Table of Content:

What is SBI Life Smart Power Insurance Plan?

- Trigger Fund Option of SBI Life Smart Power Insurance

- Smart Fund Option of SBI Life Smart Power Insurance

Features of SBI Life Smart Power Insurance Plan

Who Can Purchase SBI Life Smart Power Insurance Plan?

SBI Life Smart Power Insurance Plan: Plan Options

Investment Funds of SBI Life Smart Power Insurance

- Flexible Option

- Switching Option

- Premium Redirection Option

- Portfolio Transfer Option

- Partial Withdrawals

- Settlement Option

Benefits of SBI Life Smart Power Insurance Plan

Charges of SBI Life Smart Power Insurance Plan

- Premium Allocation Charge

- Policy Administration Charge

- Fund Management Charge

- Discontinuance Charge

- Mortality Charge

- Accelerated Total & Permanent Disability Charge

- Switching Charge

- Premium Redirection Charge

- Partial Withdrawal Charge

- Medical Expenses on Revival

Research Methodology of SBI Life Smart Power Insurance Plan

SBI Life Smart Power Insurance Plan: Analysis with Illustration

IRR of SBI Life Smart Power Insurance Plan

SBI Life Smart Power Insurance Plan vs. PPF + Term Insurance

SBI Life Smart Power Insurance Plan vs. ELSS + Term Insurance

SBI Life Smart Power Insurance Plan: Advantages

SBI Life Smart Power Insurance Plan: Disadvantages

Surrendering/Cancelling SBI Life Smart Power Insurance Plan

What Happens If You Stop Paying Premiums in SBI Life Smart Power Insurance?

Who Should Avoid SBI Life Smart Power Insurance?

Things to Consider Before Buying SBI Life Smart Power Insurance

Final Verdict of SBI Life Smart Power Insurance (ULIP) Plan

Introduction

SBI Life Smart Power Insurance plan which is a ULIP that claims that it can help you to grow your wealth.

But will it really help you to increase your wealth in a long term?

Here’s a review of the SBI Life Smart Power Insurance Plan to discover the answer.

Many investors exploring different SBI life insurance plans or reviewing the SBI life plans list often come across the Smart Power Insurance plan as a market-linked investment option.

The plan is often evaluated by investors looking for an SBI Life Smart Power Insurance maturity calculator or SBI Life insurance calculator to estimate long-term returns before investing.

What is SBI Life Smart Power Insurance Plan?

SBI Life Smart Power Insurance plan is an individual, Unit Linked Insurance Plan (ULIP).

SBI Life Smart Power Insurance plan gives freedom to manage your own investment as per your requirements.

It offers benefits to managing the risk level in your investment portfolio against market volatility.

SBI Life Smart Power Insurance plan offers flexibility to choose between two investment strategy options and multiple fund choices to take care of your needs.

SBI Life Smart Power Insurance plan provides a liquidity option after the end of the 5th policy term.

Among the various SBI life insurance products available today, ULIP-based plans like Smart Power Insurance combine life cover with market-linked investment opportunities.

Investors comparing different SBI insurance schemes or SBI insurance plans often consider this ULIP for its combination of investment flexibility and life cover.

SBI Life Smart Power Insurance has two fund options.

- Trigger Fund Option

- Smart Fund Option

Trigger Fund Option of SBI Life Smart Power Insurance:

Based on the investment philosophy “buy low…sell high”, this option can help to take advantage of the equity market to gain a return.

This strategy aims to benefit from market movements, which is why many investors evaluating SBI life investment plans consider trigger-based investment options for long-term wealth creation.

The Trigger Fund Option is designed for investors who want to benefit from market cycles while investing through an SBI Life ULIP plan.

Smart Fund Option of SBI Life Smart Power Insurance:

In this option, you can choose your own asset allocation from the 10 funds provided by SBI Life Smart Power Insurance Plan.

