Being an investor, you already know that stock market crashes are very common.

It wouldn’t take much time for investor to get used to the steep fall.

But this CoronaVirus Crash of 2020 is different.

This article is for all of you investors who believe in disciplined investing and long-term wealth creation. Read to know the impact of Corona Virus Crash on long-term investors.

Table of Contents:

1) Revealing The Investor Behaviours

2) The Ground Reality of Corona Virus Crash 2020

3) Should You Withdraw to Avoid Further Losses?

-

a) How much return are we talking about here?

b) How to Minimize CoronaVirus Crash 2020 Impact?

c) What Can SIP Investors Do?

4) Should You Time the Market Bottom?

5) 3 Useful Tips on How to Recover Faster and Better from the Stock Market Crash

6) Beware of the Wealth Threatening Situations

7) Conclusion

Revealing the Investor Behaviours

Corona virus crash of 2020 revealed the real temperament of investors in India.

By mid March 2020, the gain earned over the past 3-4 years was already lost. The fastest fall ever recorded in the history of Indian markets.

The panic brought out the two contrasting behaviours among investors.

There are investors who completely rely on the process and the plan. They have seen the turbulences and crashes and learned from them.

These investors have understood the basics and religiously follow it, knowing that every crash will be followed by a recovery.

On the other hand are the Investors who didn’t quite get the opportunities to learn the same way.

Global level panic distracted them from the basics. And in no time, fear took over their decision making process.

In the midst of a chaos, they forgot that no investor should withdraw during a crash.

Which side do you identify with the most?

Or do you feel like you are caught up in the middle?

Are you confused which is the right strategy to follow?

This is your moment to find answers to these questions.

The Ground Reality of CoronaVirus Crash 2020:

We shall jump straight to happenings and investor behaviours.

From stopping their SIPs to withdrawing their entire equity investments, investors are following different unguided panic strategies. I call it,

The Panic Impulses:

-

i) Withdraw To Avoid Further Losses

ii) Try and Time The Market Bottom

If you are intending to implement any of these strategies to your investment plan read this analysis before you do.

We can show you what will be its impact on an investor’s investment plan.

Here’s the analysis and debunking of these “strategies”, along with what you can do as the best solution.

Panic Impulse1: Should You Withdraw to Avoid Further Losses?

The very first panic impulse is to get out of investments that bring you loss.

Hence, withdrawing at this time would only seem like a rational decision.

But is this the right strategy to follow? Will this strategy work for the benefit of the investors?

See what the numbers say.

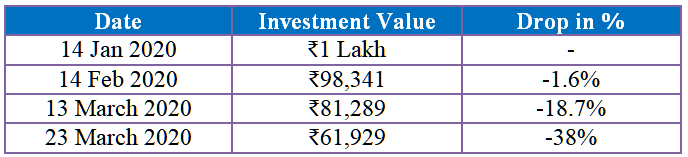

Let’s say you had an investment with a value of ₹1 lakh as on 14 Jan 2020.

At this rate anyone would be convinced to withdraw their investments and save what is left. Losing 38% of your investments in a couple of months is too much.

At this rate anyone would be convinced to withdraw their investments and save what is left. Losing 38% of your investments in a couple of months is too much.

But every investor—experienced or amateur—should remind themselves that this fall is not permanent. Even the records support it. I’ll present you the historical data below.

For example: Franklin India Bluechip Fund was launched on 1st Dec 1993. Rs. 1 lakh invested then would have had a value of Rs.84.98 lakhs in March 2020, at 18.44% CAGR.

Those 26 years had innumerable panic like situations; both domestically and globally. But those who sat out the crisis patiently were hugely rewarded. Indian markets have given around 84 times returns over the last 2.5 decades when both globally and locally we went through one crisis after another.

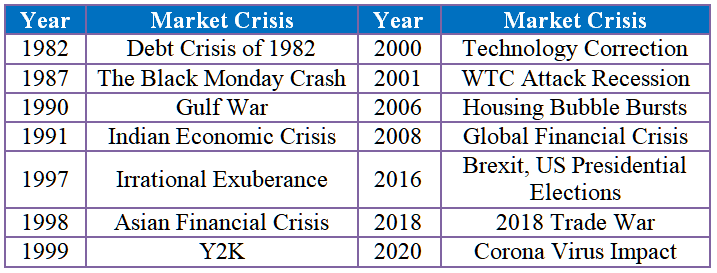

Here is some notable crisis the market suffered in the past 4 decades:

Do you know what all of these and all other economic crises have in common?

Markets recovered from all of them—rewarding those who stayed invested through the process. See the image below.

The image above shows some of the prominent market crashes and the subsequent recoveries in the past. And anyone who stayed invested was rewarded by the market earnings remarkably.

How much return are we talking about here?

