HDFC Life Super Income Plan is a non-linked participating and limited pay money-back insurance plan.

This plan comes with assured benefits and additional bonuses to plan the financial needs of an individual.

Also, this insurance plan offers guaranteed income to the policyholder for 8-15 years.

In this article, we will analyze the specific details of this plan and decide whether this insurance plan is a worthy investment in the year 2024!

Is it a good or a bad policy?

Many investors also compare this with other HDFC investment plans for 12 years or the HDFC monthly income plan to evaluate long-term income options.

Table of Contents

- How does the HDFC Life Super Income Plan work?

- HDFC Life Super Income Plan: Key Features

- HDFC Life Super Income Plan: Survival Benefits

- HDFC Life Super Income Plan: Maturity Benefit

- HDFC Life Super Income Plan: Death Benefits

- HDFC Life Super Income Plan Taxation: Are the Benefits Tax-Free?

- HDFC Life Super Income Plan: Bonuses

- HDFC Life Super Income Plan: Surrender Benefits

- HDFC Life Super Income Plan Surrender Value: What Happens If You Exit Early?

- HDFC Life Super Income Plan: Illustration and Critical Analysis

- HDFC Life Super Income Plan: Drawbacks

- Final Verdict: Should you purchase HDFC Life Super Income Plan?

- HDFC Life Super Income Plan: Commonly Asked Questions

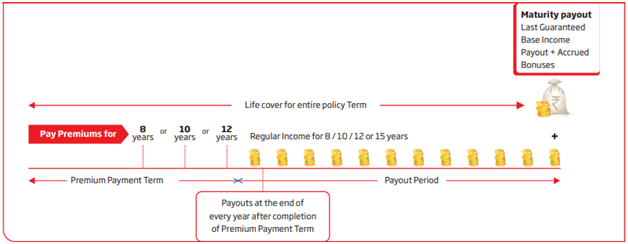

How does the HDFC Life Super Income Plan work?

You should choose to pay the premiums for 8, 10 or 12 years based on the choice of your plan.

You should choose to pay the premiums for 8, 10 or 12 years based on the choice of your plan.

You will receive the pay-outs for 8,10,12 or 15 years, based on your selection.

Plus, you will receive the Life cover for the entire policy term.

Company CLAIMS to provide the annual returns in the range of 8% – 12.5%!

The HDFC Life Super Income Plan calculator and HDFC Life Super Income Plan returns calculator are tools that help you estimate your total pay-out, bonuses, and expected survival benefits.

We will do a detailed analysis of the return on investment of this plan later in this post.

Many investors exploring HDFC Life investment plans or evaluating whether HDFC Life Super Income Plan is a good investment option often start by understanding how this structured income plan actually works.

Investors comparing HDFC Life Super Income Plan with other HDFC Lifesaving plans, HDFC guaranteed income plans, and HDFC monthly income plans often evaluate the expected pay-out schedule before making a decision.

HDFC Life Super Income Plan: Key Features

1.After completing your Premium payment term in this plan, you will get regular monthly or yearly income for a period of 8 to 15 years, along with insurance coverage throughout the policy term.

This structure is designed for policyholders looking for predictable cash flow through a life insurance income plan rather than a market-linked investment product.

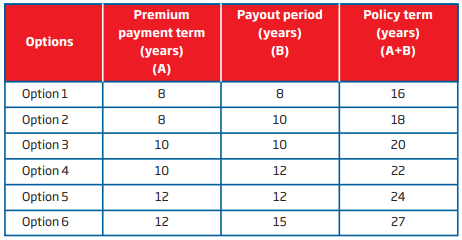

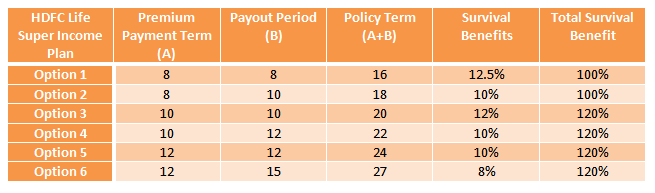

2. Range of premium payment and policy term options are available.

Below are the 6 options. You should choose any one of the 6 options.

