Is the Pramerica Life Wealth Enhancer Plan truly the growth booster your portfolio needs, or could it leave your wealth underperforming?

Could the Pramerica Life Wealth Enhancer Plan be your gateway to long-term financial security, or is it just another ULIP with hidden catches?

Will the Pramerica Life Wealth Enhancer Plan really enhance your wealth, or is it more hype than substance?

But is the Pramerica Life Wealth Enhancer Plan the right choice for such an investment? Let’s explore its features, benefits, and drawbacks to find out.

Table of Contents

What is the Pramerica Life Wealth Enhancer?

What are the features of the Pramerica Life Wealth Enhancer?

Who is eligible for the Pramerica Life Wealth Enhancer?

What are the benefits of the Pramerica Life Wealth Enhancer?

What are the investment strategies and fund options in the Pramerica Life Wealth Enhancer?

What are the charges in the Pramerica Life Wealth Enhancer?

Free Look Period for the Pramerica Life Wealth Enhancer

Surrendering the Pramerica Life Wealth Enhancer

What are the advantages of the Pramerica Life Wealth Enhancer?

What are the disadvantages of the Pramerica Life Wealth Enhancer?

Research Methodology of Pramerica Life Wealth Enhancer

Benefit Illustration – IRR Analysis of Pramerica Life Wealth Enhancer

Pramerica Life Wealth Enhancer Vs. Other Investments

Pramerica Life Wealth Enhancer Vs. Pure-term + Equity Mutual Fund

Final Verdict on the Pramerica Life Wealth Enhancer

What is the Pramerica Life Wealth Enhancer?

Pramerica Life Wealth Enhancer is a Unit-Linked Non-Participating Individual Savings Life Insurance Plan. It is a single-pay ULIP plan and a perfect combo of savings and protection. It helps you achieve your financial goals and secures your family against the uncertainties of life.

What are the features of the Pramerica Life Wealth Enhancer?

- Make a one-time payment and enjoy benefits for up to 20 years.

- Receive Wealth Additions starting right from the first policy year.

- Get Wealth Boosters at regular intervals to enhance your fund value.

- Choose the Fund Conservation option to protect your investment from market volatility.

- Manage your portfolio efficiently with the Life Stage Portfolio strategy, which balances equity and debt funds based on your age.

- Tax benefits may apply to premiums paid and benefits received, subject to prevailing tax laws.

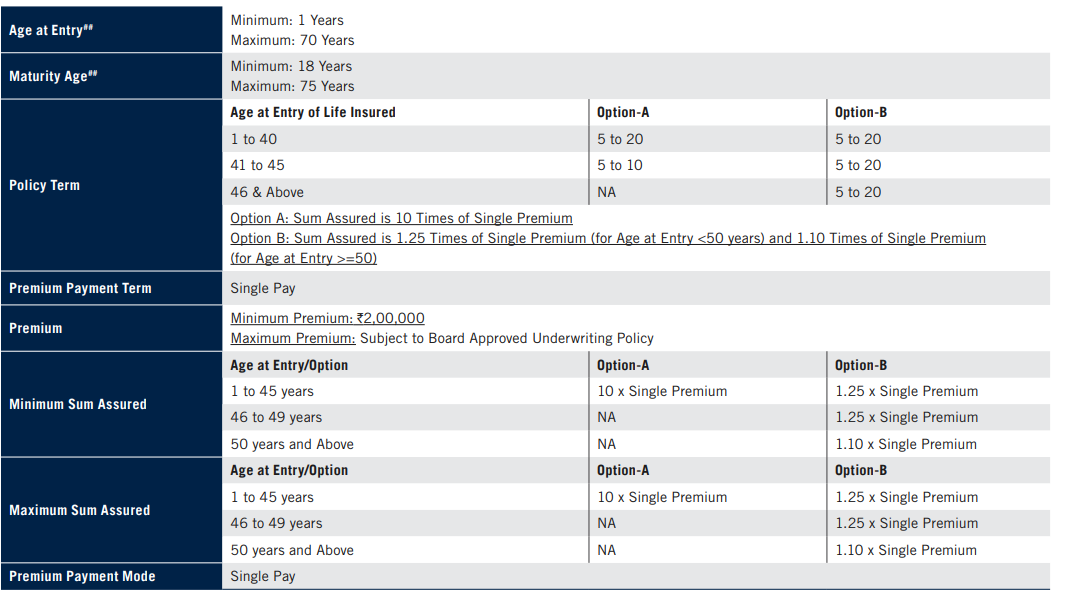

Who is eligible for the Pramerica Life Wealth Enhancer?

