“Never spend your money before you have it” – Thomas Jefferson

“The man who never has money enough to pay his debts has too much of something else” – James Lendall Basford

These are little quotes on debt for you to think about.

Table of Contents

- What is debt repayment?

- Why is debt repayment important?

- Why do you even take Loans?

- How does a debt start

- How much debt do you owe?

- What are the debt repayment methods?

- 8 Reasons to pay off your debt

- EMI (Equated Monthly Installment)

- Prepayment of loans

- How prepayment helps you?

- Do loans help in Tax Saving?

- How to pay off your debt faster?

- Reduce your interest burden

- Should you Invest or Pay off debt?

- To-do-list

- Conclusion

Now let’s see what Debt Repayment is.

What is Debt Repayment?

Debt repayment is a process of paying off your principal debt balance on a loan over a period. The repayment is done through a series of scheduled payments called EMIs. Knowing how to use debt wisely and repaying your debt effectively is a good sign of money management. It includes understanding the terms in the Debt Repayment process.

Why is Debt Repayment important?

Repaying debt efficiently will stop you from handing over more interest. It also saves you from a penalty fee, that is paid if you miss an EMI payment, which in turn can hurt your credit score.

Why do you even take Loans?

Commonly used loans are home loans, car loans, and education loans. Repaying the loan is a very big commitment. It’s a promise to pay an amount each month to the bank.

The burden of debt is always on your mind. You keep worrying especially when layoffs happen or

when you continuously suffer from ill-health. You are more worried about the after-effects of job loss than the job loss itself. The pressure of paying back debt is huge. You may not like your job but would stay as you have to pay back a huge debt.

“If I had one piece of advice to give to young people, it would be just to don’t get in debt. It is very tempting to spend more than you earn, it is very understandable. But it is not a good idea.”- Warren Buffett

How does a Debt start?

Let’s find how a debt starts. Some are due to your needs, some due to your desires and some due to family and societal pressure. A car or bike loan can be a need for some and a desire for some. A vacation on EMI is a desire. A home loan can be due to family pressure even if a person is not ready for such a commitment. A personal loan for a wedding or a function can also lead to debt.

At times, it can be a casual attitude towards debt and entertaining too much for instant pleasure can lead to debt. Slowly there is a time when you are too much in debt, servicing your loan and paying EMI for various things.

“Debt is like another trap, easy enough to get into, but hard enough to get out of” – Henry Wheeler Shaw

It is so true. Find how these credit facilities make you fall prey to the debt trap.

Can you answer this simple question?

Mr.A takes a loan for Rs. 40 lacs @ 11% interest for 16 years. His EMI is around Rs.44,360 per month. He pays his EMI for 5 years, so pays in total Rs. 44,360 X 12 X 5 = Rs.26,61,600. How much debt has reduced from Rs.40 lacs?

You may say his debt has reduced to a big margin, looking at the amount he has paid. No, he has only paid for 5 years, he still has to pay for 11 years that is, Rs.44,360 X 12 X 11 = Rs. 58,55,520.

Let’s see in detail.

How much debt do you owe?

Before you decide how to pay off the debt, find the total amount of debt you have. Gather the following information about your debts:

- Type of debt

- Amount owed

- Interest rate

- Minimum payment to be made

Now let’s see the debt repayment methods.

What are the Debt Repayment Methods?

1. Snowball method

This is an often-used debt reduction strategy. In the snowball method, the borrower who has more than one loan pays off the debt, starting with the smallest debt first and then the larger debts. The steps included are:

- Listing all your debts and paying the minimum due on all.

- Calculating the total remaining amount that has to be paid.

- Paying the minimum balance with the additional amount towards the smallest loan.

- Once the smallest loan is paid off, pay the additional amount and the minimum due for the next loan.

2. Debt stacking method

List down loans from the highest interest rate to the lowest interest rate. Now consider paying off the highest interest rate loan first. You should also be paying the minimum amount due on all the other loans.

Now let’s see why you should pay off your debt or the advantages of paying off debt.

8 Reasons to pay off your debt

How does paying off your debts really help?

