“There are decades where nothing happens, and there are weeks where decades happen.” – Lenin

That’s how the stock market crash was in March 2023. The Sensex has crashed from a peak of 41952 to 25981.

Steep & quick fall of 38%!

Resulted in panic, negativity and pessimism!

Fear and short-term thinking take over the market during these kinds of times. Perceived Risk goes up.

Table of Content:

- Questions to Ponder over

- Will we recover from this stock market crash?

- Make your Portfolio Recover Better & Faster

- A Powerful & Proven Strategy: Portfolio Optimisation

- Is it ok to Redeem & Reinvest now?

- Do I need to do this revamp NOW – during this crisis?

- A Bonus Benefit of Doing Portfolio Optimisation NOW

- Tips to Identify Poor-performing Equity Funds

- Conclusion

Questions to Ponder over

- Is this the first time, the stock market has crashed like this?

- Will this be the last time?

- Real Risk Vs Perceived Risk. – Which is higher now?

- Does the market’s overreaction lay a strong foundation for above-average returns in the future?

Also read, Stock Market Crash!!! What’s Your First Priority?

Will we recover from this stock market crash?

Do you think, next year by this time, we will have better pandemic control?

Do you think, next year by this time, all our offices will be open and functioning?

Do you think, next year by this time, we will have a more stable economy?

Volatility always gives way to tranquillity. Chaos gives birth to dancing stars.

This crisis too shall pass. This crisis will eventually remake the business world into wiser, stronger and more creative. The economy will become better than before. What’s coming for the stock market in the long-term will be amazing.

“Although the world is full of suffering, it is also full of the overcoming of it.” –Helen Keller

Instead of focusing on the suffering situation, let us focus on the overcoming of it.

Make your Portfolio Recover Better & Faster

When will the stock market recover? It depends on so many variables and all of them are outside your control.

How fast will your portfolio recover when the market recovers? It depends on only one variable and it is COMPLETELY under your control.

It depends on the performance of your individual portfolio. It depends on what do you own in your portfolio. Do you own below-average performing investments or above-average performing investments?

If you own poor-performing investment, it may not recover or it may recover slower and may take longer time to recover than the better performing investment.

A Powerful & Proven Strategy: Portfolio Optimisation

Portfolio optimization is a strategy by which you redeem your below-average investments and reinvest the redemption proceeds in above-average investments.

Cut the weeds and water the flowers. This looks like a simple strategy but it is very sound and profound.

Is it ok to Redeem & Reinvest now?

When the stock market is down, is it ok to redeem now? Are we not booking a loss? Is it required?

This strategy is not suggesting you come out of your equity investments. It is just making you come out of poor-performing equity investments and reinvest it in better-performing equity investments. This strategy helps you recover faster when the market recovers.

Also watch the video here!

Do I need to do this revamp NOW – during this crisis?

The stock market is volatile because of the prevailing abnormal situation. When normality sets in, there is a high likelihood of market recovery. When the market recovers, if you want your portfolio also to recover then you need to come out of your poor-performing investments NOW. It is better to do this when still the abnormality prevails.

Is there a proof for this? How is this strategy faired during earlier Crises?

The stock market has faced two major crashes. One is in 2000 and the other is in 2008 which were much worse than the 2023 crash. The market crashed by 53% in 2000 and by 61% in 2008.

Let us check how an investor could have benefitted if he implemented this portfolio optimization during those crises.

Assume an investor has invested in 3 equity funds Rs 1 Lac each in the year 2000 before the market crash. Let us see what would have been the impact because of the market crash.

Without doing, portfolio optimization, if the investor decided to continue to stay invested in these below-average performing schemes, then let us see how the recovery would be in 2003.

Without doing, portfolio optimization, if the investor decided to continue to stay invested in these below-average performing schemes, then let us see how the recovery would be in 2003.

Read, If Portfolio Optimization Promises Outstanding Returns, Wouldn’t You Take It

Yes. There seems to be some recovery. Is this recovery sufficient? Is this a slow recovery? If the investor could have done portfolio optimization with the help of a professional financial planner and moved out of poor-performing schemes and reinvested the money in better performing schemes, his portfolio could have recovered better and faster.

Yes. There seems to be some recovery. Is this recovery sufficient? Is this a slow recovery? If the investor could have done portfolio optimization with the help of a professional financial planner and moved out of poor-performing schemes and reinvested the money in better performing schemes, his portfolio could have recovered better and faster.

That is in the above case if he could have redeemed Rs. 157870 from those poor-performers on 21.9.2001 and reinvested the same in better-performers, let us see, how the recovery could have been.

Recovery is significantly more in the above case because of portfolio optimization.

Recovery is significantly more in the above case because of portfolio optimization.

Let us do one more experiment like the above for the 2008 crisis.

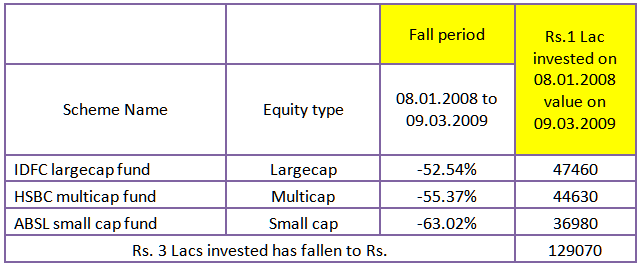

Imagine an investor has invested in 3 equity funds Rs 1 Lac each in the year 2008 before the market crash. Let us see what would have been the impact because of the market crash.