This flexibility is designed for policyholders who want to manage their own portfolio allocation while investing through SBI life ULIP plans.

Policyholders looking for greater control over asset allocation often prefer this option while reviewing SBI Life Smart Power Insurance level cover and increasing cover variants.

Features of SBI Life Smart Power Insurance plan:

- Option to choose between Level Cover Option and Increasing Cover Option in two plan options.

- The Inbuilt Accelerated Total & Permanent Disability (TPD) benefit allows you to advance the Policy Benefit to become your Living Benefit.

- Option to choose between two fund options Trigger fund option and Smart Fund Option.

- Flexibility is provided by 2 free switches.

- Liquidity in partial withdrawal.

These features are commonly highlighted when comparing different SBI insurance plans and understanding the benefits offered by modern market-linked policies.

The availability of SBI Life Smart Power Insurance Level Cover and SBI Life Smart Power Insurance Increasing Cover allows investors to choose protection based on their financial responsibilities.

Who can Purchase SBI Life Smart Power Insurance Plan?

Under both options, the Sum Assured will not exceed Rs. 50, 00, 000

Eligibility criteria and policy limits may vary depending on the policy term selected, which is why many investors review SBI life insurance plan details carefully before purchasing a policy.

SBI Life Smart Power Insurance Plan: Plan Options

The Smart Power Insurance policy allows investors to select between the SBI Life Smart Power Insurance level cover and increasing cover options depending on their protection requirements.

Investment Funds of SBI Life Smart Power Insurance:

Investment funds play a crucial role in determining the long-term performance of SBI life ULIP policies because returns depend largely on how these funds perform in different market conditions.

The long-term growth potential of SBI Life Smart Power Insurance depends on fund selection, market performance, and the power of compounding over the policy tenure.

Flexible Option:

Flexibility in fund allocation is one of the key reasons investors exploring SBI life investment plans prefer ULIP-based structures over traditional savings policies.

Switching Option:

Under the Smart investment option in SBI Life Smart Power Insurance, you can switch between the available 10 funds.

The minimum switch amount is Rs. 2000 and you don’t have to pay for two switches in the same policy term.

But after the third switch onwards, you need to pay Rs. 100 for every switch. Unused switches cannot be carried forward.

Fund switching helps investors adjust their portfolio strategy depending on market conditions while continuing their investment within the SBI Smart Power Insurance structure.

Premium Redirection Option:

You can redirect your premium from the 2nd premium term onwards.

You can avail of one redirect option free of cost per year among the 10 funds.

After that, you need to pay Rs. 100 for every transaction. The unused free transaction cannot be carried forward.

Premium redirection provides flexibility for policyholders who want to rebalance their investments across different SBI life ULIP funds over time.

Portfolio Transfer Option:

If you desire, you have the option to change the fund option which you had selected before to the options Trigger Fund and Smart fund.

You can write SBI Life at any policy term at least before 2 months of the policy anniversary to change the selected fund option.

This option can be used 2 times per annum. You will not be charged for the transfer option.

This portfolio transfer facility allows policyholders to shift their investment approach within the SBI life smart power insurance policy without interrupting the policy benefits.

Partial Withdrawals:

Partial withdrawals are allowed from the 6th policy term onwards.

Policyholders can avail of two partial withdrawals free of cost after that they have to Rs. 100 for every withdrawal.

The policyholder can withdraw from Rs. 2000 to 15% of the fund value.

4 partial withdrawals are allowed per year.

Overall a person can withdraw 10 times during the policy term or 15 times if the policy term exceeds more than 10 years.

Policyholders cannot withdraw if they are reduced to less than 50% of the total premium paid.

Such liquidity options are one of the factors investors evaluate when comparing SBI life insurance plans with other long-term investment products.

The five-year lock-in period is similar to most SBI Life ULIP plans, after which partial withdrawals provide greater financial flexibility.

Settlement Option:

During the settlement period, the Nominee bores the risk of Investment.

