Managing to live comfortably without regular paycheques coming in… can be a daunting proposition if not planned well in advance.

Financial security is the essence of a happy retired life.

Planning for a content retired life in itself requires careful planning.

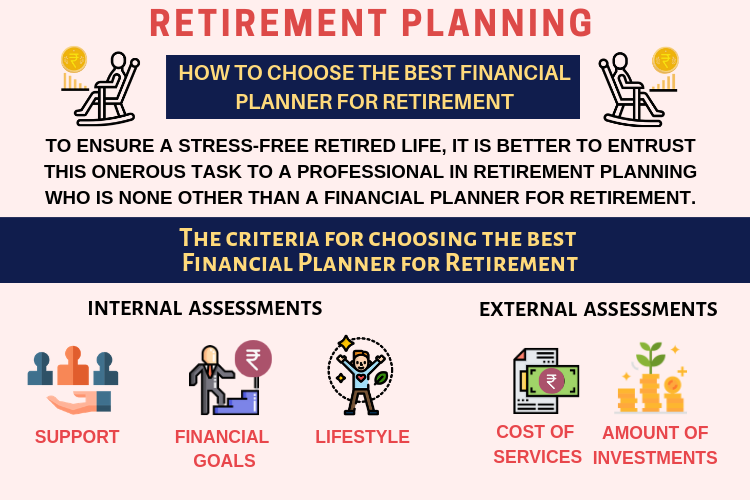

To ensure a stress-free retired life, it is better to entrust this onerous task to a professional in retirement planning who is none other than a Financial Planner for Retirement.

Table of Contents:

1. Financial Planner for Retirement

2. What are the goals of retirement planning?

3. The criteria for choosing the best Financial Planner for Retirement

4. Financial Planning for Retirees

5. A Quick checklist to select the Best Financial Planner for Retirement

6. How to find a Good Financial Planner for retirement?

Financial Planner for Retirement

Choosing a financial planner for retirement, as per your requirement and affordability, needs some guidance.

There are a lot of financial professionals who peddle their trade out there, but in order to choose the right one, it is necessary to assess a few financial planners against a set of benchmark yardsticks.

Are retirement planners worth it?

Retirement planners can be worth it for individuals seeking professional guidance, personalized advice, and peace of mind in their retirement planning journey. While there are fees or commission involved in hiring a retirement planner, the potential benefits, value, and long-term savings they can help you achieve often outweigh the costs.

By leveraging their expertise, knowledge, and resources, retirement planners can help you build a solid retirement savings plan, optimize your investment strategy, manage risks effectively, and navigate the complexities of retirement planning with confidence and ease.

They can empower you to make informed decisions, achieve your retirement goals, and enjoy a secure and comfortable retirement lifestyle.

Remember, retirement planning is a long-term journey, and having a trusted partner by your side can make a significant difference in achieving your retirement dreams and aspirations.

If you’re considering hiring a retirement planner, do your research, ask questions, and choose a planner who aligns with your values, goals, and needs.

What are the goals of retirement planning?

Why retirement planning? The goals of retirement planning encompass financial security, lifestyle maintenance, wealth preservation, legacy planning, risk management, and peace of mind.

By setting clear retirement goals, creating a personalized retirement plan, implementing sound financial strategies, and regularly reviewing and adjusting your plan as needed, retirement planning helps you achieve a comfortable, secure, and fulfilling retirement that aligns with your values, aspirations, and dreams.

The criteria for choosing the best Financial Planner for Retirement

Whom should you consult for retirement planning?

The selection could be done on the basis of a two-way analysis. One would be internal and the other external.

- The internal part would involve an objective assessment of individual requirements.

- The external one would be about deciding a set of the criteria on which each prospective financial planner for retirement would be assessed

Internal Assessments

The following internal queries may be deliberated and decided upon beforehand so that there is no ambiguity while assessing prospective financial planners for retirement:

1. Find out the type of support you need: Regular or Need-based?

It is good to have a clear idea about the specific requirements that need to be addressed post-retirement.

For some people, it would be fine to have a financial roadmap for a period of say 5 to 10 years from the date of retirement in the beginning. In such a case, the professional charges of the financial planner for retirement would be one-time to start with.

Instead, if there are issues which need detailed planning and monitoring on a regular basis, the charges could be based on the number of sessions which the financial planner has to devote.

2. Spell out the financial goals to fulfill after retirement.

Before embarking on the quest for the perfect financial plan it is imperative that the major financial responsibilities and goals be documented. The financial planner for retirement will need all the inputs in order to draw up the best plan. It is possible that at the time of retirement an individual has an outstanding home loan and money needs to be set aside for children’s higher education and/or marriage. In such a case, the financial planner for retirement will take all of these into account to draw up a time-bound plan.

3. Decide the kind of lifestyle to be maintained.

Deciding on the lifestyle requirements post-retirement is one of the most important parameters for computing the monthly income requirement.

