Insurance is precautionary, Investments are progressive.

ULIPs are apparently a fusion—they are insurance investments. But more often, a combination of products would nullify each other’s advantages.

HDFC Life ProGrowth Plus is one such insurance plan that offers the insurers a Sum Assured as benefit or fund value on successful completion of policy term.

Is it worthy to invest in HDFC Life ProGrowth Plus?

We will see the insights to how the HDFC Life ProGrowth Plus works and come to a conclusion in this review of HDFC Life ProGrowth Plus.

Table of Contents

- Review of HDFC Life ProGrowth Plus: Basic Features

- Review of HDFC Life ProGrowth Plus: Investment Features

- A Quick Review of HDFC Life

- Reviewing Benefits of HDFC Life ProGrowth Plus

- NAV Review and Analysis of HDFC ProGrowth Plus’ Funds

- Different Charges Levied in HDFC Life ProGrowth Plus

- Is It a Reasonable Trade-Off or a Hook?

- Is HDFC Life ProGrowth Plus Really Tax Free?

- Red Flags in HDFC Life ProGrowth Plus

- Verdict

Review of HDFC Life ProGrowth Plus: Basic Features

HDFC Life ProGrowth offers two different plan benefit options to choose from.

As you can see, Extra Life Option is only an enhanced version of the Life Option which increases the Sum Assured.

As you can see, Extra Life Option is only an enhanced version of the Life Option which increases the Sum Assured.

So, what does the Death Benefit has to offer for the insured?

Death Benefit: The benefit will be either Sum Assured or Unit Fund Value or Minimum Death Benefit; whichever is higher will be paid as benefit.

Extra Life Option Benefit: The benefit will be the eligible—higher—‘Death Benefit’ along with the ‘Additional Sum Assured’.

Many investors exploring HDFC Life ProGrowth Plus policy details often assume that higher sum assured automatically translates into stronger protection, which is not always true in ULIP plans.

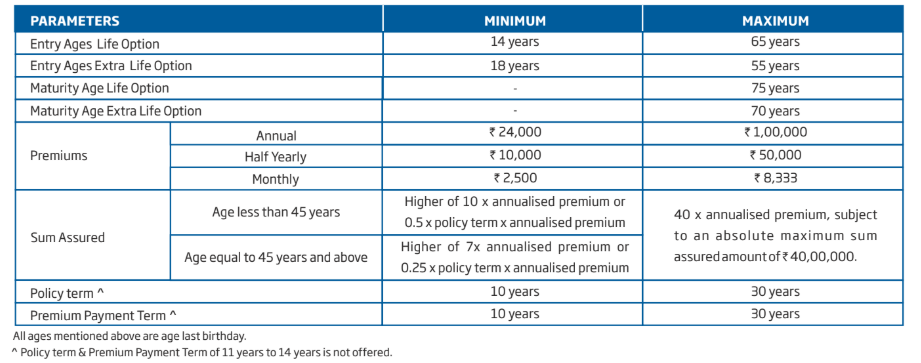

See the image below for the age eligibility, Maturity age, Policy term, Premium prices and other basic details.

Review of HDFC Life ProGrowth Plus: Investment Features

Investment feature is a vital part of any ULIP.

HDFC Life ProGrowth Plus offers 8 different funds for the insured to choose.

See the table below for the funds offered in HDFC Life ProGrowth Plus. The funds offered vary on asset allocation which in turn impacts their return and risk potential. The Debt instruments invest in Money market instruments, Government bonds, Bonds, etc.

The funds offered vary on asset allocation which in turn impacts their return and risk potential. The Debt instruments invest in Money market instruments, Government bonds, Bonds, etc.

From this list of funds, an investor will be required to choose 4 funds in which their premium can be invested.

Popular choices under HDFC Life ProGrowth Plus include the Opportunities Fund, Blue Chip Fund, Discovery Fund, and balanced fund variants depending on the investor’s risk appetite and investment horizon.

Here’s an overview of HDFC Life and their service over the years.

A Quick Review of HDFC Life

HDFC Life is a joint venture between HDFC Ltd and the UK based investment company Standard Life Aberdeen PLC.

HDFC Life—headquartered in Mumbai—is the first private sector insurance company in India. It was established in the year 2000.

HDFC Life provides a range of insurance plans such as Term plans, Health plans, Children’s plans, Women’s plans, ULIP plans, NRI insurance plans, etc. HDFC Life also launched insurance plans that can be bought online.