Without doing, portfolio optimization, if the investor decided to continue to stay invested in these below-average performing schemes, then let us see how the recovery will be in 2010.

Without doing, portfolio optimization, if the investor decided to continue to stay invested in these below-average performing schemes, then let us see how the recovery will be in 2010.

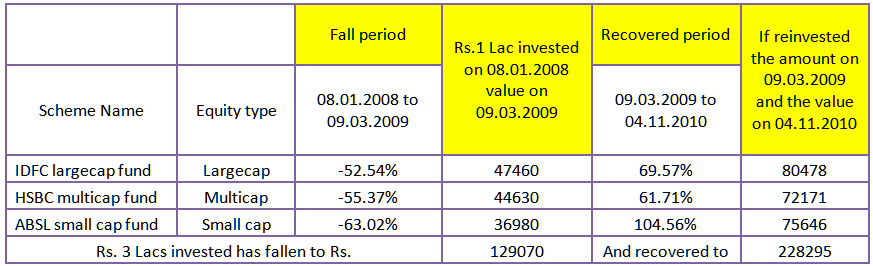

Though there is some recovery, it is very slow. Let us see, how the recovery gets faster when the portfolio optimization strategy is used by withdrawing from the above poor performers and reinvesting in the below better performers.

Though there is some recovery, it is very slow. Let us see, how the recovery gets faster when the portfolio optimization strategy is used by withdrawing from the above poor performers and reinvesting in the below better performers.

The recovery is much better because of portfolio optimization.

The recovery is much better because of portfolio optimization.

So, redeeming your non-performing equity investments and reinvesting the same in a better performing equity investment will deliver remarkable results for you.

Optimize Beyond Equity Mutual Funds:

The majority of investment portfolios are not limited to having equity mutual fund investments alone.

Investment insurance plans lock up a good portion of corpus only to give very poor returns even in long-term. It includes both the endowment insurance plans and the ULIPs.

Get Rid of your Endowment Plans:

It is not a surprise, endowment plans earn poor returns.

If an investment is giving returns around just 4%-5%, an investor must not have such products in their portfolio.

Surrender your endowment insurance plans at the first opportunity you get to enable your faster portfolio recovery.

Poor returns aside, with endowment insurances in the context, they give a false idea that ULIP are better investments—which they are not.

Get Rid of Your ULIPs, Too:

ULIPs are the investments that perform poorer than poor performing equity mutual funds, even in their best days.

I.e. 6%-8% return at their best. But the tricky part is, since ULIPs invest in equities too, this stock market crash has affected their returns too.

Post crash, the returns from ULIP investments will be lesser than the usual 6%-8%. It is a trademark poor investment that should be removed from a portfolio.

Read: Unpleasant Facts About Investing in Insurance Plans

Now that you are optimizing your portfolio for faster recovery from the stock market crash, it is more than a good reason to get back these insurance investments.

Surrender all your endowment insurance plans and ULIPs at the first opportunity you get to do justice to your investments.

This strategy to work effectively, you need to act fast and do the portfolio optimization before the market recovers.

A Bonus Benefit of Doing Portfolio Optimisation NOW

Apart from faster and better recovery, there is one more advantage of doing portfolio optimization now – during the crisis. You will have a lesser tax liability if you do the portfolio revamp now compared to doing it after recovery.

Because of the market crash, as the portfolio value has come down, if you do the revamp now the profit booked will be less. So there will be a lesser tax liability. If you do the revamp after the market recovery, then the tax liability will be more.

Let me explain this with an example.

If someone has invested Rs. 10 lacs in 2017 and the portfolio value reached Rs 15 Lacs on Jan 2023 and the value has come down to Rs.12 lacs in March 2023 because of the market crash.

If they revamp their portfolio now (2023), the taxable gain is only 2 lacs. There is a possibility that it may recover in 2-3 years to 15 lacs.

Instead of revamping their portfolio now, and they wait for the market to recover to do the revamp. As it is a poor performing scheme it will perform lesser than the revamped portfolio and reach 15 lacs after 3-4 years. If you do the revamp after the recovery / after 3-4 years, then the taxable gain is 5 lacs.

The tax liability is lower if you do the portfolio revamp now.

Also read, COVID-19 Vs. INSURANCE CLAIM: Is Your Insurance Policy Immune to Corona Virus?

Tips to Identify Poor-performing Equity Funds

1. Check if the fund is outperforming the respective benchmark index or not.

2. Check if the fund is outperforming most of the peer-group funds.

3. Check with your financial advisor for other non-quantitative analytical parameters like,

- The ability of the Mutual Fund company to retain the fund managers

- How evolved is the investment process of the mutual fund company?

- How consistently the mutual fund company follows the chosen investment philosophy?

Conclusion

Dark nights always give way to bright mornings. The biggest opportunity arises out of the worst disasters. Portfolio optimization is a very good opportunity for you to recover better and faster from this stock market crash.

Continue to Part 2:

How To Make Your Portfolio Recover Better & Faster From The Stock Market Crash? (Part 2)

Continue to Part 3:

How To Make Your Portfolio Recover Better & Faster From The Stock Market Crash? (Part 3)

[the_ad id=’13360′]

Informative article.

Thank you

Useful article from Holistic as always . The numbers and the data add up giving much confidence to readers who are looking to optimize MF allocations in these uncertain times.

Thanks Kasi. We are happy that you found it useful 🙂