3. Survival Benefits varying from 8% to 12.5% of the Sum Assured are payable on Maturity each year during the pay-out period.

3. Survival Benefits varying from 8% to 12.5% of the Sum Assured are payable on Maturity each year during the pay-out period.

8% to 12.5% seems to be high return as claimed by the company.

We will do our detailed analysis of this claim later in this post.

The Sum assured is known to the policyholder at the inception and paid by the insurer at the end of the year during the pay-out period.

Details on Survival benefits are described in the next section.

Investors also check HDFC Life Super Income Plan pdf, HDFC Life Super Income Plan brochure, and HDFC Life Super Income Plan features to understand terms and benefits before investing.

Those evaluating HDFC Life insurance plans for 10 years or HDFC investment plans for 12 years frequently review the policy brochure to compare premium commitments and income benefits across available options.

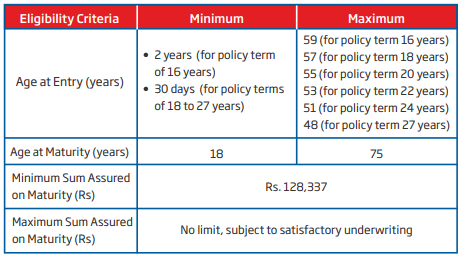

4. Eligibility criteria, age at entry and minimum sum assured is given in the table below:

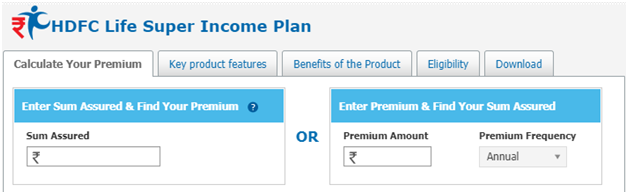

5. You can calculate the Sum Assured from HDFC Life online calculator.

You will find a dashboard as shown below, where you can enter your premium amount and frequency to get the Sum Assured.

Or, you can enter your desired Sum Assured to get your Premium Amount to be paid.

The HDFC Life Super Income Plan calculator Excel tool is another way to simulate different investment scenarios, pay-out options, and bonus structures. Such tools help investors compare projected HDFC Life Super Income Plan returns with other long-term savings or insurance investment plans.

Such tools help investors compare projected HDFC Life Super Income Plan returns with other long-term savings or insurance investment plans.

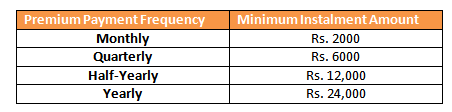

6. You can choose to pay the premiums as per your choice. You can choose to pay the premiums either monthly, quarterly, half-yearly, or yearly.

The below table shows the Premium Payment Frequency with a minimum installment amount. There is no upper limit for the Maximum Installment amount.

There is no upper limit for the Maximum Installment amount.

7. Opportunity to avail many other benefits and bonuses

In the next section, we will analyze the key benefits and bonuses provided by HDFC Life Super Income Insurance Plan.

At this point, let’s have a look at the short video illustration on the review of the HDFC Life Super Income Plan.

This video briefly reviews all the essential aspects of this plan.

Policyholders often compare HDFC Life Super Income Plan pay-out, HDFC Life Super Income Plan example, and HDFC Life Super Income Plan maturity calculator to estimate income flow.

The HDFC Life Super Income Plan pay-out structure is one of the key reasons retirees and conservative investors consider it as a potential fixed income plan for future cash-flow needs.

Understanding these projections helps investors decide whether the HDFC Life Super Income Plan fits their retirement income planning or long-term financial goals.

HDFC Life Super Income Plan: Survival Benefits

This benefit is expressed as the percentage of the total sum assured amount on maturity.

According to the company’s claim, you will get 100% or 120% of the Sum Assured on Maturity, during the pay-out period.

