Are you someone who hesitates to invest just because a friend or family member has lost money in the past?

Do you know the majority of people fail in investment due to a lack of investment knowledge?

They think the investment is too complicated to understand and procrastinate forever to invest anywhere.

But you have chosen to learn about investment; CONGRATULATIONS!

This action will separate you from the large majority of confused investors and make you an INSIDER in the investment world.

If you are planning to begin your investment in Mutual Fund or you have already started off your investment. In both cases, this post will provide you with all the necessary insights into Mutual Fund investment.

Let’s read on and learn…

If you’re wondering “what is a mutual fund in simple words,” this guide will break it down step by step.

Table of Content

1. What is Mutual Fund?

2. How do Mutual Funds work?

3. Advantages and disadvantages of Mutual Funds.

4. Mutual Fund KYC Process Explained

5. Is there any risk in a Mutual Fund investment?

6. How to Invest in Mutual Funds?

7. What are the different types of Mutual Funds?

8. What is Net Asset Value? What is its significance in Mutual Funds?

9. How to select Mutual Funds?

10. How to analyze the performance of Equity Mutual Funds?

11. Direct vs Regular Mutual Funds – What’s the Difference?

12. How to analyze the performance of a Debt Mutual Fund?

13. Taxation of Equity Funds

14. Taxation of Debt Funds

15. How the returns are calculated in Mutual Funds?

16. When to review your investment portfolio?

17. Conclusion

What is Mutual Fund?

According to the Oxford dictionary, the meaning of the term “Mutual Fund” is, “a company that offers a service to people by investing their money in various businesses”.

In simple words, the mutual fund is a kind of financial vehicle where the group of people or investors pools in money with the intention of generating returns.

The financial corpus so formed is invested in various asset classes.

What are mutual funds: diversified portfolios managed by professionals to spread risk.

A mutual fund investment allows individuals to participate in capital markets without directly selecting individual securities.

In simple words, a mutual fund meaning can be explained as collective investing managed by experts.

How do mutual funds work?

A mutual fund is a kind of financial vehicle where a group of people or investors pools in money with the intention of generating returns.

- Investment is done under a particular scheme managed by an Asset Management Company (AMC).

- The formed corpus is invested in securities like equity shares, and bonds according to the scheme’s investment objective.

- AMC appoints fund managers, who manage the investment portfolio as per the market movements to create wealth for investors.

- Investors usually make money in mutual funds by way of regular dividends/interest and capital appreciation. They may choose to reinvest the capital gains via a growth option or earn regular income by way of a dividend option.

- The fund house charges an annual fee called expense ratio from the investors to manage their portfolio.

Understanding how mutual funds work in India helps you leverage local regulations and tax benefits.

The working of mutual funds involves unit allocation, NAV calculation, and daily valuation of assets.

Knowing how mutual fund works with example helps investors understand market-linked returns better.

Where do mutual funds invest?

Mutual Funds invest basically in three types of asset classes, which are:

Stocks: Stocks represent ownership or equity in a company.

This asset class has historically outperformed all other asset classes over the long term but tends to be more volatile in the short term.

Equity mutual funds primarily invest in stocks across sectors, market capitalisations, and themes.

Bonds: This represents debt from companies, financial companies or government agencies.

They provide income in the form of interest payments and principal if held till maturity.

There can be price volatility because of interest rate movements and other events in the economy/political scenario.

Debt mutual funds focus on capital preservation and predictable income.

Money market instruments: These are inter-bank call money, commercial paper, treasury bills, certificate of deposits (CDs), and short-term bonds.

They pay interest and are the least volatile of all asset classes. But, over the long term, the returns may not keep up with inflation.

Liquid and money market mutual funds are commonly used for short-term investment needs.

Advantages and Disadvantages of Mutual Funds

Advantages:

1. Mutual funds are diversified.

When you invest in any stock, your investment is more focused. If that particular Stock goes up, you will be benefitted; otherwise, you will lose your money. If you want to diversify your stock investment, you need to invest in various stocks independently.

But, by investing in a single mutual fund, you automatically invest in various assets and stocks. If one stock or asset goes down, there are others that may compensate for it.

Your investment in a mutual fund reduces the risk to which you would’ve been exposed by investing in a single stock/bond.

A mutual fund usually invests in a broad cross section of industries/companies (Sector specific funds, as the name suggests, however invest in specified industries).

Because of this, the negative performance of one security will not have as much of an impact on the fund.

Diversification is one of the biggest advantages of mutual funds compared to direct stock investing.

2. Managed by Experts:

When you invest in a mutual fund, your money is managed by professionals who have the experience and resources to thoroughly analyze the economy/markets to spot good investment opportunities which might not be easy or feasible for an individual investor.

Fund managers in mutual funds are highly experienced and qualified professionals, they consistently research, analyze and manage their funds.

A mutual fund is a relatively cost-effective way for an investor to get full-time fund managers to make and monitor investments.

Fund managers also have better access to fund-related information.

Professional fund management reduces the burden of active monitoring for investors.

3. Liquidity:

You can buy or sell Mutual Funds anytime and can redeem total or partial investments anytime you want to. Investment can be redeemed in 2-3 working days.