Post-retirement, you may have some regular pilgrimage trips and frequent visits to relative’s places. This may increase your travel cost.

Similar other needs like tour, entertainment, dining outside and hosting parties/events need a re-look.

External Assessments

Here are a few useful queries which will help you to identify the best available financial planner for retirement:

1. Are they fiduciary?

A fiduciary must have the best interest of his or her clients in mind. In general, three types of financial advisors are seen to operate: The commission-based financial advisor, the fee-based financial advisor, and the fee-only financial advisor.

It is the last category of advisor or financial planner that a retiring individual so looks up to for doing the retirement plan. As the name signifies, the first two categories of advisors or agents look to sell insurance and other financial products for which they receive a commission or fee and hence they will always operate with a bias. So even if the ‘fee-only’ financial advisor is more expensive it is important to seek their advice.

2. How much will they charge for their services?

The cost of services provided is one very important factor for deciding upon a particular financial planner for retirement.

Some planners only recommend and advise on what to buy or sell, and there are others who help to do the same on behalf of their clients.

A professional financial planner for retirement will take care of

- Assessing the post retirement income required.

- Computing the corpus required to take care of inflation adjusted post retirement income for the individual and his/ her spouse till their life expectancy.

- Creating the plan to accumulate the retirement corpus

- Identifying investment schemes with tax efficiency for pre-retirement phase and post retirement phase

- Health insurance requirements before and after retirement

Each type and form of service has a different cost and the same should be looked into carefully before arriving at a decision.

3. What kind of clients have they been servicing?

If the financial planner is an expert on retirement planning then he is best suited for the purpose and his work portfolio will go a long way in boosting a prospective client’s confidence.

Working with different kind of retirees, for example, there are many who are extremely risk averse at the point of superannuation, trying to protect all their hard-earned money gathered during the lifetime. In such cases, the financial planner has to draw up a plan, which might not be great on returns but will be safe.

Again there are some who would keep a major part parked in safe options while utilizing a portion to see if the returns are good. The financial advisor in each case needs to find out the preferences and work accordingly.

4. What is the average amount of investments handled?

The spread of investment, the highest and the lowest would give a fair idea as to the exposure of the particular planner in handling large to small investments. In all likelihood, most retiring individuals would prefer to be somewhere in the middle.

5. What kind of investment strategy do they propose to apply?

All retirees should allow the financial planner for retirement to give their pitch.

- A simple question like “what kind of investment strategy do you choose for different clients?” will do the trick. The financial advisor could then spell out the exact path for investments to be made, which they have in mind.

- It will also provide an insight into the returns, which the individual can look forward to in the short and long term.

- It could help in understanding how best to go about if there is a major financial commitment after retirement and how best to tackle the same.

As a client, one could then assess the inputs received and compare them with their own thoughts and ideas.

Note: With increasing life expectancy, the money received at the time of retirement should be so invested that the returns can last at least until the age of 82-85 years.

6. Why do I need to consider you as my ‘Financial Planner for Retirement’?

Asking this question to the prospective financial planner for retirement will help

- bring out the uniqueness in the prospective financial planner for retirement.

- understand their unique abilities

- Discover what they can bring to the table that others can’t.

- Get more clarity on the gamut of services

- Get better insights on the way they handle the curves and bends in the financial road ahead which could make the difference.

All factors including cost should be taken into account while weighing the decision to go or not to go with a particular financial planner for retirement.

7. Do a background check on the prospective financial planner for retirement.

Trustworthiness is a basic quality, which the financial planner for retirement needs to possess in order to qualify for handling the money for retirement. A background check is, therefore, a good idea.

- Look for people who have used their services and approach them for feedback.

- Check up on different websites that list them as consultants.

- Search and check if they have ever been blacklisted by any agency, government or otherwise, for any reason whatsoever.

The above steps will help you in finding a good financial planner for retirement.

However, before making the final choice it would be a good idea to check with peers and colleagues to see if they have used similar services and what opinion they have regarding financial planners for retirement.

Financial Planning for Retirees:

Are you thinking about financial planning after your retirement?

Financial planning for retirees and post-retirement financial planning are crucial stages in an individual’s financial journey. As you transition from earning a regular income to relying on your savings and investments, it’s essential to have a well-thought-out financial plan to ensure financial security, peace of mind, and a comfortable retirement lifestyle.

Financial planning for retirees and after retirement is a continuous process that requires careful planning, monitoring, and adjustments to ensure financial security, sustainability, and a comfortable lifestyle throughout your retirement years.

By assessing your retirement income and expenses, creating a retirement budget, managing and optimizing investments, planning for healthcare and insurance needs, and engaging in estate and legacy planning, you can develop a comprehensive and robust financial plan tailored to your unique needs, goals, and preferences.

Remember, retirement is not the end but a new beginning, offering opportunities to pursue passions, hobbies, and dreams while enjoying a well-deserved break from the hustle and bustle of daily life. With proper financial planning and discipline, you can embrace retirement with confidence, peace of mind, and optimism for the future.

