What’s this Moratorium?

A moratorium is a period during which the borrower does not have to repay anything (principal or interest). Here it’s a 3-month moratorium in the beginning. On 22nd May, 2020 RBI has expended the moratorium till 31st August, 2020 for another 3 months.

This blog will clarify your doubts and questions on the moratorium. It gives you an answer to whether you should opt for it or not.

Are you willing to take this moratorium. Do you think it’s a benefit and would give you great relief once for all?

Should you opt for it? What are the terms and conditions attached to it? Will there be any drawbacks in the future? Will it be a relief today and pain later?

Now let’s see the frequently asked questions on Moratorium and see if you should avail this or not.

Questions on EMI Moratorium

What is the three-month moratorium all about?

Some of us may not be able to pay our outstanding EMIs for the next few months due to the coronavirus situation. Considering this, RBI has permitted financial institutions to provide 3 months moratorium on March 27, 2020. The first three month moratorium was valid from 01.03.2020 to 31.05.2020.

Later on 22nd May 2020, RBI announced extension on EMI moratorium to provide relief to the individuals who have difficulties to pay their loans. According to Moratorium 2.0 individuals can avail the EMI moratorium till 31st August 2020.

Does it mean that EMI’s will be given up for 6 months?

This will be temporarily stopped for 6 months. You will have to pay the EMIs as the moratorium ends after 31st August, 2020. This 6 months break in EMI will be collected from you by extending the loan tenure and adding more interest for this break.

No EMI for all kinds of loans?

This is for term loans inclusive of home loans, personal loans, education loans, auto loans (car and two-wheeler loans), loans taken for purchasing Fridge, AC, mobile phone, etc and any loan that has a fixed tenure. If your lender agrees, you don’t have to pay EMI till 31st August 2020.

Is the moratorium applies for business loans?

Yes, this applies to all loans outstanding as of 31st August 2020.

Will you have to pay interest for these three months?

If you are opting for moratorium, then for this 3 or 6 months break, there will be additional interest that will be collected from you by extending your loan tenure.

Which financial institutions are permitted to provide this moratorium?

RBI indicated that all commercial banks inclusive of small finance banks, local area banks, regional rural banks, co-operative banks and Non-Banking Finance Companies which includes housing finance companies and microfinance enterprises can provide this moratorium.

If your bank provides this moratorium are you automatically covered?

You need to check with your bank about the availability of this facility and apply for it. Then they would confirm once they accept your proposal.

If you opt for this moratorium, would it affect your Cibil Score?

No, the credit score will not be affected.

Does this moratorium apply to credit card payments too?

Yes, it applies to credit card payments too, provided your bank provides it and you accept it. However, there will be interest charged for the outstanding amount due.

Would there be interest if you use this relief on credit card outstanding?

Yes, you would be charged interest for these three months at applicable rates.

What will happen to auto-debit EMIs if the moratorium is approved?

You may still have to request for cancellation of the auto-debit for 3+3 months.

What if I don’t want to take the Moratorium 2.0?

You can cancel your EMI moratorium. You can contact your bank for the cancellation process.

Detailed analysis of Moratorium

6 months moratorium for your EMI is not waiving of your EMIs for 6 months. You need to pay these EMIs later.

6 months moratorium for your EMI is not waiving of the interest on your EMIs for 6 months. You need to pay these EMIs later with additional interest. If you have taken the EMI moratorium only for the first 3 months or last 3 months, then you need to pay your interest according to your moratorium period.

In a nutshell, this moratorium is coming to you NOT at free of cost. These 6 months EMI will be collected from you with additional interest at the end of the loan tenure by extending the loan tenure. Your loan tenure may get extended by few months. So if we see the cost involved in it, it may help you decide whether you need to utilize this moratorium or not.

Here’s the link for the EMI Moratorium calculator.

You can download EMI Moratorium calculator for 6 months here!

We have created a customizable EMI moratorium calculator. If you enter your loan details, it will show you how much additional interest you will be paying in the future and how many months, your loan tenure will get extended.