You will be able to get your money back within a short period as compared to other securities.

Liquidity makes mutual fund investment suitable for both short-term and long-term goals.

4. Offers High Convenience:

Investing in a mutual fund involves very little paperwork and helps you avoid many problems such as bad deliveries, delayed payments, and unnecessary follow-up with brokers and companies.

Mutual Fund investments are highly convenient for a beginner investor,

- as you can invest any time, can start investing with a small amount (Rs.500),

- can invest through various channels (Directly through Mutual Fund houses,

- can invest in a Demat account, through online banking/mobile banking, mutual fund distributors, various apps, etc.),

- also, you can track your portfolio easily (online or through apps), and get professional management of your fund.

Systematic Investment Plans (SIPs) make mutual funds accessible even with small monthly investments.

5. Reinvestment of your income:

A mutual fund allows investors to reinvest their returns and dividends in additional fund units.

Such investment over a period of time will produce compounding interest on your investments.

Compounding plays a crucial role in long-term mutual fund returns.

6. Provides a wide range of investment options and objectives:

It is possible to choose a suitable Mutual Fund scheme for your personal and family needs.

This could be related to your risk profile and desired investment horizon. We will discuss these factors in greater detail in the upcoming sections.

Mutual funds cater to different goals such as wealth creation, income generation, and capital protection.

7. Transparency and ease of comparison:

You can track the performance of your fund on a regular basis and you can easily compare the different mutual funds with each other to analyze their current performance and take your call to sell the existing fund or increase your investment in your existing scheme.

NAV disclosure and portfolio transparency make mutual funds easy to evaluate.

Disadvantages:

1. Expense ratio/Management fees:

The expense ratio represents all of the management fees and operating costs of the fund.

You must check this factor before you choose to invest in any fund (Equity, Debt or Liquid Fund).

Look for the lowest range of expense ratios in your chosen fund category.

Direct mutual funds generally have a lower expense ratio than regular mutual funds.

2. No fixed Exit load:

Some mutual funds charge the Exit Load. An exit load is a penalty; in case you choose to redeem your investment before a certain time frame.

For different mutual fund schemes, the exit load levied is different, it can be as much as 2% of the total redemption amount, and also it can be 0%. You should check this factor before you invest.

Exit load discourages premature withdrawal from long-term mutual fund investments.

3. No guaranteed returns:

Even though different Mutual funds carry a different risk profile, none of them could give you guaranteed returns as provided by bank FDs or PPF. Mutual funds are subject to market risks.

Market-linked returns are both an opportunity and a risk in mutual fund investment.

4. No control:

A Fund Manager has better control over the funds and you must trust his/her judgment, without any control in your hand.

Investors delegate investment decisions to the fund manager.

Our take:

Based on the above-mentioned advantages and disadvantages, it is true that the returns on mutual fund investments are not guaranteed and are subject to market risk. But mutual funds are the most transparent, efficient and convenient way of investment. If you do a careful analysis before your investment, YOU WILL GET GOOD RETURNS!

Mutual funds are best suited for disciplined, long-term investing.

- Mutual Funds are ideal for long term investors. So, to keep short-term investors away from long term investments, Exit Loads are levied as a penalty. Exit Loads are generally very low (1%-2%). Mutual Funds look after long term investors and they have separate funds (liquid funds) for short term investors, where there is no Exit-Load. Whereas, the Long term investors are adequately rewarded.

- Mutual funds consist of management charges, but it is very small. Fees are required to manage your funds and cover all the operating costs involved in the fund. And, Mutual Fund company does it very effectively.

You must consider taking advice from an experienced investment planner before making a final investment decision. They will give you the best advice in choosing your suitable Mutual Fund.

Also, you can choose to book a “30-min FREE Consultation” call with us, to take our advice in making your investment decision.

Mutual Fund KYC Process Explained

Before you start investing in any mutual fund, completing the KYC (Know Your Customer) process is mandatory.

KYC ensures that the investor’s identity and address are verified, making your investment secure and compliant with SEBI regulations.

Steps in Mutual Fund KYC:

- Document Submission: You need to provide:

- A filled KYC form

- A recent passport-size photograph

- PAN card copy (self-attested)

- Address proof (Aadhaar, Passport, or Utility Bill)

- Verification: Documents can be submitted offline at the fund house or through intermediaries like CAMS/Karvy, or online using eKYC via Aadhaar OTP verification.

- KYC Approval: Once submitted, your details are verified by the KYC Registration Agency (KRA). After approval, you receive a KYC compliance confirmation, which allows you to invest in any mutual fund across India.

Why KYC is Important:

- It prevents fraud and money laundering

- Ensures smooth processing of transactions like redemption, switching, or SIP registration

- A one-time process; once KYC is approved, you can invest in multiple mutual fund schemes without repeating the process

Completing KYC is a crucial first step to start your mutual fund investment journey safely and efficiently.

Is there any risk or insecurity in Mutual Fund investment?

As the banks are supervised by Reserve Bank of India (RBI), in a similar way, the Mutual funds are also regulated and supervised by regulatory agencies like the Securities and Exchange Board of India (SEBI) and the Association of Mutual Funds in India (AMFI).