-

It increases your financial security

-

It helps you spend on things you enjoy

-

It reduces your stress

-

It Reduces your bills

-

It improves your credit score

-

It helps you own your assets

-

It helps you keep your future income

-

It helps you be free of your lenders

Once you become debt-free, you will be able to become financially secure. You will be able to save money for emergencies and your other financial needs.

Once you pay off your debts, you can buy the things that you want without any guilt.

Debt increases stress as you keep wondering how you will be able to pay off these debts as well as other living expenses. Constant stress can even lead to heart attacks. Hence becoming debt-free can save you from stress.

Once you are debt-free you have fewer bills to pay.

Too much debt can hurt your credit score. If you become debt-free your credit score will be increased.

“Housing loan is NOT a loan on your house; it’s a loan on your future income that is secured by your house”. When you have a home loan, you don’t own the home, likewise, when you have a car loan, you don’t own the car, but the bank does. When you become debt-free, you no longer have to worry about the bank taking your assets because you are no longer able to pay it.

“A mortgaged house/ car is a liability in your balance sheet and an asset in the bank’s balance sheet”.

Whenever you borrow money, you are borrowing from your future income. The amount you borrow today will be taken from your future income. Hence it is better to be debt-free.

If you have outstanding debt, you don’t have the right to make decisions about your money, but your lenders do. In a few cases, they can increase your interest rate and minimum payment. Hence becoming debt-free helps you be in complete control of your money.

Now let’s see about EMI.

EMI (Equated Monthly Installment)

As you know EMI has two components, principal and interest. The principal is the amount you agreed to pay back. Interest is the cost of borrowing the principal. EMI is constant, but the composition of the principal and interest component keeps changing. A loan with high tenure will have a high-interest component in the starting and comes down later. There are two rules to know.

For any loan :

1. The interest component comes down as years pass.

2. The overall interest payable is high in long term loans and lesser in short term loans.

Prepayment of loans

Is there something as Prepaying for loans? What is prepayment?

Prepayment is when you pay an additional amount of principal back, ahead of time. This reduces your EMIs or your remaining loan tenure. This will make you spend less time in debt. The interest in any month is calculated based on your outstanding loan then.

Some banks allow you to prepay after a certain number of installments are paid. Some banks even charge fees for prepayment. Prepayment can be done in two ways:

1. Partial or part prepayment: Partial prepayment is when you pay off your loans in part. This helps you reduce the principal.

2. Full prepayment or pre-closure: Full prepayment is when you fully pay off your loan before the loan tenure.

How Prepayment helps you?

Now find how prepaying helps you. If you prepay your loan by a certain amount, your tenure period comes down.

Taking the initial example, let’s see how prepaying a certain amount reduces your loan tenure.

Eg : Rs.40 lacs loan @ 11% interest for 16 years tenure and EMI is Rs.44,360. Let’s say you paid EMI’s for 5 years, you will have another 11 years or 132 months to pay the remaining and after 5 years the outstanding loan will be Rs.58,55,520. At this time you can prepay some amount. Let’s see the effect of how tenure comes down if you prepay the amount at the end of the 5th year.

Here, at the end of 5 years of the loan payment, the loan outstanding is Rs.58,55,520 and you need to pay for 132 more months. Imagine you got Rs. 21 lacs and you use it for prepayment, your loan will be over in just 98 months, a reduction of 50% in the tenure.

Here, at the end of 5 years of the loan payment, the loan outstanding is Rs.58,55,520 and you need to pay for 132 more months. Imagine you got Rs. 21 lacs and you use it for prepayment, your loan will be over in just 98 months, a reduction of 50% in the tenure.

Won’t you want that?

Even if you prepay by Rs.1,77,440, you will bring down the tenure by 12 months. That’s a great relief for you. Clever home loan takers do this, as soon as they get money, they use it for prepayment and by doing so for some months or years, they finish their debt much before the scheduled tenure. Sometimes even in just 4 to 6 years.