The nominee will get the death benefit within 2 to 5 years.

It will be paid as yearly, half-yearly, quarterly, or monthly pay-outs as required, from the date of death.

Settlement options in life insurance policies allow beneficiaries to receive pay-outs in structured instalments instead of a lump sum amount.

Benefits of SBI Life Smart Power Insurance Plan:

Understanding the benefits of SBI life insurance policies is important before deciding whether such plans align with long-term financial goals.

The SBI Life Smart Power Insurance benefits extend beyond life cover by offering market-linked wealth creation opportunities and flexible fund management options.

Death Benefit:

If the policyholder passes away, unfortunately, then the nominee or the legal heir will get the highest of the following as death benefit

- Fund Value as on the death of the policyholder

- Basic Sum Assured excludes partial withdrawal

- 105% of the premium term paid

This structure is commonly seen in ULIP-based life insurance products where the death benefit is linked to the fund value and insurance cover.

Settlement option:

The nominee or the legal heir can receive the death benefit over 2 to 5 years under the ‘Settlement’ Option as yearly, half-yearly, quarterly, or monthly pay-outs as required, from the date of death.

Such structured pay-out options may help beneficiaries manage the policy proceeds more efficiently over time.

In-built Option:

If the policyholder becomes permanently disabled due to illness or accident, the policyholder will get paid 100% of the death benefit and the policy will be terminated

This built-in protection feature provides additional financial support in case of severe disability during the policy term.

Maturity Benefit:

After the end of the SBI Life Smart Power Insurance policy, the policyholder will get the fund value as Lumpsum.

The final maturity value in ULIP plans depends on the performance of the underlying funds and the charges deducted during the policy tenure.

Charges of SBI Life Smart Power Insurance Plan:

Like most ULIP plans, several charges apply throughout the policy term which may influence the overall investment returns.

Premium Allocation Charge:

This charge will be deducted from the premium paid before the allocation of the units.

Premium allocation charges are applied before the premium is invested into the selected funds.

Policy Administration Charge:

The Policy Administration charge will be deducted from the term of the policy. It will be Rs. 33.33 per month.

This policy administration charge is subject to a cap of Rs. 500 per month.

Administrative charges cover the operational expenses of maintaining the policy throughout its duration.

Fund Management Charge:

A fixed percentage will be deducted from the fund value before calculating NAV.

FMC of all the funds except the discontinuance policy fund will be subject to a cap of 1.35%.

Fund management charges represent the cost of managing the investment portfolio within the ULIP structure.

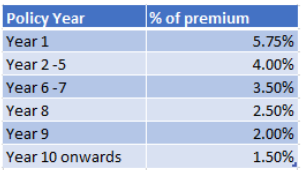

Discontinuance Charge:

This will be charged as a percentage of the annual premium or fund value.

These charges may apply if the policy is discontinued during the lock-in period.

Mortality Charge:

This charge will be deducted from the fund value on the 1st day of each policy month.

Mortality charges represent the cost of providing life insurance coverage under the policy.

Accelerated Total & Permanent Disability Charge:

This charge will be deducted from the fund value on the 1st day of every policy month. It is deducted as Rs. 0.40 per Rs. 1000 sum assured.

Such charges support the in-built disability protection available under the policy.

Switching Charge:

A charge of ₹100 is applicable for every switch, in excess of two free switches in the same policy year during the policy term or settlement period.

The switching charge is subject to a market cap of Rs. 500 per switch.

Switching charges apply when policyholders frequently change their investment funds within the policy.

Premium Redirection Charge:

The policyholder can avail of one redirection free of charge. After that, the policyholder needs to pay Rs. 100 for every redirection.

The premium redirection charge is subject to a cap of Rs. 500 per transaction.

This charge applies when the policyholder reallocates future premiums across different funds.

Partial Withdrawal Charge:

The policyholder will be charged Rs. 100 after the 2 free partial withdrawals. This Partial withdrawal charge is subject to a cap of Rs. 500.

