The SBI Life Retire Smart is a Unit Linked Insurance Plan (ULIP) designed to be a pension plan.

It invests your insurance premium in equities and other debt-oriented funds managed by SBI Life (different from SBI Mutual Fund).

And being a pension plan, it allows you to get the maturity benefits in the form of an annuity. I.e., a periodic pay-out in retirement as a source of income—in other words, a pension.

Is this retirement plan a good or bad investment for your future?

We are going to analyze the fund performance & fund value.

More importantly, does it give the promised returns mentioned in the brochure or bank relationship manager or insurance agent?

Do the pros outweigh the cons or is it the other way around?

Let’s get started!

Table Of Content

1.) Key Features of SBI Life Retire Smart Plan

2.) SBI Life Retire Smart Plan Fund Options

3.) SBI Life Retire Smart Advantage Plan Review

4.) SBI Life Retire Smart Plan Death Benefits Review

5.) SBI Retire Smart Review of Maturity Benefits

- Maturity value is 101% of total premiums paid

- If the policy generates an annual return of 4%

- If the policy generates an annual return of 8%

6.) Comparison Review of SBI Life Retire Smart vs. PPF

7.) Comparison Review of SBI Life Retire Smart vs. ELSS Fund

8.) Verdict

9.) How to Surrender Your SBI Retire Smart Plan?

10. Key Risks Investors Should Understand Before Buying Pension ULIPs

11.) Conclusion

The SBI Life Retire Smart Plan is primarily marketed for people working in jobs that do not provide a pension plan in retirement.

It is positioned as a market-linked retirement solution that aims to help individuals build a pension corpus through long-term disciplined investing.

As mentioned in the policy document, such retirement planning has become even more important because of the increased life expectancy.

With rising longevity, many investors explore retirement products such as the SBI Life Retire Smart Plus plan and other SBI pension plans to secure income after retirement.

Retirement planning should not be neglected—it is true.

But can this SBI Life Retire Smart Plan be a reliable retirement plan for you?

Many investors also compare the SBI Life Retire Smart Plus returns, maturity benefits, and fund performance before deciding whether this retirement plan fits their financial goals.

Shouldn’t you understand this policy inside out before making such a big decision?

This SBI Life Retire Smart Plan review will help you analyze, understand, and make the right and reliable financial decision.

Let’s start with…

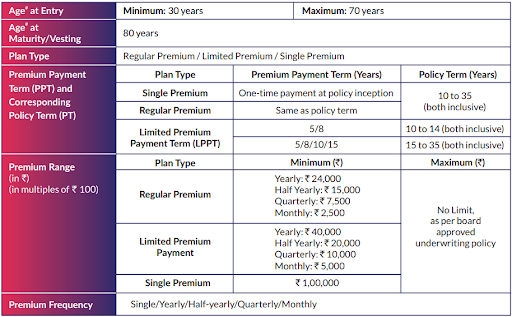

1.) Key Features of SBI Life Retire Smart Plan:

Since this ULIP is meant to be a retirement plan, its policy features are also quite different from the conventional ULIPs.

The table below shows the key features of the SBI Life Retire Smart plan.

Investors evaluating the SBI Life Retire Smart Plus plan details often focus on factors such as policy term, premium payment options, maturity benefits, and pension conversion features.

Let’s figure out how this policy works with an example.

Suppose you buy this policy. You are now 35 years of age.

And you’re choosing the 25 years’ policy term with a regular premium—you’ll pay the policy premium throughout the policy term. Your annual premium is ₹1,00,000.

You will pay ₹1,00,000 annually for the next 25 years.

Many retirement calculators such as the SBI Life Retire Smart maturity calculator or retirement planning tools help investors estimate the potential corpus they may accumulate over the policy term.

This amount, of the Retire Smart Plan will invest across the 3 different funds of this policy. Before we proceed with the example, here are the fund options of the SBI Life Retire Smart Plan.

To calculate your premium for this plan, click below.

SBI Life Retire Plan Premium Calculator.

Online tools like the SBI Retire Smart Plus calculator help investors estimate premium commitments and expected maturity values based on different assumptions.

2.) SBI Life Retire Smart Plan Fund Options:

The SBI Life Retire Smart plan offers pension-oriented funds designed to gradually shift asset allocation as the investor approaches retirement age.

Since this is a product made as a retirement plan, you cannot choose a fund of your choice.