What are the benefits of the Pramerica Life Wealth Enhancer?

i). Death Benefit

In case of an unfortunate demise of the Life Insured during the Pramerica Life Wealth Enhancer Plan Policy Term, the nominee shall receive the Death Benefit, which is the higher of

- Sum Assured (reduced by applicable partial withdrawal) or

- Fund Value or

- 105% of Single Premium

ii). Maturity Benefit

On the survival of the Life Insured till the maturity date Fund Value will be paid to you.

iii). Wealth Additions

Wealth Additions as a percentage of the average fund value of the preceding 36 monthiversaries would be allocated as extra units at the end of each policy year, starting from the first Policy year itself to your unit account if they fall within the Pramerica Life Wealth Enhancer Plan Policy Term, provided the policy is in force.

| Policy year | Wealth Additions |

| 1 to 5 | 0.20% |

| 6 onwards | 1% |

iv). Wealth Boosters

Wealth Booster of 1.5% of the average fund value of preceding 36 monthiversaries would be allocated to your unit account at the end of the 6th, 11th, and 16th Policy years, if they fall within the Pramerica Life Wealth Enhancer Plan Policy Term, provided the policy is in force.

What are the investment strategies and fund options in the Pramerica Life Wealth Enhancer?

At inception, the Pramerica Life Wealth Enhancer Plan Policyholder can choose one of the following investment strategies:

- Defined Portfolio Strategy

- Life Stage Portfolio Strategy

Once opted in, the investment strategy will continue throughout the policy term. You cannot switch from one investment strategy to another during the Pramerica Life Wealth Enhancer Plan policy term.

Defined Portfolio Strategy

Under this option, you can choose to invest in any of the funds available (except the discontinuance fund or Liquid Fund) in proportion to your choice.

Within the Defined Portfolio strategy, you also have the option to select the Systematic Transfer Plan (STP) option, for which the Liquid Fund will be made available to you. You can switch money among these funds using the switch option.

You can choose from six funds to invest your money. If you opt for more than one fund, the minimum investment in any fund should be at least 10% of the Annual Premium. The funds and fund objectives are as follows:

| S.no | Fund Name | Asset Allocation | Risk Profile | ||

| Equity & Equity-related instruments | Govt. Securities & Corp. Bonds | Money market instruments | |||

| 1 | Debt fund | 0% | 50-100% | 0-40% | Low |

| 2 | Balance Fund | 10-50% | 0-50% | 0-40% | High |

| 3 | Growth Fund | 40-80% | 0-30% | 0-40% | High |

| 4 | Large-cap Equity fund | 60-100% | 0% | 0-40% | High |

| 5 | Multi-cap opportunities | 50-100% | 0-30% | 0-50% | High |

| 6 | Balanced Equilibrium Fund | 65-75% | 25-35% | 25-35% | Medium |

| 7 | Growth Momentum fund | 75-85% | 15-25% | 15-25% | High |

| 8 | Large-cap advantage fund | 85-100% | 0-15% | 0-15% | High |

| 9 | Flexi Cap Opportunities Fund | 85-100% | 0-15% | 0-15% | High |

| 10 | Pramerica Nifty Mid Cap 50 Correlation Fund | 90-100% | 0-10% | 0-10% | High |

| Liquid fund | 0% | 0% | 100% | Low | |

| Discontinued policy fund | 0% | 60-100% | 0-40% | Low | |

Systematic Transfer Plan (STP)

With STP, you can invest a specific amount at monthly intervals, which gives you the advantage of Rupee Cost Averaging.

You can buy more units when markets are down and fewer units when markets are up, thereby reducing the average unit purchase cost.

You can choose STP only for 12 months; an option would be available to policies wherein the premium is to be paid annually.

Life Stage Portfolio Strategy

The plan offers a life-stage-based investment strategy wherein the investments are distributed between the Multi Cap Opportunities Fund and the Debt Fund, with their proportions varying as per the different life stages.