Withdrawal charges apply when policyholders access a portion of the accumulated fund value.

Medical Expenses on Revival:

These medical expenses will be charged to the policyholder.

Medical requirements may arise when a lapsed policy is revived after the grace period.

Understanding SBI insurance charges is essential because multiple deductions over the policy term can significantly reduce the final maturity value.

Research Methodology of SBI Life Smart Power Insurance Plan:

Now, we have seen all the necessary details that we need to know about SBI Life Smart Power Insurance Plan.

Though it seems a genuine plan, still it is not enough to decide whether it is worth to invest or not.

So, now let’s see how the SBI Life Smart Power Insurance plan works.

After that, let’s analyze compared to other investments, will it really creates long-term wealth or not.

A deeper evaluation of the SBI Life Smart Power Insurance policy helps investors understand whether this market-linked insurance plan can realistically deliver long-term wealth creation compared to other investment alternatives.

Rather than relying solely on SBI Life illustration figures, evaluating the Internal Rate of Return (IRR) provides a more realistic picture of long-term investment performance.

SBI Life Smart Power Insurance Plan: Analysis with Illustration

Understanding the SBI Life Smart Power Insurance returns through an illustration helps investors evaluate how this market-linked SBI life insurance plan may perform over a long investment horizon.

IRR of SBI Life Smart Power Insurance Plan:

Now, let’s see the IRR (Internal Rate of Return) for the worst-case scenario and best-case scenario.

Investment contribution: Rs. 1, 00, 000 per annum

Premium Term: 20 years

Policy term: 20 years

The assumed gross return in the worst-case scenario is 4%.

Such projections are typically shown in the SBI life insurance calculator or policy illustration to help investors estimate the possible maturity value under different return assumptions.

While the SBI Life Smart Power Insurance maturity calculator provides projected values, the actual returns will depend on fund performance and policy charges over the investment period.

As you can see in the above illustration, in the worst-case scenario, the SBI Life Smart Power Insurance plan gives us an IRR of 1.96%.

At the end of the 20 years, the SBI Life Smart Power Insurance plan gives us the maturity benefit of Rs. 24, 66, 399 and the Death benefit of Rs. 10, 71, 790.

This example highlights how the SBI Life Smart Power Insurance maturity amount depends largely on the performance of the underlying investment funds.

Now, let’s see the best-case scenario.

The assumed gross return in the best-case scenario of the SBI Life Smart Power Insurance plan is 8%.

As you can in the above illustration, in the best-case scenario, the SBI Life Smart Power Insurance plan gives us an IRR of 5.89%.

At the end of the 20 years, the SBI Life Smart Power Insurance plan gives us the maturity benefit of Rs. 38, 47, 928 and death benefit of Rs. 13, 35, 940.

Even in a favourable scenario, the returns from this SBI life ULIP plan remain dependent on market performance and policy charges deducted during the policy term.

For investors comparing SBI Life Smart Power Insurance with other SBI Life investment plans or traditional savings products, evaluating the post-charge IRR is more meaningful than looking only at projected fund values.

Compare to other investments this SBI Life Smart Power Insurance plan neither gives us the best outcome that can beat the inflation nor a good insurance coverage.

For more clarification, let’s compare this plan with PPF and see its performance for the same 20 years.

SBI Life Smart Power Insurance Plan vs. PPF + Term Insurance:

Overall contribution: Rs. 1,00,000

Tenure: 20 years

Contribution to term insurance:

Sum Assured: Rs. 1,00,00,000

Premium term: Rs. 12,500

PPF Contribution: Rs. 87,500

Many investors exploring SBI life insurance plans for long-term savings often compare ULIP policies with traditional investment options like Public Provident Fund (PPF).