Instead, your policy will follow a predefined investment strategy. Named the “Advantage Plan”, this investment strategy employs a varying asset allocation.

These retirement funds typically include equity pension funds, bond pension funds, and money market pension funds to balance growth and stability.

3.) SBI Life Retire Smart Advantage Plan Review:

It is not new for a ULIP policy to follow a predefined asset allocation strategy and restrict investor flexibility.

Even though a predefined strategy may suit a majority of investors, it does not necessarily suit every investor’s needs.

This “Advantage Plan” investment strategy spreads your premium across the available fund based on the number of years till your policy maturity.

The table below shows how the SBI Life Retire Smart Advantage Plan works.

The strategy follows a lifecycle investment approach where equity exposure reduces gradually as the retirement date approaches.

We have calculated the percentages of fund allocation under different funds like equity pension fund II, bond pension fund II, and money market pension fund II.

The idea behind this investment strategy is that, in the early years, more allocation is given towards the high-risk high-return equity fund.

And as you near the policy maturity, your fund value is reallocated to minimize risk and bring more stability to your fund value.

Such lifecycle strategies are commonly used in retirement planning products to reduce market volatility near retirement.

Now that we have seen how this Retire Smart Plan invests your premium, let’s take a look at the benefits of this policy.

If you want to find your SBI Life policy status. Click below.

4.) SBI Life Retire Smart Plan Death Benefits Review:

The SBI Life Retire Smart Plan will pay the death benefit to the nominee in case of the policyholder’s death.

It is on one condition that their Retire Smart Plan is in force at the time of death.

The Death Benefit of the SBI Life Smart Retirement Plan will be the highest of,

- Fund Value + Terminal Addition (or)

- 105% of the Total Premiums Paid

Terminal Addition: 1.5% of the fund value on date.

The death benefit structure is similar to many ULIP retirement plans where the fund value forms the primary pay-out component.

While this is the eligible death benefit, the nominee also has the option to choose how they want to utilize the death benefit. The two options are,

- Receive the Death Benefit as a lump sum (or)

- Purchase Annuity with a part of or the entire Death Benefit amount.

In many retirement plans, purchasing an annuity ensures the nominee receives a steady pension income instead of a one-time pay-out.

When it comes to purchasing an Annuity, the nominee can choose to buy it from SBI Life or any other life insurance company of their choice. However, the nominee can use only up to 50% of the proceeds to buy an annuity from a different insurer as per IRDAI regulation.

(NAV (Net Asset Value) as of 05-Jun-2023: Rs 31.1988 approx.)

Investors often track the NAV of SBI Life Retire Smart funds to evaluate the historical performance of the underlying pension funds.

Even though the SBI Life Retire Smart Plan is an insurance-cum-investment policy, it does not offer any Sum Assured as Death Benefit.

Hence, in any worst-case scenario, your nominee is likely to receive 105% of the premiums paid.

For a life insurance policy and considering risk management, it is totally worthless. In fact, the risk cover is practically non-existent.

Let’s find out what this ULIP can offer as a maturity benefit.

5.) SBI Retire Smart Review of Maturity Benefits:

We shall take the same example seen earlier.

SBI Life Retire Smart Plan with 25 years’ policy term and ₹1 lakh annual premium—with a regular premium payment term.

Your SBI Retire Smart Plan maturity benefit will be the highest of the:

- Fund Value on Maturity + Terminal Addition (or)

- 101% of total premiums paid

Terminal Addition: 1.5% of the fund value on date.

The maturity benefit in ULIP retirement plans depends largely on the long-term performance of the underlying investment funds.

We have seen that the SBI Life Retire Smart invests in equities as well. Therefore, there is no capital or return guarantee on those investments.

But the policy guarantees you will receive 101% of total premiums paid, on maturity. Hence, it is more or less a promise of capital guarantee by the SBI Life Retire Smart Plan.

However, you should note that the minimum policy term of the Retire Smart Plan is 10 years. And it is proven that in the long term, equity investments provide good capital appreciation and the capital risk is extremely low.

Hence the 101% of the premiums paid as a maturity benefit is simply an empty reassurance from the product sellers.

That being said, you only have 3 options to utilize your maturity benefit. They are,

- Buy an Annuity with the entire maturity amount

- Take up to 60% of your maturity amount as a lump sum at maturity.

The remaining amount can only be used for buying the annuity from SBI Life Retire Smart.

- Or finally, you can choose to extend your policy term.