The percentage depends on your variant. The benefit is spread evenly across the pay-out term.

(Remember: 100% or 120% is not returns. This includes the principal also. That is this includes the premium you have paid.)

- Survival Benefits are paid every year during a pay-out period which is after the completion of the premium payment period. They are expressed as the percentage of Sum Assured on Maturity.

- Total Survival Benefits are calculated as Survival Benefits per year multiplied by their respective pay-out period.

- Premium Payment Term (A) + Pay-out Term(B) = Policy Term (A+B)

Look at the table below to know about the Survival Benefit percentages:

Many investors also check HDFC Life Super Income Plan benefits and HDFC Life Super Income Plan review before investing to understand potential returns and structure.

These survival benefits are often highlighted in HDFC Life Super Income Plan benefit illustrations to demonstrate how periodic income is distributed throughout the pay-out phase.

For a detailed analysis of survival benefits, refer to Illustrative example discussed later in this post.

HDFC Life Super Income Plan: Maturity Benefit

At maturity, all the outstanding premiums have been paid off. Maturity Benefit consists of:

- Last survival benefit pay-out

- Accrued reversionary bonuses

- Interim bonuses (if any)

- Terminal bonuses (if any)

The last installment of survival benefit is paid along with the payment of maturity benefit.

HDFC Life Super Income Plan maturity calculator and HDFC Super Income Plan maturity calculator help you estimate the final maturity amount along with bonuses and survival benefits.

Investors often review HDFC Life Super Income Plan maturity value

projections to understand the overall pay-out structure at the end of the

policy term.

HDFC Life Super Income Plan: Death Benefits

In the event of the demise of the policyholder during the policy term, the nominee will get:

- Sum Assured on Death

- Accrued reversionary bonuses

- Interim bonus (if any)

- Terminal bonus (if any)

Sum Assured on Death shall be the higher of:

1. Sum Assured on Maturity

2. 10 times Annualised Premium for entry age up to 50 years or 7 times Annualised Premium for entry age greater than 50 years

As you can see that there are two components to the calculation of death benefits.

The first component is Sum Assured on maturity.

The second component is a multiple of your premium, 10 times annual premium if your entry age is up to 50 years and 7 times annual premium if your entry age is over 50 years.

For example, If you choose to invest in option 3 of the HDFC Life Super Income Plan, estimated death benefits will be described as follows: No further survival benefits shall be paid after the demise of the policyholder.

No further survival benefits shall be paid after the demise of the policyholder.

Investors often refer to HDFC Life Super Income Plan death, HDFC Life Super Income Plan surrender value, and HDFC Life Super Income Plan review to understand coverage and risk.

Compared with a pure HDFC Life monthly income plan, the Super Income Plan combines insurance protection with future income benefits under a single policy structure.

The death benefit component is what differentiates this policy from pure investment products, as it combines income benefits with life insurance protection.

HDFC Life Super Income Plan Taxation: Are the Benefits Tax-Free?

Premiums paid towards the HDFC Life Super Income Plan may qualify for tax deductions under Section 80C, subject to applicable tax rules.

In addition, maturity benefits, survival benefits, and death benefits may receive tax treatment under Section 10(10D), depending on whether the policy meets the prescribed conditions.

However, tax savings alone should not be the deciding factor.

Investors should evaluate the plan based on overall returns, liquidity, surrender value, and long-term suitability.

A tax-efficient product is beneficial only when it also aligns with your financial goals and return expectations.

Let’s discuss bonuses now.

HDFC Life Super Income Plan: Bonuses

The following are the types of bonuses provided by the insurer along with this life insurance plan:

Reversionary Bonus:

- This bonus is declared by the insurer at the end of the financial year.

- It is expressed as the percentage of the sum assured amount on maturity.

- This bonus is NOT an assured benefit as it usually depends on several factors. But, once it is added, it is guaranteed to be payable.

- In case of policy surrender or unexpected demise of the policyholder during the inter-valuable duration, the insurance plan will be eligible to get interim bonuses as per the terms and conditions of the insurance company.

