Does the Tata AIA Smart Sampoorna Rakshak Pro Plan offer comprehensive protection and growth in one?

Can the Tata AIA Smart Sampoorna Rakshak Pro Plan ensure your loved ones’ safety with a plan designed for total peace of mind?

Is Tata AIA Smart Sampoorna Rakshak Pro the right comprehensive plan to help you achieve your goals?

In this article, we will explore its features, advantages, disadvantages, costs involved, and potential returns using an Internal Rate of Return (IRR) analysis. This review aims to provide a foundation for your decision-making process.

Table of Contents:

What is the Tata AIA Smart Sampoorna Rakshak Pro Plan?

What are the features of the Tata AIA Smart Sampoorna Rakshak Pro Plan?

Who is eligible for the Tata AIA Smart Sampoorna Rakshak Pro Plan?

What are the benefits of the Tata AIA Smart Sampoorna Rakshak Pro Plan?

3. Loyalty additions and Fund Boosters

What are the charges under the Tata AIA Smart Sampoorna Rakshak Pro Plan?

Grace Period, Discontinuance & paid-up and Revival for Tata AIA Smart Sampoorna Rakshak Pro Plan

Free look period for Tata AIA Smart Sampoorna Rakshak Pro Plan

Surrendering Tata AIA Smart Sampoorna Rakshak Pro Plan

What are the advantages of the Tata AIA Smart Sampoorna Rakshak Pro Plan?

What are the disadvantages of the Tata AIA Smart Sampoorna Rakshak Pro Plan?

Research Methodology of the Tata AIA Smart Sampoorna Rakshak Pro Plan

Benefit Illustration – IRR Analysis of the Tata AIA Smart Sampoorna Rakshak Pro Plan

Tata AIA Smart Sampoorna Rakshak Pro Plan Vs Other Investments

Tata AIA Smart Sampoorna Rakshak Pro Plan Vs Pure Term + ELSS

Final Verdict on the Tata AIA Smart Sampoorna Rakshak Pro Plan

What is the Tata AIA Smart Sampoorna Rakshak Pro Plan?

Tata AIA Smart Sampoorna Raksha Pro is a Unit-linked, Non-Participating, Individual Life Insurance Plan. Tata AIA Smart Sampoorna Rakshak Pro can help you fulfil your long-term goals such as children’s education, retirement planning and wealth creation along with providing you an adequate life cover.

What are the features of the Tata AIA Smart Sampoorna Rakshak Pro Plan?

- Offers high Sum assured, to secure your loved ones from unforeseen events

- Flexible premium payment term, with an option of whole-life coverage

- Two plan options are available: Classic option and Optima option

- Customisable to exactly align with future goals

- Choose from a range of debt and equity-oriented funds

- Generate a second income with new partial withdrawal strategies.

- Return of 2X premium allocation charges and 2X mortality charges

- Smart Lady benefits for female customers

Who is eligible for the Tata AIA Smart Sampoorna Rakshak Pro Plan?

| Minimum | Maximum | |

| Entry Age | 18 years | 65 years |

| Maturity Age | 38 years | 100 years |

| Policy term | 20 years | 82 years |

| Premium paying term | Single pay Limited pay: 5 years Regular pay: 20 years |

Limited pay: Policy term minus 1 Regular pay: Equal to the policy term |

| Premium payment frequency | Annual, Half-yearly, Quarterly and Monthly | |

What are the benefits of the Tata AIA Smart Sampoorna Rakshak Pro Plan?

1.) Maturity benefit

On survival to the end of the Tata AIA Smart Sampoorna Rakshak Pro policy term, you will receive the Total fund value, including the Top-up premium fund value at the applicable NAV on the date of maturity.

2.) Death benefit

In case of death of the life insured during the Tata AIA Smart Sampoorna Rakshak Pro policy term, the nominee will get, the highest of,

- The basic sum assured net of all ‘Deductible partial withdrawals’, if any from the Premium Fund Value or

- The Premium fund value or

- 105% of the total premium paid up to the date of death

In addition to this, the highest of the following is payable

- The approved Top-up Sum assured

- Top-up premium fund value

- 105% of the total top-up premium fund value

3.) Loyalty additions and Fund Boosters

Refund of Mortality charges

Starting from the 11th policy year, at the end of each policy month, the mortality charge (excluding underwriting extra and taxes) deducted in the 120th month prior shall be added to the Fund Value in the form of an addition of units.