Retirement plans like SBI Life Retire Smart often require a portion of the maturity corpus to be converted into annuity income after retirement.

SBI Life Retire Smart policy gives you the option to use your maturity amount to buy annuities from any other insurer if you do not want to buy an annuity from SBI Life.

Calculate which SBI retirement plan suits the best for you by clicking below:

Discontinuance of Premium in SBI Retire Smart Plan:

If the premium is discontinued during the first five policy years then:

Your fund value as of that date will be disinvested and credited to the discontinued policy pension fund net of the relevant discontinuance charge.

Policyholders should carefully evaluate the surrender and discontinuance rules before committing to long-term retirement ULIP plans.

Analysis of SBI Retire Smart Plan Maturity Returns:

Internal Rate of Return (IRR) is the effective annual rate of return that you will get if you buy the SBI Life Retire Smart policy.

IRR analysis helps investors understand the real return after considering premium payments and the final maturity value.

The maturity value is 101% of total premiums paid:

The minimum guaranteed value under this policy is 101% of the total premium paid.

You will get this maturity benefit in case the premiums that were invested by SBI Life Retire Smart end up giving a return less than this guaranteed amount.

From the table below you can see that the annual return you will get is .076%.

But there is a catch. In reality, you will be making less than this annual rate of return.

This is because premium allocation charges and policy administration charges will also be levied on you each year.

After deducting these charges, the annual return that you will make will be less than even .076%.

The premium allocation charge will be between 2.5% and 5.75% during your premium payment period.

The policy administration charge will be between Rs 25 and Rs 75 per month.

Charges such as premium allocation fees, policy administration fees, and fund management costs can significantly impact long-term returns.

If the policy generates an annual return of 4%:

The policy brochure of the SBI Life Retire Smart policy assumes that the investments of your premiums in their funds are likely to generate an annual return of between 4% and 8%.

If the policy generates a 4% annual return, then as per the calculation shown below you will realize an annual rate of return of 2.46%.

Again, after factoring in the premium allocation charges and policy administration charges you will realize an annual rate of return of less than 2.46%.

|

At 4% p.a. |

|

|

Year |

Annualised premium / Maturity benefit |

|

1 |

-1,00,000 |

|

2 |

-1,00,000 |

|

3 |

-1,00,000 |

|

4 |

-1,00,000 |

|

5 |

-1,00,000 |

|

6 |

-1,00,000 |

|

7 |

-1,00,000 |

|

8 |

-1,00,000 |

|

9 |

-1,00,000 |

|

10 |

-1,00,000 |

|

11 |

-1,00,000 |

|

12 |

-1,00,000 |

|

13 |

-1,00,000 |

|

14 |

-1,00,000 |

|

15 |

-1,00,000 |

|

16 |

-1,00,000 |

|

17 |

-1,00,000 |

|

18 |

-1,00,000 |

|

19 |

-1,00,000 |

|

20 |

-1,00,000 |

|

21 |

-1,00,000 |

|

22 |

-1,00,000 |

|

23 |

-1,00,000 |

|

24 |

-1,00,000 |

|

25 |

-1,00,000 |

|

34,82,678 |

|

|

IRR |

2.46% |

Moderate market performance scenarios often highlight how charges affect the final retirement corpus in ULIP plans.

If the policy generates an annual return of 8%:

If the policy generates a rate of return of 8% annually, as per the calculation shown below, you will realize an annual rate of return of 6.29%.

|

At 8% p.a. |

|

|

Year |

Annualised premium / Maturity benefit |

|

1 |

-1,00,000 |

|

2 |

-1,00,000 |

|

3 |

-1,00,000 |

|

4 |

-1,00,000 |

|

5 |

-1,00,000 |

|

6 |

-1,00,000 |

|

7 |

-1,00,000 |

|

8 |

-1,00,000 |

|

9 |

-1,00,000 |

|

10 |

-1,00,000 |

|

11 |

-1,00,000 |

|

12 |

-1,00,000 |

|

13 |

-1,00,000 |

|

14 |

-1,00,000 |

|

15 |

-1,00,000 |

|

16 |

-1,00,000 |

|

17 |

-1,00,000 |

|

18 |

-1,00,000 |

|

19 |

-1,00,000 |

|

20 |

-1,00,000 |

|

21 |

-1,00,000 |

|

22 |

-1,00,000 |

|

23 |

-1,00,000 |

|

24 |

-1,00,000 |

|

25 |

-1,00,000 |

|

60,75,270 |

|

|

IRR |

6.29% |

After the deduction of premium allocation charges and fund administration charges, you will realize an annual return of less than 6.29%.