- Please note that these bonuses are in the future value of maturity and not in the present value. So this will NOT have the compounding effect.

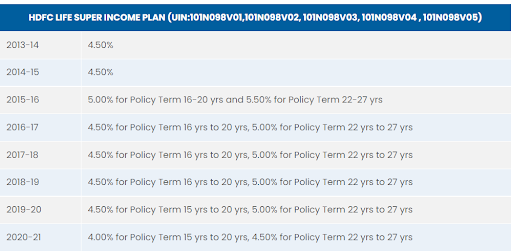

- Current Reversionary bonus rates are given as follows:

Let’s say your Policy Term is 20 years, you will get a simple reversionary bonus of 4.5% of the sum assured. Assume that in our policy, we are taking the sum assured on maturity to be Rs. 10,00,000.

Therefore, the annual bonus will be Rs 45,000 per annum. You will get this benefit at the time of policy maturity.

For 20-year policy term, you will get the reversionary bonus, Rs 45,000 * 20 = Rs 9 lacs

Terminal Bonus:

- This bonus may also be added to an insurance plan and enables the service provider to pay a share of the surplus offered.

- Just like the reversionary bonus, this benefit is also not assured and depends on the company policies and actual future experience.

Its value is not fixed, but we will find the terminal bonus with some assumptions and approximations later in the illustration.

These bonus structures are often highlighted in the HDFC Life Super Income Plan brochure to demonstrate potential long-term policy benefits.

Many policyholders also review the HDFC Life bonus chart and historical bonus declarations to understand how participating policies have performed over different market cycles.

HDFC Life Super Income Plan: Surrender benefits

If your policy term is 8 years and the policy is counted for 2 complete years, it will acquire guaranteed surrender value which is the total of a % of total premium paid and accrued bonuses.

Policyholders can use the HDFC Life Super Income Plan surrender value calculator to estimate the exact amount they can withdraw if they choose to surrender the policy before maturity.

Understanding surrender value calculations helps policyholders assess the liquidity aspect of the HDFC Life Super Income Plan before committing to a long policy tenure.

HDFC Life Super Income Plan Surrender Value: What Happens If You Exit Early?

Many investors later realize they may need liquidity before the policy term ends.

In such situations, understanding the HDFC Life Super Income Plan surrender value becomes important.

The policy generally acquires surrender value only after a minimum number of premiums are paid.

Once eligible, the policyholder may receive either the Guaranteed Surrender Value (GSV) or the Special Surrender Value (SSV), depending on the insurer’s calculations and the policy duration.

The guaranteed surrender value is usually calculated as a percentage of the total premiums paid (excluding taxes and rider premiums) and increases gradually as the policy progresses.

Some investors use the HDFC Life Super Income Plan surrender value calculator to estimate the possible amount they may receive if they exit the policy early.

However, surrendering during the initial years may result in a significantly lower pay-out because a portion of the premiums goes towards policy expenses, commissions, and administrative costs.

This is why investors should carefully evaluate long-term commitments before choosing traditional income plans and understand the financial impact of exiting the policy before maturity.

Availability of Policy Loan:

Once an insurance policy acquires its surrender value, the policy owner may avail the facility of policy loan which is up to 80% of the policy’s surrender value.

This makes HDFC Life Super Income Plan a flexible tool, as it allows partial liquidity while still keeping the insurance coverage active.

The policy loan facility is another feature often discussed in detailed HDFC Life Super Income Plan reviews, especially by investors looking for liquidity options during the policy term.

HDFC Life Super Income Plan: Illustration and Critical Analysis

Let us say, you choose a policy term of 20 years, as provided in option 3 with an assured sum of Rs. 10 Lacs.

To get the sum assured of Rs. 10 Lacs, you have to pay the annual premium of Rs. 1,35,829 for 10 years.

And, if you want illness cover, then you have to pay the extra sum of Rs. 1,690 p.a. and your annual premium will be Rs. 1,37,519 for 10 years.