At inception, the funds will be distributed between two funds, the Multi Cap Opportunities Fund & Debt Fund.

As and when the next milestone is achieved, the funds will be redistributed according to the attained age (age bands) as given in the following table:

| Age as on the last birthday and the last policy anniversary | Debt fund | Multi-Cap Opportunities Fund |

| Up to 25 | 15% | 85% |

| 26 – 30 | 20% | 80% |

| 31 – 35 | 25% | 75% |

| 36 – 40 | 30% | 70% |

| 41 – 45 | 35% | 65% |

| 46 – 50 | 40% | 60% |

| 51 – 55 | 45% | 55% |

| 56 and above | 50% | 50% |

What are the charges in the Pramerica Life Wealth Enhancer?

a). Premium Allocation charge

A premium allocation charge of 3% will be deducted from the Premium amount at the time of Premium payment before allocating the same to the unit account.

b). Policy Administration Charge

Policy administration charge of ₹ 100 per month will be deducted during the first five years at the beginning of each month by cancellation of units from the unit account. There is no policy administration charge from the 6th year onwards.

c). Mortality charge

Mortality charge will apply to the sum at risk. It will be deducted monthly by cancellation of units from the unit account. Mortality charges are guaranteed under this plan.

Annual charges per 1000 sum at risk for a healthy male & female are as follows:

| Attained Age of Life Insured | 25 | 30 | 35 | 40 | 45 | 50 | 55 | 60 |

| Mortality charge | 0.4945 | 0.535 | 0.66 | 0.9405 | 1.5175 | 2.6 | 4.1075 | 5.991 |

d). Fund Management Charges (FMC)

| S.no | Fund Name | Fund Management Charges (FMC) |

| 1 | Debt fund | 1.20% |

| 2 | Balance Fund | 1.20% |

| 3 | Growth Fund | 1.35% |

| 4 | Large-cap Equity fund | 1.35% |

| 5 | Multi-cap opportunities | 1.35% |

| 6 | Balanced Equilibrium Fund | 1.35% |

| 7 | Growth Momentum fund | 1.35% |

| 8 | Large-cap advantage fund | 1.35% |

| 9 | Flexi Cap Opportunities Fund | 1.35% |

| 10 | Pramerica Nifty Mid Cap 50 Correlation Fund | 1.25% |

| Discontinued policy fund | 0.50% |

e). Discontinuance Charge

Discontinuance charge will be based on the year of discontinuance and the premium amount. There is no discontinuance charge from the 5th policy year.

f). Switching Charge

Four switches in a policy year are free of cost, and any subsequent switch in the year will be charged a fee of INR 250 per switch.

g). Inference from the charges: These charges are levied throughout the Pramerica Life Wealth Enhancer Plan policy term, thereby reducing the portion of your premium that is actually invested.

Over time, this leads to lower compounding benefits and can significantly impact your long-term wealth accumulation.

Free Look Period for the Pramerica Life Wealth Enhancer

You will have a period of 30 days from the date of receipt of the Pramerica Life Wealth Enhancer Plan Policy document to review the terms and conditions of the Policy, and if you disagree with any of these terms and conditions, you have the option to return the Policy.

Surrendering the Pramerica Life Wealth Enhancer

Before the Completion of the first 5 policy years (lock-in period): Upon receipt of a request for surrender, the fund value, after deducting the applicable discontinuance charges, shall be credited to the Discontinued Policy Fund.

The Pramerica Life Wealth Enhancer Plan policy shall continue to be invested in the discontinued policy fund, and the proceeds from the discontinuance fund shall be paid at the end of the lock-in period.

After the completion of 5 policy years: The Pramerica Life Wealth Enhancer Plan policyholder has an option to surrender the policy anytime. Upon receipt of a request for surrender, the fund value as on the date of surrender shall be payable.

What are the advantages of the Pramerica Life Wealth Enhancer?

- The Defined Portfolio Strategy allows you to switch investments among the available funds.

- Partial withdrawals are permitted only after completing 5 policy years, which serves as the lock-in period.

- You can choose to receive the maturity benefit as structured payouts spread over up to 5 years after maturity through the settlement option.