Classic option – Refund of twice the Mortality charges

Optima option – Refund of actual Mortality charges

Refund of Premium Allocation Charges

At the end of the 10th, 11th, 12th and 13th policy years, the total Premium Allocation Charges (excluding taxes) deducted 10 years prior (i.e. over the policy years 1,2, 3 and 4 respectively) shall be added to the Fund Value in the form of addition of units.

Classic option: Refund of twice the Premium Allocation Charge

Optima option: Not applicable

What are the Investment strategies and Fund options under the Tata AIA Smart Sampoorna Rakshak Pro Plan?

This product gives you the freedom to make investments in line with your personal needs and investment risk profile.

- You can choose from the 25 investment fund options. Or

- Choose any one of the following portfolio strategies

- Enhanced Systematic Money Allocation & Regular Transfer (Enhanced SMART)

- Life-stage-based Portfolio Strategy

A. Fund options

You have several funds to pick from. According to the asset allocation strategy you’ve selected, your allocated Regular/ Single Premium and Top-Ups (if applicable) are invested in one or more investment funds. You can decide to select one or more or all of the 25 Funds.

|

S.no |

Fund Name |

Risk Profile |

Asset Allocation |

||

|

Equity |

Debt |

Money Market |

|||

|

1 |

Emerging opportunities Fund |

High |

80-100% |

0-10% |

0-20% |

|

2 |

Sustainable Equity Fund |

High |

80-100% |

0-20% |

0-20% |

|

3 |

Multi Cap Fund |

High |

60-100% |

0-40% |

0-40% |

|

4 |

India Consumption Fund |

High |

60-100% |

0-40% |

0-40% |

|

5 |

Top 50 Fund |

High |

60-100% |

– |

0-40% |

|

6 |

Top 200 fund |

High |

60-100% |

– |

0-40% |

|

7 |

Super Select Equity Fund |

High |

60-100% |

0-40% |

0-40% |

|

8 |

Large Cap Equity Fund |

High |

80-100% |

– |

0-20% |

|

9 |

Whole Life Mid-Cap Equity Fund |

High |

60-100% |

– |

0-40% |

|

10 |

Dynamic Advantage Plan |

Medium |

20-80% |

20-80% |

0-20% |

|

11 |

Whole Life Aggressive Growth Fund |

Medium to High |

50-80% |

20-50% |

0-30% |

|

12 |

Whole Life Stable Growth Fund |

Low to Medium |

30-50% |

50-70% |

0-20% |

|

13 |

Whole Life Income Fund |

Low |

– |

60-100% |

0-40% |

|

14 |

Whole Life Short-Term Fixed Income Fund |

Low |

– |

60-100% |

0-40% |

|

15 |

Flexi Growth Fund |

High |

70-100% |

0-10% |

0-30% |

|

16 |

Constant Maturity Fund |

Medium |

– |

80-100% |

0-20% |

|

17 |

Target Maturity Fund |

Medium |

– |

80-100% |

0-20% |

|

18 |

Small cap Discovery Fund |

High |

70-100% |

0-10% |

0-30% |

|

19 |

Business Cycle Fund |

High |

70-100% |

0-30% |

0-30% |

|

20 |

Rising India Fund |

High |

70-100% |

0-30% |

0-30% |

|

21 |

Mid-cap Momentum Index Fund |

High |

0-80% |

– |

0-20% |

|

22 |

Flexi Growth Fund II |

High |

70-100% |

0-10% |

0-30% |

|

23 |

Whole Life Income Fund |

Low |

– |

60-100% |

0-40% |

|

24 |

Nifty Alpha 50 Index Fund |

High |

80-100% |

– |

0-20% |

|

25 |

Multicap Momentum Quality Index Fund |

High |

80-100% |

– |

0-20% |

|

Govt Sec |

Money market |

||||

|

Discontinued policy fund |

60-100% |

0-40% |

|||

B. Enhanced SMART option

This option is applicable till PPT only. An enhanced SMART strategy is not available with top-up premium funds.