Note: Calculations are done using the online calculator of HDFC Life.

Many investors reviewing the HDFC Life Super Income Plan benefit illustration often use the company calculator to estimate how premiums translate into pay-outs and maturity benefits over the policy term.

Tools such as the HDFC Life Super Income Plan returns calculator help investors estimate whether the projected income stream aligns with their long-term retirement objectives.

You will receive the benefits after 10 years, as shown in the table below.

In the previous section, we calculated the reversionary bonus, which equals Rs. 9,00,000. The above illustration shows the maturity benefit is approx. Rs. 16,70,000. It means the terminal bonuses will be approx. Rs. 7.7 Lacs (16.7Lacs – 9Lacs).

The table shown below highlights overall inflow and outflow over the 20-year policy term.

We will find out how much returns you may get on maturity! Your return for this 20-year investment is 6% p.a. (with assumptions).

Your return for this 20-year investment is 6% p.a. (with assumptions).

Even though this plan CLAIMS the benefits in the high range of 8.5% and 12%.

You are ONLY getting a return of 6%.

Note: the bonuses are non-guaranteed benefits and they may vary with the performance of company in the market and may vary each year!

Although HDFC Life Super Income Plan claims annual returns in the range of 8.5% to 12%, the effective returns in this scenario are 6% p.a., emphasizing that the bonuses are non-guaranteed and fluctuate based on company performance.

Such examples clearly show why investors often analyse the actual

HDFC Life Super Income Plan returns rather than relying only on

projected bonus illustrations.

This illustrates why many financial planners suggest comparing the HDFC Life Super Income Plan with other HDFC Life investment plans for 10 or 12 years, mutual fund SIPs, or even PPF for better risk-adjusted returns.

HDFC Life Super Income Plan: Drawbacks

1. Hidden costs and non-guaranteed benefits.

- The commission is being paid to agents. In the first year, it is around 30%, thereafter it is around 5% in the upcoming years.

- Transparency: When you pay your premium, you will have no clue about how much goes towards expenses, how much is getting invested and where it is getting invested. It is completely not transparent. Whereas in mutual fund investment, expenses are low and they are more transparent.

- Unlike mutual funds, where expense ratios and fund allocations are regulated by SEBI, HDFC Life Super Income Plan expenses are regulated under IRDA rules, which are less investor-focused.

- Comparatively, SEBI (regulator of mutual funds) is more proactive in stopping misspelling by agents. IRDA (regulator of Insurance) follows the same commission structure to agents which got decided in 2016. SEBI revised the expense ratio limit multiple times and even in April 2019, there was a downward revision of expense ratio limits that hugely benefitted mutual fund investors.

- Marketing expenses: costs involved in advertising and various incentives are given to the marketing team.

- Policy operational expenses.

Many such costs are summed up and deducted from the premiums paid by the customers.

It will take more than five years for the policy to recover these expenses from the returns generated.

That’s why in the first five years the surrender charges are less than the premiums you paid. That means literally there are no returns for the first three to five years.

Also, the benefits provided by this plan during maturity are not guaranteed.

These hidden costs are one of the main reasons many independent

HDFC Life Super Income Plan reviews highlight lower effective returns

compared to transparent investment products.

2. Low returns (6%), as calculated in the above illustration.

- Such lower returns can’t even beat inflation for 20 long years.

- Mutual funds can give much better returns with fewer risks.

- Even PPF can give guaranteed returns in the range of 8%!

3. For a given assured sum, the annual premium is high and has increased further over the years.

4. Most of the calculations are done by HDFC Life Calculator, and the basis of this calculation is unclear.

Instead of investing in HDFC Life Super Income Plan; with the same amount of investment in the combination of Mutual Fund and Term Insurance Plan you will achieve much better benefits.

In essence, while HDFC Life Super Income Plan offers the appeal of structured pay-outs and insurance coverage, separating investment and insurance through a combination of mutual funds and term insurance can provide better returns and flexibility.