The license to run a Mutual Fund company is not much different than the license given to a bank to do its operation.

They are given the same level of screening and diligent monitoring for their smooth functioning.

Therefore, mutual funds are fully secure and there is absolutely NO risk in terms of losing all your money.

SEBI regulations ensure investor protection and transparency in mutual funds.

To address all your fears and anxieties regarding Mutual Funds, you can further read this article on “How safe are your Mutual Funds?”

Let us understand, how to Invest in Mutual Funds?

To start investing in Mutual Funds, you need to have a bank account, PAN card, and KYC documentation.

Online mutual fund investment has simplified the onboarding process for investors.

To do your KYC, you need to submit the following documents:

- Filled KYC Form

- Recent passport size photograph

- Self-attested copy of your PAN Card.

- Self-attested copy of your address proof, such as Aadhaar Card.

You can submit the above documents directly to the fund house or you can submit it through CAMS/Karvy.

KYC is a one-time process and once KYC is done, you can invest in any Mutual Fund of your choice.

Once KYC is completed, investors can choose between lump sum or SIP investment modes.

Different ways to invest in Mutual Funds

There are several ways in which you can invest in the mutual fund, there are online as well as offline ways and each method has its own pros and cons.

Understanding different options helps investors learn how to invest in mutual funds in a cost-effective and structured manner.

This section explains the mutual fund process and various mutual fund investment methods available in India.

Let’s read the description below:

1. Directly with the fund house

You can visit any fund house office and open your mutual fund account. If your KYC is done, your account can be opened online, as well.

The only problem with this method is that you can invest in the schemes of only one fund house.

In order to have multiple schemes, you need to have separate multiple accounts with different login details for each fund.

This method is commonly used for direct mutual funds and helps reduce mutual fund charges over the long term.

Investors choosing this route should clearly understand direct vs regular mutual funds before investing.

2. Through distributors or Independent Financial Advisors (IFAs)

You can also invest through AMFI (Association of Mutual Funds of India) registered distributors who can give you the basic advice on your investment and can do all the paperwork, as well as send reports, etc.

It is a convenient method and it can take away a lot of your headache regarding any queries or paperwork.

The possible risk with this method is: “the distributor may be biased toward certain schemes depending on the commission they would provide”.

So you must be aware and do your proper research before choosing a suitable financial advisor. You can this detailed article on The definite ways to find a trustworthy Investment Advisor.

Most of the banks also act as mutual fund distributors, they sell various Mutual funds to their customers.

So, choose between direct vs regular mutual funds based on your cost and advisory needs.

This mode is preferred by investors seeking mutual fund guidance and assistance with mutual fund investment details.

Distributors play an important role in mutual fund advisory and portfolio review.

Through CAMS/Karvy

Through CAMS and Karvy you can get free online access to many AMC schemes. Through this option, you can invest in direct schemes as well.

A mobile app is available for easy access to all information. However, currently, not all AMCs are registered with these platforms.

CAMS and Karvy act as mutual fund transaction platforms simplifying mutual fund investment and tracking.

These platforms help investors manage multiple mutual funds under one login.

Through our online account:

We at “Holistic Investment Planners”, offers you the best advice in your Mutual Fund investment. Click the link below to get started with your investment:

This option suits investors looking for structured mutual fund planning and long-term mutual fund investment support.

What are the different types of Mutual Funds?

In nutshell, the Mutual funds can be subdivided into different types depending upon various different characteristics:

1. Depending upon the fund schemes, the Mutual Funds are classified as:

- Open-Ended Fund

In this fund, you can enter or exit anytime.

These funds do not have a fixed maturity period.

Open-ended mutual funds offer flexibility and liquidity, making them ideal for SIP investors.

- Closed-Ended Fund

Closed-ended funds issue a fixed number of units that are traded on the stock exchange.

They are launched through New Fund Offer (NFO) to raise money and then traded in the secondary market similar to stocks.

These funds also have a fixed maturity period.

After the closure of the initial offer, new investors cannot enter, nor the existing investors could exit until the term of the scheme ends.

Its functionality is more similar to ETFs.

Closed-ended mutual funds are better suited for investors with a defined investment horizon.

- Interval Fund

These funds combine the characteristics of both of the above; closed as well as open-ended funds.

These funds do not permit regular buying and selling as these remain closed most of the time but open for a time interval predefined by the fund, wherein a new unit can be bought and existing units can be redeemed.

Interval funds may be suitable for investors seeking moderate liquidity with potential for higher returns.

2. Depending upon the management of funds, the Mutual Funds are classified as:

- Actively Managed Fund

These are the funds, in which the fund managers actively pick securities based on their own research and analysis.

In India, most of the Mutual Fund investments are done in actively managed funds as fund managers consistently beat the benchmark and create the returns over and above the predicted ones.

Actively managed mutual funds are ideal for investors seeking alpha or market-beating returns.

- Passively Managed Fund

Passive fund management involves the creation of a portfolio intended to track the returns of a particular market index or benchmark as closely as possible.

Fund Managers select stocks listed on an index and apply the same weightage.

In the passive fund management, a fund manager attempts to mimic some benchmark, replicating its holdings and the performance.