The Tata AIA Smart Sampoorna Rakshak Pro policyholder gets the choice between two funds—a debt-oriented fund and an equity-oriented fund—under the Enhanced SMART option. For the variety of available funding, please see the table below:

|

Debt oriented funds |

Equity oriented funds |

|

Whole Life Income Fund |

Emerging Opportunities Fund |

|

Whole Life Short-Term |

Sustainable Equity Fund |

|

Fixed Income Fund |

Large Cap Equity Fund |

|

Constant Maturity Fund |

Whole Life Mid Cap Equity Fund |

|

Target Maturity Fund |

Multi Cap Fund |

|

Whole Life Income Fund II |

India Consumption Fund |

|

Top 50 Fund |

|

|

Top 200 Fund |

|

|

Super Select Equity Fund |

|

|

Flexi Growth Fund |

|

|

Small Cap Discovery Fund |

|

|

Business Cycle Fund |

|

|

Rising India Fund |

|

|

Midcap Momentum Index Fund |

|

|

Flexi Growth Fund II |

|

|

Nifty Alpha 50 Index Fund |

|

|

Multicap Momentum Quality Index Fund |

Here, the entire annual/single allocable premium is parked in the selected debt-oriented fund before being systematically transferred into the policyholder’s preferred equity fund It allows you to enter the volatile equity market in a structured manner.

C. Life-Stage based Portfolio Strategy

Under this Strategy, your portfolio will be structured as per your age and risk profile selected by you (Conservative, Moderate, or Aggressive). We will automatically shift your investments from riskier assets to safer assets progressively as you age.

We will invest your Single Premium/Annualized Premium between the two funds, an equity fund, and a debt fund (as selected by you from our range of funds) in a predetermined proportion.

|

Debt oriented funds |

Equity oriented funds |

|

Whole Life Income Fund |

Emerging Opportunities Fund |

|

Whole Life Short-Term |

Sustainable Equity Fund |

|

Fixed Income Fund |

Large Cap Equity Fund |

|

Constant Maturity Fund |

Whole Life Mid Cap Equity Fund |

|

Target Maturity Fund |

Multi Cap Fund |

|

Whole Life Income Fund II |

India Consumption Fund |

|

Top 50 Fund |

|

|

Top 200 Fund |

|

|

Super Select Equity Fund |

|

|

Flexi Growth Fund |

|

|

Small Cap Discovery Fund |

|

|

Business Cycle Fund |

|

|

Rising India Fund |

|

|

Midcap Momentum Index Fund |

|

|

Flexi Growth Fund II |

|

|

Nifty Alpha 50 Index Fund |

|

|

Multicap Momentum Quality Index Fund |

| Age | Aggressive | Moderate | Conservative | |||

| Equity | Debt | Equity | Debt | Equity | Debt | |

| 01 to 30 | 90% | 10% | 70% | 30% | 50% | 50% |

| 31-40 | 80% | 20% | 60% | 40% | 50% | 50% |

| 41-50 | 70% | 30% | 50% | 50% | 30% | 70% |

| 51-60 | 55% | 45% | 35% | 65% | 15% | 85% |

| 61-70 | 40% | 60% | 20% | 80% | 0% | 100% |

| 70 & above | 25% | 75% | 5% | 95% | 0% | 100% |

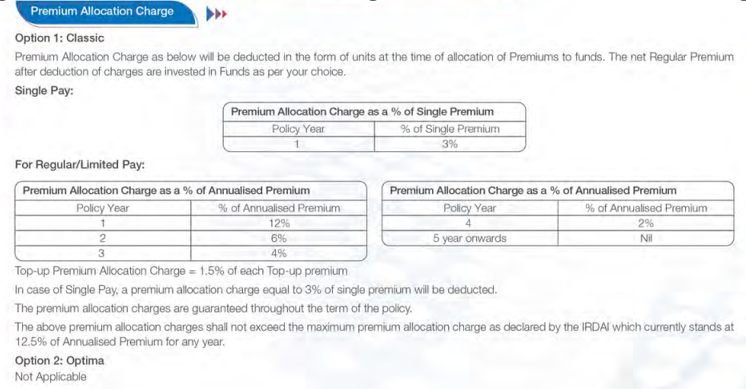

What are the charges under the Tata AIA Smart Sampoorna Rakshak Pro Plan?

i.) Premium Allocation charge

It will be deducted in the form of units at the time of allocation of premium to fund. The net regular premium after deduction of charges is invested in Funds as per your choice.