But when it comes to the merit of an Insurer, one must take the Claim Settlement Ratio into consideration. What is HDFC Life’s Claim Settlement Ratio?

Claim settlement ratio is the ratio between the total claims settled to the total number of claim requests received. A higher claim ratio would mean that the rate of rejection of insurance claims is minimal, which is a desirable quality in an insurance company.

As per IRDAI report for the year 2018-2019, HDFC Life has a Claim Settlement Ratio of 99.04%.

It is an impressive figure and should justify the reputation HDFC Life has earned over the years.

Apart from claim settlement performance, many investors also compare HDFC Life ULIP fund performance charts and fund fact sheets before choosing a policy.

Reviewing Benefits of HDFC Life ProGrowth Plus

Does the insuring company’s good reputation guarantee that this HDFC Life ProGrowth Plus is a good product too?

Not really, one must see of the benefits for the premiums paid are optimal if not best. It is because investments secure your finances and life insurance secures your family’s finances—you cannot make any compromise on neither.

Different benefit of the HDFC Life ProGrowth Plus is claimed in two different scenarios.

i) Scenario 1: Insured Dies While Policy is in Effect

ii) Scenario 2: Insured Successfully Completes the Policy Term

What kind of benefit the insured—or his nominee—will get in these scenarios?

Let us see this with an example: of Mr. Ashwin, who is a 30-year-old working as an Operations Officer.

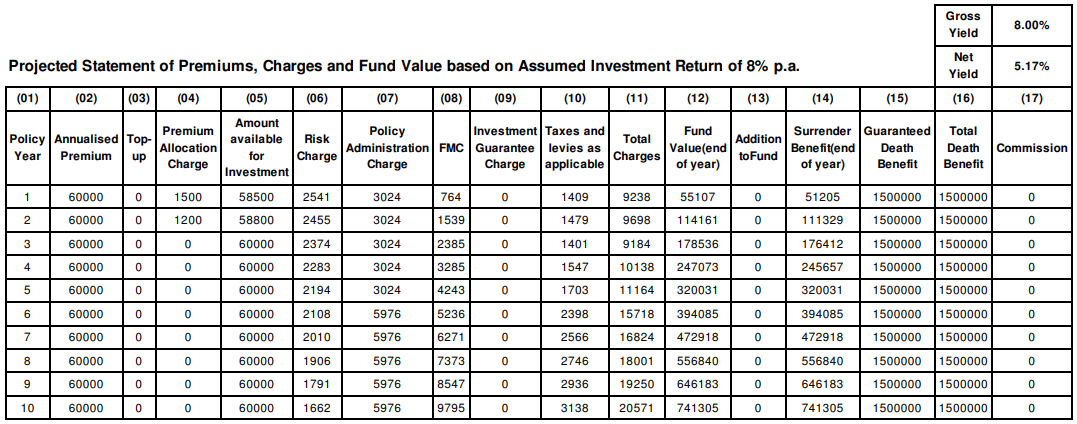

Ashwin has bought the HDFC Life ProGrowth Plus for a policy term and Sum Assured as shown in the table below.

Scenario 1: Insured Dies While Policy is in Effect

In this scenario, Ashwin’s nominee will receive a sum of ₹15 lakhs as the Sum Assured. Provided, the fund value will definitely be lesser than the sum assured since equity investments require long term to reap benefits.

If the insured dies in the initial years—even though the insured will not have paid much as premium—the Sum Assured is far less compared to a term insurance plan.

Here, the ₹15 lakhs of Sum Assured will be more or less only around his earning per annum. And if the insured happens to die in the later years—say 7th or 8th year, he will have paid quite some amount as premium.

Yet, the Sum Assured will be the same after several years. That is, the insurance benefits are on the decline as the insurance policy progresses.

For example: If the insured happens to die in the 7th year, total premium paid will be ₹4,20,000. In reality the actual benefit is only ₹10,80,000 in addition to the premiums you have paid.

On the other hand, a term insurance plan can provide life cover of ₹1Crore with almost the same amount charged as Risk Charge in HDFC Life ProGrowth Plus or any other ULIP. We will see the risk charges for the said insurance plan of Ashwin in HDFC Life ProGrowth Plus in the following section.

The gap between Sum Assured of ₹15 lakhs in HDFC Life ProGrowth Plus to the Sum Assured of ₹1 Crore of a term plan is greater than 600%.

The meagre Sum Assured compared to a term insurance plan shows that not only HDFC Life ProGrowth Plus but all other ULIPs are a lousy insurance product.