While 6.29% is not too bad, but if we consider 25 years and the equity risk, it is not a good choice.

Investors comparing retirement plans often analyze whether the risk-adjusted return justifies the long lock-in period.

It will be nice if someone explains all the aspects such as fund performance, surrender value, interest rate, tax benefit, premium payment, and more importantly the pros and cons in a video with a step-by-step explanation and calculation, right?

Do you want to see whether this plan is good or bad as a YouTube video with an illustration? Click below.

Other Alternative Investment Options For SBI Retire Smart Plan – A Comprehensive Analysis

Before committing to a long-term retirement product, many investors compare multiple SBI retirement plans and pension schemes to understand the risk, return potential, and flexibility offered by each option.

SBI Life Retire Smart vs SBI Life Retire Smart Plus – Review

SBI Life Retire Smart Plus is an Individual, Unit-linked, non-participating Pension Savings Product.

The SBI Life Retire Smart Plus plan is another ULIP-based retirement solution designed to help investors accumulate a pension corpus through diversified investment funds.

This plan has 7 diversified fund options to choose from, which come with different risk-reward ratings to suit the requirements of a variety of investors.

Benefits can be enjoyed in the form of annuities except to the extent of commutation of such benefits as allowed.

Investors evaluating the SBI Life Retire Smart Plus returns and maturity benefits often use the SBI Life Retire Smart Plus calculator or maturity calculator to estimate the potential pension income after retirement.

You can check the official brochure (pdf) below.

The official SBI Life Retire Smart Plus brochure provides detailed information about fund allocation, charges, policy benefits, and annuity options available after maturity.

Read the complete review of SBI Life Retire Smart Plus with precise calculation of the risk level for various funds and IRR (Interest Rate) analysis with the illustration.

Click below for a neutral view of the advantages and disadvantages of this plan.

SBI Life Retire Smart Plus: ULIP Review– Is it Good or Bad?

6.) PPF vs. SBI Life Retire Smart Comparison Review:

Let’s look into an alternative for the SBI Life Retire Smart Policy.

Instead of buying this policy, you choose to invest in Public Provident Fund (PPF) and buy a term insurance plan for life cover.

This investment you do for meeting your income needs after retirement.

The term insurance plan will give you the same insurance coverage that you will get under your SBI Life Retire Smart policy but at a much lesser premium charge.

However, in this calculation, we are not opting for a pure term life insurance policy.

As you get only the fund value or 105% of the premium paid as death benefit under SBI Life Retire Smart Plan, we do not assume for term-plan.

The amount that you save on premium, you can invest in PPF.

The prevailing interest rate for PPF for the 2024-25 Q4 is 7.1% p.a.

PPF is one of the most widely used long-term retirement savings options in India due to its government backing, guaranteed returns, and tax advantages.

So what will be your return if you invest ₹1,00,000 annually for the next 25 years in PPF?

Find out in the table below.

|

PPF |

|

|

Year |

PPF |

|

1 |

-1,00,000 |

|

2 |

-1,00,000 |

|

3 |

-1,00,000 |

|

4 |

-1,00,000 |

|

5 |

-1,00,000 |

|

6 |

-1,00,000 |

|

7 |

-1,00,000 |

|

8 |

-1,00,000 |

|

9 |

-1,00,000 |

|

10 |

-1,00,000 |

|

11 |

-1,00,000 |

|

12 |

-1,00,000 |

|

13 |

-1,00,000 |

|

14 |

-1,00,000 |

|

15 |

-1,00,000 |

|

16 |

-1,00,000 |

|

17 |

-1,00,000 |

|

18 |

-1,00,000 |

|

19 |

-1,00,000 |

|

20 |

-1,00,000 |

|

21 |

-1,00,000 |

|

22 |

-1,00,000 |

|

23 |

-1,00,000 |

|

24 |

-1,00,000 |

|

25 |

-1,00,000 |

|

68,72,010 |

|

|

IRR |

7.10% |

The returns from PPF are guaranteed by the Govt. of India.

And you will be able to withdraw this amount in a lump sum.

This ₹68.7 lakhs can provide you an annual income of 2,56,657.70 (64,16,442/25) for the next 25 years, even if you do not invest it anywhere.