This approach allows investors to achieve higher wealth creation potential while still maintaining adequate life insurance coverage through a pure term insurance policy.

HDFC Life Super Income Plan Vs Mutual Funds and SIPs

When comparing HDFC Life Super Income Plan with mutual funds or SIPs (Systematic Investment Plans), several key differences become apparent:

1. Returns:

- HDFC Life Super Income Plan offers guaranteed survival benefits along with non-guaranteed bonuses. However, as seen in illustrative examples, the effective returns often range around 5–6% p.a., which may not even beat inflation over long durations.

- Mutual funds, especially equity or balanced funds, historically offer higher long-term returns, often 8–15% CAGR, depending on market conditions. SIPs allow disciplined investing and benefit from rupee-cost averaging and compounding over time.

- For long-term investors focused on wealth creation, SIP investing in diversified mutual funds often provides better compounding compared to traditional income insurance plans.

- This is one reason why many financial planners prefer combining term insurance with SIP investments instead of relying solely on traditional income insurance products.

2. Liquidity:

- Withdrawals from HDFC Life Super Income Plan are limited. Surrendering the policy before the premium payment term may result in lower surrender value and delayed access to funds.

- Mutual funds and SIPs are generally liquid, with the ability to redeem units partially or fully as per the investor’s needs, making them more flexible for short- or medium-term financial goals.

3. Transparency and Costs:

- HDFC Life Super Income Plan has multiple hidden charges, such as agent commissions, marketing costs, and policy operation expenses, which reduce net returns.

- Mutual funds have a regulated expense ratio, low transparency issues, and are monitored by SEBI, providing greater clarity for investors.

4. Insurance Component:

- HDFC Life Super Income Plan combines insurance with investment, which is useful for those looking for structured pay-outs and life cover together.

- Mutual funds or SIPs do not provide insurance; however, combining them with a term insurance plan can often provide higher returns and better life cover than a single endowment-type policy.

5. Compounding and Growth Potential:

- Super Income Plan pay-outs are structured and do not allow compounding, as money is periodically withdrawn.

- Mutual funds invested via SIPs allow your wealth to compound over time, which can significantly increase corpus size for long-term goals like retirement, children’s education, or wealth accumulation.

In summary, while HDFC Life Super Income Plan can be suitable for investors seeking guaranteed pay-outs along with insurance, mutual funds and SIPs generally offer higher returns, liquidity, transparency, and compounding benefits, making them more suitable for building wealth over the long term.

Final Verdict: Should you purchase HDFC Life Super Income Plan?

In short, the answer is NO.

While HDFC Life Super Income Plan provides guaranteed survival benefits, the reversionary and terminal bonuses are non-guaranteed and may not benefit from compounding.

As you have noticed in the above analysis that the Survival Benefits, though they are guaranteed, rates are being reducing every year!

Reversionary and Terminal bonuses are NOT assured bonuses; they depend on the profit that the company makes in that duration and many other hidden factors.

These bonuses don’t get the compounding effect.

All you need is better returns on your investment and good insurance, right?

So, instead of opting for HDFC Life Super Income Plan, you must consider keeping your investment and insurance separate.

With the same amount of investment, you will achieve much higher returns and better insurance benefits.

This strategy is widely recommended in financial planning because it

allows investments to grow independently while maintaining adequate

protection through a dedicated life insurance policy.

Financially savvy investors should always consider the HDFC Life Super Income Plan review, HDFC Life Super Income Plan bonus history, and HDFC Life Super Income Plan pay-out options before making a decision.

Reviewing the HDFC Life Super Income Plan benefits, surrender conditions, and projected maturity values can help investors make a more informed decision before committing to a long-term policy.

Finally, don’t get into the trap of some 3rd party websites endorsing such a plan or your own bank’s relationship manager misselling this policy as they get the commission for each sale of the policy.

HDFC Life Super Income Plan: Commonly Asked Questions

1. What are the guaranteed returns in HDFC Life Super Income Plan?

Survival Benefits are guaranteed. Whereas the reversionary and terminal bonuses are not guaranteed, their amount may vary from time to time.