This is one of the key reasons why many financial planners question whether HDFC ULIP plans are truly effective as standalone insurance solutions.

But what if Ashwin survives till the maturity of the policy?

Will the Fund value give deliver the best investment returns for Ashwin?

Scenario 2: Insured Successfully Completes the Policy Term

In case of Ashwin surviving the policy term of 10 years, he will be paid the fund value as per the NAV on the date of policy maturity.

HDFC Life ProGrowth Plus also gives the insurer the choice to choose from 8 different funds to invest their premium. The list of funds ranges from low risk debt funds to high risk equity funds, including balanced funds with moderately high risks.

For the said policy term, premium and Sum Assured, HDFC Life suggests (not assures) a fund value of ₹7.41 lakhs at maturity with a return rate of 8% per annum.

See the table below. As you can see, the premium amount ₹60,000 is not completely invested in the funds. Instead, premium allocation charge is deducted at 2.5% for the first two years. This reduces the investment capital.

As you can see, the premium amount ₹60,000 is not completely invested in the funds. Instead, premium allocation charge is deducted at 2.5% for the first two years. This reduces the investment capital.

In addition, your investment units will be cancelled for other charges such as Policy Administration Charge, Risk Charge, Fund Management Charge, etc.

This effectively will reduce the returns potential of your investments in the consequent years.

Many investors using the HDFC Life ProGrowth Plus calculator fail to account for these layered ULIP charges while estimating long-term returns.

NAV Review and Analysis of HDFC ProGrowth Plus’ Funds

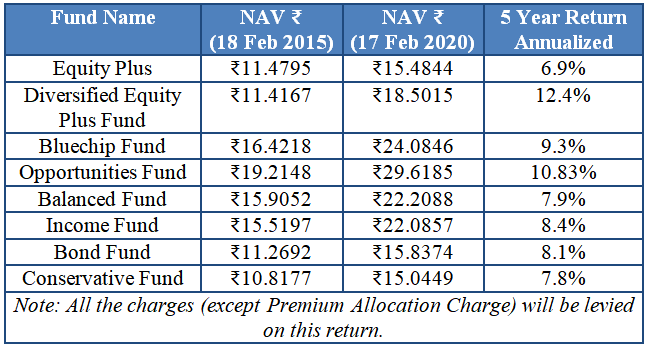

Let’s review the returns of the funds HDFC Life ProGrowth Plus has produced over the past 5 years.

The table below shows the HDFC ProGrowth Plus NAV for all the funds on 17th Feb 2023 and 18th Feb 2015 with respective 5 year return rate. From the table, the top 4 funds are high risk funds which are exposed to higher ratio equities for higher returns. But, even for such high risk, they have generated only 9.8%—a 5-year average annualized return.

From the table, the top 4 funds are high risk funds which are exposed to higher ratio equities for higher returns. But, even for such high risk, they have generated only 9.8%—a 5-year average annualized return.

Besides, on this return different charges like Fund Management Charge, Risk Charge, etc. will be levied. It will bring down the return rate even further.

Investors reviewing HDFC Life ProGrowth Plus returns last 5 years and HDFC Life ULIP returns last 10 years should compare post-charge returns instead of headline NAV growth alone.

For example: Let’s see the ratio of charges levied for Ashwin as taken from the illustration table. Also, I have excluded the premium allocation charge since it is deducted before unit allocation. An effective return of 7.86% per annum is a rate offered by low risk investments like PPF and FDs.

An effective return of 7.86% per annum is a rate offered by low risk investments like PPF and FDs.

See the table below for returns on different investment instruments in comparison to HDFC ProGrowth Plus.

You can see that the investments that give assured returns, that is investments with very low risk are on par with the high risk equity linked ULIP.

This comparison raises an important question for investors — is HDFC ULIP good enough to justify the additional lock-in, charges, and insurance costs compared to simpler investment products?

Different Charges Levied in HDFC Life ProGrowth Plus

Like all other conventional ULIPs, HDFC Life ProGrowth Plus packs pretty heavy charges.

Premium Allocation Charge: A percentage of charge levied on the premium based on the year of allocation.

For HDFC Life ProGrowth Plus: it is fixed at 2.5% of Premium for the first year and at 2% for the second year of the policy. Your premium will be invested in units only after the deduction of Premium Allocation Charge.

Premium allocation charge is one of the most overlooked HDFC Life ULIP charges, despite directly reducing the amount available for investment from day one.

Policy Administration Charge: A charge levied for the administration of your insurance policy. It will be deducted on a monthly basis.