Tax Benefit

Another advantage of PPF is that the investments and the maturity benefits of PPF are completely tax-free u/s 80C of the Income Tax Act.

It has the well-known EEE Tax Exempt status.

The EEE status means contributions, interest earned, and maturity proceeds are all exempt from tax, making PPF one of the most tax-efficient retirement savings instruments.

Now let’s compare the SBI Life Retire Smart with an equally risky investment instrument.

7.) ELSS Mutual Fund vs. SBI Retire Smart Comparison Review:

In this alternative, you can choose to invest in an ELSS mutual fund and a term insurance plan. ELSS mutual funds invest in stocks.

The advantage of this alternative is that it can give you very high returns.

The disadvantage is that there are no guaranteed returns that you will get from investments in ELSS. ELSS mutual funds’ returns depend on the performance of the stocks that they invest in.

Equity Linked Savings Schemes (ELSS) are tax-saving mutual funds that qualify for deductions under Section 80C while offering the potential for higher long-term returns.

So this alternative is good for your retirement planning only if you are a high-income earner.

In case the ELSS you invest in ends up giving high returns, you can have a very comfortable retirement income.

In case your ELSS investments give a low return, you should still have enough savings to meet your retirement needs without any difficulty.

|

ELSS |

|

|

Year |

ELSS |

|

1 |

-1,00,000 |

|

2 |

-1,00,000 |

|

3 |

-1,00,000 |

|

4 |

-1,00,000 |

|

5 |

-1,00,000 |

|

6 |

-1,00,000 |

|

7 |

-1,00,000 |

|

8 |

-1,00,000 |

|

9 |

-1,00,000 |

|

10 |

-1,00,000 |

|

11 |

-1,00,000 |

|

12 |

-1,00,000 |

|

13 |

-1,00,000 |

|

14 |

-1,00,000 |

|

15 |

-1,00,000 |

|

16 |

-1,00,000 |

|

17 |

-1,00,000 |

|

18 |

-1,00,000 |

|

19 |

-1,00,000 |

|

20 |

-1,00,000 |

|

21 |

-1,00,000 |

|

22 |

-1,00,000 |

|

23 |

-1,00,000 |

|

24 |

-1,00,000 |

|

25 |

-1,00,000 |

|

1,33,94,844 |

|

|

IRR |

11.33% |

We can assume that it is highly likely that an ELSS investment can give you an annual return of at least 12%.

At this annual rate of return, Rs 1,00,000 invested annually for 25 years will grow to Rs 1,33,94,844.

You will get this amount after a deduction of 12.5% long-term capital gains (LTCG) tax.

Despite the tax on long-term capital gains, equity investments still have the potential to outperform traditional retirement insurance products over long horizons.

|

ELSS Tax Calculation |

|

|

Maturity value after 25 years |

1,49,33,393 |

|

Purchase price |

25,00,000 |

|

Long-Term Capital Gains |

1,24,33,393 |

|

Exemption limit |

1,25,000 |

|

Taxable LTCG |

1,23,08,393 |

|

Tax paid on LTCG |

15,38,549 |

|

Maturity value after tax |

1,33,94,844 |

SBI Life Retire Smart Plan Vs Other Alternative Investment Options – Comparison Review

After a thorough review of all the other alternative investment options for the SBI Life Retire Smart Plan, it seems that ELSS and PPF are far better options.

When investors compare SBI retirement plans with traditional investment options like PPF and equity mutual funds, the difference in long-term returns becomes quite evident.

We should not fall for the glitz of new plans in the market.

But, compare and review the new plan with the traditional investment options.

This in turn helps us to analyze whether the calculated returns are good or bad compared to ELSS and PPF.

Most of the time, PPF and ELSS seem to be good options after a thorough review.

8.) Final Verdict:

To achieve financial freedom in your retirement, stay away from policies like the SBI Life Retire Smart Plan.

This is not a Smart policy for planning your retirement and meeting your life insurance needs.

If you are a conservative investor, the Smart option for you will be PPF plus a term insurance plan.

If you have a better tolerance for investment risks, the Smart option for you will be ELSS plus term insurance.

But if you have already bought this policy,

9.) How to Surrender your SBI Life Retire Smart Plan?

- Surrender during the Free-look period

You can surrender your policy within fifteen days of receiving the policy, without incurring any charge.

You can also surrender your policy within 30 days of receiving it, without incurring any charge, if you bought the policy through an online channel or any other distance channel.