The learning is that even a small amount of prepaid brings a big reduction in tenure. This understanding is very critical to plan for your repayment faster. Prepayment has to be done whenever possible, even a small amount towards the principal over a long time repeatedly would bring down the tenure a lot.

If you need to prepay your home loan, read this article on How to prepay your home loan in two practical ways. This link also includes two customizable calculators.

Do loans help in tax saving?

Yes, they do but tax saving should not be a reason for taking a loan. If you already have one and areenjoying the tax benefits, it is saving you money at the end of the day.

How to pay off your debt faster?

You don’t feel free? Feel something is controlling you? You want to get rid of debt as soon as possible but it traps you, where your desire to take a risky decision goes down. Getting rid of debt fast is important if you want to take a bold step, as it helps.

These are the few ways in which you can pay off your debt faster.

Ways to pay off your debt faster

- Use a monthly budget

- Look for an increase in income

- Stop swiping your credit card

- Create an emergency fund

- Have adequate insurance

- Check your spending habits

- Sell unused items

- Don’t fall into debt again

- Talk to a professional

A budget ensures you have enough money to cover your monthly expenses. It also helps you spend any extra money you are left with (after covering your expenses) towards paying off your debts.

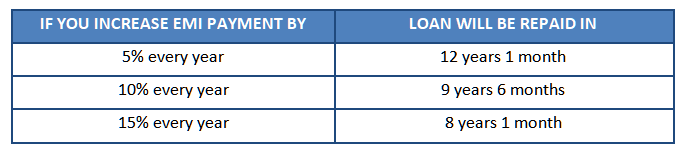

👉 Increase your EMI

You can increase your EMI amount by 5 to 6% every year. This can be done when you have an increase in salary or other annual bonuses, increments, etc.

You may ask what’s the Impact or how it makes a big difference?

If you do this you will be able to come out of your debts faster and will also be able to reduce your tenure period to a great extent. You won’t have to stay in debt for long. You will also be free from the burden and stress and have some peace of mind.

Let’s see how.

Eg. You take a loan for Rs.30,00,00 @ 9% interest for 20 years. Your EMI will be Rs.26,992. If you increase your EMI by a certain percentage every year, see how your loan tenure comes down drastically.

This is how fast or how early you can come out of your debt. Won’t you be smart enough to do this? If you do so, it would be beneficial to you. You would save a lot of time and energy.

This is how fast or how early you can come out of your debt. Won’t you be smart enough to do this? If you do so, it would be beneficial to you. You would save a lot of time and energy.

Ask for a raise in salary. Try to get a second job or a part-time job to fetch more income. Then use this income to pay off your debts. This will help you pay off your debts faster.

👉 Reduce expenses

You can’t reduce all your expenses, but you can always reduce 10%. You can aim to reduce a small amount. A big reduction is not possible as you won’t be able to do it in the long run. If you need consistency then a small amount is good enough like 10%. List down all your expenses and find which has the least value and cut down on it. Maybe you spend too much on food, clothing, accessories, or on things that are not greatly valued. Its time to restructure things and save on them.

Also if you have the habit of swiping credit cards, switch to cash. A study showed that people who used credit cards spent more than people who used cash. They spent at least 15% extra.

Even if there are cash backs or other rewards and discounts on a credit card, it’s better to avoid credit card payments.

Create an emergency fund, so in case you meet with an unexpected expense, an emergency fund would help you cover it and you wouldn’t need a loan. Ideally, this emergency fund should be 3 to 6 months worth living expenses. To know more about emergency funds click here: All about Emergency Fund Planning.

Disability, hospitalization, or damages to property can make it difficult for you to repay your debts and hence adequate insurance against such risks can help your debt repayment remain on track.

Check how much you spend daily, weekly, and monthly. This will help you recognize what you are spending more on and what are your unnecessary expenses. Then cut down on these unnecessary expenses and use it to repay your debts.

👉 Use your next increment

You can use your future increments for prepayment, if not fully at least part of it can be used. You can plan to use it only for prepayment. If you don’t want to use the full amount you can use at least 50 % of it.