If you can notice, the policy administration charge gets doubled after the 5th year and charged the same till the end of policy term.

Mortality/Risk Charge: It is the charge taken from your investments to provide you the death cover. Risk charge will be higher for higher Sum Assured and the age of policy holder.

Fund Management Charge: A charge levied for the management expenses of your investments.

For HDFC Life ProGrowth Plus: The Fund Management Charge shown in the illustration is increasing year after. In the example, fund management charge is increased 12 times by the end 10th year.

It is similar to the ‘expense ratio’ of mutual funds, although an expense ratio is not a fixed charge but a part of the returns earned.

See the image below for the different rate of these charges in the HDFC Life ProGrowth Plus. In addition to these charges, the HDFC Life ProGrowth Plus also demands a fee for providing other available services at Policyholder’s request.

In addition to these charges, the HDFC Life ProGrowth Plus also demands a fee for providing other available services at Policyholder’s request.

Switching Charge: A charge levied for the purpose of switching between funds at the request of the insured.

Premium Redirection Charge: It is the charge levied to redirect the upcoming premium payments to a different fund than the current one at the request of insured.

Premium redirection in ULIPs can help investors rebalance portfolios, but repeated changes may complicate long-term fund strategy.

Partial Withdrawal Charge: This charge will be levied at every request of a partial withdrawal when the policy is active.

All three types of these charges are priced at ₹250 per request or ₹25, if the request is made through online service.

Miscellaneous Charges: Any policy alteration request or any other administrative servicing will be levied a miscellaneous charge of ₹250 per request.

Investors should also understand ULIP discontinued charges and discontinuance charges in ULIP policies before surrendering or stopping premiums midway through the lock-in period.

Charges like these are hidden in plain sight in every other insurance-cum-investment plans. It is even more absurd to levy charges on the premium amount itself rather than on the ‘investment’ returns, even though life cover is provided from the NAV of units.

Even features like settlement option, partial withdrawal, and fund switching in ULIP plans often come with conditions that are not immediately obvious during policy purchase.

Read these “Unpleasant Facts about Investing in Insurance Plans” where we have broken down the truths into fact pieces with examples.

Is It a Reasonable Trade-Off or a Hook?

It is the common rationalization among the ULIP investors.

Every ULIP investor is aware of the fact that ULIPs, at best, give lesser returns than Mutual Funds which give 12%-15% at average.

Yet, they deliberately choose ULIPs over Mutual Funds sighting reasons that the 4%-5% lag in return is a fair trade-off for the insurance benefits. But are they fair enough?

This is one of the most common arguments made by investors comparing HDFC Life ProGrowth Plus returns with mutual fund investments and direct equity-linked options.

In the table above, if you could notice, the annualized return rate shown is for the “Investment” and not the “Premium” paid by the insured.

If we see the return rate in the context of the charges levied on the ULIP premium, the return on ULIP investments will further go down.

However, even with all of the charges involved, one can very well argue that HDFC Life ProGrowth Plus provides tax benefits.

Is HDFC Life ProGrowth Plus Really Tax Free?

On the outside, yes, it does provide tax exemptions under two different sections.

Policy holders are allowed as Income tax exemption of up to ₹1.5 lakhs per annum under section 80C for payment towards premium.

Dissecting 80C Tax Exemption:

ULIPs—like HDFC Life ProGrowth Plus—are not the only tax-saving investment instruments. There are several investment instruments such as PPF, ELSS Mutual Funds, NSCs, FDs and all forms of Life Insurances provide the same tax-benefits.

Among these, PPF has the highest lock-in period of 15 years while ELSS has the minimum at 3 years. Others like FDs, POTD (Post Office Time Deposit) including ULIPs have a lock-in period of 5 years.

On head-to-head comparison, In all of the factors considered, an ELSS funds outshine the HDFC Life ProGrowth Plus.

In all of the factors considered, an ELSS funds outshine the HDFC Life ProGrowth Plus.

Even investors reviewing HDFC ULIP returns in 5 years often realize that tax-saving alone cannot compensate for lower long-term growth and high ULIP charges.

18% GST on Charges: Even though HDFC Life ProGrowth Plus claims to give tax benefits on premium amount, it is not entirely tax free.

See the illustration table of Ashwin’s policy shown above. In the first year, the charges amount to ₹7829; and for this amount an 18% of GST is levied which will also be paid from the premium amount. In total ₹9238 of Ashwin’s premium is lost in the form of charges and taxes.