What are the disadvantages of the Pramerica Life Wealth Enhancer?

- Loans are not available under this policy.

- The plan offers no liquidity during the initial policy years.

- The sum assured provided is inadequate for comprehensive financial protection.

Research Methodology of Pramerica Life Wealth Enhancer

The Pramerica Life Wealth Enhancer plan offers market-linked benefits through a one-time premium payment, but it’s crucial to evaluate the actual returns before committing.

Let’s examine the Internal Rate of Return (IRR) based on the Pramerica Life Wealth Enhancer Plan policy’s benefit illustration.

Benefit Illustration – IRR Analysis of Pramerica Life Wealth Enhancer

Consider a 30-year-old male who purchases the plan with a 20-year policy term and pays a single premium of ₹5,00,000. The sum assured is ₹6,25,000 (1.25× the premium).

| Male | 30 years |

| Sum Assured | ₹ 6,25,000 |

| Policy Term | 20 years |

| Premium Paying Term | Single Pay |

| Annualised Premium | ₹ 5,00,000 |

At maturity, the fund value depends on assumed return rates. The illustrations use 4% and 8% returns, which are purely indicative and not guaranteed, nor do they reflect the maximum or minimum possible returns.

| At 4% p.a. | At 8% p.a. | ||||

| Age | Year | Annualised premium / Maturity benefit | Death benefit | Annualised premium / Maturity benefit | Death benefit |

| 30 | 1 | -5,00,000 | 6,25,000 | -5,00,000 | 6,25,000 |

| 31 | 2 | 0 | 6,25,000 | 0 | 6,25,000 |

| 32 | 3 | 0 | 6,25,000 | 0 | 6,25,000 |

| 33 | 4 | 0 | 6,25,000 | 0 | 6,25,000 |

| 34 | 5 | 0 | 6,25,000 | 0 | 6,25,000 |

| 35 | 6 | 0 | 6,25,000 | 0 | 6,25,000 |

| 36 | 7 | 0 | 6,25,000 | 0 | 6,25,000 |

| 37 | 8 | 0 | 6,25,000 | 0 | 6,25,000 |

| 38 | 9 | 0 | 6,25,000 | 0 | 6,25,000 |

| 39 | 10 | 0 | 6,25,000 | 0 | 6,25,000 |

| 40 | 11 | 0 | 6,25,000 | 0 | 6,25,000 |

| 41 | 12 | 0 | 6,25,000 | 0 | 6,25,000 |

| 42 | 13 | 0 | 6,25,000 | 0 | 6,25,000 |

| 43 | 14 | 0 | 6,25,000 | 0 | 6,25,000 |

| 44 | 15 | 0 | 6,25,000 | 0 | 6,25,000 |

| 45 | 16 | 0 | 6,25,000 | 0 | 6,25,000 |

| 46 | 17 | 0 | 6,25,000 | 0 | 6,25,000 |

| 47 | 18 | 0 | 6,25,000 | 0 | 6,25,000 |

| 48 | 19 | 0 | 6,25,000 | 0 | 6,25,000 |

| 49 | 20 | 0 | 6,25,000 | 0 | 6,25,000 |

| 50 | 9,19,494 | 19,39,092 | |||

| IRR | 3.09% | 7.01% | |||

At 4% assumed return: Fund value is ₹9.19 lakh, giving an IRR of 3.09% as per the Pramerica Life Wealth Enhancer Plan maturity calculator — practically no wealth creation, as returns are extremely low.

At 8% assumed return: Fund value rises to ₹19.39 lakh, with an IRR of 7.01% as per the Pramerica Life Wealth Enhancer Plan maturity calculator — still lower than typical debt instruments, highlighting limited growth potential.

The IRR analysis clearly indicates that the Pramerica Life Wealth Enhancer plan delivers minimal real returns, which can hinder long-term wealth accumulation.

For a lump-sum investment, there are far superior options that offer better returns and greater flexibility.

Pramerica Life Wealth Enhancer Vs. Other Investments

Now, let’s compare the Pramerica Life Wealth Enhancer Plan with an alternative investment strategy, using the same assumptions from the Pramerica Life Wealth Enhancer Plan policy illustration.

The goal is to address both life cover and wealth creation through separate, more efficient products.