Let’s see a detailed example of this:

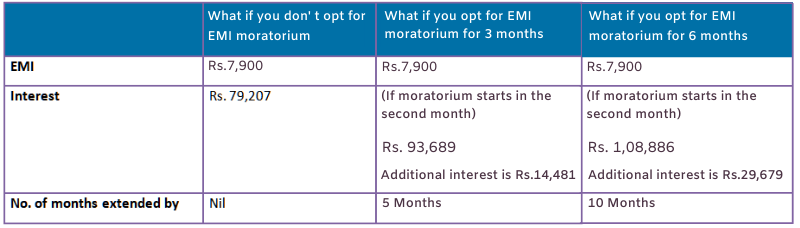

Example: You take a loan of ₹3 lakh at an interest of 12% per annum for 4 years. This tabular column is a detailed show of how much you will be paying if you opt for the moratorium and if you don’t opt for it.

What if you don’t opt for this EMI moratorium?

The EMI would be Rs.7,900 and the total interest Rs. 79,207.

What if you opt for this EMI moratorium?

If you avail of the 3-month moratorium then your interest will be Rs. 93,689. The additional interest you will pay is Rs. 14,481. The period of loan gets extended by 5 months.

What if you opt for this EMI moratorium for 6 months?

If you avail of the 6-month moratorium then your interest will be Rs. 1,08,886. The additional interest you will pay is Rs. 29,679. The period of loan gets extended by 10 months.

So what would you choose if you are in this same position?

Will you pay off the EMI’s as soon as possible?

Or will you avail this moratorium and pay extra interest charges and get your loan period extended?

The decision is in your hands now. Now that you have known the truth about the moratorium. You have got the clarity to take action.

Should you take advantage of this benefit?

You should know that this is not just three or six months, but more than three months. If you think it as a relief, it’s only a temporary (3 or 6 month) relief. At the end, additional interest will be charged and it will be an extra burden for you.

⭐ If you are a salaried employee or businessman and can get a regular income, then pay your EMIs to avoid extra interest charges and tenure extension. So don’t opt for the moratorium.

⭐ If you feel that your income is going to be disturbed or an indication that you would lose your job, opt for this moratorium so that you can join another job or find alternative ways of paying off such dues. However, you need to pay the regular EMIs after 3 or 6 months and you need to compensate this 3 or 6 month’s EMI break with additional interest at the end of the loan tenure.

⭐ For home and car loans, you can go for the moratorium if you are unable to pay your EMI’s. These are secured loans and the interest rates will be lower comparatively

⭐ For personal loans or credit cards, this should be avoided because the interest on loan outstanding is high compared to a home loan. The worst is you will be charged interest on the unpaid interests in the previous months. Hence after this moratorium, you will have a huge interest to pay.

It looks easy to covert your Credit card outstanding to EMI payments. But is it the right thing to do?

Customisable Moratorium Calculator:

This Moratorium calculator will help you find out for your specific loan details, what are the implications like what will be additional interest to be paid and the additional tenure to be extended.

If you can key in the basic details, this moratorium calculator will reveal the impact. You can use this moratorium calculator for your different loans.

In case of personal loan or credit card outstanding I would suggest, you can pledge your jewels and get a jewel loan and pay the Personal loan EMI and credit card outstanding. Jewel loans are much cheaper and credit card outstanding carry forward is a biggest debt trap you MUST avoid.

Conclusion

It is better to pay off your EMIs if you have enough funds as you will be able to avoid extra interest charges and the tenure extension. If you are not able to pay EMI with the funds you have, then you can opt for this moratorium. However remember that after the three or six months, you will have to pay EMI along with extra interest charges and the loan period also gets extended. So make a thoughtful decision.

If you have any comments or questions, write them in the comment box below.

Or are you interested in creating a Comprehensive Financial Plan for your financial goals?

Skip the queue by registering for your 30 Minute FREE Financial Plan Consultation. Click the ‘‘BOOK YOUR SLOT NOW!’’ button below.

Leave a Reply