Also, as seen before, the policy administration charge and the Fund Management Charge are increasing year after year till the end of policy term.

However, the benefits—on death or on maturity—are exempted from income tax under section 10(10D) of income tax act while ELSS returns aren’t.

Is the benefit of HDFC Life ProGrowth Plus tax free?

Dissecting 10(10D) Tax Exemption:

Short answer is yes—but you will be making a blind compromise.

The Income Tax Department of India allows tax exemptions on the ULIP maturity under 10(10D) only on satisfying a condition.

That is, the premium to be paid has to be 10% or lesser than the Sum Assured as benefit. Due to this, the insurer will be forced to charge a higher amount as risk charge—which is usually close to the premium paid in a term insurance plan.

In turn, your investment capital in the ULIP funds is reduced. This will put restriction on the returns potential of HDFC Life ProGrowth Plus.

This structure is common across many ULIP plans, including HDFC Life ProGrowth Flexi and similar market-linked insurance products.

On the other hand, ELSS funds are levied LTCG tax of 10% for withdrawal only greater than ₹1 lakh per annum, any amount less than that is completely exempted from tax.

With a planned withdrawal strategy, one can avoid unnecessary LTCG taxation and still reap the higher return rate of mutual funds.

HDFC Life ProGrowth Plus Lock-In Period and Liquidity

HDFC Life ProGrowth Plus comes with a mandatory 5-year lock-in period, similar to other ULIP plans.

During this period, investors cannot freely access their money, and early discontinuation attracts discontinuance charges in ULIP.

Although HDFC Life ProGrowth Plus withdrawal after 5 years is allowed, liquidity still remains limited compared to mutual funds.

Features like premium redirection in ULIPs and settlement option offer flexibility, but they do not eliminate the long-term lock-in restrictions associated with ULIP plans.

How to Cancel HDFC Life ProGrowth Plus?

Any decision to buy a ULIP has to be made after extensive research. However, to prevent (or fix) mis-selling of insurance policies, IRDAI allows policy holders to cancel their policy during the ‘free-look period’, which is 15 days from the receipt of policy.

Cancelling of HDFC Life ProGrowth Plus during the free-look period should incur no charges. The premium paid will be refunded to the insured excluding stamp duty charges and medical examination charges if any.

Cancelling HDFC Life ProGrowth Plus After Free-Look Period:

Once the free-look period is over, the procedure to cancel the HDFC Life ProGrowth Plus is not the same.

Since the HDFC Life ProGrowth Plus has a 5-year lock-in period, you cannot claim any benefit until the policy completes the lock-in period.

But, during this period, you are allowed to discontinue your policy and stop premium payment. However, a discontinuation charge will be levied based on the policy year.

Discontinuance Charges: In case of you decide to discontinue your insurance policy within the first 4 years; you will be required to pay discontinuance charge as prescribed by IRDAI.

See the image below for the discontinuance charges in HDFC Life ProGrowth Plus. It you are in the initial years of your HDFC Life ProGrowth Plus, it is not too late for you to switch to better investment instruments. You can download this HDFC ProGrowth Plus PDF here to cancel the policy and restructure your portfolio.

It you are in the initial years of your HDFC Life ProGrowth Plus, it is not too late for you to switch to better investment instruments. You can download this HDFC ProGrowth Plus PDF here to cancel the policy and restructure your portfolio.

Also, your life cover benefits of HDFC Life ProGrowth Plus will be ceased the moment you submit your discontinuance request. Hence it is advisable to make sure you have your life insurance taken care of, before you surrender your HDFC Life ProGrowth Plus.

Red Flags in HDFC Life ProGrowth Plus

In this review of HDFC ProGrowth Plus, we have analysed different facets of the ULIP.

Here’s a summary of all the red flags warning you why you shouldn’t invest in HDFC Life ProGrowth Plus:

- Reduction in investment capital since premium is invested only after Premium Allocation Charge.

- Section 10(10D) in context with 80C (3) of Income Tax Act, 1961 restricts the returns potential of investments in HDFC Life ProGrowth Plus.

- HDFC ProGrowth Plus investments are in no way regulated by SEBI, hence no strict guidelines to manage investment risks.

- Policy Administration Charge and Fund Management Charge are increasing year after year till policy maturity.

- All the Charges are subject to GST of 18% every year.

- Lack of investment transparency restricts investors from reviewing fund performance and making appropriate investment decisions.

- 5 Year lock-in and long policy term will put no compulsion on fund manager to yield consistent higher returns, which is common with mutual funds.