👉 Sell investments

You may have invested in low return products like endowment/money back plans and also would be paying off EMI on a high-interest loan. If so, you can liquidate those low return products and use them for prepayment. You can also redirect the money that was going into low return products into loan prepayment regularly.

You can also sell old or unused things that you may have and the money from that can be used to pay off your debt.

👉 Use future inflows

You might not have the resources to currently pay off the debt, but you might be expecting income in the future like a gift from family, friends, etc. it’s a good idea to mark them for prepayment at the beginning itself. Most of them don’t do it and when they get the money, they use it for some other purpose.

👉 Take credit from friends

You take loans from banks, but not from friends and relatives. But for prepayment, you can ask if they have a surplus or extra cash and find if they can lend you at interest. Many have cash in banks like fixed deposits. If you can borrow money from them at interest, it will benefit you both.

This may not help you come out of debt but at least you won’t get worse in debt. If you keep adding debt, it will become difficult to pay off debt. Reduce your temptation to debt, by stop swiping the credit cards. All your loans combined should not be more than 40% of your take-home income. Keep this 40% as a limit and do not go beyond it.

If you can’t take debt repayment on your own, try talking to a financial planner, he can help you work through your debt problems and help you understand how to pay off debts in a smart way. He can help you develop a plan, reduce your interest costs, and get you out of debt over time. Since everyone’s finances are different a personalized plan or advice really helps.

Reduce your Interest Burden

- Choose a loan with the lowest interest rate. Interest rates can also be negotiable and you could ask your bank to lower your interest rate. Customers with good payment history are more likely to get a lower interest rate. You can even make a home loan balance transfer, to know more check this article on Home Loan Balance Transfer. The link also includes a home loan balance transfer calculator.

- You can pay one more EMI (in addition to the actual number of EMI) every year. This will reduce your loan tenure and in turn the interest cost. If you can pay one additional EMI every year, you can reduce the interest burden.

Here is an easy EMI calculator to calculate the monthly EMIs.

- Choose an EMI you can afford. Keep affordability as a primary factor when choosing your EMI.

Want to get out of debt faster? Yes? Then find the ways to get out of debt and stay out of debt. If you have a credit card, find how to pay off your credit card debt.

Should you Invest or Pay off debt?

You may have additional money, but don’t know whether to invest or pay off debt. This depends on you. How emotionally are you attached to a loan? Do loans make you uncomfortable? If yes, better get rid of it faster. If you are too afraid of taking risks and are going to keep the money in bank deposits, better pay off the loan.

To-do-list

- You can pay your loan online by linking your loan account with your bank account, this will help you prepay as soon as you are ready with the money.

- Check your bank’s restrictions on how much minimum and maximum you can prepay and include it in your repayment plan.

- Banks let you the option to either keep the EMI constant and decrease the tenure or reduce the EMI and keep the same tenure.

- You can ask your bank to increase EMI, in case of extra income, additional pay, increments, etc.

- You can also ask your bank to reduce EMI in cases like job loss, any emergencies, etc. If you had made prepayments, they might give you this option.

- If Interest rates go down, ask your bank to decrease your tenure.

Conclusion

Now you would have understood all about debts, prepayment and the advantages and effects of prepaying. It is better to pay off your debts as fast as possible because,

- You won’t have to be in debt for long

- You won’t be charged high interest

- You won’t be fined a penalty fee

- You can avoid stress

- You will get a good credit score

- You will start achieving your financial goals

- You will avoid bankruptcy and

- Get relieved from these debts.

Don’t you now think paying off all your debts help?

Many investors have used these debt repayment strategies and come out of debt. Don’t you also, want to be debt-free?

“Want to be free or enslaved? Savings: Frees your future; Borrowings: Enslaves your future.”

Pay off your debts and increase your credit score.

If you have any comments or questions, write them in the comment box below.

Or are you interested in creating a Comprehensive Financial Plan for your financial goals?

Skip the queue by registering for your 30 Minute FREE Financial Plan Consultation. Click the ‘‘BOOK YOUR SLOT NOW!’’ button below.

Thanks to you, this information becomes a priceless gem that benefits us all.