Passively managed mutual funds, such as index funds and ETFs, offer low-cost investing aligned with benchmark returns.

- Our take

For your long term investment, an Actively Managed Fund is better as compared to passively managed funds. Active fund management is when fund managers actively pick investments in an effort to outperform some benchmark, usually a stock market index.

Whereas, the purpose of passive portfolio management is to generate a return that is the same as the chosen index, instead of outperforming it.

3. Depending upon the Asset Class, the Mutual Funds are classified as:

- Equity Funds

Equity funds invest their assets in the Stock Market. These are also known as Stock Funds. Below are the core benefits of investing in the equity fund:

- Expert money management

- Portfolio diversification

- Systematic investment

- Better Liquidity, and

- Tax benefits

Equity mutual funds are best suited for long-term capital appreciation and wealth creation.

-

- Debt Funds

-

These types of Mutual Funds invest their assets only in Debt (Fixed Income) instruments such as corporate bonds, debentures, Government Securities, etc. The overall risk profile of the debt fund is low.

-

-

Liquid Funds

-

These funds invest their assets in low maturity money market instruments such as treasury bills, Certificate of Deposit, etc. they have maturity span of 1 to 180 days. They are the least risky type of Mutual Funds.

Liquid mutual funds are commonly used for parking surplus cash for short-term goals.

-

- Hybrid Funds

-

4. Depending upon the investment style, the Mutual Funds are classified as:

-

-

Growth funds

-

These are equity-based funds that invest primarily in Stock Markets.

-

-

The fund managers handling these funds, preferably invest in the stocks that have low dividend yield and high growth potential.

-

Growth mutual funds are designed for aggressive investors seeking capital appreciation over time.

- Value funds

- Income funds

-

These funds are known for the safety of the principal.

-

Income mutual funds cater to retirees and risk-averse investors focused on generating steady cash flows.

-

5. Few of the special Mutual funds are:

-

-

Index Funds

-

Index funds, as the name suggests, invest in an index.

-

-

These funds purchase all the stocks in the same weightage as in a particular index (Sensex or Nifty).

Index funds are ideal for investors who are risk-averse and expect predictable returns.

-

These are the passively managed funds. Index funds are not meant to outperform the market, but mimic the performance of the index.

However, if you wish to earn market-beating returns, then you can opt for actively-managed funds. -

The returns of index funds may match the returns of actively-managed funds in the short run. However, the actively-managed fund tends to perform better in the long term.

-

Index mutual funds offer broad market exposure at a low expense ratio, making them attractive for beginners.

- Sectoral/Thematic Fund

-

For example, Banking, Technology, Pharma, Infrastructure, etc.

-

Sectoral mutual funds carry higher risk and are suitable for investors with strong views on specific industries.

- ELSS, the tax-saving fund

- International funds

-

They will allow you to invest in foreign markets and give you the exposure of global companies.

-

International mutual funds offer diversification beyond Indian markets and hedge against domestic volatility.

- Retirement/Children fund

What is Net Asset Value (NAV)? What is its importance in Mutual Funds?

Net Asset Value (NAV) is a mutual fund’s price per unit. In simple terms, it is the value of a single unit of a mutual fund.

NAV in mutual fund helps investors understand the daily valuation of their mutual fund investment.

Understanding what is NAV in mutual fund is essential before starting mutual fund investment.

For example, if a mutual fund has a NAV of ₹50, it means the single unit cost of this fund is Rs. 50.

And, if you invest ₹10000 in a mutual fund with a Net Asset Value of ₹50, then you will get (10000/50) = 200units of that fund.

This example explains how NAV of mutual funds works in real life.

NAV is calculated by dividing the total value of all assets such as stocks/bonds, minus all liabilities and expenses, divided by the total number of units of the mutual fund. It is represented using the formula given below:

This NAV calculation formula is common across all mutual fund schemes in India.

As the value of the stocks, bonds and deposits change every working day; NAV also gets updated on a regular basis.

Mutual fund NAV is updated at the end of each trading day based on market movements.

NAV is not an indicator of a Mutual Fund Performance. Lower NAV does not mean the better performance of a Mutual Fund.

- In order to know the actual performance of a Mutual Fund, other performance factors must be taken care of. They are described in the next section.

- Don’t confuse low NAV with cheap valuation—performance depends on returns, consistency, and fund management.

- The NAV of a Mutual fund is more useful in understanding how the fund performs on an everyday basis.

Many beginners wrongly assume that low NAV mutual funds give higher returns, which is not true.

You can check the NAV of any mutual fund from any financial website such as amfiindia.com.

Regular tracking of mutual fund NAV helps investors monitor their mutual fund portfolio effectively.

How to select Mutual Funds? Performance Parameters and analysis

Based on the types of Mutual funds there are different factors that describe the performance of a Mutual fund.

Mutual fund analysis plays a crucial role in identifying the best mutual funds for long-term investment.

- In this section, performance analysis of Equity Funds and Debt Funds are described in sufficient detail, because these funds are more popular as compared to other funds.

- Knowing the key mutual fund performance parameters helps investors choose the best mutual funds in India suited to their goals.

These mutual fund selection tips are useful for both beginners and experienced investors.