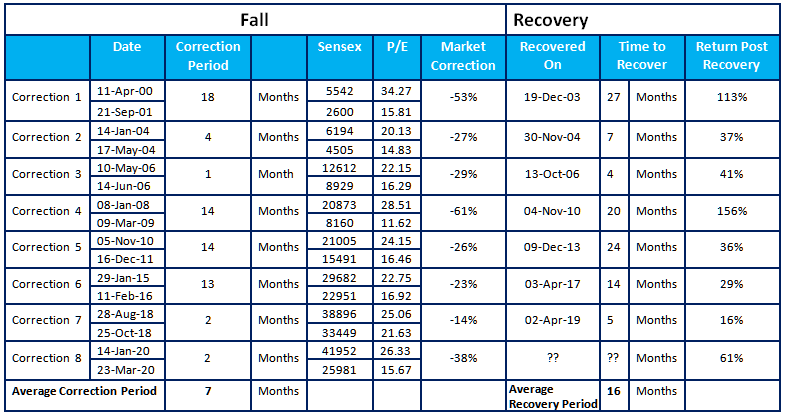

We have the recorded data of recovery from all the past market crashes.

Of all these, two incidents were the worst there is—The Dot Com Bubble Burst of 2000 and the Global Financial Crisis of 2008.

See the table below for the after-effects of these two worst crashes in recorded history.

In the long –term every notion about the stock market crashes change diametrically.

In the long –term every notion about the stock market crashes change diametrically.

17.14% and 21.8% CAGR for the next 5 years span. And this is only the BSE Sensex index return. There are actively managed Equity Mutual Funds that perform consistently way better than the index.

The overlooked fact you have to keep in mind is that as long as you don’t withdraw, it is only a drop in investment value. But the moment you withdraw your investments, the drop in value will become a permanent loss.

For example: In the 2008 Global Financial Crisis, investors who had withdrawn their investments during the 15 months drop would have never recovered the loss incurred. They also missed out on the 21.8% CAGR that followed for the next 5 years.

Now, do you think withdrawing your investments in panic can save investments?

It not only causes permanent damage to your portfolio, but also takes away the growth opportunity that follows every market crash.

How to Minimize CoronaVirus Crash 2020 Impact?

More than “how-to”, the most important question is, should you?

During these volatile times, your equity investments are much like a wet painting. The more your touch it, the worse it is going to get.

I presume you made these investments as per your investment plan. Or you may have invested as suggested by your investment advisor. Just as seen in the analysis above, every crash is followed by a recovery. They come as a package.

Stick to your investment plan. Do what you would have done if everything was normal, unless your investment advisor says different.

What Can SIP Investors Do?

Continuing your SIP is the effective solution.

The very purpose of investing through SIPs is to take advantage of Rupee Cost Averaging.

Through SIP’s Rupee Cost Averaging, you buy less number of units during the bull phase. It is averaged out only during times such as these.

Take a look at your investment fund portfolio, ignore the investment value but look at the NAV of your fund. The 38% fall is not a loss but an offer price for your upcoming SIP unit purchases.

Follow your investment plan. Be consistent.

Also, watch the video here!

Panic Impulse2: Should You Time the Market Bottom?

Timing the market bottom is an attempt to outsmart the market.

Although not everyone is as ignorant to follow this “strategy”; a good number of investors still believe it will save them from fall.

The Idea behind Strategy: Their idea is to stop all their SIPs and STPs—some even withdraw their equity investments. They wait for the market to hit rock bottom before they enter the equity investments again.

This way, investors hope to avoid the fall of the market and only get the recovery rise benefits.

On paper, it is a brilliant strategy. But unless you are a time traveller, there is no way you can know the bottom. It is because market bottom is not a pre-defined line.

No industry expert or any Supercomputer or AI can predict it either.

For example: Sensex may lose 1000 points today, gain 1500 in the next two days and then go on to lose 4000 points in the following 5 days.

Which one do you think is the bottom?

Market is never linear. It’s a gamble to time the market. And you cannot just gamble away your investments when a solid plan works better.

Timing the market may work in one in million or billion times.

Would you bet against these impossible odds?

There is no way any investor or expert can outsmart the market. However, you can always work with the market and this situation to get the best out of your investments.

Learn To Work With The Market:

Businesses have to stay afloat and they’ll do anything in their power to keep it up and running.

During crisis such as these, the market will be in dire need of capital. It is now investors will be getting the best value for their investments.

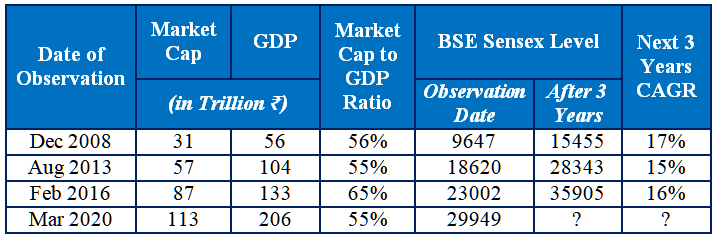

See the table below.