There is no premium allocation charge for the Optima Option. The following percentage applies to the Classic Option.

ii.) Policy administration charge

There is no policy administration charge for the Optima Option. For the Classic Option, a policy administration charge of 0.41% p.a. of annualised premium for Regular/Limited pay and 0.75% of the Single premium from the 5th policy year will be deducted at the beginning of each policy month.

iii.) Fund Management charges

|

Sr. No |

Fund Name |

Fund Management Charge per annum |

|

1 |

Multi Cap Fund |

1.20% |

|

2 |

India Consumption Fund |

1.20% |

|

3 |

Top 50 fund |

1.20% |

|

4 |

Top 200 fund |

1.20% |

|

5 |

Super Select Equity Fund |

1.20% |

|

6 |

Large Cap Equity Fund |

1.20% |

|

7 |

Whole Life Mid-cap Equity Fund |

1.20% |

|

8 |

Whole Life Aggressive Growth Fund |

1.10% |

|

9 |

Whole Life Stable Growth Fund |

1.00% |

|

10 |

Whole Life Income Fund |

0.80% |

|

11 |

Whole Life Short Term Fixed Income Fund |

0.65% |

|

12 |

Emerging Opportunities Fund |

1.20% |

|

13 |

Sustainable Equity Fund |

1.20% |

|

14 |

Dynamic Advantage Fund |

1.20% |

|

15 |

Flexi Growth Fund |

1.20% |

|

16 |

Constant Maturity Fund |

0.80% |

|

17 |

Target Maturity Fund |

0.80% |

|

18 |

Small Cap Discovery Fund |

1.20% |

|

19 |

Business Cycle Fund |

1.20% |

|

20 |

Rising India Fund |

1.20% |

|

21 |

Midcap Momentum Index Fund |

1.20% |

|

22 |

Flexi Growth Fund II |

1.35% |

|

23 |

Whole Life Income Fund II |

1.35% |

|

24 |

Nifty Alpha 50 Index fund |

1.35% |

|

25 |

Multicap Momentum Quality |

1.35% |

iv.) Mortality Charges

Mortality charge = Sum at Risk (SAR) multiplied by the appropriate Mortality Rate for the month, based on the attained age of the insured.

| Age | 25 | 35 | 45 | 55 |

| Mortality charge per 1000 Sum at risk p.a. | 0.787 | 1.016 | 2.179 | 6.348 |

v.) Discontinuance charges

The discontinuance charge depends on the year of discontinuance, premium amount & premium paying term. There is no discontinuance charge after the 5th policy year onwards.

vi.) Partial Withdrawal Charge

There are no partial withdrawal charges under the Tata AIA Smart Sampoorna Rakshak Pro Plan

vii.) Fund Switching Charge

There are no fund-switching charges.

viii.) Miscellaneous Charge

Nil

ix.) Premium Re-direction Charge

There is no fund re-direction charge applicable under this Tata AIA Smart Sampoorna Rakshak Pro plan

Inference from the charges: Compared to other ULIP plans available in the market, this Tata AIA Smart Sampoorna Rakshak Pro plan has relatively fewer charges.

However, the presence of discontinuance charges, policy administration charges, and premium allocation charges make the plan less attractive compared to other market-related investments.

Grace Period, Discontinuance & paid-up and Revival for Tata AIA Smart Sampoorna Rakshak Pro Plan

Grace period

A Grace Period of 30 days (15 days for monthly mode) from the due date of the first unpaid premium will be allowed in the Tata AIA Smart Sampoorna Rakshak Pro Policy.