|

Term Insurance + PPF |

|||

|

Age |

Year |

Term Insurance premium + PPF |

Death benefit |

|

35 |

1 |

-1,00,000 |

1,00,00,000 |

|

36 |

2 |

-1,00,000 |

1,00,00,000 |

|

37 |

3 |

-1,00,000 |

1,00,00,000 |

|

38 |

4 |

-1,00,000 |

1,00,00,000 |

|

39 |

5 |

-1,00,000 |

1,00,00,000 |

|

40 |

6 |

-1,00,000 |

1,00,00,000 |

|

41 |

7 |

-1,00,000 |

1,00,00,000 |

|

42 |

8 |

-1,00,000 |

1,00,00,000 |

|

43 |

9 |

-1,00,000 |

1,00,00,000 |

|

44 |

10 |

-1,00,000 |

1,00,00,000 |

|

45 |

11 |

-1,00,000 |

1,00,00,000 |

|

46 |

12 |

-1,00,000 |

1,00,00,000 |

|

47 |

13 |

-1,00,000 |

1,00,00,000 |

|

48 |

14 |

-1,00,000 |

1,00,00,000 |

|

49 |

15 |

-1,00,000 |

1,00,00,000 |

|

50 |

16 |

-1,00,000 |

1,00,00,000 |

|

51 |

17 |

-1,00,000 |

1,00,00,000 |

|

52 |

18 |

-1,00,000 |

1,00,00,000 |

|

53 |

19 |

-1,00,000 |

1,00,00,000 |

|

54 |

20 |

-1,00,000 |

1,00,00,000 |

|

55 |

38,84,001 |

||

|

IRR |

5.97% |

||

Investment return: 7.10% without taking the risk.

As you can see in the above illustration, PPF gives us an IRR of 5.97%.

At the end of the 20 years, we will get Rs. 38.84 Lakhs as investment return.

PPF remains one of the most popular government-backed long-term savings schemes in India because of its guaranteed returns and tax-free maturity benefits.

Unlike many SBI insurance schemes that combine insurance with investment, PPF offers a transparent structure where returns are independent of insurance charges and market-linked fund performance.

Now compare to the SBI Life Smart Power Insurance plan, PPF gives us the same investment return without taking the risk.

|

Investment option |

Internal Rate of Return (IRR) |

Maturity benefit |

Death benefit |

|

SBI Life Smart Power – 4% Scenario |

1.96% |

24,66,999 |

10 lakhs |

|

SBI Life Smart Power – 8% Scenario |

5.89% |

38,47,928 |

10 lakhs |

|

PPF |

5.97% |

38,84,001 |

1 crore |

This comparison highlights how separating insurance and investment through a term insurance policy and PPF can sometimes offer better financial efficiency.

Many investors comparing an SBI policy plan with government-backed savings options prefer to separate insurance and investment, using a pure term plan for protection and PPF for stable long-term wealth creation.

Now, let’s compare SBI Life Smart Power Insurance Plan with ELSS.

SBI Life Smart Power Insurance Plan vs. ELSS + Term Insurance:

Overall contribution: Rs. 1,00,000

Tenure: 20 years

Contribution on term insurance:

Sum Assured: Rs. 1,00,00,000

Premium term: Rs. 12,500

ELSS Contribution: Rs. 87,500

Assumed Investment Return: 12% with risk

Equity Linked Savings Schemes (ELSS) are tax-saving mutual funds that invest primarily in equities and are known for their potential to deliver higher long-term returns.

Unlike an SBI Life ULIP plan where multiple policy charges can affect returns, ELSS investments directly participate in equity market growth with comparatively simpler cost structures.