- Equity Funds:

The first step to select an Equity oriented fund is to categorize your goals into the short, mid and long term and then choose the fund type, as shown below:

- Large-cap funds: if your investment horizon is around 5 years, then it is the better option, it can give you the return of 10-12% p.a.

- Multi-cap funds: if your investment horizon is around 7 years, then you may consider investing in the Multi-cap category. It can provide the post-tax return of 11-13% p.a.

- Small or Mid-cap funds: they are ideal for the investment horizon of more than 10 years. Small/mid-cap can provide the post-tax returns of 12-15%.

Choosing equity mutual funds based on time horizon reduces mutual fund investment risk.

When you’re learning how to select mutual funds, matching your investment horizon with the right fund type is crucial for optimizing returns.

Our Take:

Your investment depends on 2 factors:

i). Your financial goals (Short term, Midterm and Long Term)

Define your investment needs by asking yourself these simple questions

What do I require money for?

Goal-based mutual fund investment ensures better financial planning and disciplined investing.

Once you determine your financial goals, you can make a financial plan and stick with it. For example

- If you are investing for children’s education/marriage, retirement, or any other long-term goal, the schemes suited for you would be growth-oriented schemes that invest primarily in stocks

- If you are investing for regular income, the schemes suited for you would be income-oriented schemes which invest primarily in fixed-income securities

- If you are investing for an expense in less than a year or looking for a short-term parking place, money market schemes that offer capital preservation would be best suited for you.

Different mutual fund types are designed to meet different financial goals.

When do I require the money?

If you have a longer time frame in your mind, you should consider those schemes which will be the best performers in the long term, notwithstanding the fluctuations over the short term.

- On the other hand, if you require the money in less than a year, you should consider a money market scheme.

Time horizon is a key factor in mutual fund selection and asset allocation.

Understanding your financial goals and time horizon is a key part of mutual fund selection tips that every investor should follow.

- ii). Your Risk-taking appetite

How much risk am I willing to take?

Before making an investment decision, you will have to ascertain your feelings about risk.

Will you be comfortable with the short-term fluctuations in the share price or not?

Risk profiling helps investors choose mutual funds aligned with their comfort level.

If you do not want to take the risk, you can opt for an income scheme/money market scheme.

- If you are a first-time investor, then a large portion of your investment should go towards Large Cap Funds, as they involve less risk.

- If you are already investing in Mutual Funds, then you should make sure to diversify your investment in such a way that you ensure the equal weightage of your investment in “Large Cap Funds” and “Mid and Small Cap funds”.

- If you are a more aggressive investor, then you should give more weightage to Large Cap funds.

- And, if you are willing to take more risk, then you should give more weightage to Mid/Small Cap funds or Multi Cap funds. Mid/Small Cap funds are riskier, but they will provide you with better returns in the long run.

Risk appetite directly impacts mutual fund returns and portfolio volatility.

Your risk appetite plays a significant role in deciding which mutual funds are right for you, making it an essential mutual fund performance parameter.

How to select a good equity fund?

After choosing the right fund based on your investment horizon, now look for the right schemes under large-cap OR multi-cap, OR mid/small-cap.

This step is critical when shortlisting the best equity mutual funds in India.

Once you have determined the type of scheme which would suit your investment objectives, evaluate different schemes on the following parameters:

- Track record of performance: Check the fund’s performance over the last few years vis-à-vis the broad markets (BSE Sensex/S&P CNX 500) and similar schemes in the same category (Growth/Income. etc.)

- Service and transparency: Check the service and transparency standards of the mutual fund i.e whether their turnaround times are better or on par with industry standards and whether they communicate regularly the fund’s strategy, top holdings, key developments etc.

- Find out about the expenses and fees: All mutual funds charge a management fee. These details will be available in the prospectus. Some funds will have sales load and/or redemption load. You will have to decide whether the load suits your time frame.

These evaluation criteria are vital mutual fund selection tips for picking the best mutual funds in India.

The parameters described below will help you select the right scheme.

- Research the years of business, compliance record, past performance, etc. of various fund houses. This criterion can also be used for the elimination of undesired funds.

- Look for a competitive Fund Manager. A fund manager is largely responsible for the good or bad performance of any fund. Look at how the scheme is performing under the current fund manager. Also have a look at the data on how the other schemes have performed, which are managed by this fund manager, in the past.

- Selecting a skilled fund manager is one of the key mutual fund performance parameters you should consider.

Based on the above fundamental analysis, now its time to filter the schemes by analyzing their Key-ratios and other factors, as described below:

Quantitative Parameters to choose a Mutual Fund Scheme

1. Alpha and Beta

Alpha measures whether the fund has outperformed its predicted returns. Look for higher alpha.

Beta is an indicator of the volatility of the fund. A beta of greater than 1, say 1.15, means that the fund is more

volatile, in this case, it is 15%volatile with respect to the index level. It has a higher risk margin.

volatile, in this case, it is 15%volatile with respect to the index level. It has a higher risk margin.A lower beta indicates that the fund is less volatile and more stable.

Lower beta is advisable to consider but other factors must also be considered along with beta.

Alpha and beta are widely used mutual fund performance parameters for risk-return analysis.

