -1,00,000 | 15,00,000 | -1,00,000 | 15,00,000 |

| 40 | 6 | -1,00,000 | 15,00,000 | -1,00,000 | 15,00,000 |

| 41 | 7 | -1,00,000 | 15,00,000 | -1,00,000 | 15,00,000 |

| 42 | 8 | -1,00,000 | 15,00,000 | -1,00,000 | 15,00,000 |

| 43 | 9 | -1,00,000 | 15,00,000 | -1,00,000 | 15,00,000 |

| 44 | 10 | -1,00,000 | 15,00,000 | -1,00,000 | 15,00,000 |

| 45 | 11 | 0 | 15,00,000 | 0 | 15,00,000 |

| 46 | 12 | 0 | 15,00,000 | 0 | 15,00,000 |

| 47 | 13 | 0 | 15,00,000 | 0 | 15,00,000 |

| 48 | 14 | 0 | 15,00,000 | 0 | 15,00,000 |

| 49 | 15 | 0 | 15,00,000 | 0 | 15,00,000 |

| 50 | 16 | 0 | 15,00,000 | 0 | 15,00,000 |

| 51 | 17 | 0 | 15,00,000 | 0 | 15,00,000 |

| 52 | 18 | 0 | 15,00,000 | 0 | 15,00,000 |

| 53 | 19 | 0 | 15,00,000 | 0 | 15,00,000 |

| 54 | 20 | 0 | 15,00,000 | 0 | 15,00,000 |

| 55 | 15,63,799 | 26,58,977 | |||

| IRR | 2.90% | 6.40% | |||

At 4% return, the projected fund value is ₹15.63 lakhs, translating to an Internal Rate of Return (IRR) of 2.90% as per the PNB MetLife TULIP Plan maturity calculator.

At 8% return, the projected fund value is ₹26.58 lakhs, yielding an IRR of 6.40% as per the PNB MetLife TULIP Plan maturity calculator.

Market-linked products are typically chosen with the expectation that they will generate returns that outpace inflation over the long term. However, the PNB MetLife TULIP Plan falls short in this regard—the projected returns may not be sufficient to beat inflation and grow your wealth meaningfully.

Moreover, the sum assured offered under the plan is relatively low, making it inadequate for comprehensive financial protection. This combination of modest returns and limited life cover raises concerns about the plan’s effectiveness in meeting both investment and insurance needs.

This highlights a potential shortfall in achieving the target corpus if you rely solely on this ULIP.

PNB MetLife TULIP Vs. Othe Investments

The PNB MetLife TULIP Plan, though a market-linked product, delivers returns that fall short, even when compared to conservative debt instruments.

Given the mismatch between the risk taken and the returns offered, it’s worth exploring alternative strategies that provide better risk-adjusted outcomes.

ULIPs combine insurance and investment, but in many cases, separating these two components can lead to far more effective financial planning. Let’s revisit the earlier scenario with a more efficient approach.

PNB MetLife TULIP Vs. Pure-term + ELSS

To secure life coverage, a pure-term insurance policy with a sum assured of ₹15 lakhs costs approximately ₹12,000 annually for a 20-year term with a 10-year premium payment period.

Compared to the ₹1,00,000 annual premium under the TULIP plan, this leaves an investible surplus of ₹88,000 per year.

| Pure Term Life Insurance Policy | |

| Sum Assured | ₹ 15,00,000 |

| Policy Term | 20 years |

| Premium Paying Term | 10 years |

| Annualised Premium | ₹ 12,000 |

| Investment | ₹ 88,000 |

Your investment strategy can be tailored to your risk appetite. Conservative investors might opt for instruments like PPF, while growth-oriented individuals may choose equity-linked options such as ELSS funds. In this example, we assume the investment is made in ELSS.

| Term insurance + ELSS | |||

| Age | Year | Term Insurance premium + ELSS | Death benefit |

| 35 | 1 | -1,00,000 | 15,00,000 |

| 36 | 2 | -1,00,000 | 15,00,000 |

| 37 | 3 | -1,00,000 | 15,00,000 |

| 38 | 4 | -1,00,000 | 15,00,000 |

| 39 | 5 | -1,00,000 | 15,00,000 |

| 40 | 6 | -1,00,000 | 15,00,000 |

| 41 | 7 | -1,00,000 | 15,00,000 |

| 42 | 8 | -1,00,000 | 15,00,000 |

| 43 | 9 | -1,00,000 | 15,00,000 |

| 44 | 10 | -1,00,000 | 15,00,000 |

| 45 | 11 | 0 | 15,00,000 |

| 46 | 12 | 0 | 15,00,000 |

| 47 | 13 | 0 | 15,00,000 |

| 48 | 14 | 0 | 15,00,000 |

| 49 | 15 | 0 | 15,00,000 |

| 50 | 16 | 0 | 15,00,000 |

| 51 | 17 | 0 | 15,00,000 |

| 52 | 18 | 0 | 15,00,000 |

| 53 | 19 | 0 | 15,00,000 |

| 54 | 20 | 0 | 15,00,000 |

| 55 | 48,26,025 | ||

| IRR | 10.40% | ||

With an ELSS investment of ₹88,000 per year for 10 years, the estimated pre-tax maturity value is ₹53.71 lakhs. After applying capital gains tax, the net maturity value comes to around ₹48.26 lakhs, delivering a post-tax IRR of 10.40%.

| ELSS Tax Calculation | |

| Maturity value after 20 years | 53,71,885 |

| Purchase price | 8,80,000 |

| Long-Term Capital Gains | 44,91,885 |

| Exemption limit | 1,25,000 |

| Taxable LTCG | 43,66,885 |

| Tax paid on LTCG | 5,45,861 |

| Maturity value after tax | 48,26,025 |

This clearly demonstrates that separating insurance from investment not only improves returns but also supports stronger wealth creation and long-term financial growth—a significant improvement over what the PNB MetLife TULIP Plan offers.

Final Verdict on PNB MetLife TULIP

The PNB MetLife Term with Unit Linked Insurance Plan (TULIP), as the name indicates, combines life insurance with market-linked investment. Like most ULIPs, it carries multiple charges that reduce the net premium invested.

While some of these charges are refunded at intervals, the time value of money is not factored in considerably, which diminishes their actual benefit.

Our return analysis reveals that the plan’s long-term performance is relatively weak. For a market-linked product, the returns are modest, indicating an unfavourable risk-to-return balance and it also has a high agent commission.

Furthermore, the sum assured offered may be inadequate to cover even basic family protection needs, potentially jeopardising your financial plan over time. Overall, the PNB MetLife TULIP Plan is not a suitable option for long-term wealth creation.

Bundling insurance with investments—as in ULIPs—is generally not advisable. A better approach is to opt for a pure-term life insurance policy that provides essential financial protection at a low cost.

The savings from lower premiums can be invested in a diversified portfolio across asset classes, offering a stronger chance of meeting long-term financial goals.

Choosing the right insurance and investment products requires careful analysis. If you’re unsure where to begin, consider consulting a Certified Financial Planner (CFP).

Do Quora, Facebook, and Twitter have the final say when it comes to financial advice?

Their professional guidance can help you align your insurance coverage and investment strategy with your specific financial needs and goals.

Leave a Reply