Pramerica Life Wealth Enhancer Vs. Pure-term + Equity Mutual Fund

A pure-term life insurance policy with ₹6.5 lakh coverage for 20 years can be bought for a single premium of ₹31,300.

This leaves ₹4.68 lakh available for investment. Depending on risk preference, this amount can be allocated to either debt or equity instruments.

| Pure Term Life Insurance Policy | |

| Sum Assured | ₹ 6,50,000 |

| Policy Term | 20 years |

| Premium Paying Term | Single Pay |

| Annualised Premium | ₹ 31,300 |

| Investment | ₹ 4,68,700 |

Low-risk investors can choose fixed-income or debt products.

Growth-oriented investors can invest in Equity Mutual Funds.

Assuming the ₹4.68 lakh is invested in an Equity Mutual Fund, over 20 years, the pre-tax maturity value grows to ₹45.21 lakh. After accounting for long-term capital gains tax, the post-tax value is ₹40.30 lakh.

| Term insurance + Equity Mutual Fund | |||

| Age | Year | Term Insurance premium + Equity Mutual Fund | Death benefit |

| 30 | 1 | -5,00,000 | 6,50,000 |

| 31 | 2 | 0 | 6,50,000 |

| 32 | 3 | 0 | 6,50,000 |

| 33 | 4 | 0 | 6,50,000 |

| 34 | 5 | 0 | 6,50,000 |

| 35 | 6 | 0 | 6,50,000 |

| 36 | 7 | 0 | 6,50,000 |

| 37 | 8 | 0 | 6,50,000 |

| 38 | 9 | 0 | 6,50,000 |

| 39 | 10 | 0 | 6,50,000 |

| 40 | 11 | 0 | 6,50,000 |

| 41 | 12 | 0 | 6,50,000 |

| 42 | 13 | 0 | 6,50,000 |

| 43 | 14 | 0 | 6,50,000 |

| 44 | 15 | 0 | 6,50,000 |

| 45 | 16 | 0 | 6,50,000 |

| 46 | 17 | 0 | 6,50,000 |

| 47 | 18 | 0 | 6,50,000 |

| 48 | 19 | 0 | 6,50,000 |

| 49 | 20 | 0 | 6,50,000 |

| 50 | 40,30,278 | ||

| IRR | 11.00% | ||

| Equity Mutual Fund Tax Calculation | |

| Maturity value after 20 years | 45,21,218 |

| Purchase price | 4,68,700 |

| Long-Term Capital Gains | 40,52,518 |

| Exemption limit | 1,25,000 |

| Taxable LTCG | 39,27,518 |

| Tax paid on LTCG | 4,90,940 |

| Maturity value after tax | 40,30,278 |

The combined post-tax IRR (from both the Equity Mutual Fund and term insurance) comes to 11%, which is significantly higher than the IRR offered by the Pramerica Life Wealth Enhancer Plan.

This alternative approach provides higher returns, better liquidity, and more efficient wealth creation, areas where the Pramerica Life Wealth Enhancer Plan falls short.

Final Verdict on the Pramerica Life Wealth Enhancer

The Pramerica Life Wealth Enhancer is a single-premium ULIP plan with two options:

- Plan Option A provides a death benefit of 10× the premium.

- Plan Option B offers a death benefit of 1.25× or 1.10× the premium.

Both options provide the fund value at maturity, including wealth boosters and additions, but the plan lacks any distinctive or standout features and it also has a high agent commission.

In terms of returns, the plan is not impressive for long-term wealth creation.

Charges are deducted from your premium, and some continue throughout the Pramerica Life Wealth Enhancer Plan policy term, which hampers corpus growth. Despite its name, the plan does not effectively enhance wealth.

Additionally, the sum assured is inadequate for securing a family’s financial needs.

A pure-term life insurance policy, by contrast, provides much higher coverage at a fraction of the cost, freeing up funds to invest in high-growth instruments like mutual funds or other market-linked products aligned with your risk profile.

Do Quora, Facebook, and Twitter have the final say when it comes to financial advice?

By selecting the right investment avenues—ideally with guidance from a trusted financial advisor—you can achieve your financial goals more efficiently and with greater confidence.

Leave a Reply