For more details on Alpha and Beta, read this detailed post on “Statistical tools to select a rewarding Mutual Fund”.

2. Sharpe ratio

It measures the returns with respect to the risk taken. A good fund will high Sharpe ratio, as there will be better returns with the amount of risk.

Sharpe ratio helps investors compare mutual funds with similar risk profiles.

3. Asset Under Management (AUM)

It is the total market value of the investments that are managed by the Mutual Fund companies.

AUM in mutual fund reflects investor confidence and fund stability.

AUM increases when more assets are bought in or the value of the asset increases.

And, AUM decreases when assets are withdrawn or the value of the assets decreases.

You can reject the schemes with very low AUM as their volatility, expenses and risk profile could be higher.

4. Expense Ratio

As described earlier, it is a fee charged for handling your money in your investment.

Lower expense ratio mutual funds are more efficient for long-term investors.

You should avoid schemes with a very high expense ratio.

As per industry standards, the expense ratio of 1.5% is a good deal.

The average expense ratio of equity funds varies between 1.5-2.2%.

5. Exit Load

In the event of an early withdrawal from the plan before the pre-defined lock-in period, the investors are required to pay the exit load.

Exit load varies between 1%-3%. An exit load of 1% under the duration of 1 year is a common norm in 80% of the cases.

Though the equity fund investment is for the long-term, still you should avoid the funds with high exit loads (above 1%).

Let us say, you want to withdraw from the fund because of its bad performance or any other valid reason, you must not lose money in such cases.

Understanding exit load in mutual funds prevents unnecessary losses during redemption.

6. Online ratings of Mutual Funds

Nowadays there are many 3rd party agencies that give fund ratings online such as Morningstar, CRISIL, and value-research; here you can get some idea of the fund performance based on the ratings given to them, by these parties. But you should not over-depend on these ratings.

All the performance parameters of Mutual Funds mentioned above should be taken together into consideration and only after understanding them well, the investment decision must be taken.

Understanding and analyzing these mutual fund quantitative performance parameters will help you select the right fund.

All the performance parameters of Mutual Funds mentioned above should be taken together into consideration and only after understanding them well, the investment decision must be taken.

Direct vs Regular Mutual Funds – What’s the Difference?

When investing in mutual funds, you have two primary options: Direct and Regular plans.

The choice between them can significantly impact your overall returns.

- Direct Mutual Funds:

These are purchased directly from the Asset Management Company (AMC) without any intermediary. As there are no distributor commissions involved, the expense ratio is lower, which means more of your money is invested in the fund itself. Direct mutual funds are ideal for investors who are confident in researching and managing their investments online or through the AMC portal. - Regular Mutual Funds:

These are bought through distributors or financial advisors, who may provide guidance, advice, and assistance with paperwork. While they are convenient, the cost is slightly higher because the distributor earns a commission, increasing the expense ratio of the fund. Regular plans are suitable for investors who prefer professional support and personalized investment advice.

Key Difference:

The main difference lies in cost and control.

Direct plans cost less and can give higher returns in the long term, while regular plans offer convenience and advisory support at a slightly higher cost.

By understanding this distinction, investors can make an informed choice based on their experience level, comfort with research, and willingness to pay for advisory services.

Qualitative parameters to choose a Mutual Fund Scheme:

1. How long does the Mutual Fund company is in existence? And, what is its historical performance?

You should choose to invest in a scheme that has a very good long-term track record against your peers.

Long-standing mutual fund companies often demonstrate stronger governance and operational stability.

- Though it is true that historical performance is not a guarantee of future performance. But it definitely gives a key insight into the scheme.

Historical mutual fund performance helps investors understand consistency across market cycles

We recommend you find the details of the funds in Mutual Fund Factsheets and look for the funds which have consistently outperformed in the market over the medium and longer terms (3, 5, and 10 years).

Mutual fund factsheets provide crucial information such as portfolio allocation, risk ratios, and returns.

Equity funds are conducive to long-term investment only. Therefore, the focus should be on Long term performance, instead of looking into weekly, monthly, or quarterly performances!

Long-term mutual fund investing smoothens short-term market volatility.

When analyzing past returns, it is also helpful to compare the fund’s performance against relevant benchmarks such as the Nifty 50 or Sensex to understand relative strength.

Benchmark comparison is an essential part of mutual fund analysis.

- The ability of a Mutual Fund company to retain the Fund Managers!

The major credit for the outperformance or underperformance of any mutual fund scheme lies with the fund manager.

Fund manager experience plays a key role in mutual fund performance consistency.

- All Mutual Fund Companies look after good fund managers to manage their funds.

You should look at whether the Mutual Fund Company is able to retain a good Fund Manager in their company for a long time.

Low fund manager churn indicates a stable mutual fund investment philosophy.

- If a company is able to retain a good Fund Manager for a Long time, it means the company is active and performing well in its investment strategy!

- Therefore, you should consider investing in such companies.

- Fund Manager stability often translates into consistent fund management style, which is a crucial factor in reducing portfolio volatility and improving risk-adjusted returns.

Consistent fund management helps investors stay aligned with long-term investment goals.

- The investment process of a Mutual Fund Company!