The free-look period allows policyholders to review the terms of the SBI Life Retire Smart policy and exit without penalty if the plan does not meet their expectations.

- Surrender value after the Free-look period:

Surrender Value is the sum payable by the life insurer when you surrender your life insurance plan.

You can also surrender the policy any time you want.

You will get the amount to which your invested premiums have grown, after deduction of surrender charges.

There is a lock-in period of 5 years in this policy.

This means that in the first five years of the policy, you cannot withdraw any money from this policy.

So if you surrender the policy within the first five years, you will need to wait till the end of five years for getting your money back.

Understanding surrender rules and lock-in periods is crucial before investing in long-term retirement ULIP products.

If you want to know whether SBI Life Retire Smart Plan is good or bad in Hindi. Then, please check out our Hindi YouTube review of the SBI Life Retire Smart Plan below (एसबीआई लाइफ पॉलिसी स्टेटस).

Key Risks Investors Should Understand Before Buying Pension ULIPs

Before investing in a pension ULIP like SBI Life Retire Smart, investors should understand a few important risks that can influence their long-term retirement outcomes.

One key factor is market risk, as the underlying funds invest in equity, balanced, or debt instruments whose performance depends on market conditions.

Another aspect is annuity rate uncertainty, since a large portion of the accumulated corpus must typically be used to purchase an annuity at retirement, and the pension income depends on the annuity rates available at that time.

Investors should also consider the lock-in period and limited liquidity associated with pension ULIPs.

These plans usually come with a mandatory lock-in period, making early access to funds difficult compared to other investment options.

Additionally, policy charges such as fund management fees, mortality charges, and administration charges can gradually reduce the compounding effect over time, potentially impacting the final retirement corpus.

Understanding these factors can help investors evaluate whether a pension ULIP fits well within their overall retirement planning strategy.

10.) Conclusion:

SBI Life Retire Smart is presented as a retirement plan.

But considering the benefits, and the alternatives, it is clear that it is a well-presented par product.

Neither a reliable insurance plan nor a retirement plan.

And for you, as a long-term investor, it would be better for you to go for alternatives rather than fall for such products.

A well-structured retirement strategy should ideally combine growth assets like equity with stable income sources rather than relying solely on insurance-based pension products.

Consult your financial advisor, and chart out a retirement plan so that you can achieve real financial freedom that you can 100% depend on.

Please don’t adhere to amateur bits of advice and fake customer reviews on social media platforms like Quora, Facebook, Twitter, etc.

It is always wise to consult a professional planner before taking a decision that will affect your future in the long run.

If you have any comments or questions, write them in the comment box below.

Or are you interested in creating a Comprehensive Financial Plan for your financial goals?

Skip the queue by registering for your 30-minute FREE Financial Plan Consultation. Click the ‘‘BOOK YOUR SLOT NOW!’’ button below.

It’s a rip off.

Never invest in SBI.LIFE IR SBI RETIRE SMART.

THEY WILL JUSG STEAL YOUR MONEY.

sbi retire smart is useless fund, they steal peoples money, 40% of commission goes to the broker or agent

Thank you – this is very helpful analysis !

SBI bank employees contact the SBI insurance agent for any customer that has a bank balance and an easy target to be duped. We get a call and they trap us into signing for big amounts. If send any complaints to higher authorities it is the same agent that calls back to say” do not worry and do not try to cancel, you are going to be very rich , continue paying “.

Even the higher officials do not bother to answer our concerns. They just let the same agent know.It is like once we sign, only contact we can have is that agent.

All of them focus only on their commission. They just do not care about customers.

1/3 amount withdrawn after 5 years in SBI retire smart plan. Annuity taken for balance amount. Is 1/3 withdrawn amount taxable ?

No.

Don’t buy this product.

After completion of 5 five years , we will not get the surrender value in full. They will give only 1/3 of our fund value. Balance they will give as pensions.

I paid at SBI Life Retire Smart policy 1lac / year for 3 years . I plan to surrender this policy . I have to wait for 5 years to surrender the policy … 4th and 5th year policy should pay or not . If 5th year surrender means how much can get back

Consulting your financial planner is essential. They will compare the benefits of continuing with the policy versus surrendering it and investing in mutual funds. If you convert to a paid-up policy, you retain some insurance coverage and accrued benefits. If you surrender and invest in MFs, you could potentially achieve higher returns, but this carries more risk. Your planner can project both scenarios to help you make an informed decision.