|

Term insurance + ELSS |

|||

|

Age |

Year |

Term Insurance premium + ELSS |

Death benefit |

|

35 |

1 |

-1,00,000 |

1,00,00,000 |

|

36 |

2 |

-1,00,000 |

1,00,00,000 |

|

37 |

3 |

-1,00,000 |

1,00,00,000 |

|

38 |

4 |

-1,00,000 |

1,00,00,000 |

|

39 |

5 |

-1,00,000 |

1,00,00,000 |

|

40 |

6 |

-1,00,000 |

1,00,00,000 |

|

41 |

7 |

-1,00,000 |

1,00,00,000 |

|

42 |

8 |

-1,00,000 |

1,00,00,000 |

|

43 |

9 |

-1,00,000 |

1,00,00,000 |

|

44 |

10 |

-1,00,000 |

1,00,00,000 |

|

45 |

11 |

-1,00,000 |

1,00,00,000 |

|

46 |

12 |

-1,00,000 |

1,00,00,000 |

|

47 |

13 |

-1,00,000 |

1,00,00,000 |

|

48 |

14 |

-1,00,000 |

1,00,00,000 |

|

49 |

15 |

-1,00,000 |

1,00,00,000 |

|

50 |

16 |

-1,00,000 |

1,00,00,000 |

|

51 |

17 |

-1,00,000 |

1,00,00,000 |

|

52 |

18 |

-1,00,000 |

1,00,00,000 |

|

53 |

19 |

-1,00,000 |

1,00,00,000 |

|

54 |

20 |

-1,00,000 |

1,00,00,000 |

|

55 |

64,12,872 |

||

|

IRR |

10.14% |

||

As you can see in the above illustration, after taking risk, ELSS gives us the IRR of 10.55%.

At the end of the 20 years, it gives us Rs. 64.12 Lakhs as investment return.

Equity-based investments like ELSS have historically shown the potential to generate inflation-beating returns over long investment horizons.

|

ELSS Tax Calculation |

|

|

Maturity value after 20 years |

70,61,139 |

|

Purchase price |

17,50,000 |

|

Long-Term Capital Gains |

53,11,139 |

|

Exemption limit |

1,25,000 |

|

Taxable LTCG |

51,86,139 |

|

Tax paid on LTCG |

6,48,267 |

|

Maturity value after tax |

64,12,872 |

Now, compare to SBI Life Smart Power Insurance Plan, after taking risk, ELSS gives us inflation beating return.

|

Investment option |

Internal Rate of Return (IRR) |

Maturity benefit |

Death benefit |

|

SBI Life Smart Power – 4% Scenario |

1.96% |

24,66,999 |

10 lakhs |

|

SBI Life Smart Power – 8% Scenario |

5.89% |

38,47,928 |

10 lakhs |

|

ELSS |

10.14% |

64,12,872 |

1 crore |

This comparison clearly shows how combining term insurance with equity investments can potentially create a stronger long-term wealth strategy.

SBI Life Smart Power Insurance Plan: Advantages

Before purchasing any policy, investors usually review the advantages of SBI life insurance plans to understand the value they provide.

- There are two life cover options and a variety of fund options available for you to choose from.

- You can switch between the available 10 funds under the Smart Funds Option.

- You have the choice to choose between the Trigger Fund Option and the Smart Fund Option.

- The candidate has the option to receive the death benefit in instalments.

- During the settlement stage, switches are permitted.

- During the settlement period, no charges will be deducted except FMC and switching charges.

SBI Life Smart Power Insurance Plan: Disadvantages

Like most market-linked insurance policies, there are also certain limitations that investors should consider carefully.

- The policy holder bears the investment risk in the investment portfolio during the settlement term.

- The lock-in period is 5 years.

- During the first five years of the contract, Unit Linked Insurance products do not provide any liquidity.

- Policyholders will not be able to totally or partially surrender or withdraw funds invested in Unit Linked Insurance Products until the conclusion of the fifth year.

- The premium is invested after different costs have been deducted.

- Even though it is a hybrid insurance/investment product, neither the insurance is adequate nor does the investment serve its goal.

Surrendering/Cancelling SBI Life Smart Power Insurance Plan:

Free look period:

If you are not satisfied with any of the terms and conditions of the SBI Life Smart Power Insurance plan, then you can surrender the policy by returning the policy documents during the free look period.