- Unlike mutual funds, HDFC Life ULIP fund performance sheets and fund fact sheets are not always easy for retail investors to interpret independently.

- You are restricted to only 8 fund options, which are not even listed in any stock exchange.

- Even premium redirection and fund switching flexibility cannot fully compensate for the limited investment universe available within most ULIP plans.

- From the Insurance Perspective: Life Cover is too low compared to a term insurance plan from HDFC Life itself for almost same amount of risk charge.

- From the Investment Perspective: You will have to face a 5-year lock-in and illiquidity of your investments until maturity for a post-tax return of around 6-8% at best.

- This becomes more concerning when compared against diversified equity investments capable of generating inflation-beating returns over the same time period.

- On any given circumstances, you are your nominee will receive only the Fund Value OR the Sum Assured respectively.

- But with a separate Term insurance and Mutual fund/PPF investment combo, your family will receive both the insurance benefits AND the Investment returns in case of your demise.

Verdict

HDFC Life ProGrowth Plus will look like a brilliant investment opportunity to uninformed investors conditioned for Endowment plans. But, it fails to deliver both as an insurance plan and as an investment.

A simple term insurance and mutual fund investment strategy has been proven to fetch greater benefit than HDFC Life ProGrowth Plus while also giving tax-benefits.

For investors evaluating ULIP plans from HDFC Life, separating insurance and investments continues to remain the more cost-efficient and transparent approach.

It certainly is Not Worthwhile to Invest in HDFC Life ProGrowth Plus. Life insurance decisions itself are important life decisions. Even a micro mistake will prove to be too expensive.

What are your thoughts on investing in ULIPs? Tell us in the comments section below. If you find this review of HDFC Life ProGrowth Plus helpful, share it on Facebook and other platforms to bring about awareness among your social circle.

If you have any comments or questions, write them in the comment box below.

Or are you interested in creating a Comprehensive Financial Plan for your financial goals?

Skip the queue by registering for your 30 Minute FREE Financial Plan Consultation. Click the ‘‘BOOK YOUR SLOT NOW!’’ button below.

Very poor policy I paid 6 lac yearly one lac after 6 th year policy value only 58000

Very poor policy I paid 1 lac per year and paid 6 lacks after 6 years it’s only 580000 so many charges

I have taken a policy in April 2017 and the lock in period ends in April 2022. Kindly suggest me whether I have to wait till the end or close the policy. Which is beneficial to me. Please advise

Since you have already taken this insurance plan, then you have two options.

Option: 1 You can surrender and encash the policy. And reinvest the surrender value and future premium money with better investment plans like PPF or MF.

Option: 2 You can continue with the insurance plan until the policy matures.

It is advisable to work out the outcome of both options and proceed with the better option.

80% of the time, option 1 is better.

You can consult a financial planner to choose the better option.

Or

You can take advantage of our free complimentary financial plan consultation and talk to our financial planners.

Get your appointment here: https://www.holisticinvestment.in/complimentary-financial-plan-consultation/

WORST INVESTMENT.MONTHLY CHARGES EAT UP SO MUCH.VERY POOR RETURNS.NOT AT ALL DESIGNED TO BE PROCUSTOMER, PROINVESTOR.

Thanks for sharing this impressive blog.

You are welcome

You are welcome.

Hi, I have been sold Progrowth plus yesterday and I have made the payment today. After reading all the reviews and the documents which have been shared with me online, i have realized that its completely different from what i have been told during the time of selling this policy. I would like to cancel the policy immediately, what is the process.

You can watch the video to know the process.

https://youtu.be/K8rFZLwHjcc

Sir , Currently I am in my 3 rd year of the said plan (15years) . After your detailed explanation I decided to discontinue the policy. Now If I do so when My amount would get back to me.

Immediately after the end of your lock-in period.

I have purchased HDFC Life ProGrowth Plus this year. I cannot discontinue it for 5 years now but what if I stop paying the annual premium from the second year onwards.

Please check with your financial planner.

You can also book a slot with our financial planner for an initial complimentary consultation.

https://www.holisticinvestment.in/complimentary-financial-plan-consultation/

If my policy is discontinued. And after lock in period if i apply for refund. How much TDS will be charged and on what amount?

Weather on interest only or on the total refund.

When you surrender immediately after the lock-in period is over, usually, there will not be gain and there will be loss. No tax on the loss.

In case, if there is gain, then only on that gain, the tax will be levied and not on the total amount.

The gain will be added to your income and taxed as per your tax slab.