This is an important distinction because guaranteed survival benefits

should not be confused with overall investment returns.

2. What will happen if you stop paying the premiums?

If you stop paying the premiums, the insurance policy will still continue but with the reduced benefits.

However, you should revive it within two years from the date of their first unpaid premium. Otherwise, it lapses.

3. What is Free-look period of HDFC Life Super Income Plan?

The Free-look period is 15 days from the date of receipt of the policy.

The Free-look period for the policies purchased through Distance Marketing will be 30 Days from the date of the receipt.

Please note, Distance marketing refers to the policies sold through telephone or online or any other method which do not involve face-to-face selling.

You can cancel the policy during the free look-in period. The premium will be refunded without any questions.

If your Bank relationship manager has missold this policy, you may exercise this option before the free look-in period.

4. How to cancel HDFC Life Super Income Plan?

You can cancel the plan within the free look in period of 15/30 days, your premium will be refunded but they are subject to deduction of the:

- The proportionate risk premium for the period on cover,

- The expenses incurred by the company on medical examination (if any) and

- Stamp duty.

In OFFLINE Mode you can fill & submit the Mandate Deactivation Form available at any HDFC Life branch.

In ONLINE Mode you may send an email at: atservice@hdfclife.com from your registered email ID and request for deactivation.

A policy once returned shall not be revived, reinstated, or restored at any point in time and a new proposal will have to be made for a new policy.

You can also explore HDFC Life Super Income Plan pdf and HDFC Life Super Income Plan brochure for more details on terms, bonus structure, and maturity calculations.

Reviewing the policy document carefully helps investors fully understand

the pay-out structure, surrender conditions, and bonus mechanisms

before making a long-term commitment.

If you have any comments or questions, write them in the comment box below.

Or are you interested in creating a Comprehensive Financial Plan for your financial goals?

Skip the queue by registering for your 30 Minute FREE Financial Plan Consultation. Click the ‘‘BOOK YOUR SLOT NOW!’’ button below.

Sir, I am S P Vaijayanthy.my hdfclife super income plan policy number 19040713. I have paid my premium starting from 2017. Premium amount is 50000/ annually.my plan is 8+8 years.my last premium paid on 21/02/2024.please.let me know the benefits I will get.Reply

Hi

I have paid 2 premiums for this . What should I do?

Since you have already taken this insurance plan, then you have two options.

Option: 1 You can surrender and encash the policy. And reinvest the surrender value and future premium money with better investment plans like PPF or MF.

Option: 2 You can continue with the insurance plan until the policy matures.

It is advisable to work out the outcome of both options and proceed with the better option.

80% of the time, option 1 is better.

You can consult a financial planner to choose the better option.

Or

You can take advantage of our free complimentary financial plan consultation and talk to our financial planners.

Get your appointment here: https://www.holisticinvestment.in/complimentary-financial-plan-consultation/

How much return I will get after cancellation of HDFC super income policy after three years?

Premium amount ₹1 lakh

Please check with your financial planner.

You can also book a slot with our financial planner for an initial complimentary consultation.

https://www.holisticinvestment.in/complimentary-financial-plan-consultation/

Hi, I have taken Hdfc life super income plan and its been 5 years already.

My question is-

If I plan to discontinue with the said plan now after 5 years, I would like to know where will my pay-off and maturity benefits stand?

It will be calculated based on the premium you paid and the policy term.

Thanks

You’re welcome.

Dear Sir/Madam,

I had bought a HDFC life Super income plan for 16 years (8 years premium payment) in 2019. Now I felt the premium is more than the benefits we get. If i opt to surrender the policy, I get very less amount. I am contacting them regularly to make some change in the policy But, HDFC is not replying properly.

I have two doubts:

1. I couldn’t see the payment of Terminal bonuses anywhere. Have they really

paid.

2. Is there anyway we can alter or reduce the premium payment. The insurer

can reduce the benefits accordingly. for eg. I can continue paying premium upto 4 years instead of 8 years and the insurer can reduce the benefits by 50%.