Discontinuance & Paid-up

For Regular / Limited pay policies

Discontinuance of payment of premium during first five policy years (Lock-in Period) – Upon the expiry of the grace period, the Fund Value, by the creation of units will be credited into the Discontinued Policy Fund after deducting applicable Discontinuance Charges.

The risk cover under the Tata AIA Smart Sampoorna Rakshak Pro Plan will stop and no further charges will be levied other than the Fund Management Charge. The Policyholder is not permitted to exercise Switches or Partial Withdrawals during this time.

Discontinuance of payment of premium post first five policy years (i.e., after the expiry of the Lock in Period) – the policy shall be converted into a reduced paid-up policy with the paid-up sum assured i.e., current sum assured multiplied by the total number of premiums paid to the original number of premiums payable as per the terms and conditions of the Policy.

Revival

You will have a Revival Period of three years from the Date of Discontinuance to revive your Tata AIA Smart Sampoorna Rakshak Pro policy.

Free look period for Tata AIA Smart Sampoorna Rakshak Pro Plan

If you disagree with the terms of the Tata AIA Smart Sampoorna Rakshak Pro policy, you can return the policy within 30 days beginning from the date of receipt of the policy document, whether received electronically or otherwise.

Surrendering Tata AIA Smart Sampoorna Rakshak Pro Plan

Within the lock-in period of Policy (5 years) – The “Discontinued Policy Fund,” which is kept by the Company, will be credited with the fund value less any applicable discontinuance charges as of the date of discontinuance.

The ‘Proceeds of the Discontinued Policy’, or the fund value as of the date of discontinuance plus all income collected after deducting fund management fees, shall be paid to the Tata AIA Smart Sampoorna Rakshak Pro policyholder after completion of the lock-in period.

After the Lock-in Period (5 years) – the total fund value as of the date of complete withdrawal shall be paid to the Tata AIA Smart Sampoorna Rakshak Pro policyholder.

What are the advantages of the Tata AIA Smart Sampoorna Rakshak Pro Plan?

- The systematic Withdrawal facility allows Tata AIA Smart Sampoorna Rakshak Pro policyholders to withdraw the funds at pre-determined intervals.

- You can choose either a Chosen-Rate Withdrawal plan or an Index-based withdrawal plan for withdrawing funds.

- You have the flexibility to pay additional premiums as a Top-up premium and the Sum assured will increase accordingly.

- You have the option to receive the maturity benefit either in lumpsum or in the form of periodical payments over a settlement period of 5 years.

What are the disadvantages of the Tata AIA Smart Sampoorna Rakshak Pro Plan?

- A loan facility is not available.

- The lock period is five years.

- During the settlement term, the Tata AIA Smart Sampoorna Rakshak Pro policyholder bears the investment risk in the investment portfolio.

Research Methodology of the Tata AIA Smart Sampoorna Rakshak Pro Plan

Any investment should be evaluated in terms of safety, liquidity, and returns. Since Tata Sampoorna Rakshak Pro is a long-term, market-linked product, it’s crucial to understand the potential returns before making a purchase.

We will do this by computing the Internal Rate of Return (IRR) and then comparing it with returns from other investments.

Benefit Illustration – IRR Analysis of the Tata AIA Smart Sampoorna Rakshak Pro Plan

Consider a 35-year-old male who buys the Tata AIA Smart Sampoorna Rakshak Pro Plan with a sum assured of ₹1 Crore. The policy term is 50 years, and the premium paying term is 15 years, with an annual premium of ₹81,301. He opts for the classic option.

| Male | 35 years |

| Sum Assured | ₹ 1,00,00,000 |

| Policy Term | 50 years |

| Premium Paying Term | 15 years |

| Annualised Premium | ₹ 81,301 |

At the end of the Tata AIA Smart Sampoorna Rakshak Pro policy term, he is eligible for the maturity benefit, which is the fund value. Illustrations show two assumed rates of future investment returns: 8% p.a. and 4% p.a.