Events shown in the table are some of the worst market crashes in the recent past.

Events shown in the table are some of the worst market crashes in the recent past.

For example: Let’s take the Global Financial Crisis of 2008 from the table. Back then, the Market Cap to GDP ratio was only 56%.

If this ratio is 100%, it is ideal. Any purchase you make is fair value for investment. But when it is lesser than 100%, it signifies the market is under-valued.

In simple terms, the lesser the ratio is, the more value you get for the purchases. The return earned in the following 3 years proves the same.

After the 2008 crash, the investors who stayed invested earned a 17% CAGR.

Again, this is only for the BSE Sensex index. Any time-tested actively managed equity Mutual Fund would have earned much more than the index.

You can expect the same after the Corona Virus Crash 2020, too. It may not happen precisely in the same way, but a recovery is certain.

Qualify for the Recovery & Reward:

Forget about timing the market

Be on the winning side during the recovery from this crash—DO NOT WITHDRAW OR STOP your investments.

Instead, increase your investment rate gradually.

Even if you receive any sort of Lumpsum amount, buy additional units in your existing equity mutual fund scheme. Rather than investing it all in one go, invest it in parts over the next few months.

For example: Say you are receiving ₹2 lakhs cash from somewhere as lump sum. You can invest it in equal parts over the next 4 months or 6 months in your existing equity mutual fund scheme.

It is the best way to do it when the market is volatile.

If there is anything that would get you the best value for money, it would be these equity units.

Accumulate equity units in your existing best mutual fund scheme. The units you accumulate now will accumulate the wealth for you when the bull returns.

3 Useful Tips on How to Recover Faster and Better from the Stock Market Crash

Due to the recent fall in the Stock market, many of you might be keen on finding ways to save your portfolio from the stock market crash. Here are the best ways for you to recover your portfolio faster and better from the stock market crash.

1. Does a portfolio revamp help?

Yes, absolutely. A portfolio revamp helps you recover faster and better from the stock market crash.

It is done by moving your funds from poor-performing into better-performing. This is called as portfolio optimization.

Experiments were conducted on past data and a revamp did work. One more appropriate thing to do is to get rid of your endowment plans and ULIP’s and invest in best performing mutual funds.

Do you think … is there a need to redeem and reinvest now? To know more read: How to revamp for faster and better results. (With this link also find a bonus benefit of doing portfolio optimization, and tips to find poor performing funds).

2. Is a portfolio rebalance needed during the stock market crash?

Yes, a portfolio rebalancing can help during the stock market crash. Head start portfolio recovery by rebalancing. After a stock market crash, the asset allocation would have changed. Then you are supposed to bring it back to the original asset allocation. This is portfolio rebalance. This will also help you recover faster and better from the Stock market crash.

Read: How portfolio rebalance is done (with this link find the steps to rebalance your portfolio, also download a free portfolio rebalancing tool).

3. What are you supposed to do with your SIP now?

You have three options left to you. Either to stop, continue, or increase your SIP.

We did two experiments with three different investors, each of them who chose one among the following options. One chose to stop SIP, another to continue SIP and another to increase SIP (all during the market fall).

Among these who do you think earned the highest portfolio value?

In both the experiments, it was the one who opted to increase his SIP during the market fall, earning the highest portfolio value.

What happens if you stop, continue, or increase SIP?

If you stop SIP, you will recover slower.

If you continue SIP, you will gain better than if you stop them.

If you increase SIP, you will gain much better than if you stop or continue it.

Hence increasing your SIP will help you recover faster and better from the stock market crash.

For more information, read: How to play smart with your SIP.?

Beware of the Wealth Threatening Situations

Fear is deep-rooted in the sub-conscious; and is difficult to overcome.

Even with rational explanations and evidences shown above, you may try to convince yourself to do otherwise.

Especially when you have a financial goal or a financial need, you will be tempted the most to withdraw your equity investments.

After all you will have a legitimate reason to withdraw. You’re not withdrawing out of panic and fear. But that is not true.

If you indeed have an unavoidable financial need, or having a cash crunch, handle them wisely. In such times, you can,

- Use your Debt Investments

- Use your Emergency Fund

- For EMIs: Request lender to hold payments temporarily

These measures can help you pass the rough tides. It is safer this way without compromising on your long-term wealth creation process.

Conclusion

The COVID-19 outbreak and the subsequent market crash is a crisis indeed.

It may sound banal, but it is true that crises are doorways to opportunities.

You have two choices: you can give in to your fear and regret the missed opportunity later.

Or you can choose trust the process and endure this storm.

Anyone who succumbed to panic selling will make their loss permanent. But those who endured go on to realize their financial goals faster.

Keep a calm head. Trust the time-tested process. Be resilient.

At any time, if you want to make any change to your investment plan, seek your investment advisor’s help first.

Leave a Reply