Kindly assist to give me some solution.

Kind regards,

Radhakrishnan Meyyappan

Since you have already taken this insurance plan, then you have two options.

Option: 1 You can surrender and encash the policy. And reinvest the surrender value and future premium money with better investment plans like PPF or MF.

Option: 2 You can continue with the insurance plan until the policy matures.

It is advisable to work out the outcome of both options and proceed with the better option.

80% of the time, option 1 is better.

You can consult a financial planner to choose the better option.

Or

You can take advantage of our free complimentary financial plan consultation and talk to our financial planners.

Get your appointment here: https://www.holisticinvestment.in/complimentary-financial-plan-consultation/

I pay only first year premium of Rs 70000 for a12+12 year plan after believing the agent and stopped there after knowing the drawbacks.. They asked me to continue three more years mo

…should it be beneficial? What’s is the paid up value after 5 years

Since you have already taken this insurance plan, then you have two options.

Option: 1 You can surrender and encash the policy. And reinvest the surrender value and future premium money with better investment plans like PPF or MF.

Option: 2 You can continue with the insurance plan until the policy matures.

It is advisable to work out the outcome of both options and proceed with the better option.

80% of the time, option 1 is better.

You can consult a financial planner to choose the better option.

Or

You can take advantage of our free complimentary financial plan consultation and talk to our financial planners.

Get your appointment here: https://www.holisticinvestment.in/complimentary-financial-plan-consultation/

Mr. Pradeep Kumar (141875) Mobile No. 8929618704 and Ms. Siddhi Agarwal Mobile No. 7766926172 has cheated me. They sold me HDFC Life policy along with benefit of medical policy with OPD facility in the month of Jan20. For this policy I forced to my husband to cancel Apollo Munich Optima Restore Personal Family Medical Floater policy. My husband cancelled Apollo Munich Optima Restore Personal Family Medical Floater policy and invested in the said policy.

Today company is not fulfilling the commitment and my family is unsafe due to no health protection.

I want to request you to beware from cheater employees Mr. Pradeep Kumar (141875) Mobile No. 8929618704 and Ms. Siddhi Agarwal Mobile No. 7766926172.

You can approach the HDFC grievance redressal officer to file your complaint or you can approach IRDA to file a complaint if you have not received any response from HDFC.

Grievance Cell (irdai.gov.in)

Dear Sir,

I purchased a policy “HDFC Life Super Income Plan”. This was a false selling of HDFC Life Super Income Plan (Option 1) (HDFC306560R) by an advisor Ajay Mathur +91 9350822357. Before selling this policy he promised to return 40% of the first payment and 10% relaxation in the subsequent payments. Along with this, he promised to give a 5000/- brochure to be purchase thing from certain stores. He also committed to giving these things in writing in the policy draft.

After that, he did not deliver any policy draft and denied to give all these benefits. I wish to cancel my policy and to file a case against this guy as soon as possible so that I can manage my fund for my better future.

Thanking you.

You can approach the HDFC grievance redressal officer to file your complaint or you can approach IRDA to file a complaint if you have not received any response from HDFC.

As for cancelling your HDFC Life insurance, this video can help you!

https://youtu.be/K8rFZLwHjcc

Hi,

What would I do to deactivate my super income policy. I am under option 5 and I paid one premium on 2019. I don’t want to pursue this policy anymore. Would they refund any amount that I paid. And how can I deactivate it online as I am residing in Canada. Hope to hear from you. Thank you.

Please check with your financial planner.

You can also book a slot with our financial planner for an initial complimentary consultation.

https://www.holisticinvestment.in/complimentary-financial-plan-consultation/

I am 58 yes old retired person. Will the HDFC sanchay par advantage be good for me , ifI deposit 1.5 Lac per annum for six years

Please check with your financial planner.

You can also book a slot with our financial planner for an initial complimentary consultation.

https://www.holisticinvestment.in/complimentary-financial-plan-consultation/