These rates are not guaranteed and do not represent the upper or lower limits of potential returns.

|

At 4% p.a. |

At 8% p.a. |

||||

|

Age |

Year |

Annualised premium / Maturity benefit |

Death benefit |

Annualised premium / Maturity benefit |

Death benefit |

|

35 |

1 |

-81,301 |

1,00,00,000 |

-81,301 |

1,00,00,000 |

|

36 |

2 |

-81,301 |

1,00,00,000 |

-81,301 |

1,00,00,000 |

|

37 |

3 |

-81,301 |

1,00,00,000 |

-81,301 |

1,00,00,000 |

|

38 |

4 |

-81,301 |

1,00,00,000 |

-81,301 |

1,00,00,000 |

|

39 |

5 |

-81,301 |

1,00,00,000 |

-81,301 |

1,00,00,000 |

|

40 |

6 |

-81,301 |

1,00,00,000 |

-81,301 |

1,00,00,000 |

|

41 |

7 |

-81,301 |

1,00,00,000 |

-81,301 |

1,00,00,000 |

|

42 |

8 |

-81,301 |

1,00,00,000 |

-81,301 |

1,00,00,000 |

|

43 |

9 |

-81,301 |

1,00,00,000 |

-81,301 |

1,00,00,000 |

|

44 |

10 |

-81,301 |

1,00,00,000 |

-81,301 |

1,00,00,000 |

|

45 |

11 |

-81,301 |

1,00,00,000 |

-81,301 |

1,00,00,000 |

|

46 |

12 |

-81,301 |

1,00,00,000 |

-81,301 |

1,00,00,000 |

|

47 |

13 |

-81,301 |

1,00,00,000 |

-81,301 |

1,00,00,000 |

|

48 |

14 |

-81,301 |

1,00,00,000 |

-81,301 |

1,00,00,000 |

|

49 |

15 |

-81,301 |

1,00,00,000 |

-81,301 |

1,00,00,000 |

|

50 |

16 |

0 |

1,00,00,000 |

0 |

1,00,00,000 |

|

51 |

17 |

0 |

1,00,00,000 |

0 |

1,00,00,000 |

|

52 |

18 |

0 |

1,00,00,000 |

0 |

1,00,00,000 |

|

53 |

19 |

0 |

1,00,00,000 |

0 |

1,00,00,000 |

|

54 |

20 |

0 |

1,00,00,000 |

0 |

1,00,00,000 |

|

55 |

21 |

0 |

1,00,00,000 |

0 |

1,00,00,000 |

|

56 |

22 |

0 |

1,00,00,000 |

0 |

1,00,00,000 |

|

57 |

23 |

0 |

1,00,00,000 |

0 |

1,00,00,000 |

|

58 |

24 |

0 |

1,00,00,000 |

0 |

1,00,00,000 |

|

59 |

25 |

0 |

1,00,00,000 |

0 |

1,00,00,000 |

|

60 |

26 |

0 |

1,00,00,000 |

0 |

1,00,00,000 |

|

61 |

27 |

0 |

1,00,00,000 |

0 |

1,00,00,000 |

|

62 |

28 |

0 |

1,00,00,000 |

0 |

1,00,00,000 |

|

63 |

29 |

0 |

1,00,00,000 |

0 |

1,00,00,000 |

|

64 |

30 |

0 |

1,00,00,000 |

0 |

1,00,00,000 |

|

65 |

31 |

0 |

1,00,00,000 |

0 |

1,00,00,000 |

|

66 |

32 |

0 |

1,00,00,000 |

0 |

1,00,00,000 |

|

67 |

33 |

0 |

1,00,00,000 |

0 |

1,00,00,000 |

|

68 |

34 |

0 |

1,00,00,000 |

0 |

1,00,00,000 |

|

69 |

35 |

0 |

1,00,00,000 |

0 |

1,00,00,000 |

|

70 |

36 |

0 |

1,00,00,000 |

0 |

1,00,00,000 |

|

71 |

37 |

0 |

1,00,00,000 |

0 |

1,00,00,000 |

|

72 |

38 |

0 |

1,00,00,000 |

0 |

1,00,00,000 |