The investment process in some Mutual Fund Companies are run totally by the Fund Manager’s experience; they are free to take all the major investment decisions.

Mutual fund investment process differs across fund houses and impacts portfolio outcomes.

Whereas in other companies, part of the investment process is already established, based on the investment process, which is proven and evolved over a period of time.

Process-driven mutual fund companies offer additional checks and balances.

Fund managers have to follow the defined process of investment in such companies, along with implementing their own investment strategies.

Fund managers are humans; some are more experienced, whereas others are less experienced.

Therefore, it is possible for them to make some mistakes, if the entire responsibility of the investment process is given to them.

So, companies with a defined and evolved investment process develop an added layer of safety and allow their Fund Managers to do their tasks vigilantly.

A structured investment framework reduces emotional decision-making in volatile markets.

In this process, the Fund Manager is able to concentrate well on the top-level activities.

Therefore, you should choose Mutual Fund Companies having a defined investment process.

- Such companies are considered better.

A structured investment process often incorporates risk management frameworks that help safeguard investors’ capital during market downturns.

Risk management is a critical qualitative parameter in mutual fund selection.

- Consistency of the Investment Strategy

A Mutual Fund Company must always be consistent in its investment strategy.

Also, there are various schools of thought followed by different Mutual Fund companies, when it comes to their investment strategy.

Investment strategy consistency improves predictability of mutual fund returns.

It doesn’t matter, which investment strategy a Mutual Fund Company may choose, it should stick to ONE investment strategy and must not be tempted to acquire another investment strategy in the mid-way.

Style drift in mutual funds can increase risk and confuse investors.

For example, some Mutual Fund companies follow the Market-Timing Strategy, it implies the ability to get into and out of sectors, assets or markets at the right time. Generally, they try to get into the sector when the market is low and then sell their assets when the market is high.

Other Mutual Fund Companies do not time the market and remain fully invested regardless of the market opportunity.

So, the core idea is that a Mutual Fund Company must stick to its originally adopted investment strategy and it should not be tempted to acquire the different investment strategies by seeing varying results produced by different Mutual Fund companies in the market.

Consistency in strategy also helps investors understand the fund’s risk profile better and align it with their own investment goals.

Clear strategy alignment simplifies mutual fund portfolio construction.

- Debt Funds

Debt funds are usually short-term investments.

Debt mutual funds are preferred for capital preservation and predictable income.

You should consider the points given above for choosing a good fund manager and a Mutual Fund Company to invest in.

In addition to the points mentioned above, you should also consider the key ratios as applied to debt funds, as described below:

1. Average Maturity:

It refers to the weighted average time until all securities in a debt portfolio in a mutual fund get mature.

Average maturity helps investors assess interest rate risk in debt mutual funds.

The lower the average maturity; the better it is in terms of the interest rate risk and lower volatility.

The higher the average maturity of a debt fund, the longer it will take for each security to mature in the portfolio and vice-versa.

Before investing in debt funds, it is advisable to have a look at the average maturity of the fund. For example, if you want to invest in the debt fund for 2 years, then choose the fund with an average maturity of 2 years. Similarly, if you want to invest for 5 years, choose the fund with the average maturity of 5 years and so on.

2. Modified Duration (MD):

It reflects the sensitivity of the debt security price when the scenario of the interest rate changes.

Lower modified duration indicates lower volatility in debt funds.

Particularly this parameter helps in understanding the volatility of the fund. Lower the MD, lower the volatility.

3. Yield to Maturity (YTM):

It refers to the expected rate of returns anticipated on a debt portfolio if the investments are held until maturity.

YTM is a key indicator of expected debt mutual fund returns.

For example, if a fund has a YTM of 8.5% and an average maturity of 4 years, it means, the fund will give approx. 8.5% returns if you remain invested for at least 4 years.

Apart from the above 3-factors, you should also consider the following points:

- Expense ratio: As described earlier, you should avoid schemes with a very high expense ratio. And you should choose a scheme with an average or lower expense ratio (around 1.5% or below), based on your risk-taking ability and the tenure of your investment. Most of the established fund schemes will have a lower expense ratio.

- Exit Load: There should not be any exit load on investment of ultra-short duration in debt funds. Short-duration funds with an exit load after 180 days and mid/long-duration funds with an exit load after 365 days should be avoided.

- Credit Risk and Credit Ratings: Each debt instrument in India is mandatorily rated based on its creditworthiness by various credit ratings agencies such as CRISIL, CARE, and ICRA. Each rating denotes a certain degree of risk involved – for example, the AAA rating indicates the highest credit rating. This way you can assess the risk taken by fund managers by checking the credit rating of the fund’s portfolio.

Credit quality assessment protects investors from default risk in debt mutual funds.

Additionally, investors should consider the fund’s portfolio diversification to reduce concentration risk within debt holdings.

Diversification lowers credit risk exposure in debt fund portfolios.