The free look period is 15 days from the date of purchasing if you purchase it directly and 30 days if you purchase the SBI Life Smart Power Insurance Plan in online mode.

The free-look period allows policyholders to review the policy terms and cancel the policy if it does not meet their expectations.

Surrendering after free look period:

You can surrender the policy during any time of the policy term.

Surrendering during lock-in period:

Charges will be deducted based on the terms and conditions.

You will earn a minimum interest rate of 4% in your fund value.

The fund value will be payable on the 1st day of the 6th policy term. For more details, you can read, the SBI Life Smart Power Insurance plan brochure here.

Surrendering after lock-in period:

You will get paid the fund value immediately.

What Happens If You Stop Paying Premiums in SBI Life Smart Power Insurance?

If premiums are discontinued in SBI Life Smart Power Insurance during the mandatory five-year lock-in period, the policy does not immediately lapse.

The fund value, after applicable discontinuance charges, is moved to a discontinued policy fund and remains there until the lock-in period ends.

Once the five years are completed, the remaining fund value can be withdrawn.

However, the life cover under SBI Life Smart Power Insurance typically ceases after the policy is discontinued.

This makes it important for investors to view the policy as a long-term commitment and ensure premiums can be sustained throughout the intended investment period.

Investors considering SBI Life insurance yearly plans or long-term premium commitments should evaluate affordability carefully, as discontinuing premiums midway can reduce the overall effectiveness of the investment strategy.

Who Should Avoid SBI Life Smart Power Insurance?

While SBI Life Smart Power Insurance offers both investment and insurance benefits, it may not suit every investor.

Individuals looking for short-term investment options or liquidity within a few years may find the five-year lock-in period restrictive.

Similarly, investors who prefer simple and transparent investment structures may find ULIPs more complex compared to standalone investment options and pure term insurance.

Those who are uncomfortable with market-linked fluctuations in fund value may also need to carefully evaluate whether this policy aligns with their risk tolerance.

Things to Consider Before Buying SBI Life Smart Power Insurance

Before investing in SBI Life Smart Power Insurance, consider your investment horizon, risk appetite, liquidity needs, and long-term financial goals.

Since it is a market-linked ULIP with a five-year lock-in period, returns are not guaranteed and are influenced by fund performance and various policy charges.

It is also advisable to compare the plan with alternatives such as a pure term insurance policy combined with PPF or mutual funds.

Evaluating the expected IRR, insurance coverage, charges, and inflation-adjusted returns can help determine whether the policy is suitable for your wealth creation objectives.

Final Verdict of SBI Life Smart Power Insurance (ULIP) plan:

Like any other ULIP plan, this SBI Life Smart Power Insurance plan is no different from others.

Even after taking a risk, it gives us a return that can barely beat inflation.

On the other side, it has a lock-in period of 5 years which offers no liquidity.

Many investors evaluating SBI life investment plans eventually realize that combining pure term insurance with separate investments can provide better financial outcomes.

So, if the policy holder meets any misfortune during this time, he cannot get any benefit.

So, this SBI Life Smart Power Insurance plan does not really help you to grow your wealth in the long term.

If you don’t want to take any risk, then you can choose PPF and Term Insurance combination to create long-term wealth.

Or you can go for ELSS (mutual fund) and term insurance combination to create a long-term wealth after taking a risk.

A well-structured financial strategy focuses on adequate life insurance protection along with diversified investments for long-term wealth creation.

Whether reviewing SBI Life Smart Power Insurance level cover, increasing cover, or other SBI Life plans, investors should evaluate inflation-adjusted returns, insurance adequacy, liquidity, and overall cost before making a long-term financial commitment.

If you have any comments or questions, write them in the comment box below.

Or are you interested in creating a Comprehensive Financial Plan for your financial goals?

Skip the queue by registering for your 30 Minute FREE Financial Plan Consultation. Click the ‘Register Now!’ button below.

Leave a Reply