|

73 |

39 |

0 |

1,00,00,000 |

0 |

1,00,00,000 |

|

74 |

40 |

0 |

1,00,00,000 |

0 |

1,00,00,000 |

|

75 |

41 |

0 |

1,00,00,000 |

0 |

1,00,00,000 |

|

76 |

42 |

0 |

1,00,00,000 |

0 |

1,00,00,000 |

|

77 |

43 |

0 |

1,00,00,000 |

0 |

1,00,00,000 |

|

78 |

44 |

0 |

1,00,00,000 |

0 |

1,00,00,000 |

|

79 |

45 |

0 |

1,00,00,000 |

0 |

1,00,00,000 |

|

80 |

46 |

0 |

1,00,00,000 |

0 |

1,00,00,000 |

|

81 |

47 |

0 |

1,00,00,000 |

0 |

1,00,00,000 |

|

82 |

48 |

0 |

1,00,00,000 |

0 |

1,00,00,000 |

|

83 |

49 |

0 |

1,00,00,000 |

0 |

1,00,00,000 |

|

84 |

50 |

0 |

1,00,00,000 |

0 |

1,00,00,000 |

|

85 |

18,74,929 |

1,00,00,000 |

1,39,17,062 |

1,00,00,000 |

|

|

IRR |

1.00% |

5.75% |

|||

In a 4% return scenario, the fund value is ₹18.74 lakhs, yielding an IRR of 1.00%, which essentially provides no value addition. In an 8% return scenario, the fund value is ₹1.39 crores, yielding an IRR of 5.75% as per the Tata AIA Smart Sampoorna Rakshak Pro Plan maturity calculator.

Although the policy term under the Plan is 50 years, the returns are not favourable for a long-term investment. Over time, inflation will increase the cost of your life goals, while the returns from the plan may not keep pace.

This indicates a potential shortfall in the required corpus if you choose the Tata AIA Smart Sampoorna Rakshak Pro Plan.

Tata AIA Smart Sampoorna Rakshak Pro Plan Vs Other Investments

Any market-related product should outpace the inflation rate. The TATA AIA Smart Sampoorna Rakshak Pro Plan, despite being a market-linked product, offers returns that do not even match those of a debt instrument.

In this case, the risk and return are not proportionate. Let’s explore alternative investment opportunities that provide better risk-adjusted returns.

Tata AIA Smart Sampoorna Rakshak Pro Plan Vs Pure Term + ELSS

ULIPs combine insurance and investment, but separating the two can be more beneficial. Using the same metrics from the previous illustration, let’s examine the following scenario.

For life insurance, a pure term life insurance policy with a sum assured of ₹1 crore costs ₹25,200 annually. The policy term is 30 years (coverage till 65 years), with a premium-paying term of 15 years.

Life coverage till your retirement is recommended. So, we have considered the policy term as 30 years, instead of 50 years.

After paying the premium, you have ₹56,101 left for investment, which can be allocated based on personal risk tolerance.