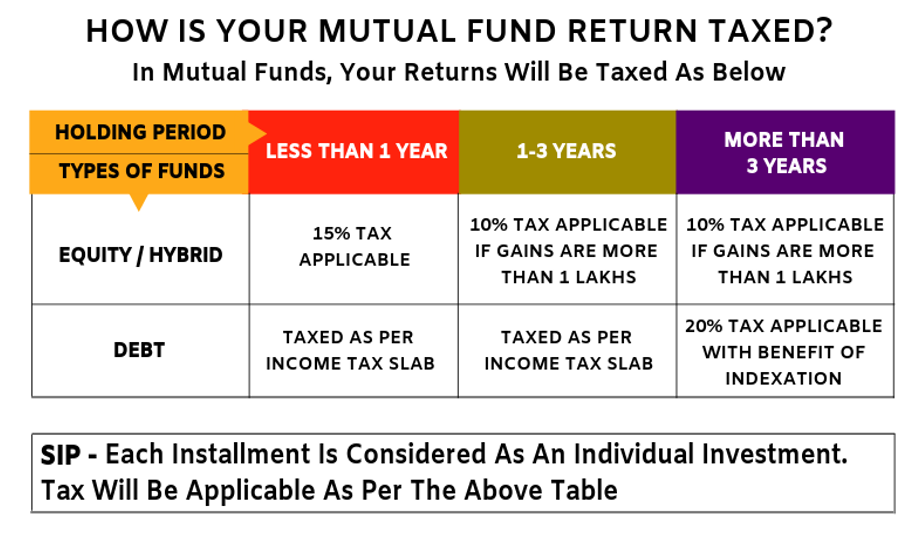

Mutual Fund Taxation

Equity and debt funds have different ways of taxation, details of both funds are discussed below:

Taxation of Equity funds

If you redeem your investments before 12 months, there is a flat 20% Capital Gain tax on your gains.

Equity mutual fund taxation depends on holding period and capital gains.

Till FY 2017-18, Equity-oriented funds had no tax on long-term capital gains if you want to sell your funds after 12 months.

But things changed after the 2025 budget, now the 12.5% tax is applicable, if the gains are more than 1.25 Lakhs, for a holding period of more than 1 year. It is demonstrated in the table below:

|

Holding Period |

Taxation |

|

Less than 1 year |

Flat 20% Capital Gain tax |

|

More than 1 year |

12.5% tax is applicable if the gains are more than |

Understanding equity mutual funds tax is essential for effective tax planning in your investment portfolio.

Taxation of Debt Funds

Gains are taxed as per your income tax slab irrespective of the holding period.

Debt mutual fund taxation differs significantly from equity funds.

Debt funds offer a unique tax advantage.

Unlike fixed deposits (FDs), where interest is taxed annually, debt funds are taxed only at the time of withdrawal and only on the amount withdrawn.

What is indexation?

Indexation means adjustment of gains with respect to inflation, that is, subtracting the impact of inflation on your returns and then paying taxes.

Indexation reduces taxable gains by accounting for inflation impact.

Here inflation is calculated based on the CII (Cost Inflation Index) provided by the income tax department each year.

Knowing debt mutual funds tax treatment helps you optimize returns on your fixed-income investments.

How the returns are calculated in a Mutual Fund?

By now you might want to know, how your returns on Mutual Fund investment are calculated!!

Well… there are various ways to calculate returns, which depend on the duration of the investment.

Mutual fund returns calculation varies based on investment duration and mode.

The various ways to calculate the returns are given below:

- Absolute Returns:

- Simple Annualized Returns:

- CAGR (Compounded Annual Growth Rate)

- XIRR (for calculating SIP Returns)

XIRR is widely used for calculating SIP returns in mutual funds.

For more illustrations and examples on calculating Mutual Fund Returns, you can read this article on Calculating Mutual Fund returns.

You can use the calculator, shown below, to find your estimated Mutual Fund Returns.

In this calculator, you can choose the option:

-

-

- whether you want to do Lumpsum Investment or SIP

- choose your desired amount of investment.

- desired frequency of paying SIP. (if the SIP option is chosen)

- duration of your investment; and

- your expected annual interest rate. For better clarity on annual returns, you can watch the video in the next section.

-

So, how much returns you should expect from your Mutual Fund Scheme?

This short video will give you an estimate on what returns should you expect from your Mutual Fund scheme.

When to review your Mutual Fund portfolio?

The consistent review of your mutual fund portfolio enables stable returns and easy accomplishment of targets.

Periodic mutual fund portfolio review ensures alignment with financial goals.

Remember the 4 simple tactics given below to review your Mutual Fund portfolio:

-

-

- Do a Quarterly check.

- Review it during the stock market fluctuations.

- Review it at the Financial year-end.

- Review it in the case of emergency situations, such as job loss, injury or accident.

-

For more details, you can read this article on “When to Review your investment portfolio?”

Regular mutual fund portfolio review helps you rebalance and stay aligned with your financial goals.

Conclusion

We hope that this exhaustive post has provided you with enough clarity on Mutual Fund Investments.

A disciplined approach to mutual fund investing leads to long-term wealth creation.

If you have further queries related to the topics discussed in this post or specific to your investment, feel free to leave them below.

Also, to create your customized investment plan and utilize our best investment services; you can book a FREE Consultation call with us by clicking the link below:

Hello sir,

I have just started my career and i was searching about mutual funds and found this and this article help me a lot in understanding about the Mutual funds.

Thank you 🙂