A Quick checklist to select the Best Financial Planner for Retirement

Give your Rating for financial planners in a scale of 0 to 100 to the below-mentioned questions.

1. Will the Financial Planner work on the best interest of you?

Your Rating = ?

2. Do you think this financial planning offer is worth the cost?

Your Rating = ?

3. Is the financial planner an expert in handling the clients similar to your Age & Income?

Your Rating = ?

4. Is the financial planner an expert with reference to the average amount of investments handled similarly to yours?

Your Rating = ?

5. How suitable is the investment strategy proposed by the financial planner?

Your Rating = ?

6. How is this Financial Planner a better choice comparatively?

Your Rating = ?

7. How satisfied are you with your background check on the financial planner for retirement?

Your Rating = ?

Use the Rating Questions above to choose the best financial planner for Retirement from your list of financial planners.

Financial Planners with an average ratings of above 70 can be chosen for your retirement planning.

How to find a Good Financial Planner for retirement?

How to pick a financial planner for retirement?

Here’s how you can find a good financial planner for retirement:

1. Define Your Needs and Goals:

- Before searching for a planner, identify your specific retirement goals and financial needs. What kind of lifestyle do you envision? What income sources do you have (Social Security, pensions, investments)?

- Knowing your priorities will help you find a planner with the right expertise.

2. Ask for Referrals:

Talk to friends, family, colleagues, or your current financial advisor (if you have one) for recommendations. People you trust who have had positive experiences with a planner are a great starting point.

3. Research and Interview Candidates:

- Look for planners with experience specializing in retirement planning. Certifications like CFP® (Certified Financial Planner™) indicate expertise.

- Use online directories like the CFP Board’s planner search tool to find qualified professionals in your area.

4. Consider Fees and Services:

- Financial planners charge fees in various ways, such as hourly rates, a percentage of assets under management (AUM), or flat retainer fees. Understand the fee structure upfront and ensure it aligns with your budget.

- Ask about the services included for the fee. Do they create a personalized plan, offer ongoing investment management, or focus solely on retirement income planning?

5. Conduct Initial Interviews:

- Schedule consultations with a few shortlisted planners. This initial meeting is a chance for you to assess their communication style, investment philosophy, and fit with your personality.

- Prepare questions beforehand to understand their approach to retirement planning, experience with clients in similar situations, and how they handle potential conflicts of interest.

6. Ask About Fiduciary Duty:

A crucial aspect is the planner’s legal obligation. Look for a planner who acts as a fiduciary, meaning they are legally bound to act in your best interests ahead of their own.

7. Check Background and Credentials:

Verify the planner’s credentials and any disciplinary history using resources. Consider the experience and expertise of the financial planner in retirement planning. Look for a planner with a proven track record of helping clients achieve their retirement goals and navigate complex financial challenges during retirement.

8. Make an Informed Decision:

Don’t feel pressured to choose the first planner you meet. Take your time, compare options, and choose someone you feel comfortable trusting with your financial future.

Bonus Tip:

Consider attending seminars or workshops on retirement planning hosted by financial institutions or local organizations. This can be a great way to learn more about the process and potentially meet planners who specialize in retirement.

By following these steps, you can increase your chances of finding a qualified and trustworthy financial planner to guide you on your retirement journey.

Conclusion

A good financial planner for retirement can make a world of difference by ensuring that the days of your retirement are spent peacefully without having to worry about regular cash flow.

The earlier one starts to plan for retirement, the better.

However, it is never too late to start.

But, it will be too late if one does not start at all.

Kindly write your comments, and also spread the valuable information by sharing with your family and friends.

Related Articles:

Revealed: Are Financial Planners worth the cost?

99% of investors are not with the right Investment Planners. What about you?

If you have any comments or questions, write them in the comment box below.

Or are you interested in creating a Comprehensive Financial Plan for your financial goals?

Skip the queue by registering for your 30 Minute FREE Financial Plan Consultation. Click the ‘‘BOOK YOUR SLOT NOW!’’ button below.

Thanks for the tip about finding a financial planner who can offer you guidance. It would be smart to check with their past clients to know how qualified they are as well. My husband and I are looking for a retirement planner, so we’ll have to make sure they are qualified first.

Yes Katie, You are right. That is why we have covered that in detail in the 7th point of external assessment.

Good article very informative. Thanks, Holistic.

Thanks Vikky

Good post

Thanks

Informative blog.

Hope that information is useful to you…

More useful Article.

I am happy that you found it useful

Very nice Article

Thanks Dhayalan for your appreciation

I am happy to have visited your website. Your website articles cover the subject indepth and at the same time explains everything in a simple lucid language.

Thanks. We take conscious effort to write it in-depth and in lucid language. Really happy that you liked that.

Thank you for writing.

It is always a pleasure to write for our readers like you.

Good post

Thanks Sankar for your feedback.

I always read all of your articles. They are really useful. You guys are doing great job.

Thanks for your appreciation. It means a lot.