|

Pure Term Life Insurance Policy |

|

|

Sum Assured |

₹ 1,00,00,000 |

|

Policy Term |

30 years |

|

Premium Paying Term |

15 years |

|

Annualised Premium |

₹ 25,200 |

|

Investment |

₹ 56,101 |

|

Term insurance + ELSS |

|||

|

Age |

Year |

Term Insurance premium + ELSS |

Death benefit |

|

35 |

1 |

-81,301 |

1,00,00,000 |

|

36 |

2 |

-81,301 |

1,00,00,000 |

|

37 |

3 |

-81,301 |

1,00,00,000 |

|

38 |

4 |

-81,301 |

1,00,00,000 |

|

39 |

5 |

-81,301 |

1,00,00,000 |

|

40 |

6 |

-81,301 |

1,00,00,000 |

|

41 |

7 |

-81,301 |

1,00,00,000 |

|

42 |

8 |

-81,301 |

1,00,00,000 |

|

43 |

9 |

-81,301 |

1,00,00,000 |

|

44 |

10 |

-81,301 |

1,00,00,000 |

|

45 |

11 |

-81,301 |

1,00,00,000 |

|

46 |

12 |

-81,301 |

1,00,00,000 |

|

47 |

13 |

-81,301 |

1,00,00,000 |

|

48 |

14 |

-81,301 |

1,00,00,000 |

|

49 |

15 |

-81,301 |

1,00,00,000 |

|

50 |

16 |

0 |

1,00,00,000 |

|

51 |

17 |

0 |

1,00,00,000 |

|

52 |

18 |

0 |

1,00,00,000 |

|

53 |

19 |

0 |

1,00,00,000 |

|

54 |

20 |

0 |

1,00,00,000 |

|

55 |

21 |

0 |

1,00,00,000 |

|

56 |

22 |

0 |

1,00,00,000 |

|

57 |

23 |

0 |

1,00,00,000 |

|

58 |

24 |

0 |

1,00,00,000 |

|

59 |

25 |

0 |

1,00,00,000 |

|

60 |

26 |

0 |

1,00,00,000 |

|

61 |

27 |

0 |

1,00,00,000 |

|

62 |

28 |

0 |

1,00,00,000 |

|

63 |

29 |

0 |

1,00,00,000 |

|

64 |

30 |

0 |

1,00,00,000 |

|

65 |

31 |

0 |

1,00,00,000 |

|

66 |

32 |

0 |

|

|

67 |

33 |

0 |

|

|

68 |

34 |

0 |

|

|

69 |

35 |

0 |

|

|

70 |

36 |

0 |

|

|

71 |

37 |

0 |

|

|

72 |

38 |

0 |

|

|

73 |

39 |

0 |

|

|

74 |

40 |

0 |

|

|

75 |

41 |

0 |

|

|

76 |

42 |

0 |

|

|

77 |

43 |

0 |

|

|

78 |

44 |

0 |

|

|

79 |

45 |

0 |

|

|

80 |

46 |

0 |

|

|

81 |

47 |

0 |

|

|

82 |

48 |

0 |

|

|

83 |

49 |

0 |

|

|

84 |

50 |

0 |

|

|

85 |

10,83,38,951 |

||

|

IRR |

10.75% |

||

Here, we have chosen an equity instrument—the ELSS fund, which is also a market-linked product. After the initial investment period of 15 years, the fund is allowed to grow. The final pre-tax maturity value is ₹12.36 crores.

After accounting for capital gains tax, the final maturity amount is ₹10.83 crores, with an IRR of 10.75% (post-tax return).

|

ELSS Tax Calculation |

|

|

Maturity Value after 50 years |

12,36,77,870 |

|

Purchase price |

8,41,515 |

|

Long-Term Capital Gains |

12,28,36,355 |

|

Exemption limit |

1,25,000 |

|

Taxable LTCG |

12,27,11,355 |

|

Tax paid on LTCG |

1,53,38,919 |

|

Maturity value after tax |

10,83,38,951 |

For comparison purposes, we allowed the fund to grow until the age of 85 years. Alternatively, you have the flexibility to withdraw the funds as needed, without any restrictions. The returns are far superior to the Tata AIA Smart Sampoorna Rakshak Pro Plan.

The liquidity and inflation-beating returns are significant advantages over the Tata AIA Smart Sampoorna Rakshak Pro Plan.

Final Verdict on the Tata AIA Smart Sampoorna Rakshak Pro Plan

The Tata AIA Sampoorna Rakshak Pro Plan offers life cover protection and market-linked investment opportunities. However, the high premium includes many charges for policy operations, reducing the net amount invested in the market. Over the long run, this results in below-average returns.

While the life cover is adequate, the investment aspect of the Tata AIA Smart Sampoorna Rakshak Pro Plan is unsatisfactory and also it has a high agent commission.

Long-term investments should facilitate wealth accumulation, but this plan falls short, making it an unfit investment option.

For an affordable premium and adequate life cover, consider a pure term life insurance policy.

This provides a safety net and peace of mind. Investments for life goals should be chosen prudently, based on your risk tolerance level. Selecting appropriate investment products keeps your financial plan on track.

Are Facebook, Twitter, and Quora the last word when it comes to financial advice?

To achieve your financial milestones, a solid financial plan tailored to your personal requirements is essential. Professionals like Certified Financial Planners can create a comprehensive financial plan to meet your needs.

Leave a Reply